|

시장보고서

상품코드

2059966

자동차용 와이어 하네스 시장 예측(-2033년) : 유형 및 용도별, 변속기 유형별, 재료 유형별, 전송 속도별, 용도별, 전압별, 내연기관(ICE) 및 EV 변속기 유형 및 용도별, 컴포넌트별, 카테고리별, 지역별Automotive Wiring Harness Market by Application (Engine, Chassis, Cabin, Body & Lighting, HVAC, Battery, Dashboard/Cabin, Seat, Sunroof, Door, infotainment, ADAS), ICE & EV Transmission Type, Data Rate, Material & Region - Global Forecast To 2033 |

||||||

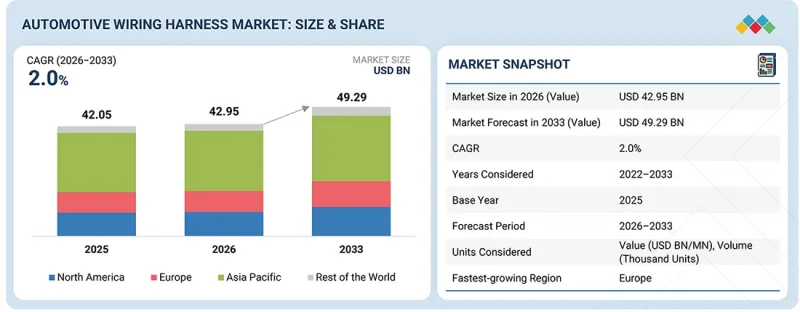

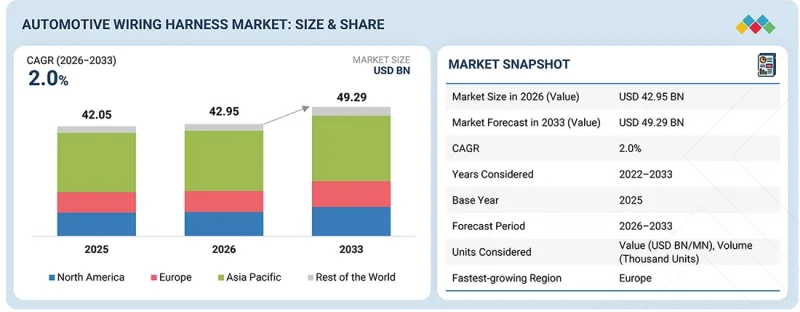

자동차용 와이어 하네스 시장 규모는 2026년 429억 5,000만 달러에서 2033년까지 492억 9,000만 달러로, CAGR 2.0%로 확대할 것으로 예측됩니다.

자동차 제조사들은 소프트웨어 정의 차량, ADAS, 자율주행, 커넥티드 서비스 및 OTA 업데이트에 대응하기 위해 기존의 분산형 E/E 아키텍처에서 존형 E/E 아키텍처로의 전환을 가속화하고 있습니다. 이 아키텍처에서는 여러 개의 ECU가 존 컨트롤러에 통합되어, 고속 자동차용 이더넷 네트워크를 통해 중앙 집중식 고성능 컴퓨터로 연결됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2033년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 대상 단위 | 100만 달러 |

| 부문 | 유형 및 용도별, 변속기 유형별, 재료 유형별, 전송 속도별, 용도별, 전압별, 내연기관(ICE) 및 EV 변속기 유형 및 용도별, 컴포넌트별, 카테고리별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 세계의 기타 지역 |

존형 아키텍처는 배선 총 연장 거리, 차량 중량 및 하네스의 복잡성을 20-30% 가까이 줄여주지만, 업계가 배선량 증가가 아닌 고부가가치 하네스 시스템으로 전환하고 있으므로 자동차용 와이어 하네스 시장의 성장을 촉진할 것으로 예상됩니다.

"예측 기간 중 와이어는 가장 큰 구성 요소 부문이 될 것입니다. " '

와이어는 엔진, 섀시, 차체 전자장치, 인포테인먼트, HVAC, ADAS를 포함한 모든 차량 시스템에서 전력 분배, 접지 및 신호 전송의 핵심 매개체 역할을 하므로 자동차용 와이어 하네스 부품 시장을 주도하고 있습니다. 커넥터 및 전자 모듈의 사용이 증가하고 있음에도 불구하고 차량의 전동화 진전과 차량용 전자 기기의 증가로 인해 자동차용 전선에 대한 강한 수요가 계속 유지되고 있습니다. 구리선은 널리 보급되어 있으며, 뛰어난 전도성, 내구성, 유연성 및 높은 비용 효율성 덕분에 금액 기준으로 시장의 60% 이상을 차지하고 있습니다. 한편, 차량의 경량화를 도모하기 위해 특정 용도에서 알루미늄 선의 사용이 증가하고 있습니다. 북미, 유럽, 아시아태평양의 프리미엄 차량 모델에서는 각 OEM 업체들이 ADAS, 디지털 콕핏, 커넥티드 카, 자율주행 애플리케이션용으로 100 Mbps에서 멀티 기가비트급 데이터 전송 속도를 지원하는 차폐 트위스트 페어 케이블, 동축 케이블, 자동차용 이더넷 배선 등 고속 데이터 전송용 케이블을 점점 더 적극적으로 채택하고 있습니다. 또한 존형 E/E 아키텍처, 소프트웨어 정의 차량, 첨단 안전 시스템, 커넥티드 모빌리티 기술의 도입이 확대됨에 따라 특수한 고전압, 내열성, 경량성 및 고대역폭을 갖춘 배선 솔루션에 대한 수요가 증가하고 있습니다.

“예측 기간 중 ICE(내연기관) 차량 분야에서 광섬유는 가장 빠르게 성장하고 있는 소재 부문입니다. ” '

자동차용 와이어 하네스 시스템에서 광섬유는 주로 초고속 데이터 통신에 사용되며, 특히 대량의 실시간 데이터를 최소한의 지연과 전자기 간섭 없이 전송해야 하는 용도로 활용되고 있습니다. 기존에 광섬유 케이블은 주로 오디오, 비디오, 내비게이션, 뒷좌석 엔터테인먼트 시스템을 위한 MOST(Media Oriented Systems Transport) 아키텍처를 통해 프리미엄 인포테인먼트 및 멀티미디어 네트워크에 사용되었으며, 일반적으로 25 Mbps에서 150 Mbps의 데이터 전송 속도를 지원했습니다. 그러나 ADAS, 자율주행 기술, 디지털 콕핏, 360도 카메라 시스템, LiDAR, 레이더, 고해상도 디스플레이, 그리고 중앙 집중형 컴퓨팅 플랫폼의 급속한 통합에 따라 데이터 전송 요구 사항이 대폭 증가하는 첨단 운전자 지원 시스템(ADAS) 및 차량용 백본 통신 시스템에서 광섬유의 도입이 점점 더 확대되고 있습니다. 북미, 유럽, 아시아·태평양 지역의 최신 프리미엄 차량, 특히 테슬라, 메르세데스-벤츠, BMW, 아우디, 현대자동차 그룹, 도요타 자동차 등의 OEM이 개발하는 고급차 및 소프트웨어 정의 차량(SDV) 플랫폼에서, 1Gbps에서 10Gbps의 데이터 전송 속도를 지원하는 자동차용 이더넷 및 고속 통신 아키텍처의 채택이 확대되고 있습니다.

