|

시장보고서

상품코드

1441631

민간 항공기 재료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2024-2029년)Commercial Aircraft Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

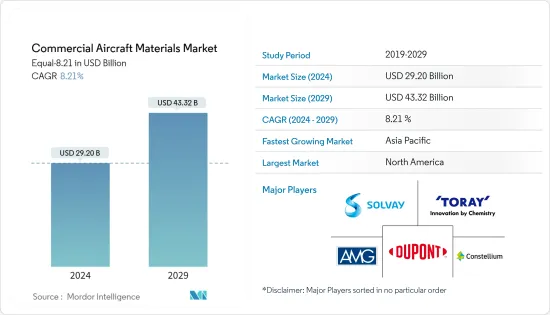

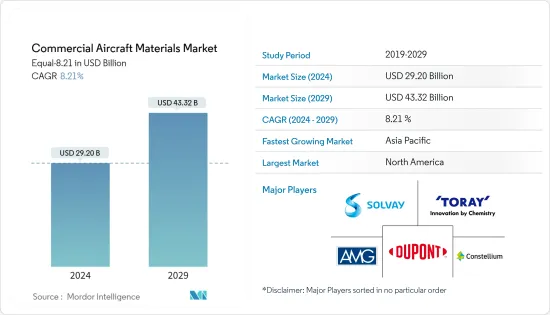

민간 항공기 재료 시장 규모는 2024년 292억 달러로 추정되고, 2029년까지 433억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 8.21%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

항공기에 사용되는 재료의 최적 특성은 고강도, 경량, 우수한 내열성입니다. 이 재료는 내구성이 있으며 상당한 수명을 가지고 있습니다. 지금까지 항공기의 구조는 주로 티타늄 합금과 알루미늄 합금에 의존했으며, 이러한 합금은 전체 구성 요소의 약 80%를 차지했습니다.

금속 합금보다 복합재료의 사용이 증가함에 따라 향후 시장이 크게 추진될 것으로 예상됩니다. 복합재료는 다른 재료에 비해 높은 강도 중량비, 고온 내성 및 내파괴성을 갖추고 있으며, 이 요인은 민간 항공기 제조에서 복합재료의 대규모 채용을 촉진하고 있습니다.

가볍고 연료 효율적인 항공기에 대한 수요 증가는 세계 항공기 재료 시장의 성장을 가속하는 중요한 요소입니다. 항공기 경량화는 운항과 관련된 비용을 크게 줄이고 연료 효율을 향상시켜 항공기 운항 회사의 수익성을 향상시킵니다.

민간 항공기 재료 시장 동향

좁은 바디 항공기 부문은 예측 기간 동안 최고의 성장을 이룹니다.

현재 협동기 부문은 여객기 카테고리에서 우세하며 세계 점유율의 80%를 차지하고 있습니다. 저가 항공사의 이용 증가로 예측 기간 동안에도 우위성이 지속될 것으로 예상됩니다. 이 요인은 단거리 노선에서의 낮은 운항 비용과 연료 효율 등의 이점을 갖춘 신세대 협동기에 대한 엄청난 수요가 발생했습니다.

항공사는 특히 단거리 노선의 항공사에 있어서 실현 가능하게 되었기 때문에 광동기에서 협동기로의 이행을 진행하고 있습니다. 협동기 수요가 급증함에 따라 OEM은 항공기 생산을 증가시키고 있습니다. 세라믹 및 금속 매트릭스 복합재, 섬유 강화 폴리머, 탄소 탄소 복합재 등의 복합재는 뛰어난 특성으로 인해 항공기 제조 회사에서 사용됩니다.

일부 항공사는 노선 범위와 시장 점유율을 강화하기 위한 전반적인 전략의 일환으로 장비를 확장하고 있습니다. 예를 들어, 2023년 6월에 IndiGo는 에어버스 A320 패밀리 항공기를 500대 주문했습니다. 연료 효율이 높은 A320NEO 패밀리 항공기는 인디고가 운항 비용 절감과 높은 수준의 신뢰성을 갖춘 연료 효율 실현에 중점을 둘 수 있습니다. 2023년부터 2028년에 걸쳐 약 10,000대의 협동기가 세계에 납입될 예정입니다.

북미는 예측 기간 동안에도 우위를 유지합니다.

