|

시장보고서

상품코드

1687087

민간항공기 객실 좌석 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Commercial Aircraft Cabin Seating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

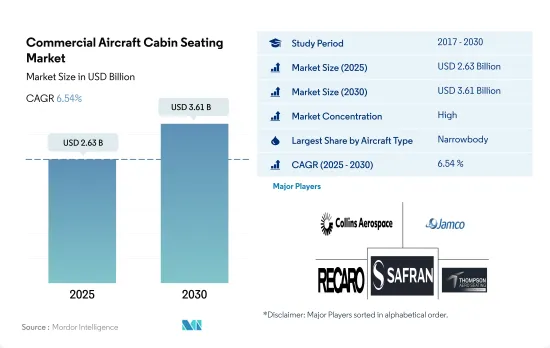

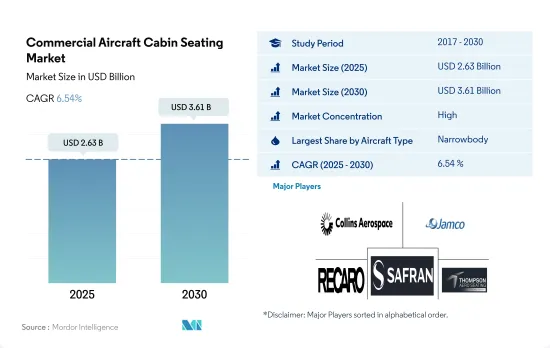

민간항공기 객실 좌석 시장 규모는 2025년에 26억 3,000만 달러, 2030년에는 36억 1,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 6.54%로 성장할 것으로 예상됩니다.

전 세계 항공기 확장 전략은 좁은 동체와 넓은 동체 항공기의 취득을 촉진하고 예측 기간 동안 상용 항공기의 좌석 확장을 촉진할 것으로 예상됩니다.

- 여행자의 선호도가 높아짐에 따라 이코노미 클래스보다 넓은 공간을 갖춘 좌석 구조가 매우 중요해지고 있습니다. 좁은 동체가 우위를 독점해, 2017-2022년의 전체의 납입수의 83%를 차지했습니다. 객실 클래스별로는 2022년에 납품된 항공기의 좌석 전체에서 이코노미 클래스와 프리미엄 이코노미 클래스의 좌석 비율은 좁은 동체가 93%, 넓은 동체가 86%였습니다.

- 좁은 동체와 넓은 동체를 포함한 전체 여객기 범주에서 2020년에 30%의 감소가 보였으며, 이는 세계 항공기 시트 수요에 영향을 미쳤습니다. 좁은 동체 부문에서 2022년 이코노미 및 프리미엄 이코노미 좌석의 세계 점유율은 94%였지만 넓은 동체에서는 86%였습니다. 대부분의 좌석이 이코노미 클래스에 속하는 이코노미 좌석 카테고리에는 지역항공의 급증이 도움이 되었습니다.

- 항공사는 장거리 노선에서 좁은 동체를 자주 사용하게 되어, 인체공학에 근거한 시트 시장 도입이 촉진되고 있습니다. 예를 들어, 아시아나항공과 대한항공은 인체공학을 기반으로 한 디자인, 개별적으로 조정가능한 카프레스트, 프라이버시 기능을 도입하여 비행 중 편안함과 전반적인 체험 수준을 높이기 위해 노력하고 있습니다.

- 세계 항공사와 OEM은 인체공학을 도입하여 경량화를 도모하고 좌석의 쾌적성을 향상시키는 노력을 강화하고 있습니다. 세계 항공사의 장거리 노선에서는 좁은 동체의 채용이 증가하고 있어 좁은 동체에 항공기용 시트의 배치를 뒷받침하고 있습니다. 2023-2030년간, 약 13,358기의 항공기가 납입될 전망입니다. 이 지역의 항공기 성장 계획은 좁은 동체와 넓은 동체의 조달을 촉진할 것으로 예상됩니다.

예측 기간 동안 아시아태평양이 가장 활기찬 시장이 될 것으로 예상되는 반면, 북미 시장은 여전히 세계 최대 시장이 될 것으로 예측됩니다.