“예측 기간 중 아시아태평양이 전 세계 자동차용 와이어 하네스 시장을 주도할 것으로 전망됩니다. ” '

아시아태평양은 중국, 일본, 한국, 인도 등 여러 국가의 막대한 자동차 생산량 덕분에 전 세계 자동차용 와이어 하네스 시장을 주도하고 있습니다. 이 지역에서는 프리미엄 차량이나 고급차 모델에 비해 차량당 와이어 하네스 사용량이 적은 경제적인 승용차(80% 이상)의 대량 생산이 시장의 주요 원동력이 되고 있습니다. 그러나 엔트리급 차량의 경우 하네스의 복잡도는 낮은 편이지만, 차체 및 조명용 하네스는 헤드램프, 테일램프, 안개등, 실내 조명, 파워 윈도우, 도어 모듈, 계기판, HVAC(공조) 제어, 와이퍼, 중앙 잠금 장치, 미러, 시트 시스템 등 차량의 여러 영역과 용도에서 광범위하게 사용되고 있으므로 이 부문은 여전히 주도적인 위치를 차지하고 있습니다. 따라서 저비용 차량에서도 없어서는 안 될 존재가 되고 있습니다. 동시에 중국, 한국, 일본에서 프리미엄차 및 고급차의 판매는 꾸준히 증가하고 있으며, 중국에서는 주요 도시 시장의 승용차 판매량 중 15-18% 가량을 프리미엄차가 차지하고 있습니다. 한편, 일본과 한국에서는 첨단 커넥티드 카와 안전 장비를 탑재한 차량의 보급이 계속해서 확대되고 있습니다. 일본이나 한국 등에서는 엄격한 자동차 안전 규제와 NCAP 기준이 마련되어 있으며, 각 OEM 업체들에게 ADAS, 에어백, 차선이탈 경고, 사각지대 모니터링, 적응형 조명, 주차 보조, 충돌 회피 시스템 등의 첨단 안전 기능을 탑재하도록 권장하고 있습니다. 이 모든 것에는 추가 센서, ECU, 커넥터, 그리고 첨단 와이어 하네스 네트워크가 필요합니다.

자동차용 와이어 하네스 시장의 주요 기업은 Yazaki Corporation(일본), Sumitomo Electric Industries(일본), Aptiv(아일랜드), Furukawa Electric(일본), Leoni AG(독일), Samwardhana Motherson International(인도), Lear Corporation(미국), Prysmian Group(이탈리아), Nexans(독일), Gebauer & Griller Group(독일), 그리고 Fujikura Ltd.(일본)입니다.

조사 범위

본 조사에서는 자동차용 와이어 하네스 시장을 세분화하고, ICE(응용 분야별, 소재별, 변속기 유형별)를 기준으로 시장 규모를 예측하고 있습니다. 구체적으로는 용도별(엔진 하네스, 섀시 하네스, 차체 및 조명 하네스, HVAC 하네스, 대시보드/실내 하네스, 배터리 하네스, 도어 하네스, 인포테인먼트 하네스, 능동 및 수동 안전 하네스, ADAS 하네스, 루프 하네스, 시트 하네스, 기타/보조 하네스), ICE 구성 부품별(커넥터, 와이어, 단자, 기타), ICE 재질별(금속, 광섬유), ICE 전송 유형별(데이터 전송, 전기 배선), ICE 차종 및 용도(승용차, 소형 상용차, 버스, 트럭), EV의 차종 및 용도(BEV, PHEV, FCEV), EV의 재질(금속, 광섬유), EV의 전송 유형(데이터 전송, 전기 배선), 고전압 용도(배터리 및 배터리 관리 시스템, 모터 관리), 데이터 전송 속도(150 Mbps 미만, 150 Mbps-1 Gbps), 용도별 데이터 전송(ADAS, 인포테인먼트, 보안, 기타), 전압(<400V, >(400V) 및 지역(아시아태평양, 유럽, 북미, 기타 지역).

이 보고서를 구매할 때의 주요 이점:

이 보고서는 시장 선도 기업 및 신규 진입 기업을 대상으로, 자동차용 와이어 하네스 시장 및 그 하위 부문의 매출에 관한 가장 정확한 추정치를 제공합니다. 또한 공급업체의 자동차용 와이어 하네스 판매 동향을 분석하고 있으며, 부품 공급업체가 전략을 수립하는 데 도움이 됩니다. 이 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 유리한 위치에 놓으며, 적절한 시장 진입 전략을 수립하는 데 필요한 인사이트를 얻는 데 도움이 됩니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(도메인 아키텍처에서 존 아키텍처로의 전환 및 전기 에너지 밀도의 급증), 제약 요인(E/E 아키텍처 개발을 위한 숙련된 인력 부족), 기회(고전압 와이어 하네스 및 광섬유 케이블 사용 증가, 알루미늄 와이어 하네스의 광범위한 채택), 그리고 과제(고급 차량에서의 개발 비용 상승, 와이어 준비, 스테이징, 압착과 관련된 과제) 등, 자동차용 와이어 하네스 시장의 성장에 영향을 미치는 요인들에 대해 분석하고 있습니다.

- 제품 개발 및 혁신: 자동차용 와이어 하네스 시장의 향후 기술 동향 및 신제품·서비스 출시에 관한 상세 인사이트

- 시장 개발: 포괄적인 시장 정보 - 이 보고서에서는 다양한 지역의 인증 및 브랜드 보호 시장을 분석하고 있습니다.

- 시장의 다양화: 자동차용 와이어 하네스 시장의 신제품·서비스, 미개발 지역, 최근 동향 및 투자에 관한 포괄적인 정보

- 경쟁사 분석: Yazaki Corporation(일본), Sumitomo Electric Industries(일본), Aptiv(아일랜드), Furukawa Electric(일본), Leoni AG(독일), Samwardhana Motherson International(인도), Lear Corporation(미국), Prysmian Group(이탈리아), Nexans(독일), Gebauer & Griller Group(독일) 및 Fujikura Ltd.(일본) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 전략적 응용

제7장 고객 상황과 구매 행동

제8장 규제 상황

제9장 전기자동차용 와이어링 하네스 시장(유형 및 용도별)

제10장 전기자동차용 와이어 하네스 시장(변속기 유형별)

제11장 전기자동차용 와이어 하네스 시장(재료 유형별)

제12장 데이터 전송 하네스 시장(데이터 전송 속도별)

제13장 데이터 전송 하네스 시장(용도별)

제14장 고전압 와이어링 하네스 시장(용도별)

제15장 자동차용 와이어 하네스 시장(전압별)

제16장 내연기관 차량용 와이어링 하네스 시장(변속기 유형별)

제17장 내연기관 차량용 자동차용 와이어 하네스 시장(재료 유형별)

제18장 자동차용 와이어 하네스 시장(내연기관 차종별 및 용도별)

제19장 내연기관 차량용 자동차용 와이어 하네스 시장(컴포넌트별)

제20장 자동차용 와이어 하네스 시장(카테고리별)

제21장 내연기관 차량용 자동차용 와이어 하네스 시장(용도별)

제22장 48 V 및 EV 와이어링 하네스 아키텍처

제23장 내연기관 차량용 와이어링 하네스 시장(지역별)

제24장 경쟁 구도

제25장 기업 개요

제26장 조사 방법

제27장 시장의 권장사항

제28장 부록

KSA 26.06.24The automotive wiring harness market is projected to grow from USD 42.95 billion in 2026 to USD 49.29 billion by 2033 at a CAGR of 2.0%. Automotive OEMs are increasingly shifting from traditional distributed E/E architectures toward zonal E/E architectures to support software-defined vehicles, ADAS, autonomous driving, connected services, and OTA updates, where multiple ECUs are consolidated into zonal controllers connected through centralized high-performance computers using high-speed automotive Ethernet networks.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Million |

| Segments | by Application, ICE & EV Transmission Type, Data Rate, Material & Region |

| Regions covered | North America, Europe, Asia Pacific, Rest of the World |

Although zonal architecture reduces overall wire length, vehicle weight, and harness complexity by nearly 20-30%, it is expected to drive growth in the automotive wiring harness market because the industry is shifting toward higher-value harness systems rather than higher wire volumes.

"Wires are the largest component segment during the forecast period."

Wires lead the automotive wiring harness component market because they are the core medium for power distribution, grounding, and signal transmission across all vehicle systems, including engine, chassis, body electronics, infotainment, HVAC, and ADAS. Despite increasing use of connectors and electronic modules, growing vehicle electrification and rising electronic content in vehicles continue to sustain strong demand for automotive wires. Copper wires are prevalent, capturing more than 60% of the market in terms of value due to their high conductivity, durability, flexibility, and cost-effectiveness. Meanwhile, aluminum wires are increasingly adopted in selected applications to reduce vehicle weight. In premium vehicles across North America, Europe, and Asia Pacific, OEMs are increasingly integrating high-speed data transmission wires such as shielded twisted-pair cables, coaxial cables, and automotive Ethernet wiring capable of supporting data transfer rates ranging from 100 Mbps to multi-gigabit speeds for ADAS, digital cockpit, connected car, and autonomous driving applications. Additionally, rising adoption of zonal E/E architectures, software-defined vehicles, advanced safety systems, and connected mobility technologies is increasing the requirement for specialized high-voltage, heat-resistant, lightweight, and high-bandwidth wiring solutions.

"Optical fiber is the fastest-growing material segment for ICE vehicles during the forecast period."

Optical fiber in automotive wiring harness systems is primarily used for ultra-high-speed data communication, particularly in applications where large volumes of real-time data must be transferred with minimal latency and zero electromagnetic interference. Traditionally, fiber optic cables were mainly used in premium infotainment and multimedia networks through MOST (Media Oriented Systems Transport) architecture for audio, video, navigation, and rear-seat entertainment systems, typically supporting data transfer speeds from 25 Mbps to 150 Mbps. However, with the rapid integration of ADAS, autonomous driving technologies, digital cockpits, 360-degree camera systems, LiDAR, radar, high-resolution displays, and centralized computing platforms, optical fiber is increasingly being adopted in advanced driver assistance and in-vehicle backbone communication systems, where data transmission requirements are significantly higher. Modern premium vehicles in North America, Europe, and Asia Pacific are increasingly adopting automotive Ethernet and high-speed communication architectures capable of supporting 1 Gbps to 10 Gbps data transfer rates, especially in luxury and software-defined vehicle platforms developed by OEMs such as Tesla, Mercedes-Benz, BMW, Audi, Hyundai Motor Group, and Toyota Motor Corporation.

"Asia Pacific dominates the global automotive wiring harness market during the forecast period."

Asia Pacific dominates the global automotive wiring harness market due to its massive vehicle production from countries such as China, Japan, South Korea, and India, where the market is largely driven by high-volume production of economical passenger (more than 80%) cars that typically use lower wiring harness content per vehicle than premium or luxury models. However, despite lower harness complexity in entry-level vehicles, body and lighting harnesses continue to dominate the segment because they are extensively used across multiple vehicle areas and applications, including headlamps, taillamps, fog lamps, interior lighting, power windows, door modules, instrument clusters, HVAC controls, wipers, central locking, mirrors, and seating systems, making them essential even in low-cost vehicles. At the same time, premium and luxury vehicle sales are steadily increasing across China, South Korea, and Japan, with premium vehicle penetration in China accounting for nearly 15-18% of passenger car sales in major urban markets, while Japan and South Korea continue witnessing higher adoption of advanced connected and safety-equipped vehicles. Countries such as Japan and South Korea have stringent vehicle safety regulations and NCAP standards that encourage OEMs to integrate advanced safety features, including ADAS, airbags, lane departure warning, blind-spot monitoring, adaptive lighting, parking assist, and collision avoidance systems, all of which require additional sensors, ECUs, connectors, and sophisticated wiring harness networks.

Breakdown of primaries

The study draws insights from industry experts across the supply chain, including component suppliers, Tier-1 companies, and OEMs. The breakdown of the primary respondents is as follows:

- By Company Type: OEM - 70%, Tier I - 30%

- By Designation: D Level - 30%, C Level - 60%, and Others - 10%

- By Region: North America - 10%, Europe - 30%, Asia Pacific - 60%,

The key players in the automotive wiring harness market are Yazaki Corporation (Japan), Sumitomo Electric Industries (Japan), Aptiv (Ireland), Furukawa Electric (Japan), and Leoni AG (Germany), Samwardhana Motherson Internation Limited (India), Lear Corporation (US), Prysmian Group (Italy), Nexans (Germany), Gebauer & Griller Group (Germany), and Fujikura Ltd. (Japan).

Research Coverage

The study segments the automotive wiring harness market and forecasts the market size based on ICE by application (engine harness, chassis harness, body and lighting harness, HVAC harness, dashboard/cabin harness, battery harness, door harness, infotainment harness, active and passive safety harness, ADAS harness, roof harness, seat harness, other/auxiliary harness), ICE by component (connectors, wires, terminals, others), ICE by material (metallic, optical wiring), ICE by transmission type (data transmission, electric wiring), ICE vehicle type & application (passenger cars, light commercial vehicles, buses, trucks), EV type & application (BEVs, PHEVs, FCEVs), EV by material (metallic, optical wiring), EV by transmission type (data transmission, electric wiring), high voltage by application (battery & battery management systems, motor management), data rate (<150 Mbps, 150 Mbps to 1 Gbps), data transmission by application (ADAS, Infotainment, security, others), voltage (<400V, >400V), and region (Asia Pacific, Europe, North America, Rest of the World).

Key Benefits of Buying this Report:

The report will provide market leaders and new entrants with the closest approximations of revenue figures for the automotive wiring harness market and its subsegments. It also examines automotive wire harness sales trends from suppliers, enabling component suppliers to plan their strategies. This report will help stakeholders understand the competitive landscape and gain insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Transition from domain to zonal architecture and Electric energy density explosion), restraints (Lack of skilled workforce for developing E/E architecture), opportunities (Increase in use of high-voltage harnesses and optical fiber cablese, Extensive use of aluminum wiring harnesses), and challenges (Higher development cost in premium cars, Issues related to wire preparation, staging, and crimping) influencing the growth of the automotive wiring harness market.

- Product Development/Innovation: Detailed insights on upcoming technologies and new product & service launches in the automotive wiring harness market

- Market Development: Comprehensive market information - the report analyzes the authentication and brand protection market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the automotive wiring harness market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players like Yazaki Corporation (Japan), Sumitomo Electric Industries (Japan), Aptiv (Ireland), Furukawa Electric (Japan), Leoni AG (Germany), Samwardhana Motherson Internation Limited (India), Lear Corporation (US), Prysmian Group (Italy), Nexans (Germany), Gebauer & Griller Group (Germany), and Fujikura Ltd. (Japan), among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 REGIONAL SCOPE

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNIT CONSIDERED

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.2 KEY STRENGTHS OF AUTOMOTIVE WIRING MANUFACTURERS

- 2.3 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

- 2.4 HIGH GROWTH SEGMENTS

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE WIRING HARNESS MARKET

- 3.2 AUTOMOTIVE WIRING HARNESS MARKET, BY ICE VEHICLE TYPE

- 3.3 ICE VEHICLE WIRING HARNESS MARKET, BY APPLICATION

- 3.4 ICE VEHICLE WIRING HARNESS MARKET, BY TRANSMISSION TYPE

- 3.5 ELECTRIC VEHICLE WIRING HARNESS MARKET, BY TRANSMISSION TYPE

- 3.6 ELECTRIC WIRING HARNESS MARKET, BY VEHICLE TYPE

- 3.7 AUTOMOTIVE WIRING HARNESS MARKET, BY COMPONENT

- 3.8 AUTOMOTIVE WIRING HARNESS MARKET, BY MATERIAL

- 3.9 DATA TRANSMISSION HARNESS MARKET, BY DATA TRANSFER RATE

- 3.10 HIGH VOLTAGE WIRING HARNESS MARKET, BY APPLICATION

- 3.11 AUTOMOTIVE WIRING HARNESS MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Transition from domain architectures to zonal electrical architecture

- 4.2.1.2 Rise in demand for multi-voltage and energy platforms

- 4.2.2 RESTRAINTS

- 4.2.2.1 Lack of skilled workforce

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increase in use of high-voltage wiring harnesses and optical fiber cables

- 4.2.3.2 Increase in use of aluminum wiring harness

- 4.2.4 CHALLENGES

- 4.2.4.1 High development cost in premium vehicles

- 4.2.4.2 Issues related to wire preparation, staging, and crimping

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.6 OEM ANALYSIS

- 4.6.1 COMPETITIVE ANALYSIS FOR DOMAIN AND ZONAL E/E ARCHITECTURE

- 4.6.1.1 Zonal E/E architecture companies overview

- 4.6.1.2 Domain architecture

- 4.6.1 COMPETITIVE ANALYSIS FOR DOMAIN AND ZONAL E/E ARCHITECTURE

- 4.7 OEM ROADMAPS FOR VEHICLE PLATFORMS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.1.3.1 Regional GDP dynamics

- 5.1.3.1.1 Developed markets (Asia Pacific, Europe, North America, and Rest of the World)

- 5.1.3.1.2 Emerging markets

- 5.1.3.1.2.1 China

- 5.1.3.1.2.2 India

- 5.1.3.1.2.3 Brazil

- 5.1.3.1.2.4 Mexico

- 5.1.3.1.2.5 Indonesia

- 5.1.3.1.2.6 Thailand

- 5.1.3.1.2.7 Malaysia

- 5.1.3.2 Investment environment

- 5.1.3.1 Regional GDP dynamics

- 5.2 SUPPLY CHAIN ANALYSIS

- 5.3 ECOSYSTEM ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE OF WIRING HARNESSES, BY ICE VEHICLE TYPE

- 5.4.2 AVERAGE SELLING PRICE OF WIRE HARNESSES, BY EV TYPE

- 5.4.3 AVERAGE SELLING PRICE, BY REGION

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 854430)

- 5.5.2 EXPORT SCENARIO (HS CODE 854430)

- 5.6 KEY CONFERENCES & EVENTS, 2026-2027

- 5.7 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT & FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 URBAN LEAN MAINTENANCE IMPLEMENTATION USING TOTAL PRODUCTIVE MAINTENANCE (TPM) IN AUTOMOTIVE WIRING HARNESS PRODUCTION

- 5.9.2 STRUCTURED WIRING HARNESS DEVELOPMENT FOR COMPLEX AUTOMOTIVE SYSTEMS

- 5.9.3 LIGHTWEIGHT AND PERFORMANCE OPTIMIZATION OF AUTOMOTIVE WIRING HARNESS ASSEMBLIES

- 5.9.4 LIGHTWEIGHT AND INTEGRATED CABLE ASSEMBLY OPTIMIZATION FOR AUTOMOTIVE WIRING HARNESS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE STRATEGIC APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 High-voltage (HV) wiring systems (EV/HEV)

- 6.1.1.2 High-speed data transmission (Automotive Ethernet)

- 6.1.1.3 Lightweight & advanced materials

- 6.1.1.4 Zonal/Modular E/E architecture

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 ADAS & sensor integration

- 6.1.2.2 Smart/Intelligent harness systems

- 6.1.2.3 Thermal & EMC management technologies

- 6.1.2.4 Modular & pre-assembled harness systems

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Electric powertrain systems

- 6.1.3.2 Autonomous & software-defined vehicles

- 6.1.3.3 Connectivity & infotainment ecosystem (5G, V2X)

- 6.1.3.4 Manufacturing automation and AI

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM ROADMAP

- 6.2.2 MID-TERM ROADMAP

- 6.2.3 LONG-TERM ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 INTRODUCTION

- 6.4 FUTURE APPLICATIONS

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 CUSTOMER LANDSCAPE AND BUYER BEHAVIOUR

- 7.1 DECISION-MAKING PROCESS

- 7.2 KEY STAKEHOLDERS & BUYING CRITERIA

- 7.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 7.4 UNMET NEEDS FROM VARIOUS END-USER INDUSTRIES

- 7.5 MARKET PROFITABILITY

- 7.5.1 MARKET PROFITABILITY FOR ICE VEHICLES

- 7.5.2 MARKET PROFITABILITY FOR EVS

8 REGULATORY LANDSCAPE

- 8.1 REGULATORY LANDSCAPE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 REGULATORY ANALYSIS, BY REGION/COUNTRY

- 8.1.2.1 Europe

- 8.2 GLOBAL SAFETY REGULATION

9 ELECTRIC VEHICLE WIRING HARNESS MARKET, BY TYPE AND APPLICATION

- 9.1 INTRODUCTION

- 9.2 TOTAL NUMBER OF HARNESSES USED IN EVS

- 9.3 OPERATIONAL DATA

- 9.4 BATTERY ELECTRIC VEHICLE (BEV)

- 9.4.1 STRONG GOVERNMENT SUPPORT AND FAVORABLE POLICIES IN ASIA PACIFIC TO DRIVE MARKET.

- 9.4.2 CHASSIS HARNESS

- 9.4.3 BODY & LIGHTING HARNESS

- 9.4.4 TRACTION HARNESS

- 9.4.5 HVAC HARNESS

- 9.4.6 DASHBOARD/CABIN HARNESS

- 9.4.7 BATTERY HARNESS

- 9.4.8 DOOR HARNESS

- 9.4.9 INFOTAINMENT HARNESS

- 9.4.10 ACTIVE & PASSIVE SAFETY HARNESS

- 9.4.11 ADAS HARNESS

- 9.4.12 SEAT HARNESS

- 9.4.13 OTHER HARNESSES

- 9.5 PLUG-IN HYBRID ELECTRIC VEHICLE (PHEV)

- 9.5.1 PHEVS HAVE MORE WIRING HARNESSES THAN BEVS AND HEVS

- 9.5.2 TRACTION HARNESS

- 9.5.3 ENGINE HARNESS

- 9.5.4 CHASSIS HARNESS

- 9.5.5 BODY & LIGHTING HARNESS

- 9.5.6 HVAC HARNESS

- 9.5.7 DASHBOARD/CABIN HARNESS

- 9.5.8 BATTERY HARNESS

- 9.5.9 SEAT HARNESS

- 9.5.10 DOOR HARNESS

- 9.5.11 INFOTAINMENT HARNESS

- 9.5.12 ACTIVE & PASSIVE SAFETY HARNESS

- 9.5.13 ADAS HARNESS

- 9.6 FUEL CELL ELECTRIC VEHICLE (FCEV)

- 9.6.1 FCEVS PRODUCE ELECTRICITY USING FUEL CELL POWERED BY HYDROGEN

- 9.6.2 TRACTION HARNESS

- 9.6.3 CHASSIS HARNESS

- 9.6.4 BODY & LIGHTING HARNESS

- 9.6.5 HVAC HARNESS

- 9.6.6 DASHBOARD/CABIN HARNESS

- 9.6.7 INFOTAINMENT HARNESS

- 9.6.8 SEAT HARNESS

- 9.6.9 DOOR HARNESS

- 9.6.10 INDUSTRY INSIGHTS

10 ELECTRIC VEHICLE WIRING HARNESS MARKET, BY TRANSMISSION TYPE

- 10.1 INTRODUCTION

- 10.2 DATA TRANSMISSION

- 10.2.1 INCREASING ADOPTION OF USER-FRIENDLY FEATURES IN EVS TO DRIVE MARKET

- 10.3 ELECTRICAL WIRING

- 10.3.1 RAPID EXPANSION OF EV INDUSTRY TO DRIVE MARKET

- 10.4 INDUSTRY INSIGHTS

11 ELECTRIC VEHICLES WIRING HARNESS MARKET, BY MATERIAL TYPE

- 11.1 INTRODUCTION

- 11.2 METALLIC

- 11.2.1 METALLIC MATERIALS POSSESS EXCEPTIONAL ELECTRICAL CONDUCTIVITY, CRITICAL ATTRIBUTE FOR AUTOMOTIVE WIRING HARNESSES

- 11.2.2 COPPER

- 11.2.2.1 Superior electrical conductivity to drive market

- 11.2.3 ALUMINUM

- 11.2.3.1 Lower weight and cost than copper to drive market

- 11.2.3.2 Other materials

- 11.3 OPTICAL FIBER

- 11.3.1 PLASTIC OPTICAL FIBER (POF)

- 11.3.1.1 Growing need for vehicle weight reduction to drive market

- 11.3.2 GLASS OPTICAL FIBER

- 11.3.2.1 High-temperature tolerance and durability to drive market

- 11.3.1 PLASTIC OPTICAL FIBER (POF)

- 11.4 INDUSTRY INSIGHTS

12 DATA TRANSMISSION HARNESS MARKET, BY DATA TRANSFER RATE

- 12.1 INTRODUCTION

- 12.2 < 150 MBPS

- 12.2.1 RAPID ELECTRIFICATION TO DRIVE MARKET

- 12.3 150 MBPS-1 GBPS

- 12.3.1 GROWING DEMAND FOR CAR NAVIGATION SYSTEMS TO DRIVE MARKET

- 12.4 INDUSTRY INSIGHTS

13 DATA TRANSMISSION HARNESS MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 ADAS HARNESS

- 13.2.1 STRINGENT SAFETY REGULATIONS TO DRIVE MARKET

- 13.3 INFOTAINMENT HARNESS

- 13.3.1 GROWING DEMAND FOR MULTIMEDIA AND CAR NAVIGATION SYSTEMS TO DRIVE MARKET

- 13.4 ACTIVE & PASSIVE SAFETY HARNESS

- 13.4.1 GROWING SAFETY REGULATION GLOBALLY TO DRIVE MARKET

- 13.5 INDUSTRY INSIGHTS

14 HIGH-VOLTAGE WIRING HARNESS MARKET, BY APPLICATION

- 14.1 INTRODUCTION

- 14.2 BATTERY & BATTERY MANAGEMENT SYSTEM

- 14.2.1 GROWING POPULARITY OF ELECTRIC CARS TO DRIVE MARKET

- 14.3 MOTOR MANAGEMENT

- 14.3.1 INCREASING CONSUMER INTEREST IN BEVS TO DRIVE MARKET

- 14.4 INDUSTRY INSIGHTS

15 AUTOMOTIVE WIRING HARNESS MARKET, BY VOLTAGE

- 15.1 INTRODUCTION

- 15.2 < 400 V

- 15.2.1 GROWING POPULARITY OF ELECTRIC CARS TO DRIVE MARKET

- 15.3 > 400 V

- 15.3.1 INCREASING CONSUMER INTEREST IN BEVS TO DRIVE MARKET

- 15.3.2 BATTERY TO INVERTER

- 15.3.3 INVERTER TO MOTOR

- 15.3.4 DC FAST CHARGING CABLES

- 15.4 INDUSTRY INSIGHTS

16 ICE VEHICLE AUTOMOTIVE WIRING HARNESS MARKET, BY TRANSMISSION TYPE

- 16.1 INTRODUCTION

- 16.2 DATA TRANSMISSION

- 16.2.1 DEVELOPMENT OF ADVANCED ELECTRICAL SYSTEMS IN VEHICLES TO DRIVE MARKET

- 16.3 ELECTRICAL WIRING

- 16.3.1 INCREASING INSTALLATION OF HIGH-END ELECTRONICS IN VEHICLES TO DRIVE MARKET

- 16.4 INDUSTRY INSIGHTS

17 AUTOMOTIVE WIRING HARNESS MARKET FOR ICE VEHICLES, BY MATERIAL TYPE

- 17.1 INTRODUCTION

- 17.2 COMPARISON BETWEEN COPPER AND OPTICAL FIBER

- 17.3 METALLIC

- 17.3.1 COPPER

- 17.3.1.1 Increasing demand for electronic features in vehicles to drive market

- 17.3.2 ALUMINUM

- 17.3.2.1 Demand for vehicle weight reduction to drive market

- 17.3.3 OTHER MATERIALS

- 17.3.1 COPPER

- 17.4 OPTICAL FIBER

- 17.4.1 PLASTIC OPTICAL FIBER

- 17.4.1.1 Growing demand for premium vehicles to drive market

- 17.4.2 GLASS OPTICAL FIBER

- 17.4.2.1 Growing demand for EVs and vehicles with advanced features to drive market

- 17.4.1 PLASTIC OPTICAL FIBER

- 17.5 INDUSTRY INSIGHTS

18 AUTOMOTIVE WIRING HARNESS MARKET, BY ICE VEHICLE TYPE AND APPLICATION

- 18.1 INTRODUCTION

- 18.2 NUMBER OF HARNESSES IN ICE VEHICLES, BY APPLICATION

- 18.3 PASSENGER CARS

- 18.3.1 GROWING DEMAND FOR COMFORT AND LUXURY FEATURES TO DRIVE MARKET

- 18.3.2 ENGINE HARNESS

- 18.3.3 CHASSIS HARNESS

- 18.3.4 BODY & LIGHTING HARNESS

- 18.3.5 HVAC HARNESS

- 18.3.6 DASHBOARD/CABIN HARNESS

- 18.3.7 BATTERY HARNESS

- 18.3.8 DOOR HARNESS

- 18.3.9 INFOTAINMENT HARNESS

- 18.3.10 ACTIVE & PASSIVE SAFETY HARNESS

- 18.3.11 ADAS HARNESS

- 18.3.12 ROOF HARNESS

- 18.3.13 SEAT HARNESS

- 18.3.14 OTHER/AUXILIARY HARNESSES

- 18.4 LIGHT COMMERCIAL VEHICLES

- 18.4.1 INCREASING DEMAND FOR ADVANCED TECHNICAL FEATURES TO DRIVE MARKET

- 18.4.2 ENGINE HARNESS

- 18.4.3 CHASSIS HARNESS

- 18.4.4 BODY & LIGHTING HARNESS

- 18.4.5 HVAC HARNESS

- 18.4.6 DASHBOARD/CABIN HARNESS

- 18.4.7 BATTERY HARNESS

- 18.4.8 DOOR HARNESS

- 18.4.9 INFOTAINMENT HARNESS

- 18.4.10 ACTIVE & PASSIVE SAFETY HARNESS

- 18.4.11 ADAS HARNESS

- 18.4.12 ROOF HARNESS

- 18.4.13 SEAT HARNESS

- 18.4.14 OTHER/AUXILIARY HARNESSES

- 18.5 BUSES

- 18.5.1 EXPANSION OF PUBLIC TRANSPORTATION SERVICES TO DRIVE MARKET

- 18.5.2 ENGINE HARNESS

- 18.5.3 CHASSIS HARNESS

- 18.5.4 BODY & LIGHTING HARNESS

- 18.5.5 HVAC HARNESS

- 18.5.6 DASHBOARD/CABIN HARNESS

- 18.5.7 BATTERY HARNESS

- 18.5.8 DOOR HARNESS

- 18.5.9 INFOTAINMENT HARNESS

- 18.5.10 ACTIVE & PASSIVE SAFETY HARNESS

- 18.5.11 ADAS HARNESS

- 18.5.12 SEAT HARNESS

- 18.5.13 OTHER/AUXILIARY HARNES

- 18.6 TRUCKS

- 18.6.1 HIGH NUMBER OF WIRING HARNESSES OWING TO LARGE SIZE TO DRIVE MARKET

- 18.6.2 ENGINE HARNESS

- 18.6.3 CHASSIS HARNESS

- 18.6.4 BODY & LIGHTING HARNESS

- 18.6.5 HVAC HARNESS

- 18.6.6 DASHBOARD/CABIN HARNESS

- 18.6.7 BATTERY HARNESS

- 18.6.8 DOOR HARNESS

- 18.6.9 INFOTAINMENT HARNESS

- 18.6.10 ACTIVE & PASSIVE SAFETY HARNESS

- 18.6.11 ADAS HARNESS

- 18.6.12 SEAT HARNESS

- 18.6.13 OTHER/AUXILIARY HARNES

- 18.7 INDUSTRY INSIGHTS

19 AUTOMOTIVE WIRING HARNESS MARKET FOR ICE VEHICLES, BY COMPONENT

- 19.1 INTRODUCTION

- 19.2 CONNECTORS

- 19.2.1 GROWING TREND OF HIGH-VOLTAGE CONNECTORS TO DRIVE MARKET

- 19.3 WIRES

- 19.3.1 INCREASING ADOPTION OF ADAS FEATURES IN VEHICLES TO DRIVE MARKET

- 19.4 TERMINALS

- 19.4.1 INCREASING PRODUCTION OF HEVS TO DRIVE MARKET

- 19.5 OTHERS

- 19.6 INDUSTRY INSIGHTS

20 AUTOMOTIVE WIRING HARNESS MARKET, BY CATEGORY

- 20.1 INTRODUCTION

- 20.2 GENERAL WIRES

- 20.3 HEAT-RESISTANT WIRES

- 20.4 SHIELDED WIRES

- 20.5 TUBED WIRES

21 AUTOMOTIVE WIRING HARNESS MARKET FOR ICE VEHICLES, BY APPLICATION

- 21.1 INTRODUCTION

- 21.2 NUMBER OF HARNESSES IN PREMIUM CARS, BY APPLICATION

- 21.3 ENGINE HARNESS

- 21.3.1 REQUIREMENT OF SAFETY FEATURES AS PER GOVERNMENT MANDATES TO DRIVE MARKET

- 21.4 CHASSIS HARNESS

- 21.4.1 RISE IN SAFETY FEATURES TO DRIVE MARKET

- 21.5 BODY & LIGHTING HARNESS

- 21.5.1 BODY AND LIGHTING WIRING HARNESS IS RESPONSIBLE FOR POWERING AND CONTROLLING EXTERIOR AND INTERIOR LIGHTING, AS WELL AS VARIOUS BODY ELECTRONICS

- 21.6 HVAC HARNESS

- 21.7 DASHBOARD/CABIN HARNESS

- 21.7.1 INTRODUCTION OF NEW INTERACTIVE FEATURES IN DASHBOARDS TO DRIVE MARKET

- 21.8 BATTERY HARNESS

- 21.8.1 GROWING NUMBER OF CONNECTORS USED THROUGH BATTERIES IN VEHICLES TO DRIVE MARKET

- 21.9 SEAT HARNESS

- 21.9.1 GROWTH OF LUXURY VEHICLES TO DRIVE MARKET

- 21.10 DOOR HARNESS

- 21.10.1 INCREASING PENETRATION OF LUXURY SEGMENT VEHICLES IN DEVELOPED ECONOMIES TO DRIVE MARKET

- 21.11 INFOTAINMENT HARNESS

- 21.11.1 INCREASE IN DEMAND FOR PREMIUM CARS TO DRIVE MARKET

- 21.12 ACTIVE & PASSIVE HARNESS

- 21.12.1 INCREASE IN DEMAND FOR SAFETY FEATURES TO DRIVE MARKET

- 21.13 ADAS HARNESS

- 21.13.1 INCREASE IN DEMAND FOR SAFETY FEATURES TO DRIVE MARKET

- 21.14 ROOF HARNESS

- 21.14.1 INCREASE IN DEMAND FOR SAFETY FEATURES TO BOOST GROWTH

- 21.15 OTHER/AUXILIARY HARNESSES

- 21.15.1 INCREASE IN DEMAND FOR SAFETY FEATURES TO DRIVE MARKET

- 21.16 INDUSTRY INSIGHTS

22 48V AND EV WIRING HARNESS ARCHITECTURE

- 22.1 GROWING TREND OF VEHICLE ELECTRIFICATION

- 22.2 NEW AND UPCOMING ELECTRIC VEHICLE MODELS, 2025-2027

- 22.3 OEMS AND THEIR EV INVESTMENTS

- 22.4 NEED FOR 48 V ARCHITECTURE

- 22.4.1 REDUCED CO2 EMISSIONS TO IMPROVE FUEL ECONOMY

- 22.4.2 ENGINE DOWNSIZING TO IMPROVE DRIVABILITY

- 22.5 IMPACT OF 48 V ARCHITECTURE ON AUTOMOTIVE WIRING HARNESS

- 22.5.1 IMPACT ON WIRING HARNESS

- 22.5.2 ELECTRIC VEHICLE WIRING HARNESS

- 22.5.2.1 Pipe-shielded wiring harness

- 22.5.2.2 Power cable

- 22.5.2.3 Direct connector

- 22.6 48 V PASSENGER CAR WIRING HARNESS MARKET, BY REGION

- 22.6.1 ASIA PACIFIC

- 22.6.2 EUROPE

- 22.6.3 NORTH AMERICA

23 ICE VEHICLE WIRING HARNESS MARKET, BY REGION

- 23.1 INTRODUCTION

- 23.2 ASIA PACIFIC

- 23.2.1 CHINA

- 23.2.1.1 Increasing production of passenger cars to drive market

- 23.2.2 JAPAN

- 23.2.2.1 Introduction of advanced technologies and demand for enhanced safety and comfort to drive market

- 23.2.3 SOUTH KOREA

- 23.2.3.1 Growing demand for passenger cars to drive market

- 23.2.4 INDIA

- 23.2.4.1 Government support to boost passenger car sales to drive market

- 23.2.5 THAILAND

- 23.2.5.1 High production of LCVs to drive market

- 23.2.6 REST OF ASIA PACIFIC

- 23.2.1 CHINA

- 23.3 EUROPE

- 23.3.1 GERMANY

- 23.3.1.1 Demand for all vehicle types to drive market

- 23.3.2 FRANCE

- 23.3.2.1 Incorporation of premium features in buses to drive market

- 23.3.3 UK

- 23.3.3.1 Increasing sales of premium cars to drive market

- 23.3.4 SPAIN

- 23.3.4.1 Growing demand for luxury vehicles to drive market

- 23.3.5 RUSSIA

- 23.3.5.1 Demand for LCVs to drive market

- 23.3.6 ITALY

- 23.3.6.1 Growing ICE vehicle production to drive market

- 23.3.7 REST OF EUROPE

- 23.3.1 GERMANY

- 23.4 NORTH AMERICA

- 23.4.1 US

- 23.4.1.1 Increasing number of premium features in passenger cars to drive market

- 23.4.2 CANADA

- 23.4.2.1 Growing passenger car production to drive market

- 23.4.3 MEXICO

- 23.4.3.1 Increase in demand for trucks to drive market

- 23.4.1 US

- 23.5 REST OF THE WORLD (ROW)

- 23.5.1 BRAZIL

- 23.5.1.1 Growth of passenger car sales to drive market

- 23.5.2 SOUTH AFRICA

- 23.5.2.1 Rising passenger car and commercial vehicle production to drive market

- 23.5.3 OTHERS

- 23.5.4 INDUSTRY INSIGHTS

- 23.5.1 BRAZIL

24 COMPETITIVE LANDSCAPE

- 24.1 OVERVIEW

- 24.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 24.3 REVENUE ANALYSIS OF KEY PLAYERS

- 24.4 MARKET SHARE ANALYSIS, 2025

- 24.4.1 MARKET SHARE ANALYSIS: AUTOMOTIVE WIRING HARNESS, JAPAN, 2025

- 24.4.2 MARKET SHARE ANALYSIS: AUTOMOTIVE WIRING HARNESS, INDIA, 2025

- 24.4.3 KEY PLAYER RANKING: AUTOMOTIVE WIRING HARNESS MARKET, EUROPE, 2025

- 24.4.4 KEY PLAYER RANKING: AUTOMOTIVE WIRING HARNESS MARKET, CHINA, 2025

- 24.4.5 KEY PLAYER RANKING: AUTOMOTIVE WIRING HARNESS MARKET, THAILAND, 2025

- 24.5 BRAND COMPARISON

- 24.6 COMPANY EVALUATION MATRIX: KEY PLAYERS (AUTOMOTIVE WIRING HARNESS SUPPLIERS)

- 24.6.1 STARS

- 24.6.2 EMERGING LEADERS

- 24.6.3 PERVASIVE PLAYERS

- 24.6.4 PARTICIPANTS

- 24.6.5 COMPANY FOOTPRINT

- 24.7 COMPANY EVALUATION MATRIX: KEY PLAYERS (ELECTRIC VEHICLE WIRING HARNESS MANUFACTURERS)

- 24.7.1 STARS

- 24.7.2 EMERGING LEADERS

- 24.7.3 PERVASIVE

- 24.7.4 PARTICIPANTS

- 24.7.5 COMPANY FOOTPRINT

- 24.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES (AUTOMOTIVE WIRING HARNESS MANUFACTURERS)

- 24.8.1 PROGRESSIVE COMPANIES

- 24.8.2 RESPONSIVE COMPANIES

- 24.8.3 DYNAMIC COMPANIES

- 24.8.4 STARTING BLOCKS

- 24.9 COMPETITIVE BENCHMARKING

- 24.10 COMPANY VALUATION

- 24.11 COMPANY FINANCIAL METRICS

- 24.12 COMPETITIVE SCENARIO

- 24.12.1 PRODUCT LAUNCHES

- 24.12.2 DEALS

- 24.12.3 EXPANSION

25 COMPANY PROFILES

- 25.1 KEY PLAYERS

- 25.1.1 SUMITOMO ELECTRIC INDUSTRIES, LTD.

- 25.1.1.1 Business overview

- 25.1.1.2 Products offered

- 25.1.1.3 Recent developments

- 25.1.1.3.1 Product launches

- 25.1.1.3.2 Deals

- 25.1.1.3.3 Expansion

- 25.1.1.4 MnM view

- 25.1.1.4.1 Key strengths

- 25.1.1.4.2 Strategic choices

- 25.1.1.4.3 Weaknesses and competitive threats

- 25.1.2 YAZAKI CORPORATION

- 25.1.2.1 Business overview

- 25.1.2.2 Products offered

- 25.1.2.3 Recent developments

- 25.1.2.3.1 Deals

- 25.1.2.3.2 Expansion

- 25.1.2.4 MnM view

- 25.1.2.4.1 Key strengths

- 25.1.2.4.2 Strategic choices

- 25.1.2.4.3 Weaknesses and competitive threats

- 25.1.3 APTIV.

- 25.1.3.1 Business overview

- 25.1.3.2 Products offered

- 25.1.3.3 Recent developments

- 25.1.3.3.1 Product launches

- 25.1.3.3.2 Deals

- 25.1.3.3.3 Expansion

- 25.1.3.3.4 Other developments

- 25.1.3.4 MnM view

- 25.1.3.4.1 Key strengths

- 25.1.3.4.2 Strategic choices

- 25.1.3.4.3 Weaknesses and competitive threats

- 25.1.4 LEONI AG

- 25.1.4.1 Business overview

- 25.1.4.2 Products offered

- 25.1.4.3 Recent developments

- 25.1.4.3.1 Product launches

- 25.1.4.3.2 Deals

- 25.1.4.3.3 Expansion

- 25.1.4.3.4 Other developments

- 25.1.4.4 MnM view

- 25.1.4.4.1 Key strengths

- 25.1.4.4.2 Strategic choices

- 25.1.4.4.3 Weaknesses and competitive threats

- 25.1.5 FURUKAWA ELECTRIC CO., LTD.

- 25.1.5.1 Business overview

- 25.1.5.2 Products offered

- 25.1.5.3 Recent developments

- 25.1.5.3.1 Product launches

- 25.1.5.3.2 Deals

- 25.1.5.3.3 Expansion

- 25.1.5.4 MnM view

- 25.1.5.4.1 Key strengths

- 25.1.5.4.2 Strategic choices

- 25.1.5.4.3 Weaknesses and competitive threats

- 25.1.6 NEXANS

- 25.1.6.1 Business overview

- 25.1.6.2 Products offered

- 25.1.6.3 Recent developments

- 25.1.6.3.1 Deals

- 25.1.7 LEAR

- 25.1.7.1 Business overview

- 25.1.7.2 Products offered

- 25.1.7.3 Recent developments

- 25.1.7.3.1 Deals

- 25.1.8 FUJIKURA LTD.

- 25.1.8.1 Business overview

- 25.1.8.2 Products offered

- 25.1.8.3 Recent developments

- 25.1.8.3.1 Product launches

- 25.1.8.3.2 Deals

- 25.1.9 MOTHERSON

- 25.1.9.1 Business overview

- 25.1.9.2 Products offered

- 25.1.9.3 Recent developments

- 25.1.9.3.1 Deals

- 25.1.9.3.2 Expansion

- 25.1.10 GEBAUER & GRILLER GROUP

- 25.1.10.1 Business overview

- 25.1.10.2 Products offered

- 25.1.10.3 Recent developments

- 25.1.10.3.1 Expansion

- 25.1.10.3.2 Others

- 25.1.1 SUMITOMO ELECTRIC INDUSTRIES, LTD.

- 25.2 OTHER PLAYERS

- 25.2.1 PRYSMAIN GROUP

- 25.2.2 CYPRESS INDUSTRIES

- 25.2.3 KROMBERG & SCHUBERT AUTOMOTIVE GMBH & CO. KG

- 25.2.4 DRAXLMAIER GROUP

- 25.2.5 KE ELEKTRONIK GMBH

- 25.2.6 FINTALL OY

- 25.2.7 COROPLAST FRITZ MULLER GMBH & CO. KG

- 25.2.8 CZECH REPUBLIC ONAMBA

- 25.2.9 SPARK MINDA

- 25.2.10 TBH GROUP

- 25.2.11 YURA CORP

- 25.2.12 SAISON ELECTRONICS LTD.

- 25.2.13 SHENZHEN DEREN ELECTRONICS CO., LTD

- 25.2.14 UNITY HARNESS LIMITED

- 25.2.15 HESTO HARNESS

- 25.2.16 BRASCABOS

- 25.2.17 THAI SUMMIT GROUP

26 RESEARCH METHODOLOGY

- 26.1 RESEARCH DATA

- 26.1.1 SECONDARY DATA

- 26.1.1.1 List of key secondary sources to estimate vehicle production

- 26.1.1.2 List of key secondary sources to estimate market size

- 26.1.1.3 Key data from secondary sources

- 26.1.2 PRIMARY DATA

- 26.1.2.1 List of primary participants

- 26.1.1 SECONDARY DATA

- 26.2 MARKET ESTIMATION METHODOLOGY

- 26.2.1 BOTTOM-UP APPROACH: BY REGION AND APPLICATION

- 26.2.2 TOP-DOWN APPROACH

- 26.3 DATA TRIANGULATION

- 26.3.1 FACTOR ANALYSIS FOR MARKET SIZING: DEMAND AND SUPPLY SIDES

- 26.4 FACTOR ANALYSIS

- 26.5 RESEARCH ASSUMPTIONS

- 26.6 RESEARCH LIMITATIONS

27 RECOMMENDATIONS BY MARKETSANDMARKETS

- 27.1 ASIA PACIFIC TO DOMINATE AUTOMOTIVE WIRING HARNESS MARKET

- 27.2 OPTICAL FIBER WIRES FOR FUTURE APPLICATIONS: KEY FOCUS AREAS

- 27.3 ALUMINUM WIRING HARNESS FOR FUTURE APPLICATIONS: KEY FOCUS AREAS

- 27.4 HIGH-VOLTAGE WIRING HARNESS TO OFFER GROWTH OPPORTUNITY TO MARKET PLAYERS

- 27.5 CONCLUSION

28 APPENDIX

- 28.1 INSIGHTS FROM INDUSTRY EXPERTS

- 28.2 DISCUSSION GUIDE

- 28.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 28.4 CUSTOMIZATION OPTIONS

- 28.4.1 AUTOMOTIVE WIRING HARNESS MARKET (ICE), BY APPLICATION & REGION

- 28.4.1.1 Asia Pacific

- 28.4.1.1.1 China

- 28.4.1.1.2 India

- 28.4.1.1.3 Japan

- 28.4.1.1.4 South Korea

- 28.4.1.1.5 Thailand

- 28.4.1.1.6 Rest of Asia Pacific

- 28.4.1.2 Europe

- 28.4.1.2.1 Germany

- 28.4.1.2.2 France

- 28.4.1.2.3 UK

- 28.4.1.2.4 Spain

- 28.4.1.2.5 Russia

- 28.4.1.2.6 Italy

- 28.4.1.2.7 Rest of Europe

- 28.4.1.3 North America

- 28.4.1.3.1 US

- 28.4.1.3.2 Canada

- 28.4.1.3.3 Mexico

- 28.4.1.4 Rest of the World

- 28.4.1.4.1 Brazil

- 28.4.1.4.2 South Africa

- 28.4.1.4.3 Others

- 28.4.1.1 Asia Pacific

- 28.4.2 AUTOMOTIVE WIRING HARNESS MARKET (EV), BY TYPE & REGION

- 28.4.2.1 Asia Pacific

- 28.4.2.1.1 China

- 28.4.2.1.2 India

- 28.4.2.1.3 Japan

- 28.4.2.1.4 South Korea

- 28.4.2.1.5 Thailand

- 28.4.2.1.6 Rest of Asia Pacific

- 28.4.2.2 Europe

- 28.4.2.2.1 Germany

- 28.4.2.2.2 France

- 28.4.2.2.3 UK

- 28.4.2.2.4 Spain

- 28.4.2.2.5 Russia

- 28.4.2.2.6 Italy

- 28.4.2.2.7 Rest of Europe

- 28.4.2.3 North America

- 28.4.2.3.1 US

- 28.4.2.3.2 Canada

- 28.4.2.3.3 Mexico

- 28.4.2.1 Asia Pacific

- 28.4.3 DETAILED ANALYSIS AND PROFILING OF ADDITIONAL MARKET PLAYERS (UP TO 3)

- 28.4.1 AUTOMOTIVE WIRING HARNESS MARKET (ICE), BY APPLICATION & REGION

- 28.5 RELATED REPORTS

- 28.6 AUTHOR DETAILS