북미의 민간 항공 산업은 수년간 세계 항공 시장에서 중요한 역할을 해왔습니다. 이 지역의 민간 항공 활동 수요는 비행기로 여행하는 승객 수가 매년 증가함에 따라 촉진되고 있습니다. 2022년 이 지역의 항공 여객 수는 60억 명에 달했습니다. 미국이 83%로 가장 큰 점유율을 차지하고 이어 캐나다, 멕시코, 북미의 다른 지역이 각각 8%, 6%, 2%를 차지하고 있습니다.

또한 복합재료 수요가 증가함에 따라 기업은 고급 복합재료 개발을 위한 새로운 시설을 개설하고 있습니다. 예를 들어, 2021년 7월, RTX의 일부인 플랫 앤 휘트니는 미국 칼스 배드에 세라믹 매트릭스 복합재료(CMC) 엔지니어링 및 개발 시설을 개설한다고 발표했습니다. 시설의 면적은 60,000 평방 피트를 초과합니다. 이는 항공우주 용도을 위한 세라믹 매트릭스 복합재(CMC) 개발, 통합 엔지니어링 및 저속도 생산에 사용됩니다.

항공기 현대화 프로그램의 일환으로 미국과 캐나다에서 운항하는 항공사의 엄청난 주문이 수요를 밀어 올리고 있습니다. 2023년 5월, 에어 캐나다는 보잉 B787 드림 라이너를 최대 20대 구입할 계획을 발표했습니다. 이 지역의 주요 항공사에 의한 이러한 신형 항공기의 주문은 향후 몇 년동안 항공기 재료 수요가 증가할 것으로 예상됩니다.

민간 항공기 재료 산업 개요

민간 항공기 재료 시장은 접착제, 화학제품, 복합재료, 금속 및 비금속 재료, 플라스틱 등을 제공하는 다양한 기업에 의해 세분화됩니다. 시장의 유명한 기업으로는 솔베이 SA, 도레이 주식회사, 콘스테륨, 듀폰 등이 있습니다.

시장에서는 재료 기술의 협업, 인수 및 혁신이 증가하고 있으며 시장 성장을 지원합니다. 예를 들어, 2021년 9월, Hexcel Corp는 보잉 B777X용 HexPEKK-100 재료로 만들어진 항공우주 구조물을 제조하는 다년 계약을 체결했습니다. 이 계약에 따라 HexPEKK 부품은 항공기의 기류 덕트 용도 및 기타 지원 요소를 위해 하트퍼드 주변의 Hexcel 라미네이팅 빌딩 시설에서 제조됩니다. 항공기 OEM과의 이러한 파트너십은 향후 몇 년동안 회사의 성장을 추진할 것으로 예상됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제 조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화

- 항공기 유형별

- 좁은 바디 항공기

- 와이드 바디 항공기

- 지역 제트

- 재료별

- 복합 재료

- 알루미늄 합금

- 강철

- 기타 재료

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Solvay SA

- Hexcel Corporation

- Toray Industries Inc.

- Constellium

- DuPont de Nemours Inc.

- Arconic Inc.

- ATI Inc.

- AMG Critical Materials NV

- Novelis Deutschland GmbH

- Notus Composites FZC

- VSMPO-AVISMA Corporation

제7장 시장 기회 및 미래 동향

AJY 24.03.15The Commercial Aircraft Materials Market size is estimated at USD 29.20 billion in 2024, and is expected to reach USD 43.32 billion by 2029, growing at a CAGR of 8.21% during the forecast period (2024-2029).

The optimal attributes for materials used in aircraft are high strength, low weight, and exceptional resistance to heat. These materials exhibit durability and possess a significant lifespan. In the past, aeronautical construction predominantly relied on titanium alloy and aluminum alloy, which comprised approximately 80% of all constituent elements.

Increasing the use of composite materials over metal alloys is expected to significantly drive the market in the future. Composites provide a high strength-to-weight ratio, high temperature, and fracture resistance over other materials, and this factor is fuelling the large-scale adoption of composites in commercial aircraft manufacturing.

The growing demand for aircraft that are both lightweight and fuel-efficient is a key factor driving the growth of the global aircraft materials market. Due to the reduced weight of the aircraft, the costs associated with operating the flights are significantly decreased, resulting in increased profitability for the aircraft operators because of improved fuel efficiency.

Commercial Aircraft Materials Market Trends

Narrow-body Aircraft Segment to Witness the Highest Growth During the Forecast Period

The narrowbody aircraft segment currently dominates the passenger aircraft category, with 80% of the global share. It is expected to continue its dominance during the forecast period due to the increase in the utilization of low-cost carriers. This factor resulted in huge demand for newer generation narrowbody aircraft, with advantages such as low cost of operation and fuel efficiency in short-haul routes.

Airline companies are shifting from widebody aircraft to narrowbody aircraft as they have become particularly doable for airlines for short-haul routes. The surge in demand for narrowbody aircraft is driving OEMs to increase their production of aircraft. Composites such as ceramic and metal matrix composites, fiber-reinforced polymers, carbon-carbon composites, etc., are used in aircraft manufacturing companies because of their favorable properties.

Several airlines are implementing fleet expansion as part of their overall strategies to enhance their route coverage and market share. For instance, in June 2023, IndiGo orders 500 Airbus A320 family aircraft. The fuel-efficient A320NEO family aircraft will allow IndiGo to maintain its strong focus on lowering operating costs and delivering fuel efficiency with high standards of reliability. During 2023-2028, around 10,000 narrowbody aircraft are expected to deliver across the globe.

North America to Continue its Dominance During the Forecast Period

The commercial aviation industry in North America has long been a significant player in the global aviation market. The demand for commercial aviation activity in the region is driven by the rising number of passengers traveling by air annually. In 2022, the region's air passenger traffic stood at 6 billion. The US accounted for the largest share which is 83%, followed by Canada, Mexico, and the Rest of North America accounted for 8%, 6%, and 2% respectively.

Furthermore, with the increasing demand for composites, companies are opening new facilities to develop advanced composites. For instance, in July 2021, Pratt & Whitney, a division of RTX, announced the inauguration of a ceramic matrix composites (CMCs) engineering & development facility in Carlsbad, the US. The facility has an area of over 60,000 square feet. It will be used for developing, integrating engineering, and low-rate production of Ceramic Matrix Composites (CMCs) for aerospace applications.

The huge order book of airlines operating in the US and Canada as a part of their fleet modernization programs is driving the demand. In May 2023, Air Canada announced that it is planning to purchase up to 20 Boeing B787 Dreamliners. Such orders for new aircraft by major airlines in the region are expected to boost the demand for aircraft materials in the coming years.

Commercial Aircraft Materials Industry Overview

The commercial aircraft materials market is fragmented due to various players providing adhesives, chemicals, composites, metals and non-metal materials, plastics, etc. Some of the prominent players in the market are Solvay SA, Toray Industries, Inc., Constellium, DuPont de Nemours, Inc., and AMG Critical Materials N.V., among others. Solvay is the major provider of composites to major aircraft programs like Airbus A220, Boeing B737, Boeing B777, Boeing B787 Dreamliner, COMAC C919, and Airbus A350. In addition to the aforementioned players, companies like General Plastics Manufacturing Company, Inc. and Alcoa Corporation provide plastic materials and metal. Alcoa Corporation provides metal and alloy products for Airbus A320, Airbus A330, Airbus A350, Boeing B737 MAX, Boeing B787 Dreamliner, and COMAC C919 aircraft programs.

The market is witnessing increased collaborations, acquisitions, and innovations in material technology, supporting the market growth. For instance, in September 2021, Hexcel Corp was awarded a multi-year contract to manufacture aerospace structures made with HexPEKK-100 material for the Boeing B777X. Under the agreement, the HexPEKK parts will be manufactured at Hexcel's additive manufacturing site near Hartford for airflow ducting applications and other supporting elements on the aircraft. Such partnerships with aircraft OEMs are expected to propel the company's growth in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Narrow-Body Aircraft

- 5.1.2 Wide-Body Aircraft

- 5.1.3 Regional Jets

- 5.2 Material

- 5.2.1 Composites

- 5.2.2 Aluminum Alloys

- 5.2.3 Steel

- 5.2.4 Other Materials

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Solvay SA

- 6.2.2 Hexcel Corporation

- 6.2.3 Toray Industries Inc.

- 6.2.4 Constellium

- 6.2.5 DuPont de Nemours Inc.

- 6.2.6 Arconic Inc.

- 6.2.7 ATI Inc.

- 6.2.8 AMG Critical Materials N.V.

- 6.2.9 Novelis Deutschland GmbH

- 6.2.10 Notus Composites FZC

- 6.2.11 VSMPO-AVISMA Corporation