|

시장보고서

상품코드

1435894

항공화물 운송 : 시장 점유율 분석, 업계 동향 통계, 성장 예측(2024-2029년)Air Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

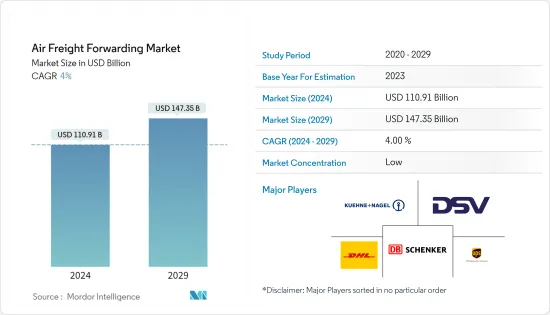

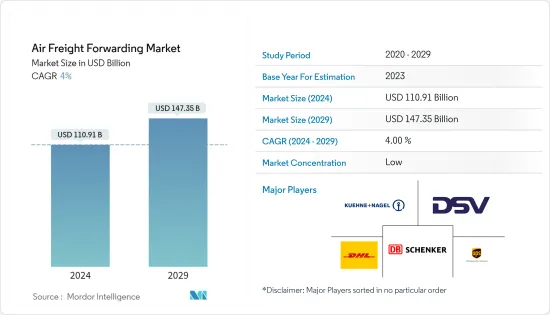

항공화물 운송 시장 규모는 2024년 1,109억 1,000만 달러로 추정되고, 2029년까지 1,473억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 4%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

육상 및 선박에 의한 화물 운송은 여전히 탁월한 선택이지만, 항공에 의한 물품 운송은 가장 빠르고 방해받지 않는 수단으로 간주됩니다. 화물 통킬로(CTK)로 측정한 세계의 항공화물 수요는 10월 211억으로 전월 대비 3.5% 증가했습니다. 하지만 업계 CTK는 2022년 같은 달에 비해 전년 대비 13.6% 감소했으며 2019년 팬데믹 전 수준보다 6.2% 낮았습니다. 2022년 10월의 계절조정 완료(SA) 항공화물 수요는 소폭 완화되었으며, 9월 대비 2.3%의 감소를 기록했습니다. CTK와 마찬가지로 SA CTK는 전년 대비 13.1% 감소하여 2019년 10월에 비해 6.1% 감소했습니다.

항공화물 업계는 선진국의 고인플레이션율, 세계 상품과 서비스 흐름의 침체, 우크라이나에서 계속되는 전쟁, 비정상적인 미국 고등 등으로 2022년 10월도 상황은 계속됐습니다. 이 모든 요인은 항공화물의 성장에 압박을 가하고 있습니다. 신규 수출 수주는 역사적으로 항공화물 운송의 선행 지표였지만 여전히 호조는 아닙니다. 세계의 PMI는 여전히 중요한 50개 라인을 밑돌고 있으며, 세계 평균에서 계속 줄어들고 있음을 시사합니다. 중국과 한국은 2022년 10월에 2022년 9월보다 약간 증가한 신규 수출 수주를 기록했지만 여전히 50을 밑돌았습니다. 다른 주요 국가들은 하락세를 유지했습니다. 특히 독일은 3월 이래 50개 미만의 수준에서 평평해지고 있으며 동유럽 전쟁의 경제에 미치는 영향이 계속되고 있음을 보여주고 있습니다.

유효 화물 톤키로(ACTK)로 측정한 업계 전체 항공화물 운송 능력은 9월에 비해 2% 증가했습니다. 10월 산업화물 적재율(CLF)은 마이너스 7.4%로 9월 마이너스 7.0%에서 하락했습니다. 업계 SA ACTK는 2021년 10월에 비해 거의 동일한 수준을 유지했습니다. 라틴아메리카는 SA ACTK의 전년 대비 가장 높은 20.3% 성장을 달성했습니다. 이에 북미가 전년 대비 3%, 중동이 같은 기준으로 1.1%로 이어집니다. 이에 대해 올 10월 SA ACTK가 전년 대비 마이너스 성장이 된 지역은 아프리카(-7.5%), 유럽(-5%), 아시아태평양(-2.1%)이었습니다.

항공화물 운송 시장 동향

전자상거래 증가가 시장을 견인

전자상거래는 향후 5년간 세계적으로 14% 성장할 것으로 예측됩니다. 미국 중관세 전쟁의 영향으로 지난 10년간 최악의 해를 맞이한 항공화물 업계에 있어서 이것은 절호의 기회가 됩니다. 항공화물 사업 전체의 16%를 차지하는 세계 전자상거래 산업은 2022년 3조 5,000억 달러의 상품 규모에서 2025년까지 7조 달러로 증가할 것으로 예측됩니다.