- 항공사의 고객 경험은 항상 최우선 사항입니다. 승객은 여행에서 긍정적인 경험을 해야 합니다. 따라서 최고의 경험을 제공하기 위해 세계 항공사는 승객이 편안하게 보낼 수있는 객실 시트의 현대화에 힘을 쏟고 있습니다.

- 여객 수송량 증가는 결국 새로운 항공기의 조달과 주문을 촉진하고 항공기 좌석 시장을 끌어 올릴 수 있습니다. 2022년 10월 현재 에미레이트 항공, 카타르항공, 에티하드항공, 델타항공, 아메리칸항공, 루프트한자 독일항공, 터키항공, 에어프랑스항공, 싱가포르항공, 일본항공, 전일공, 중국국제항공 등 세계 각종 항공사가 보잉과 에어버스 총 534대를 발주하고 있습니다.

- 항공기의 무게를 줄이고 객실 공간의 효율성과 활용도를 높이기 위해 세계의 다양한 주요 항공사가 경량 시트를 채택하기 시작했습니다. 예를 들어, 아시아태평양, 대한항공, 아시아나항공은 인체공학을 기반으로 한 시트 디자인, 개별적으로 조정 가능한 카프레스트, 프라이버시 기능을 갖춘 시트를 채용함으로써 승객의 쾌적성 향상을 위해 노력하고 있습니다. 캐나다 항공사 포터 항공은 북미 항공기에 경량 시트를 도입했습니다. 유럽에서는 항공사의 시트 제조업체가 티타늄 및 탄소섬유 시트를 고급 클래스용으로 도입하기 시작했습니다. 승객의 쾌적성과 프라이버시를 향상시키는 이러한 기술 혁신이 향후 세계의 민간 항공기 객실 좌석 시장을 견인해 나갈 것으로 예상됩니다.

- 2023-2030년간, 약 13,358기의 항공기가 납입될 전망입니다. 북부는 세계 최대 시장이 될 것으로 예상되며, 아시아태평양은 예측 기간 동안 가장 수익성이 높은 시장이 될 것으로 예상됩니다.

세계 민간항공기 객실 좌석 시장 동향

아프리카 국가의 항공 수요 증가가 새로운 항공기 납품 수요를 촉진

- 항공 여객 수송량 증가는 항공사가 다양한 국내 노선과 국제 노선에서의 수요에 대응하기 위해 새로운 항공기를 조달하는 원동력으로서 중요한 역할을 하고 있습니다. 2021년 아프리카 항공 여객수는 1억 400만 명에 달했고, 2020년 대비 191%, 2019년 대비 3% 증가했습니다. 항공사는 증가하는 항공 수요에 대응하기 위해 기체 규모의 확대를 도모하고 있으며, 아프리카 국가 전체에서 신형기에 대한 큰 수요를 창출하고 있습니다. 남아프리카, 이집트, 알제리 등 주요 국가들은 이 지역의 총 여객 수송량의 40%를 차지하고 있으며, 아프리카의 다른 국가들에 비해 신조 항공기에 대한 높은 수요를 창출하고 있습니다.

- 2017년부터 2022년 사이에 아프리카 국가 전체에서 총 36대의 신규 항공기가 납품되었으며, 지난 기간 동안 이 지역에서 납품된 신규 제트기는 전 세계 여객기 납품 총수의 1% 미만이었습니다. 항공 여객 운송이 생성하는 수요는 결국 항공기 조달 증가로 이어질 수 있습니다. 아프리카의 주요 항공사로는 에티오피아 항공, 이집트 항공, 로열 에어 모로코, 에어 알제리, 케냐 항공 등이 있습니다. 2022년 9월 현재 다른 항공사 중 일부는 86대 이상의 항공기를 체류하고 있습니다. 86대 중 52대는 좁은 동체가 될 전망입니다. 연비가 좋은 장거리기의 채용이 증가하고 있으며 저렴한 항공사의 성공이 좁은 동체 부문을 견인하는 주요 요인입니다. 이러한 요인은 예측 기간 동안 아프리카의 객실 내장 시장을 끌어 올릴 수 있습니다.

COVID-19 팬데믹 이후 국제 여객 수송량 증가가 시장 수요를 견인하고 있습니다.

- COVID-19 팬데믹 이후 2022년 국경을 넘은 여행이 점차 회복됨에 따라 아시아태평양 항공사는 사람들의 여행 욕구와 2년간의 격리 기간에 축적된 저축의 현금화에 자극을 받아 폭주하는 수요에 대응하기 위해 증편을 서두르고 있습니다. 그 결과, 2022년에, 이 지역의 항공 여객 수송량은 다른 지역보다 빠르게 팬데믹으로부터 회복되었습니다. 예를 들어, 2022년 아시아태평양 전체의 항공 여객 수는 19억명을 기록했으며, 2021년 대비 6%, 2020년 대비 151% 증가했습니다. 이 지역의 항공사는 주요 국가에서 항공 여객 수송량 증가에 대응하기 위해 장비의 확장 계획을 실시했습니다. 중국, 인도, 일본, 인도네시아는 이 지역의 항공 여객 수송량 전체의 70%를 차지하고 있으며, 기타 아시아태평양 국가들과 비교하여 신조 항공기에 대한 높은 수요를 창출하고 있습니다.

- 아시아태평양 항공사는 또한 세계적으로 경제 상황이 엄격해지고 있음에도 불구하고 여행 수요가 계속 성장하고 있기 때문에 국제 항공 여객 시장의 순조로운 회복을 목격했습니다. 예를 들어, 2022년 8월 국제선 여객수는 1,310만명을 기록했으며, 140만명이었던 2021년 8월과 비교하면 836%의 성장세를 보였습니다. 연초 8개월 동안 국제선 여객 수의 건전한 성장은 비즈니스 및 레저 소비자로부터의 강한 여행 수요를 보여줍니다. 이 지역의 항공 여객 수송량의 급증은 향후 항공 수송 업계를 견인할 것으로 기대됩니다.

민간항공기 객실 좌석 산업 개요

민간항공기 객실 좌석 시장은 상당히 통합되어 상위 5개 기업에서 82.68%를 차지합니다. 이 시장 주요 기업은 다음과 같습니다. Collins Aerospace, Jamco Corporation, Recaro Group, Safran and Thompson Aero Seating(sorted alphabetically).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 항공 여객 수송량

- 아시아태평양

- 유럽

- 중동

- 북미

- 신규 항공기 납품 수

- 아프리카

- 아시아태평양

- 유럽

- 중동

- 북미

- 남미

- 1인당 GDP(현재 가격)

- 아시아태평양

- 유럽

- 중동

- 북미

- 항공기 제조업체의 수입

- 항공기 수주 잔량

- 수주 총액

- 공항 건설 지출(진행중)

- 항공사의 연료비

- 규제 프레임워크

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 항공기 유형

- 좁은 동체

- 넓은 동체

- 지역

- 아시아태평양

- 국가별

- 중국

- 인도

- 인도네시아

- 일본

- 싱가포르

- 한국

- 기타 아시아태평양

- 유럽

- 국가별

- 프랑스

- 독일

- 스페인

- 터키

- 영국

- 기타 유럽

- 중동

- 국가별

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 북미

- 국가별

- 캐나다

- 미국

- 북미의 기타

- 세계 기타 지역

- 아시아태평양

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Adient Aerospace

- Collins Aerospace

- Expliseat

- Jamco Corporation

- Recaro Group

- Safran

- STELIA Aerospace(Airbus Atlantic Merginac)

- Thompson Aero Seating

- ZIM Aircraft Seating GmbH

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Commercial Aircraft Cabin Seating Market size is estimated at 2.63 billion USD in 2025, and is expected to reach 3.61 billion USD by 2030, growing at a CAGR of 6.54% during the forecast period (2025-2030).

Fleet expansion strategies globally are anticipated to facilitate the acquisition of narrowbody and widebody aircraft and stimulate the expansion of commercial aircraft seating during the forecast period

- An enhanced seating structure with more developed space than economy-class seats is becoming highly essential due to rising preferences from travelers. The narrowbody aircraft dominated the number of deliveries, with 83% of the overall deliveries during 2017-2022. In terms of cabin class, economy and premium economy seats accounted for 93% of the overall seats of the aircraft delivered in 2022 for narrowbody aircraft and 86% for widebody aircraft.

- The overall passenger aircraft category, including narrowbody and widebody aircraft, witnessed a decline of 30% in 2020, which affected the demand for aircraft seats globally. In the narrowbody segment, the share of economy and premium economy seats globally was 94% in 2022, while their share was 86% in widebody aircraft. The surge in regional aviation has aided the economy seating category, where most seats belong to economy class.

- Airlines are using narrowbody aircraft more frequently on longer routes, facilitating the introduction of ergonomic seats in the market. For instance, Asiana Airlines and Korean Air are working to improve the level of comfort and overall experience during the flight by implementing ergonomic design, individually adjustable calf rests, and privacy features.

- Aviation operators and OEMs across the world are stepping up their efforts to reduce weight and improve the comfort features in seats by implementing ergonomics. The adoption of narrowbody aircraft in the longer haul routes airlines worldwide has increased, thus aiding the deployment of aircraft seats in narrowbody aircraft. Around 13,358 aircraft are expected to be delivered between 2023 and 2030. The fleet expansion plans in the region are expected to aid the procurement of both narrowbody and widebody aircraft.

The North market is projected to remain the largest in the world, while Asia-Pacific is anticipated to the most lucarative market during the forecast period.

- Customer experience is always the top priority for airlines. Passengers must have a positive experience with travel. Thus, to provide the best experience, airlines worldwide focus on modernized cabin seats that comfort passengers.

- The increased passenger traffic may eventually drive new aircraft procurements and orders, thus boosting the aircraft seating market. As of October 2022, a total of 534 Boeing and Airbus planes were ordered by various airlines globally, such as Emirates, Qatar Airways, Etihad Airways, Delta Airlines, American Airlines, Lufthansa, Turkish Airlines, Air France, Singapore Airlines, Japan Airlines, ANA, and Air China.

- Various major airlines worldwide started adopting lighter seats to reduce the aircraft's weight and improve cabin space efficiency and utilization. For instance, Asia-Pacific, Korean Air, and Asiana Airlines are working to improve passenger experience by adopting ergonomic seat designs, individually adjustable calf rests, and privacy-featured seats. The Canadian airline Porter Airlines integrated lightweight seats in its regional aircraft in North America. In Europe, airline seat manufacturers have started introducing titanium and carbon fiber seats for the higher-end classes. Such innovations to improve passenger comfort and privacy are expected to drive the global commercial aircraft cabin seating market in the future.

- Around 13,358 aircraft are expected to be delivered between 2023 and 2030. The North is expected to be the largest market globally, while the Asia-Pacific region is expected to be the most lucrative market in the forecast period.

Global Commercial Aircraft Cabin Seating Market Trends

Growing demand for air travel in African countries is driving the demand for new aircraft deliveries

- Rising air passenger traffic plays a vital role in driving airlines to procure new aircraft to meet the demand from various domestic and international routes. In 2021, air passenger traffic in Africa reached 104 million, a growth of 191% compared to 2020 and 3% compared to 2019. Airlines are looking to expand their fleet sizes to cater to the growing demand for air travel, which is generating significant demand for new aircraft across African nations. Major countries, such as South Africa, Egypt, and Algeria, accounted for 40% of the total air passenger traffic in the region, generating higher demand for new aircraft compared to other countries across Africa.

- A total of 36 new aircraft were delivered across African countries between the years of 2017 and 2022, and the new jet deliveries in the region during the historic period accounted for less than 1% of the total worldwide passenger aircraft deliveries. The demand generated by air passenger traffic may eventually lead to an increase in aircraft procurements. Some of the major airlines in Africa are Ethiopian Airlines, Egyptair, Royal Air Maroc, Air Algerie, and Kenya Airways. As of September 2022, some other airlines had a backlog of over 86 aircraft. Of the 86 jets, 52 are expected to be narrowbody aircraft. The increasing adoption of fuel-efficient, long-range aircraft and the growing success of low-cost carriers are the major factors driving the narrowbody segment. Such factors may boost the African cabin interior market in the forecast period.

An increase in international passenger traffic post the COVID-19 pandemic is driving market demand

- As cross-border travel was progressively restored in 2022 post the COVID-19 pandemic, the carriers in Asia-Pacific raced to increase their flights to meet runaway demand, stimulated by people's desire to travel and cash in on savings accumulated in the two years of isolation. As a result, in 2022, the air passenger traffic in the region recovered more rapidly from the pandemic than in the other regions. For instance, in 2022, air passenger traffic in the whole of Asia-Pacific was recorded at 1.9 billion, a growth of 6% compared to 2021 and 151% compared to 2020. Airline companies in the region are implementing fleet expansion plans to cater to the growing air passenger traffic in the major countries. China, India, Japan, and Indonesia accounted for 70% of the total air passenger traffic in the region, generating higher demand for new aircraft compared to other Asia-Pacific countries.

- Airlines in Asia-Pacific also witnessed a good recovery in international air passenger markets as travel demand continued to fuel growth despite increasingly challenging global economic conditions. For instance, in August 2022, the region recorded 13.1 million international air passenger traffic, an 836% increase compared to August 2021, when it was recorded at 1.4 million. The healthy growth in international passenger traffic in the first eight months of the year showed strong travel demand from business and leisure consumers. The rapid increase in air passenger traffic in the region is expected to drive the air transport industry in the future.

Commercial Aircraft Cabin Seating Industry Overview

The Commercial Aircraft Cabin Seating Market is fairly consolidated, with the top five companies occupying 82.68%. The major players in this market are Collins Aerospace, Jamco Corporation, Recaro Group, Safran and Thompson Aero Seating (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.1.1 Asia-Pacific

- 4.1.2 Europe

- 4.1.3 Middle East

- 4.1.4 North America

- 4.2 New Aircraft Deliveries

- 4.2.1 Africa

- 4.2.2 Asia-Pacific

- 4.2.3 Europe

- 4.2.4 Middle East

- 4.2.5 North America

- 4.2.6 South America

- 4.3 GDP Per Capita (current Price)

- 4.3.1 Asia-Pacific

- 4.3.2 Europe

- 4.3.3 Middle East

- 4.3.4 North America

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.2 Region

- 5.2.1 Asia-Pacific

- 5.2.1.1 By Country

- 5.2.1.1.1 China

- 5.2.1.1.2 India

- 5.2.1.1.3 Indonesia

- 5.2.1.1.4 Japan

- 5.2.1.1.5 Singapore

- 5.2.1.1.6 South Korea

- 5.2.1.1.7 Rest of Asia-Pacific

- 5.2.2 Europe

- 5.2.2.1 By Country

- 5.2.2.1.1 France

- 5.2.2.1.2 Germany

- 5.2.2.1.3 Spain

- 5.2.2.1.4 Turkey

- 5.2.2.1.5 United Kingdom

- 5.2.2.1.6 Rest of Europe

- 5.2.3 Middle East

- 5.2.3.1 By Country

- 5.2.3.1.1 Saudi Arabia

- 5.2.3.1.2 United Arab Emirates

- 5.2.3.1.3 Rest of Middle East

- 5.2.4 North America

- 5.2.4.1 By Country

- 5.2.4.1.1 Canada

- 5.2.4.1.2 United States

- 5.2.4.1.3 Rest of North America

- 5.2.5 Rest of World

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Adient Aerospace

- 6.4.2 Collins Aerospace

- 6.4.3 Expliseat

- 6.4.4 Jamco Corporation

- 6.4.5 Recaro Group

- 6.4.6 Safran

- 6.4.7 STELIA Aerospace (Airbus Atlantic Merginac)

- 6.4.8 Thompson Aero Seating

- 6.4.9 ZIM Aircraft Seating GmbH

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms