|

시장보고서

상품코드

1435768

세라믹 기판 : 시장 점유율 분석, 산업 동향, 성장 예측(2024-2029년)Ceramic Substrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

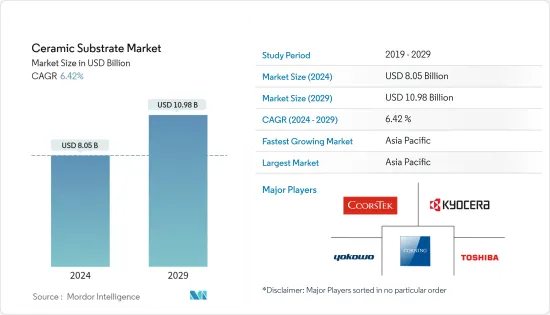

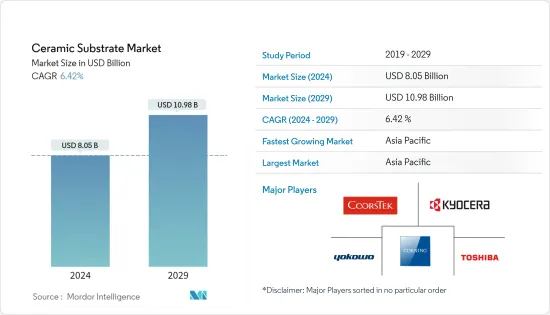

세라믹 기판 시장 규모는 2024년에 80억 5,000만 달러로 추정되고, 2029년까지 109억 8,000만 달러에 이를 것으로 예측되고 있으며, 예측 기간(2024-2029년) 동안 6.42%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다.

세라믹 기판 시장은 2020년에 신형 코로나 바이러스 감염(COVID-19)에 의해 악영향을 받았습니다. 그러나 신형 코로나바이러스 감염의 팬데믹 이후 업계는 급속히 회복되고 있고 향후 수년간 상승할 것으로 추정되고 있으며, 이는 세라믹 기판 시장 수요를 자극할 것으로 예상됩니다.

주요 하이라이트

- 조사 대상 시장을 견인하는 주요 요인은 금속보다 세라믹 기판 수요가 높아지고 있으며, 전자 용도에서 세라믹 기판의 채용이 증가하고 있다는 것입니다.

- 세라믹 기판의 사용에 따른 비용이 높고, 손상되기 쉽고, 조립이나 테스트 중에 신중한 취급이 필요하기 때문에 예측 기간 중에 세라믹 기판 시장 성장 억제요인이 될 것으로 예상됩니다.

- 의료 산업 및 자동차 산업의 새로운 용도에서의 수요가 증가하는 것은 예측 기간 동안 세라믹 기판 시장에 대한 기회입니다.

- 아시아태평양은 가장 큰 시장을 나타내며, 중국, 인도, 일본 등 국가에서의 소비 증가로 예측 기간 동안 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다.

세라믹 기판 시장 동향

반도체 산업 수요 증가

- 세라믹 기판은 제조에서 필수적인 역할을 통해 반도체 산업의 발전을 가능하게 하는 중요한 역할을 합니다.

- 반도체 제조업체는 알루미나, 산화 베릴륨, 질화 알루미늄 등의 세라믹 기판을 사용합니다. 이들 재료는 단단하고 내마모성이 있으며, 고온에서 강산과 알칼리에 대한 내성, 양호한 열전도율, 매우 높은 체적 저항률, 매우 낮은 유전율 및 손실 탄젠트 등의 특성으로 반도체 산업에서 사용됩니다.

- 세계의 반도체 산업은 자율주행과 인공지능 등 기술 수요에 따라 최근 순조롭게 성장하고 있습니다.

- 반도체 산업협회(SIA)에 따르면 2022년 세계 반도체 매출은 5,740억 달러에 이르렀으며, 2021년 5,559억 달러에 비해 3.3% 증가했습니다.

- 세계의 반도체 무역 통계(WSTS)에 따르면 2022년에는 모든 지리적 지역에서 반도체 무역이 두 자리 성장을 보였습니다. 아메리카 지역은 17.0%, 유럽은 12.6%, 일본은 10.0% 증가했습니다. 그러나 같은 해 아시아태평양의 성장률은 2.0% 감소했습니다.

- 따라서, 성장하는 반도체 산업은 앞으로 수년간 세라믹 기판 수요가 증가할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 아시아태평양은 최대 시장을 차지할 것으로 예상되며, 예측 기간 동안 세라믹 기판의 가장 빠르게 성장하는 지역이기도 합니다.

- 중국은 향후 수년간 전자 및 반도체 제품의 가장 큰 시장이 될 것으로 예상됩니다. 산업과학기술 국제전략센터(ISTI)에 따르면 인공지능 용도를 위한 집적회로(IC) 디바이스 수요가 증가함에 따라 대만 반도체 산업의 생산액이 대폭 증가할 것으로 예상됩니다.

- 중국 정부는 집적회로 생산 자급률을 2025년까지 70%로 끌어올리는 '중국 제조 2025' 정책을 도입했습니다.

- 반도체산업협회(SIA)에 따르면 2022년 중국 매출은 1,804억 달러로 반도체 시장을 독점하였고 2021년에 비해 6.2% 감소했습니다.

- 인도 전자반도체협회에 따르면 이 나라의 반도체 부품 시장은 2025년까지 323억 5,000만 달러에 달할 것으로 예상되고 있으며 CAGR은 10.1%로 전망됩니다. 게다가 정부가 현재 진행하고 있는 'Make in India' 구상은 이 나라의 반도체 산업에 대한 투자가 기대됩니다.

- 또한 인도 전자반도체협회(IESA)는 싱가포르 반도체산업협회(SSIA)와 각서를 체결하여 양국의 일렉트로닉스 및 반도체 산업 간의 무역 및 기술협력을 확립 및 발전시켰습니다. 이에 따라 인도의 반도체 제조에 있어서 세라믹 기판의 소비 범위가 더욱 확대되는 다양한 획기적인 반도체 제조 기술의 개발이 초래될 것으로 기대되고 있습니다.

- 현재 일본에는 약 30개의 반도체 제조 산업이 있으며, 다양한 유형의 반도체 칩 제조에 종사하고 있습니다. 일본 반도체 공급망은 세계 반도체 제조 장비의 3분의 1과 업계 재료의 절반 이상을 제공합니다.

- 게다가 필리핀이나 한국 등의 국가도 최근 조사 대상이 되고 있는 시장의 성장에 공헌하고 있습니다.

- 위의 요인은 예측 기간 동안 아시아태평양의 세라믹 기판 시장에 대한 수요를 더욱 촉진할 것으로 예상됩니다.

세라믹 기판 산업 개요

세계의 세라믹 기판 시장은 시장에서 중요한 경쟁사의 존재로 부분적으로 통합됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 금속보다 세라믹 기판 수요 증가

- 일렉트로닉스 용도에 있어서 세라믹 기판의 채용 증가

- 기타 촉진요인

- 억제요인

- 세라믹 기판의 사용에 따른 고비용

- 손상을 받기 쉽고, 조립이나 테스트시에 신중한 취급 필요

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 원재료 분석

제5장 시장 세분화(금액 기반 시장 규모)

- 유형별

- 알루미나

- 질화알루미늄

- 질화규소

- 산화베릴륨

- 기타

- 최종 사용자 산업별

- 소비자 일렉트로닉스

- 항공우주 및 방위

- 자동차

- 반도체

- 통신

- 기타

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 시장 점유율(%) 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- CeramTec GmbH

- CoorsTek Inc.

- Corning Incorporated

- ICP TECHNOLOGY Co.,LTD

- KOA Speer Electronics INC.

- KYOCERA Corporation

- LEATEC Fine Ceramics Co,.Ltd.

- MARUWA Co., Ltd.

- NEOTech

- NIPPON CARBIDE INDUSTRIES CO., INC.

- Niterra Co., Ltd.

- Ortech Advanced Ceramics

- TOSHIBA MATERIALS Co. LTD.,

- TTM Technologies Inc.

- Yokowo co., ltd.

제7장 시장 기회 및 앞으로의 동향

AJY 24.03.05The Ceramic Substrate Market size is estimated at USD 8.05 billion in 2024, and is expected to reach USD 10.98 billion by 2029, growing at a CAGR of 6.42% during the forecast period (2024-2029).

The ceramic substrate market was negatively impacted by COVID-19 in 2020. However, post-COVID-19 pandemic, the industries are recovering fast and are estimated to rise in the coming years, which will stimulate the demand for the ceramic substrate market.

Key Highlights

- The major factor driving the market studied are the increasing demand for ceramic substrates over metal and the rise in the adoption of ceramic substrates in electronics applications.

- The high cost associated with the use of ceramic substrate and prone to damage and need careful handling during assembly and testing is expected to act as a restraint for the ceramic substrate market during the forecast period.

- Increasing demand from the medical industry and emerging applications in the automotive industry is an opportunity for ceramic substrate market during the forecast period.

- Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period owing to the increasing consumption from countries such as China, India, and Japan.

Ceramic Substrate Market Trends

Increasing Demand from the Semiconductor Industry

- Ceramic substrate plays an important role in enabling developments in the semiconductor industry through their essential role in manufacturing.

- Semiconductor manufacturers use ceramic substrates such as alumina, beryllium oxide, and aluminum nitride. These materials are used in the semiconductor industry owing to their properties such as hard and resistant to wear, resistant to strong acid and alkali at high temperatures, good thermal conductivity, extremely high bulk resistivity, very low dielectric constant and loss tangent among others.

- The global semiconductor industry is growing at a healthy rate in recent times, owing to the demand for technologies such as autonomous driving, artificial intelligence, etc.

- According to the Semiconductor Industry Association (SIA), in 2022, the worldwide sales of semiconductors reached to USD 574 billion which was increase by 3.3% compared to 2021 at USD 555.9 billion.

- According to World Semiconductor Trade Statistics (WSTS), In 2022, all geographical regions exhibited double-digit growth in trade of semiconductors. The Americas region has increased by 17.0%, Europe by 12.6%, and Japan by 10.0%. However, The growth of Asia-Pacific has declined by 2.0% in the same year.

- Therefore, the growing semiconductor industry is expected to boost the demand for ceramic substrates incoming years.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to account for the largest market and is also forecasted to be the fastest-growing region for ceramic substrates during the forecast period.

- China is expected to become the largest market for electronics and semiconductor products over the coming years. According to the Industry, Science and Technology International Strategy Center (ISTI), the production value of Taiwan's semiconductor industry is anticipated to grow substantially, owing to the increasing demand for integrated circuit (IC) devices for artificial intelligence applications.

- The Chinese government has introduced the 'Made in China 2025' policy to increase the nation's self-sufficiency in integrated circuits production to 70% by 2025.

- According to Semiconductor Industry Association (SIA), in 2022, China dominated the semiconductor market with sales of USD 180.4 billion which declined as compared to 2021 by 6.2%.

- According to India Electronics and Semiconductor Association, the semiconductor component market in the country is expected to be worth USD 32.35 billion by 2025, displaying a CAGR of 10.1%. In addition, the ongoing Make in India initiative by the government is expected to result in investments in the semiconductor industry in the country.

- Additionally, India Electronics and Semiconductor Association (IESA) signed a MoU with Singapore Semiconductor Industry Association (SSIA) to establish and develop trade and technical cooperation between the electronics and semiconductor industries of both the countries. This is expected to result in development of various break-through semiconductor manufacturing technologies that would further increase the scope for the consumption of ceramic substrate in semiconductor manufacturing in India.

- Japan currently has about 30 semiconductor fabrication industries, which are involved in manufacturing of various types of semiconductor chips. Japan's semiconductor supply chain provides one third of the world's semiconductor manufacturing equipment and more than half of the industry's materials.

- Furthermore, countries such as Philippines and South Korea have also been contributing to the growth of the market studied lately.

- The above mentioned factors are expected to further drive the demand for ceramic substrate market in Asia-Pacific over the forecast period.

Ceramic Substrate Industry Overview

The Global Ceramic Substrate market is partially consolidated with the presence of significant competitors in the market. The major companies in the market are Corning Incorporated, CoorsTek Inc. TOSHIBA MATERIALS Co. LTD., KYOCERA Corporation, and Yokowo co., ltd. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Ceramic Substrates Over Metal

- 4.1.2 Rise in the Adoption of Ceramic Substrates in Electronics Application

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost Associated with the Use of Ceramic Substrate

- 4.2.2 Prone to Damage and Need Careful Handling During Assembly and Testing

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Raw Material Analysis

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Alumina

- 5.1.2 Aluminum Nitride

- 5.1.3 Silicon Nitride

- 5.1.4 Beryllium Oxide

- 5.1.5 Others

- 5.2 End-user Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Aerospace & Defense

- 5.2.3 Automotive

- 5.2.4 Semiconductor

- 5.2.5 Telecommunication

- 5.2.6 Others

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 CeramTec GmbH

- 6.4.2 CoorsTek Inc.

- 6.4.3 Corning Incorporated

- 6.4.4 ICP TECHNOLOGY Co.,LTD

- 6.4.5 KOA Speer Electronics INC.

- 6.4.6 KYOCERA Corporation

- 6.4.7 LEATEC Fine Ceramics Co,.Ltd.

- 6.4.8 MARUWA Co., Ltd.

- 6.4.9 NEOTech

- 6.4.10 NIPPON CARBIDE INDUSTRIES CO.,INC.

- 6.4.11 Niterra Co., Ltd.

- 6.4.12 Ortech Advanced Ceramics

- 6.4.13 TOSHIBA MATERIALS Co. LTD.,

- 6.4.14 TTM Technologies Inc.

- 6.4.15 Yokowo co., ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand From Medical Industry

- 7.2 Emerging Applications in Automotive Industry