일부 세계의 통신 사업자는 아마존, 알리바바, 교토 상사 등 온라인 쇼핑 대기업이 독점하는 택배 시장에서 더 큰 점유율을 획득하려고 노력하고 있습니다. 두바이에 본사를 둔 에미레이트 항공은 에미레이트 델리버스를 시작했고, 루프트한자 독일 항공은 헤이데이, 브리티시 에어웨이즈의 모회사인 IAG에는 젠다가 포함되어 있습니다. 그러나 IATA는 이러한 감소에도 불구하고 11월 실적은 8개월 만에 최고였고, 전년 대비 축소율은 2019년 3월 이후 가장 낮은 것으로 나타났습니다.

항공화물 산업은 전자상거래 성장을 최대한 활용할 수 있는 유리한 위치에 있습니다. 항공화물은 전자상거래를 처리하기 위해 제작되었으며, 기업 간 소비자의 국경을 넘어서는 전자상거래의 약 80%가 항공에 의해 운송됩니다. 전자기기의 경우, 고액의 것에 비해 체적이나 톤수가 비교적 적기 때문에 항공화물이 선호되는 발송 방법입니다.

그러므로 온라인 쇼핑이 세계의 소포 배송 서비스에 대한 수요를 높이기 때문에 전자상거래는 항공화물 산업을 활성화할 것으로 예상됩니다. 항공화물은 고객의 요구에 부응하고 신속하고 효율적이며 신뢰할 수 있는 상품을 제공합니다. 급성장하는 국경을 넘어서는 전자상거래 시장과 크고 작은 전자소매업체에 의한 국내 배송량 증가가 세계 항공화물 시장의 성장을 견인하고 있습니다.

아시아태평양의 항공화물에 가장 큰 기여자

많은 아시아태평양 국가에서 부과된 여행 제한으로 인해 COVID-19 감염의 팬데믹에 따라 항공 부문이 침체되었음에도 불구하고 항공화물 수요는 상대적으로 견조해졌습니다. 그러나 공급망의 혼란, 불확실성 증가 및 실업률 상승으로 인한 기업과 소비자 신뢰감의 감소는 항공화물 사업에 악영향을 미쳤습니다.

아시아태평양 항공 협회(AAPA)는 항공화물 부서가 필수 의료기기 및 물자 운송에 적극적으로 참여하고 있다고 말합니다. 많은 아시아태평양 국가들은 여러 항공사들이 여객기를 항공화물 운송을 위해 일시적으로 개조하도록 격려했습니다. 표준 여객용 ATR72-600은 1.7톤의 화물 밖에 운반할 수 없지만, 화물기를 개조한 모델은 최대 8톤까지 운반할 수 있어 지역 수요와 운항 조건을 고려하면 태평양 섬국가에 적합합니다.

한국은 2022년 아시아태평양 항공화물 시장 점유율에서 4위 시장 점유율을 차지했습니다. 한국에는 세계에서 가장 중요한 항공화물 운송업체 산업 중 하나가 포함되어 있습니다. 여객 운송의 붕괴로 인해 이용 가능한 운송 공간이 감소했을 때 왕성한 수요의 혜택을 받았습니다. 항공사는 성명에서 화물기의 운항률을 높여 아이돌 상태의 여객기를 운송에 활용한다는 항공사의 전략이 화물의 매출을 지원했다고 발표했습니다. 한국의 2대 항공사인 대한항공과 아시아나항공은 화물운송 수요의 급증을 이용해 여객수 감소를 보완해 2021년 영업수익을 크게 늘렸습니다.

COVID-19 감염증의 진단 키트와 자동차 부품의 요구가 높아짐에 따라 해상화물 수요가 항공운송으로 옮겨 항공화물의 매출이 늘어났습니다. 그러므로 이것은 한국 항공화물 시장의 상당한 성장으로 이어집니다. 게다가 2022년 6월에는 대한항공이 계속해서 높은 화물 수요를 향한 태세를 갖추었기 때문에 에어버스와 보잉이 지난 몇 달간 발표한 신형 와이드바디 화물기로의 이행을 검토하고 있습니다. 또한 장기적인 강한 화물 수요로 인해 에어버스는 작년 2021년에 A350 화물기를, 보잉은 2022년 1월에 777X 화물기를 취항시켰습니다. 따라서 화물 서비스 항공기 수 증가는 예측 기간 동안 아시아태평양 항공화물 시장을 밀어 올릴 것입니다.

항공화물 운송 산업 개요

항공화물 운송 시장은 유명한 국제 기업의 존재로 인해 적당히 집중되어 있습니다. 대부분의 서비스 제공업체는 포장, 라벨 붙여넣기, 문서화, 전세 서비스, 화물 운송 등의 번들 솔루션을 제공합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 성과

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

- 분석조사방법

- 조사 단계

제3장 주요 요약

제4장 시장 인사이트

- 현재의 시장 시나리오

- 밸류체인 및 공급망 분석

- 기술 동향

- 투자 시나리오

- 정부의 규제 및 대처

- 스포트라이트-항공화물 운송 비용 및 운임

- 전자상거래 산업에 대한 인사이트

- COVID-19의 항공화물 운송 시장에 미치는 영향

제5장 시장 역학

- 성장 촉진요인

- 항공화물 운송 능력 수요 증가

- 전자상거래의 상승

- 억제요인

- 화물 제한

- 기회

- AI와 자동화의 통합

- 업계의 매력-Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제6장 시장 세분화

- 서비스별

- 항공사

- 우편

- 기타 서비스

- 목적지별

- 국내

- 국제

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 네덜란드

- 영국

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 호주

- 인도

- 싱가포르

- 말레이시아

- 인도네시아

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 남아프리카

- 이집트

- GCC 국가

- 기타 중동 및 아프리카

- 남미

- 브라질

- 칠레

- 기타 남미

- 북미

제7장 경쟁 구도

- 시장 집중도 개요

- 기업 프로파일

- DHL Supply Chain &Global Forwarding

- Kuehne Nagel

- DB Schenker Logistics

- DSV Panalpina

- UPS Supply Chain Solutions

- Expeditors International

- Nippon Express

- Bollore Logistics

- Hellmann Worldwide Logistics

- Kintetsu World Express*

제8장 시장 기회 및 장래의 동향

제9장 부록

AJY 24.03.08The Air Freight Forwarding Market size is estimated at USD 110.91 billion in 2024, and is expected to reach USD 147.35 billion by 2029, growing at a CAGR of 4% during the forecast period (2024-2029).

Although land and ship cargo transportation remain outstanding options, goods transport by air is considered the quickest and unhindered mode. Global air cargo demand, measured by cargo tonne-kilometers (CTKs), was 21.1 billion in October, increasing by 3.5% month-on-month (MoM). However, industry CTKs fell by 13.6% YoY compared to the same month in 2022 and were also 6.2% lower than the pre-pandemic levels in 2019. Seasonally adjusted (SA) air cargo demand softened slightly in October 2022, with a 2.3% MoM decline compared with September. Similar to the CTKs, SA CTKs contracted by 13.1% YoY and were 6.1% lower than in October 2019.

The air cargo industry persisted in October 2022, including high inflation rates in advanced economies, weak performance in the global flows of goods and services, the ongoing war in Ukraine, and the unusual strength of the US dollar. All of these factors put downward pressure on air cargo growth. The new export orders, historically a leading indicator for air cargo shipments, were still not buoyant. The global PMI remains below the critical 50 lines, suggesting continued contraction on average globally. China and Korea registered slightly higher new export orders in October 2022 than in September 2022, although they remained below 50. Other significant economies maintained a downward trend. Notably, Germany moved sideways at levels below 50 since March, signaling the continuous impact on the economy of the war in Eastern Europe.

Industry-wide air cargo capacity, measured by available cargo tonne-kilometers (ACTKs), increased by 2% compared with September. It produced an industry cargo load factor (CLF) of -7.4% in October, down from -7.0% in September. Industry SA ACTKs remained at about the same level compared with October 2021. Latin America achieved the highest YoY growth in SA ACTKs, at 20.3%. North America follows this with 3% YoY and the Middle East with 1.1% on the same basis. In comparison, regions that saw negative YoY growth in SA ACTKs this October were Africa (-7.5%), Europe (-5%), and Asia Pacific (-2.1%).

Air Freight Forwarding Market Trends

The increase in E-Commerce is driving the Market

E-commerce is forecast to grow 14% globally over the next five years. It creates an excellent opportunity for the air cargo industry, which witnessed its worst year in a decade due to the US-China tariff war. The global e-commerce industry, which makes up 16% of the total air cargo business, is projected to increase from USD 3.5 trillion in goods in 2022 to USD 7 trillion by 2025.

Some global carriers are working to gain a more significant share of the door-to-door delivery market that online shopping giants such as Amazon, Alibaba, and JD.com dominate. Dubai-based Emirates launched Emirates Delivers, Lufthansa includes Heyday, and British Airways parent IAG includes Zenda. However, IATA pointed out that despite this decline, November's performance was the best in eight months, with the slowest year-on-year rate of contraction recorded since March 2019.

The air cargo industry is well-positioned to capitalize on the growth in e-commerce. Air cargo is built to handle e-commerce, and approximately 80% of business-to-consumer cross-border e-commerce is transported by air. Air cargo is the preferred way of shipment for electronics due to the relatively small volume or tonnage compared to high value.

Thus, e-commerce is expected to fuel the air cargo industry, as online shopping boosts the demand for parcel delivery services across the globe. Air cargo can serve customers' needs and deliver goods with speed, efficiency, and reliability. The fast-growing cross-border e-commerce market and the rising domestic volumes sent by large and small e-retailers are driving growth in the global air cargo market.

APAC Largest Contributor to Air Freight

Irrespective of a downfall in the airline sector during the COVID-19 pandemic due to travel restrictions imposed in many Asian-Pacific countries, air cargo demand held up relatively well. However, supply chain disruptions and weakening business and consumer confidence due to increased uncertainties and rising unemployment adversely affected the air cargo businesses.

The Association of Asia-Pacific Airlines (AAPA) states that the air cargo sector is active in transporting essential medical equipment and supplies. Many Asian-Pacific countries encouraged several airlines to modify their passenger aircraft for air freight transport temporarily. While a standard passenger ATR72-600 can only carry 1.7 metric tons of cargo, its freighter-modified model can carry up to 8 metric tons, making it suitable for Pacific Island countries, given the region's demand and operating conditions.

South Korea accounted for the fourth-largest market share in the Asia-Pacific air cargo market share in 2022. South Korea includes one of the world's most significant air cargo carrier industries. It benefitted from strong demand when the collapse of passenger traffic reduced available transport space. Cargo sales were underpinned by the airline's strategy to increase the cargo plane operation rate and utilize idle passenger planes for transport, the airline said in a statement. Korean Air and Asiana Airlines, South Korea's two largest airlines, increased their operational earnings significantly in 2021, harnessing surging demand for cargo transport to help offset low passenger traffic.

The need for COVID-19 diagnostic kits and auto parts increased, and the sea cargo demand transferred to air transport, driving air cargo sales. Therefore, this leads to significant air cargo market growth in South Korea. Further, in June 2022, as Korean Air continues to position itself for high cargo demand, it is considering a move for the new wide-body freighters released by Airbus and Boeing in recent months. Long-term strong cargo demand also prompted Airbus to launch its A350 freighter last year in 2021 and Boeing its 777X freighter in January 2022. Thus, increasing the number of aircraft in cargo service will boost the Asia-Pacific air cargo market during the forecast period.

Air Freight Forwarding Industry Overview

The Air Freight Forwarding Market is moderately concentrated with the presence of prominent international players. Most service providers offer bundled solutions, such as packaging, labeling, documentation, charter services, and freight transportation. Some of the existing major players in the market include - DHL Supply Chain & Global Forwarding, Kuehne + Nagel, DB Schenker Logistics, DSV Panalpina, UPS Supply Chain Solutions, Expeditors International, Nippon Express, Bollore Logistics, Hellmann Worldwide Logistics, and Kintetsu World Express.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Value Chain / Supply Chain Analysis

- 4.3 Technological Trends

- 4.4 Investment Scenarios

- 4.5 Government Regulations and Initiatives

- 4.6 Spotlight - Air Freight Transportation Costs/Freight Rates

- 4.7 Insights on the E-commerce Industry

- 4.8 Impact of Covid-19 on Air Freight Forwarding Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Increase in the demand for the Air Cargo Capacity

- 5.1.2 The Rise of E-commerce

- 5.2 Restraints

- 5.2.1 Cargo Restrictions

- 5.3 Opportunities

- 5.3.1 AI and Automation Integration

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Airlines

- 6.1.2 Mail

- 6.1.3 Other services

- 6.2 By Destination

- 6.2.1 Domestic

- 6.2.2 International

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Mexico

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 France

- 6.3.2.3 Netherlands

- 6.3.2.4 United Kingdom

- 6.3.2.5 Italy

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 Australia

- 6.3.3.4 India

- 6.3.3.5 Singapore

- 6.3.3.6 Malaysia

- 6.3.3.7 Indonesia

- 6.3.3.8 South Korea

- 6.3.3.9 Rest of Asia-Pacific

- 6.3.4 Middle East & Africa

- 6.3.4.1 South Africa

- 6.3.4.2 Egypt

- 6.3.4.3 GCC Countries

- 6.3.4.4 Rest of Middle East & Africa

- 6.3.5 South America

- 6.3.5.1 Brazil

- 6.3.5.2 Chile

- 6.3.5.3 Rest of South America

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 DHL Supply Chain & Global Forwarding

- 7.2.2 Kuehne + Nagel

- 7.2.3 DB Schenker Logistics

- 7.2.4 DSV Panalpina

- 7.2.5 UPS Supply Chain Solutions

- 7.2.6 Expeditors International

- 7.2.7 Nippon Express

- 7.2.8 Bollore Logistics

- 7.2.9 Hellmann Worldwide Logistics

- 7.2.10 Kintetsu World Express*