|

시장보고서

상품코드

2035084

자동차 와이어링 하네스 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Wiring Harness - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

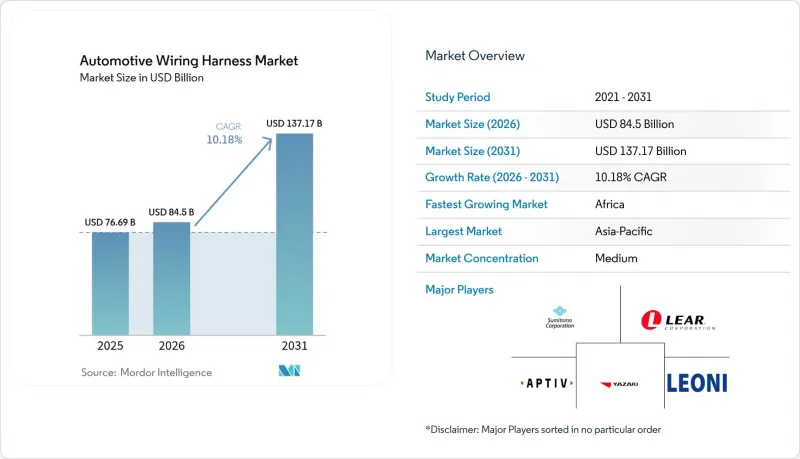

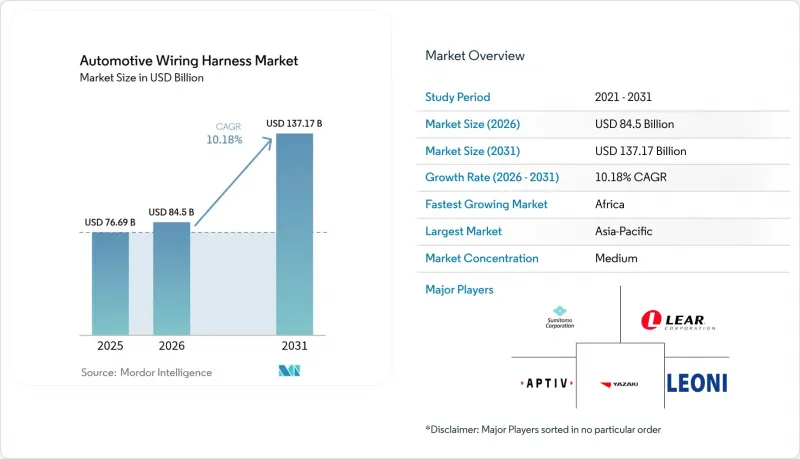

2026년 자동차 와이어링 하네스 시장 규모는 845억 달러로 추정되고 있어 2025년 766억 9,000만 달러에서 확대해, 2031년에는 1,371억 7,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 10.18%를 나타낼 것으로 예측됩니다.

대당 전자부품 증가를 배경으로 시장은 꾸준히 성장하고 있지만, 이 표면적인 성장률의 이면에는 두 가지 상반된 경향이 숨어있습니다. 배터리 전기자동차(BEV)에 사용되는 고전압 하네스 수요는 두 자릿수 속도로 증가하고 있는 반면, 기존 저전압 내연기관(ICE) 하네스는 가격 하락이 진행되고 있습니다. 지역별로 보면, 아시아는 여전히 생산과 소비의 중심지이며, 아프리카는 유리한 인건비와 현지 조달 규제 덕분에 새로운 생산 능력을 유치하고 있습니다. 한편, 북미와 유럽의 성숙한 시장에서는 케이블 배선 거리를 줄이면서 나머지 각 배선의 가치를 높이는 구역형 전기 아키텍처로의 전환이 진행되고 있습니다.

세계 자동차 와이어링 하네스 시장 동향과 인사이트

전동화에 따른 고전압 하네스 수요 급증

배터리 팩의 전압이 800V, 심지어 1000V까지 상승함에 따라 엄격한 전자기 호환성(EMC) 기준을 충족하면서 더 큰 열 부하를 전달할 수 있는 새로운 등급의 케이블 어셈블리가 요구되고 있습니다. 현재 많은 중국 브랜드가 주 구동 라인에 알루미늄 도체를 지정하고 있으며, 재료의 혁신은 EV의 비용 절감과 직결되어 있습니다. 알루미늄은 새로운 접합 기술이 필요하기 때문에 공급업체들은 5년 전만 해도 볼 수 없었던 속도로 마찰 용접 및 레이저 용접 장비에 투자하고 있습니다. 이를 통해 도출되는 새로운 관점은 경쟁의 중요한 장벽으로 구리 조달보다 용접 노하우가 곧 중요하게 여겨질 수 있다는 것입니다.

OEM은 경량 알루미늄 및 광섬유 하네스를 홍보합니다.

자동차 제조업체들은 1g 단위의 경량화를 지속적으로 추구하고 있으며, 고급차에서는 배선만 20kg 이상을 차지하기도 합니다. 알루미늄 도체는 구리에 비해 질량을 약 60% 줄일 수 있을 뿐만 아니라, 구리 가격 변동 위험도 줄일 수 있습니다. 전도도 저하라는 단점은 접촉 저항을 사양 범위 내로 유지하는 다심 설계와 바이메탈 단자에 의해 상쇄되고 있습니다. 연결 기술이 성숙함에 따라 여러 OEM이 알루미늄 전력선과 데이터용 광섬유를 결합한 혼합 도체 하네스를 도입하고 있으며, 이는 단일 금속 솔루션이 아닌 하이브리드 복합 번들이 다음 개척지가 될 것임을 시사하고 있습니다.

구리 및 수지 가격 변동으로 인한 수익률에 대한 압력

기존 하네스에서 구리는 부품 원가의 절반 이상을 차지하기 때문에 최근 가격 변동으로 인해 공급업체의 총 이익률이 압박을 받고 있습니다. 대부분의 라인 핏 계약에는 가격 전가 조항이 포함되어 있지만, 자동차 제조업체는 생산주기 중간에 가격 인상을 받아들이는 것을 점점 더 꺼려하고 있습니다. 따라서 공급업체들은 위험분산 차원에서 상품거래소에서 헤지를 하거나 알루미늄으로 다변화를 추진하기도 합니다. 이러한 상황은 수익성 확보에 있어 재무 설계 및 조달 전략의 고도화가 핵심 엔지니어링 못지않게 중요해지고 있다는 것을 보여줍니다.

부문 분석

2025년 자동차 와이어링 하네스 시장 규모에서 차체, 조명 및 실내 편의 시스템이 가장 큰 비중을 차지하며 시장 규모의 35.35%를 차지했습니다. LED의 높은 보급률, 파워 리프트 게이트 및 멀티존 공조 모듈이 지속적인 수요의 배경이 되고 있습니다. 흥미롭게도, 판매량을 증가시키는 이러한 편의 장비는 동시에 최종 차량 조립을 복잡하게 만들기 때문에 OEM 업체들은 대시보드나 도어 패널에 꽂기만 하면 되는 사전 구성된 서브 하네스를 요구하고 있습니다.

충전 및 전원 시스템용 하네스는 2031년까지 연평균 복합 성장률(CAGR) 25.44%로 가장 높은 성장률을 보일 것으로 예상되며, 전기자동차 모델의 판매점 도입이 증가함에 따라 10%대 중반의 성장률을 유지할 것으로 예측됩니다. 이러한 하네스는 배터리 팩 주변의 급격한 온도 상승과 기계적 진동을 견뎌내야 하기 때문에 고성능 절연 재료가 주류가 되고 있습니다. 액체 냉각 슬리브 및 박형 실드 기술을 습득한 공급업체는 높은 가격대로 판매할 수 있을 것입니다. 향후 고전압 배선에 대한 전문 지식이 배터리 관리 시스템으로의 교차 판매의 디딤돌이 될 수 있습니다.

구리는 독보적인 전기 전도성과 100년의 제조 노하우를 바탕으로 현재도 자동차 와이어링 하네스 시장에서 약 93.45%의 점유율을 유지하고 있습니다. 그러나 고밀도와 가격 변동성으로 인해 OEM 구매 부서는 대체 소재를 찾아야 하는 상황에 처해 있습니다. 새로운 트렌드로 구리 데이터 페어와 알루미늄 전원 코어를 동일한 간선에 묶어 신호의 무결성을 유지하면서 경량화를 실현하는 방식이 주목받고 있습니다.

알루미늄의 예상 CAGR은 2031년까지 11.95%를 나타낼 것으로 예측되며, 이는 전체 자동차 와이어링 하네스 산업의 성장 궤도를 쉽게 능가할 것으로 예측됩니다. 내식성 단자 및 마찰 용접 연결 기술의 발전으로 인해 과거 신뢰성에 대한 우려는 사라졌습니다. 알루미늄은 구리에 비해 가격이 안정적이기 때문에 금융권에서 헤지 수단으로 활용하는 사례가 늘고 있습니다. 이러한 변화는 주요 공급업체 내부에서 재료과학의 선택이 재무적 리스크 관리 전략과 직접적으로 연관되어 있음을 보여줍니다.

지역별 분석

아시아태평양은 자동차 와이어링 하네스 시장 점유율의 약 48.40%를 차지하고 있으며, 절대적인 매출 성장이 가장 빠릅니다. 중국은 방대한 경차 생산량과 탄탄한 전기차 공급망을 통해 이 지역의 중심적인 역할을 하고 있으며, 일본과 한국은 데이터 및 고전압 용도를 위한 고도의 연구개발(R&D)에 기여하고 있습니다. 인도와 동남아시아의 전기화에 대한 정부 인센티브는 세계 성장이 정상화되더라도 이 지역 수요는 견고하게 유지될 것임을 시사합니다. 주목할 만한 동향으로, 여러 중국 OEM이 유럽에 EV를 수출하고 있으며, 유럽연합(EU)의 규제 기준을 충족하는 통일된 배선 사양을 요구하고 있기 때문에 아시아에 기반을 둔 공급업체들도 세계 컴플라이언스 표준에 대응해야 합니다.

아프리카는 2026년부터 2031년까지 11.79%의 가장 높은 CAGR을 기록했습니다. 경쟁력 있는 인건비, 유럽연합(EU)과의 무역협정을 통한 접근성, 그리고 정부의 산업단지 정책이 결합되어 새로운 하네스 투자를 불러일으키고 있습니다. 유럽의 여러 Tier 1 기업들은 노동집약적인 서브 어셈블리를 이 지역에 배치하여 본국 공장에서 자동화 공정에 집중할 수 있도록 하고 있습니다. 케이블 압착 및 품질 검사에 대한 현지 인력의 숙련도 향상 프로그램이 등장하여 인적 자본 전략이 지역 성장과 밀접한 관련이 있음을 보여줍니다.

북미와 유럽의 성장은 더 완만하지만, 기술의 최첨단을 달리고 있습니다. 구역별 아키텍처의 시범 프로젝트는 독일의 고급 브랜드와 북미 전기자동차 스타트업에 집중되어 있으며, 뮌헨, 슈투트가르트, 실리콘밸리의 디자인 사무실이 차세대 와이어링 하네스 컨셉의 중심지 역할을 하고 있습니다. 이러한 추세는 지적재산권 창출이 노동집약적 생산과 분리되고 있음을 시사합니다. 이에 따라 OEM 본사 인근에 연구개발(R&D) 클러스터가 형성되고, 대량 생산 조립 공정이 비용 최적화된 지역으로 이동하는 '양극화된 세계 전개'가 더욱 강화되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20Automotive Wiring Harness Market size in 2026 is estimated at USD 84.5 billion, growing from 2025 value of USD 76.69 billion with 2031 projections showing USD 137.17 billion, growing at 10.18% CAGR over 2026-2031.

The market is expanding steadily on the back of rising electronic content per vehicle, but the headline growth masks two contrasting currents: demand for high-voltage harnesses used in battery-electric vehicles is rising at a double-digit pace, while traditional low-voltage ICE looms are seeing price compression. Regionally, Asia remains the production and consumption hub, Africa is attracting new capacity thanks to favorable labor economics and local-content rules, and mature markets in North America and Europe are pivoting toward zonal electrical architectures that shorten cable runs yet increase the value of each remaining line.

Global Automotive Wiring Harness Market Trends and Insights

Electrification-Driven Surge in High-Voltage Harness Demand

Rising battery pack voltages to 800 V and even 1000 V are spurring a new class of cable assemblies that carry greater thermal loads while meeting tight electromagnetic-compatibility (EMC) targets. Many Chinese brands now specify aluminum-based conductors for main traction lines, directly linking material innovation to EV cost reduction. Because aluminum requires revised joining techniques, suppliers are investing in friction and laser welding cells at a pace unseen five years ago. An emerging inference is that welding know-how may soon overshadow raw copper sourcing as the key competitive barrier.

OEM Push for Lightweight Aluminum and Optical Harnesses

Automakers continue to chase every gram of weight saving, and wiring can account for more than 20 kg in premium cars. Aluminum conductors slash mass by roughly 60% relative to copper and also cut exposure to copper-price swings. The downside-lower conductivity-is being offset through multi-strand designs and bimetal terminals that keep contact resistance within specification. As connection technology matures, several OEMs have introduced mixed conductor looms that pair aluminum power lines with optical fibres for data, hinting that the next frontier will lie in hybrid composite bundles rather than single-metal solutions.

Margin Pressure from Volatile Copper and Resin Prices

Copper accounts for well over half of total bill-of-materials cost in a conventional loom, so recent price gyrations have compressed supplier gross margin. Although most line-fit contracts include pass-through clauses, automakers are increasingly reluctant to accept mid-cycle price increases. Suppliers are therefore hedging on commodity exchanges and diversifying into aluminum as a risk-spreading measure. The situation underscores that financial engineering and procurement sophistication are becoming as important as core engineering in safeguarding profitability.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Centralized Zonal E/E Architectures in Premium Cars

- Regulatory Mandates for ADAS Wiring Redundancy

- EV-Specific Thermal and EMC Challenges Raising Validation Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Body, Lighting, and Cabin Comfort systems command the largest share of the Automotive Wiring Harness market size in 2025, accounting for 35.35% of the market size. High LED adoption, power lift-gates, and multi-zone climate modules explain persistent demand. An interesting observation is that the same comfort features that boost volume also complicate final vehicle assembly, nudging OEMs to request pre-configured sub-looms that snap into dashboards and door panels.

Charging and power supply system harnesses show the fastest forecast CAGR expanding at an 25.44% through 2031, expanding in the mid-teens as more electric models reach showrooms. These harnesses must endure temperature spikes and mechanical vibration around battery packs, so higher-grade insulation materials are becoming mainstream. Suppliers that master liquid-cooling sleeves and low-profile shielding will likely command premium price points. Over time, expertise in high-voltage routing may provide cross-selling entry into battery management systems.

Copper retains around 93.45% of the Automotive Wiring Harness market share today, supported by unmatched conductivity and a century of process know-how. Yet its density and volatile cost profile keep pressure on OEM purchasing departments to pursue alternatives. An emerging pattern is the bundling of copper data pairs with aluminum power cores in the same trunk line, achieving weight reduction without sacrificing signal integrity.

Aluminum's forecast CAGR is 11.95% by 2031, easily outpacing the broader Automotive Wiring Harness industry trajectory. Advances in anti-corrosion terminals and friction-weld splice techniques have removed earlier reliability concerns. Because aluminum is price-stable relative to copper, finance teams increasingly model its use as a hedge. The shift indicates that material science choices now intersect directly with treasury risk management strategies inside large suppliers.

The Automotive Wiring Harness Market Report is Segmented by Application Type (Ignition System, and More), Conductor Material (Copper, and More), Voltage Rating (Low-Voltage [less Than 60V] and More), Propulsion Type (Internal Combustion Engine Vehicles and More), Vehicle Type (Passenger Cars and More), Sales Channel (OEM and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia Pacific holds almost 48.40% Automotive Wiring Harness market share and boasts the fastest absolute revenue expansion. China anchors the region through its vast light-vehicle output and deep EV supply chains, while Japan and South Korea contribute high-grade R&D for data and high-voltage applications. Government incentives for electrification in India and Southeast Asia suggest that regional demand will remain resilient even as global growth normalises. A noteworthy development is that multiple Chinese OEMs are exporting EVs to Europe, requiring harmonised wiring specifications that meet European Union regulatory norms and thus elevating Asia-based suppliers to global compliance standards.

Africa, records the highest CAGR of 11.79% between 2026-2031. Competitive labour costs, trade-agreement access to the European Union, and government industrial-park policies together attract fresh harness investment. Several European tier-1 firms are locating high-labour-content sub-assemblies in the region, freeing up home-market plants for automated processes. Local workforce up-skilling programs in cable crimping and quality inspection are emerging, indicating that human-capital strategy is entwined with regional growth.

North America and Europe grow more modestly but remain technology front-runners. Zonal architecture pilots are concentrated in German luxury brands and North American electric start-ups, so design offices in Munich, Stuttgart, and Silicon Valley serve as nerve centres for next-generation loom concepts. This pattern implies that intellectual property creation is decoupling from labour-intensive production. This reinforces the two-speed global footprint in which R&D clusters near OEM headquarters and large-batch assembly migrate to cost-optimised regions.

- Yazaki Corporation

- Sumitomo Electric Industries Ltd.

- LEONI AG

- Lear Corporation

- Motherson Wiring Harness Ltd.

- Furukawa Electric Co. Ltd.

- Fujikura Ltd.

- Kyungshin Corporation

- Draexlmaier Group

- Kromberg & Schubert

- Nexans Autoelectric

- PKC Group (Motherson)

- Coroplast Fritz Muller GmbH & Co.

- THB Group

- Prestolite Wire LLC

- Lear Yangzhou (China)

- Guangdong Hivolt Wiring Harness

- BizLink Holding Inc.

- Shanghai Shenglong Automotive Harness

- Samvardhana Motherson Reydel

- Korea Electric Terminal Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Electrification-Driven Surge in High-Voltage Harness Demand (Asia)

- 4.1.2 OEM Push for Lightweight Aluminum & Optical Harnesses

- 4.1.3 Shift Toward Centralized Zonal E/E Architectures in Premium Cars (EU)

- 4.1.4 Regulatory Mandates for ADAS Wiring Redundancy (US, Japan)

- 4.1.5 Rising Local Content Rules Fueling Wire-Harness Localization (India, Mexico)

- 4.1.6 Autonomous Vehicle Development Driving Redundant Circuit Architectures

- 4.2 Market Restraints

- 4.2.1 Margin Pressure From Volatile Copper & Resin Prices

- 4.2.2 EV-Specific Thermal & EMC Challenges Raising Validation Costs

- 4.2.3 Mismatch Between Design Complexity & Skilled Labor Availability (ASEAN)

- 4.2.4 Manufacturing Automation Limitations Constraining Productivity Gains

- 4.3 Value / Supply-Chain Analysis

- 4.4 Regulatory & Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Ignition System

- 5.1.2 Charging & Power Supply System

- 5.1.3 Drivetrain & Powertrain (ICE)

- 5.1.4 High-Voltage Traction Harness (xEV)

- 5.1.5 Infotainment, Cockpit & Telematics

- 5.1.6 ADAS & Safety Control

- 5.1.7 Body, Lighting & Cabin Comfort

- 5.2 By Conductor Material

- 5.2.1 Copper

- 5.2.2 Aluminum

- 5.3 By Voltage Rating

- 5.3.1 Low-Voltage (<60 V)

- 5.3.2 High-Voltage (60-1,000 V)

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine Vehicles

- 5.4.2 Battery Electric Vehicles

- 5.4.3 Plug-in Hybrid & Hybrid Vehicles

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Light Commercial Vehicles

- 5.5.3 Heavy-duty Trucks & Buses

- 5.6 By Sales Channel

- 5.6.1 OEM

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Spain

- 5.7.2.5 Russia

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia Pacific

- 5.7.4 Middle East

- 5.7.4.1 GCC

- 5.7.4.2 Turkey

- 5.7.4.3 Rest of Middle East

- 5.7.5 Africa

- 5.7.5.1 South Africa

- 5.7.5.2 Egypt

- 5.7.5.3 Rest of Africa

- 5.7.6 South America

- 5.7.6.1 Brazil

- 5.7.6.2 Argentina

- 5.7.6.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Strategic Initiatives

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Yazaki Corporation

- 6.3.2 Sumitomo Electric Industries Ltd.

- 6.3.3 LEONI AG

- 6.3.4 Lear Corporation

- 6.3.5 Motherson Wiring Harness Ltd.

- 6.3.6 Furukawa Electric Co. Ltd.

- 6.3.7 Fujikura Ltd.

- 6.3.8 Kyungshin Corporation

- 6.3.9 Draexlmaier Group

- 6.3.10 Kromberg & Schubert

- 6.3.11 Nexans Autoelectric

- 6.3.12 PKC Group (Motherson)

- 6.3.13 Coroplast Fritz Muller GmbH & Co.

- 6.3.14 THB Group

- 6.3.15 Prestolite Wire LLC

- 6.3.16 Lear Yangzhou (China)

- 6.3.17 Guangdong Hivolt Wiring Harness

- 6.3.18 BizLink Holding Inc.

- 6.3.19 Shanghai Shenglong Automotive Harness

- 6.3.20 Samvardhana Motherson Reydel

- 6.3.21 Korea Electric Terminal Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment