|

시장보고서

상품코드

2059964

절제 기술 시장 예측(-2031년) : 기술(고주파, 초음파, 마이크로파, 레이저, 냉동절제, 펄스 필드), 제품(시스템, 소모품), 용도(순환기, 암, 비뇨기), 최종사용자별(병원, 외래 수술 센터)Ablation Technology Market by Technology (Radiofrequency, Ultrasound, Microwave, Laser, Cryoablation, Pulse-field), Product (Systems, Consumables), Application (Cardiovascular, Cancer, Urological), End User (Hospitals, ASC) - Global Forecasts to 2031 |

||||||

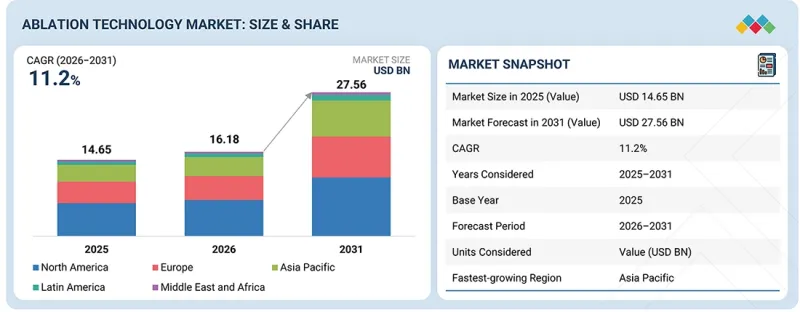

절제 기술 시장 규모는 2026년 161억 8,000만 달러에서 2031년에는 275억 6,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR은 11.2%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 기술, 제품, 용도, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

심혈관 질환, 암, 만성 통증, 부인과 질환 등 만성질환의 증가에 따라 절제술 기술에 대한 수요가 크게 증가하고 있습니다. 만성질환의 유병률 증가는 최소 침습 수술의 보급률을 더욱 높일 것으로 예상됩니다. 기존 수술법보다 저침습 수술이 선호되는 경향은 시장에서의 중요한 요인으로 작용하고 있습니다. 이는 입원 기간 단축, 빠른 회복, 통증 완화, 합병증 발생 위험 감소, 흉터 감소 등 절제술에 따른 장점 덕분입니다. 또한 전 세계에서 고령 인구가 증가하고 있는 점도 환자층의 확대로 이어지고 있습니다. 고주파 절제술, 마이크로파 절제술, 냉동 절제술, 레이저 절제술, 펄스 전기장 절제술술 분야의 기술 혁신을 통해 시술의 안전성과 정확성이 보장되고 있습니다.

“제품별로는 소모품 부문이 절삭 기술 시장을 주도할 것으로 전망된다”

제품 카테고리별로 보면 소모품 카테고리가 가장 큰 시장 점유율을 차지하고 있습니다. 이는 순환기, 종양, 통증 관리, 산부인과 등 다양한 의료 분야에서 절제술 시술시 이러한 제품의 사용이 증가하고 있기 때문입니다. 카테터, 전극, 프로브, 바늘, 일회용 제품 등은 절제술시 항상 사용되는 필수적인 구성 요소이며, 그 결과 병원, 수술 센터, 절제술 전문 클리닉에서 이러한 제품에 대한 수요는 안정적으로 유지되고 있습니다. 저침습적 절제술의 증가로 인해 이러한 일회용 제품에 대한 수요가 크게 증가하고 있습니다.

"최종사용자별로는 병원·수술 센터·절제 센터가 가장 큰 시장 점유율을 차지할 것으로 전망된다"

이는 해당 시설에서 시행되는 절제술 건수가 많고, 또한 첨단 의료 설비가 갖춰져 있기 때문입니다. 이러한 의료기관에는 특수 수술실, 최신 영상 진단 및 내비게이션 기술, 심혈관 질환, 암, 만성 통증, 부인과 질환과 관련된 복잡한 절제술을 시행할 수 있는 첨단 자격을 갖춘 의료진이 배치되어 있습니다. 병원이나 전문 절제술 센터는 포괄적인 의료 서비스와 시설을 제공하므로 환자들 사이에서 가장 인기가 높습니다.

"북미의 절삭 기술 시장에서 미국은 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망된다"

미국에서는 심장병, 암, 만성 통증, 심방세동 등 다양한 만성질환의 유병률이 증가하고 있으며, 최소 침습 수술에 대한 필요성이 높아지고 있으며, 북미의 절제술 기술 시장에서 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 또한 미국에는 고도로 발달된 의료제도가 있으며, 최신 기술 도입률이 높고, 절제 기기 분야에서 지속적으로 연구개발에 투자하고 있는 주요 기업이 있습니다. 저침습 수술에 대한 선호도 증가, 고령화, 인식 제고 역시 시장을 촉진하고 있습니다.

이 보고서에서는 전 세계 절삭 기술 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 절제 기술 시장 : 유형별

제10장 절제 기술 시장 : 제품별

제11장 절제 기술 시장 : 용도별

제12장 절제 기술 시장 : 최종사용자별

제13장 절제 기술 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

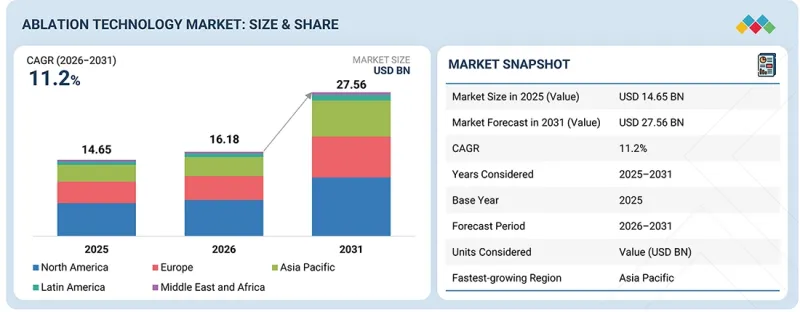

KSA 26.06.25The ablation technology market is projected to reach USD 27.56 billion by 2031 from USD 16.18 billion in 2026, at a CAGR of 11.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Technology, Product, Application, End User, and Region |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa, GCC Countries |

There has been a huge demand for ablation technology due to an increasing number of chronic diseases, such as cardiovascular diseases, cancer, chronic pain, and gynecological diseases. The growing incidence of chronic diseases is expected to fuel the adoption rate of minimally invasive procedures. The preference for minimally invasive surgery over the traditional surgical method is a significant factor in the market. It can be credited to the benefits associated with ablation, including shorter hospital stay, quick recovery, low pain, low risks of developing complications, and reduced scarring. In addition to that, the increasing population of the geriatric segment across the globe is increasing the patient pool. Innovation in radiofrequency ablation, microwave ablation, cryoablation, laser ablation, and pulsed field ablation is ensuring procedural safety and accuracy.

"By product, the consumables segment is expected to lead the ablation technology market."

The consumables category has the largest market share in the product category of ablation technologies, owing to the increasing use of these products in performing ablation procedures for different medical applications, such as cardiology, oncology, pain management, and gynecology. Products such as catheters, electrodes, probes, needles, and disposables are essential components consistently utilized in ablation procedures, resulting in a steady demand for these items from hospitals, surgery centers, and ablation clinics. The rising number of minimally invasive ablation procedures has created a huge demand for these disposables.

"By end user, the hospitals, surgical centers, and ablation centers segment is estimated to account for the largest share of the ablation technology market."

By end user, hospitals, surgery centers, and ablation centers account for the largest share of the ablation technology market due to the high volume of ablation treatments performed in these institutions, as well as the availability of advanced healthcare facilities. Such healthcare institutions are equipped with special operation theaters, modern imaging and navigation technologies, and highly qualified healthcare personnel to perform complicated ablations in connection with cardiovascular diseases, cancer, chronic pain, and gynecological conditions. Hospitals and specialized ablation centers are most popular among patients due to the provision of complete healthcare services and facilities.

"The US is expected to register the highest CAGR in the North America ablation technology market."

The US is anticipated to register the highest CAGR in the ablation technology market in North America because of the increasing prevalence of many kinds of chronic diseases, such as heart disease, cancer, chronic pain, and atrial fibrillation, thus making it essential to conduct minimally invasive surgeries. The US has a highly developed healthcare system, a high rate of adoption of the latest technologies, and the presence of leading medical device companies that constantly invest in R&D in the field of ablation devices. Rising preference for minimally invasive surgeries, aging population, and rising awareness are driving the market.

A breakdown of the primary participants (supply-side) for the ablation technology market referred to in this report is provided below:

- By Company Type: Tier 1-35%, Tier 2-40%, and Tier 3-25%

- By Designation: C-level-45%, Director Level-35%, and Others-20%

- By Region: North America-27%, Europe-25%, Asia Pacific-30%, Latin America- 8%, Middle East & Africa-10%.

Prominent players in the ablation technology market are Johnson & Johnson (US), Medtronic (Ireland), Boston Scientific Corporation (US), Abbott Laboratories (US), ArtiCure, Inc. (US), and AngioDynamics (US).

Research Coverage:

The report analyzes the ablation technology market and aims at estimating the market size and future growth potential of this market based on various segments such as technology, product, application, end user, and region. The report also includes a competitive analysis of the key players in this market along with their company profiles, service offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall ablation technology market. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (Emerging ablation technologies, Rising prevalence of chronic diseases, Increasing geriatric population worldwide), restraints (Strong market positioning of alternative therapies, High cost of advanced ablation devices and procedures, Stringent regulatory systems), opportunities (Growth potential in emerging economies) and challenges (Concerns regarding long-term efficacy and recurrence rates in certain ablation procedures, Intense competition among market players leading to pricing pressure and rapid technological obsolescence).

- Market Penetration: It includes extensive information on products offered by the major players in the ablation technology market. The report includes various segments in product, application, end user, and region.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global ablation technology market.

- Market Development: Thorough knowledge and analysis of the profitable rising markets by technology, product, application, end user and region.

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the ablation technology market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products, and capacities of the major competitors in the ablation technology market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONS CONSIDERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS & DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET GROWTH

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ABLATION TECHNOLOGY MARKET OVERVIEW

- 3.2 ASIA PACIFIC: ABLATION TECHNOLOGY MARKET, BY PRODUCT AND COUNTRY (2025)

- 3.3 ABLATION TECHNOLOGY MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES (2025)

- 3.4 ABLATION TECHNOLOGY MARKET, BY REGION (2024-2031)

- 3.5 ABLATION TECHNOLOGY MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.1.1 DRIVERS

- 4.1.1.1 Emerging ablation technologies

- 4.1.1.2 Increasing demand for minimally invasive procedures

- 4.1.1.3 Increasing geriatric population worldwide

- 4.1.1.4 Rising prevalence of chronic diseases

- 4.1.2 RESTRAINTS

- 4.1.2.1 Strong market positioning of alternative therapies

- 4.1.2.2 Stringent regulatory systems

- 4.1.2.3 High cost of advanced ablation devices and procedures

- 4.1.3 OPPORTUNITIES

- 4.1.3.1 Growth potential in emerging economies

- 4.1.3.2 Growing demand for pulsed field ablation (PFA) and non-thermal ablation technologies

- 4.1.4 CHALLENGES

- 4.1.4.1 Concerns regarding long-term efficacy and recurrence rates in certain ablation procedures

- 4.1.4.2 Therapeutic challenges and hazardous effects of ablation

- 4.1.1 DRIVERS

- 4.2 UNMET NEEDS AND WHITE SPACES

- 4.2.1 UNMET NEEDS IN ABLATION TECHNOLOGY MARKET

- 4.2.2 WHITE SPACE OPPORTUNITIES

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INTERCONNECTED MARKET

- 4.3.2 CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ELECTROPHYSIOLOGY INDUSTRY

- 5.2.4 TRENDS IN GLOBAL PAIN MANAGEMENT DEVICES INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.4.1 RESEARCH & PRODUCT DEVELOPMENT

- 5.4.2 RAW MATERIAL PROCUREMENT AND MANUFACTURING

- 5.4.3 DISTRIBUTION, MARKETING & SALES, AND POST-SALES SERVICES

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS (2023-2025)

- 5.6.1 AVERAGE SELLING PRICE TREND, BY KEY PLAYER (2025)

- 5.6.2 AVERAGE SELLING PRICE TREND, BY REGION (2023-2025)

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO FOR HS CODE 9018

- 5.7.2 EXPORT SCENARIO FOR HS CODE 9018

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 CASE STUDY 1: RADIOFREQUENCY ABLATION ANALYSIS CASE STUDY

- 5.11.2 CASE STUDY 2: THERMOCOOL CATHETER CASE STUDY

- 5.11.3 CASE STUDY 3: HYBRID ABLATION LEFT VENTRICULAR FUNCTION NORMALIZED, MEDICATION REDUCED

- 5.12 IMPACT OF US TARIFFS-ABLATION TECHNOLOGY MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USER INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 THERMAL ABLATION TECHNOLOGY

- 6.1.2 NON-THERMAL ABLATION TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 MEDICAL COOLING SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ABLATION PLANNING SOFTWARE

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.4.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS OF ABLATION TECHNOLOGY

- 6.7 IMPACT OF AI/GEN AI ON ABLATION TECHNOLOGY MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN ABLATION TECHNOLOGY PROCESSING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN ABLATION TECHNOLOGY

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ABLATION TECHNOLOGY MARKET

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.2.1 North America

- 7.1.2.1.1 US

- 7.1.2.1.2 Canada

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 Japan

- 7.1.2.3.2 China

- 7.1.2.3.3 India

- 7.1.2.4 Latin America

- 7.1.2.4.1 Brazil

- 7.1.2.1 North America

- 7.1.3 INDUSTRY STANDARDS

- 7.2 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 ABLATION TECHNOLOGY MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 RADIOFREQUENCY ABLATION

- 9.2.1 LOWER COST AND HIGHER EFFICACY TO PROPEL MARKET GROWTH

- 9.3 LASER/LIGHT ABLATION

- 9.3.1 LOWER RISK OF TISSUE DAMAGE AND BETTER REAL-TIME MONITORING TO AID MARKET GROWTH

- 9.4 ULTRASOUND ABLATION

- 9.4.1 HIGH INCIDENCE OF LIVER TUMORS AND CANCER TO FUEL MARKET GROWTH

- 9.5 CRYOABLATION

- 9.5.1 FEWER COMPLICATIONS AND SHORTER PROCEDURAL TIME TO DRIVE MARKET

- 9.6 MICROWAVE ABLATION

- 9.6.1 FASTER ABLATION TIME AND LESSER PROCEDURAL PAIN TO AUGMENT MARKET GROWTH

- 9.7 PULSED FIELD ABLATION

- 9.7.1 IMPROVED SAFETY, SHORTER PROCEDURAL TIME, AND FEWER COMPLICATIONS TO PROPEL MARKET GROWTH

- 9.8 HYDROTHERMAL/HYDROMECHANICAL ABLATION

- 9.8.1 INCREASED USAGE IN GYNECOLOGICAL DISORDERS AND MENORRHAGIA TO AID MARKET GROWTH

- 9.9 OTHER ABLATION TECHNOLOGIES

10 ABLATION TECHNOLOGY MARKET, BY PRODUCT

- 10.1 INTRODUCTION

- 10.2 SYSTEMS

- 10.2.1 RADIOFREQUENCY ABLATION SYSTEMS

- 10.2.1.1 Temperature-controlled RF ablation systems

- 10.2.1.1.1 Technological advancements and improved clinical outcomes to propel segment growth

- 10.2.1.2 Irrigated RF ablation systems

- 10.2.1.2.1 Enhanced lesion formation and improved procedural efficiency to support market growth

- 10.2.1.3 Multi-electrode RF ablation systems

- 10.2.1.3.1 Reduced procedure time and improved ablation precision to accelerate segment adoption

- 10.2.1.4 Bipolar RF systems

- 10.2.1.4.1 Superior energy delivery control and precise tissue targeting to drive market growth

- 10.2.1.1 Temperature-controlled RF ablation systems

- 10.2.2 LASER/LIGHT ABLATION SYSTEMS

- 10.2.2.1 Excimer laser ablation systems

- 10.2.2.1.1 Low direct tissue interaction, precise ablation zone, and high procedural efficiency to drive adoption

- 10.2.2.2 CO2 laser ablation systems

- 10.2.2.2.1 High precision tissue vaporization and minimal bleeding to support market growth

- 10.2.2.3 Diode laser ablation systems

- 10.2.2.3.1 Compact design, energy efficiency, and versatile clinical applications to accelerate segment growth

- 10.2.2.4 Other laser/light ablation systems

- 10.2.2.1 Excimer laser ablation systems

- 10.2.3 ULTRASOUND ABLATION SYSTEMS

- 10.2.3.1 High-intensity focused ultrasound ablation systems

- 10.2.3.1.1 Low procedural time and reduced bleeding to support system adoption

- 10.2.3.2 Magnetic resonance-guided focused ultrasound ablation systems

- 10.2.3.2.1 Non-pregnancy safe treatment procedure to limit adoption

- 10.2.3.1 High-intensity focused ultrasound ablation systems

- 10.2.4 CRYOABLATION SYSTEMS

- 10.2.4.1 Technological advancements and introduction of new cryoprobes to aid adoption

- 10.2.5 PULSED FIELD ABLATION SYSTEMS

- 10.2.5.1 Tissue-selective ablation and reduced thermal injury to accelerate market adoption

- 10.2.6 MICROWAVE ABLATION SYSTEMS

- 10.2.6.1 Production of large ablation zones without a heat-sink effect on surrounding tissues to drive market

- 10.2.7 HYDROTHERMAL/HYDROMECHANICAL ABLATION SYSTEMS

- 10.2.7.1 Increased need for minimally invasive procedures for gynecological disorders to support market growth

- 10.2.8 OTHER ABLATION SYSTEMS

- 10.2.1 RADIOFREQUENCY ABLATION SYSTEMS

- 10.3 CONSUMABLES

- 10.3.1 GROWING PREFERENCE FOR ADVANCED MINIMALLY INVASIVE PROCEDURES TO SPUR MARKET GROWTH

11 ABLATION TECHNOLOGY MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 CVD TREATMENT

- 11.2.1 INCREASING TARGET PATIENT POPULATION TO PROPEL MARKET GROWTH

- 11.3 CANCER TREATMENT

- 11.3.1 HIGH PREVALENCE OF CANCER AND NEED FOR ADVANCED TREATMENT PROCEDURES TO AUGMENT MARKET GROWTH

- 11.3.2 LIVER CANCER

- 11.3.3 KIDNEY CANCER

- 11.3.4 PROSTATE CANCER

- 11.3.5 LUNG CANCER

- 11.3.6 BONE METASTASIS

- 11.3.7 BREAST CANCER

- 11.4 ORTHOPEDIC TREATMENT

- 11.4.1 GROWING DISEASE PREVALENCE AND RISING GERIATRIC POPULATION TO SPUR MARKET GROWTH

- 11.5 COSMETIC/AESTHETIC SURGERY

- 11.5.1 INCREASING DEMAND FOR AESTHETIC SURGICAL PROCEDURES TO FUEL MARKET GROWTH

- 11.6 UROLOGICAL TREATMENT

- 11.6.1 HIGH DEMAND FOR MINIMALLY INVASIVE PROCEDURES AMONG PATIENTS TO DRIVE MARKET

- 11.7 GYNECOLOGICAL TREATMENT

- 11.7.1 INCREASING REPRODUCTIVE HEALTH CONCERNS AND DECREASING FERTILITY RATE TO PROPEL MARKET GROWTH

- 11.8 PAIN MANAGEMENT

- 11.8.1 MINIMUM RECOVERY TIME AND LONG-LASTING PAIN RELIEF TO SUPPORT MARKET GROWTH

- 11.9 OPHTHALMOLOGICAL TREATMENT

- 11.9.1 RISING PREVALENCE OF VISION DISORDERS AMONG ALL AGE GROUPS TO AID MARKET GROWTH

- 11.10 OTHER APPLICATIONS

12 ABLATION TECHNOLOGY MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 HOSPITALS, SURGICAL CENTERS, AND ABLATION CENTERS

- 12.2.1 HIGH ADOPTION OF ROBOTIC PROCEDURES IN SURGERIES AND IMPROVED HEALTHCARE INFRASTRUCTURE TO DRIVE MARKET

- 12.3 AMBULATORY SURGERY CENTERS

- 12.3.1 NEED FOR COST-EFFECTIVE OUTPATIENT TREATMENTS TO SPUR MARKET GROWTH

- 12.4 MEDICAL SPAS AND AESTHETIC & DERMATOLOGY CLINICS

- 12.4.1 INCREASING PREFERENCE FOR MINIMALLY INVASIVE AND NON-INVASIVE AESTHETIC PROCEDURES TO BOOST MARKET GROWTH

- 12.5 OTHER END USERS

13 ABLATION TECHNOLOGY MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 US to dominate North American market during forecast period

- 13.2.2 CANADA

- 13.2.2.1 Rising burden of cancer and growing demand for minimally invasive procedures to support market growth

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Developed healthcare infrastructure and high incidence of chronic diseases to support market growth

- 13.3.2 FRANCE

- 13.3.2.1 Growing geriatric population and rising prevalence of cancer to aid market growth

- 13.3.3 UK

- 13.3.3.1 Rising target patient population and growing awareness about advanced treatment options to drive market

- 13.3.4 ITALY

- 13.3.4.1 Increasing number of clinical trials and growing focus on advanced research activities to augment market growth

- 13.3.5 SPAIN

- 13.3.5.1 Increasing government research funding and growing focus on effective cancer diagnosis to propel market growth

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 JAPAN

- 13.4.1.1 Presence of a universal healthcare reimbursement system to augment market growth

- 13.4.2 CHINA

- 13.4.2.1 Increased patient pool and favorable government initiatives to fuel market growth

- 13.4.3 INDIA

- 13.4.3.1 Modernization of healthcare infrastructure and increased medical tourism to aid market growth

- 13.4.4 AUSTRALIA

- 13.4.4.1 Increased research investments and favorable government initiatives to spur market growth

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Focus on healthcare R&D and supportive government initiatives to positively impact market growth

- 13.4.6 REST OF ASIA PACIFIC

- 13.4.1 JAPAN

- 13.5 LATIN AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Increasing government funding and growing burden of chronic diseases to propel market growth

- 13.5.2 MEXICO

- 13.5.2.1 Availability of advanced care initiatives and awareness programs to fuel market growth

- 13.5.3 REST OF LATIN AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 GCC COUNTRIES

- 13.6.1.1 Increasing healthcare modernization and rising investments in advanced medical technologies to drive market growth

- 13.6.2 REST OF MIDDLE EAST AND AFRICA

- 13.6.1 GCC COUNTRIES

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN ABLATION TECHNOLOGY MARKET

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 Type footprint

- 14.5.5.4 Product footprint

- 14.5.5.5 Application footprint

- 14.5.5.6 End-user footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 DYNAMIC COMPANIES

- 14.6.3 STARTING BLOCKS

- 14.6.4 RESPONSIVE COMPANIES

- 14.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.7 COMPANY VALUATION AND FINANCIAL METRICS

- 14.7.1 FINANCIAL METRICS

- 14.7.2 COMPANY VALUATION

- 14.7.3 BRAND COMPARISON

- 14.8 COMPETITIVE SCENARIO

- 14.8.1 PRODUCT APPROVALS

- 14.8.2 DEALS

- 14.8.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 JOHNSON & JOHNSON

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product approvals

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 MEDTRONIC

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product approvals

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 BOSTON SCIENTIFIC CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product approvals

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices made

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 ABBOTT LABORATORIES

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product approvals

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices made

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 ATRICURE, INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches and approvals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices made

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 ANGIODYNAMICS

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product approvals

- 15.1.6.3.2 Deals

- 15.1.7 CONMED CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.8 OLYMPUS CORPORATION

- 15.1.8.1 Products offered

- 15.1.8.2 Recent developments

- 15.1.8.2.1 Product launches

- 15.1.8.2.2 Deals

- 15.1.9 VARIAN MEDICAL SYSTEMS, INC.

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches & approvals

- 15.1.9.3.2 Deals

- 15.1.10 SMITH+NEPHEW

- 15.1.10.1 Business overview

- 15.1.10.2 Product offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Expansions

- 15.1.11 STRYKER

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product approvals

- 15.1.11.3.2 Expansions

- 15.1.12 MICROPORT SCIENTIFIC CORPORATION

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product approvals

- 15.1.13 CYNOSURE LUTRONIC

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Deals

- 15.1.14 BIOTRONIK SE & CO. KG

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.15 MERIT MEDICAL SYSTEMS

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.16 ARTHREX, INC.

- 15.1.16.1 Business overview

- 15.1.16.2 Products offered

- 15.1.1 JOHNSON & JOHNSON

- 15.2 OTHER PLAYERS

- 15.2.1 HOLOGIC, INC.

- 15.2.2 ICECURE MEDICAL

- 15.2.3 MINIMAX MEDICAL HOLDING GROUP

- 15.2.4 CARDIOFOCUS

- 15.2.5 EMBLATION LTD.

- 15.2.6 MERMAID MEDICAL

- 15.2.7 MONTERIS

- 15.2.8 SONABLATE CORP.

- 15.2.9 ECO MEDICAL

- 15.2.10 SURGNOVA

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key secondary sources

- 16.1.1.2 Objectives of secondary research

- 16.1.1.3 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.2.3 BASE NUMBER ESTIMATION

- 16.3 MARKET FORECAST APPROACH

- 16.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 16.5 ASSUMPTIONS

- 16.6 GROWTH RATE ASSUMPTIONS

- 16.7 FACTOR ANALYSIS

- 16.8 RISK ASSESSMENT

- 16.9 METHODOLOGY-RELATED LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS