|

시장보고서

상품코드

1850065

3D 프린팅 재료 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)3D Printing Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

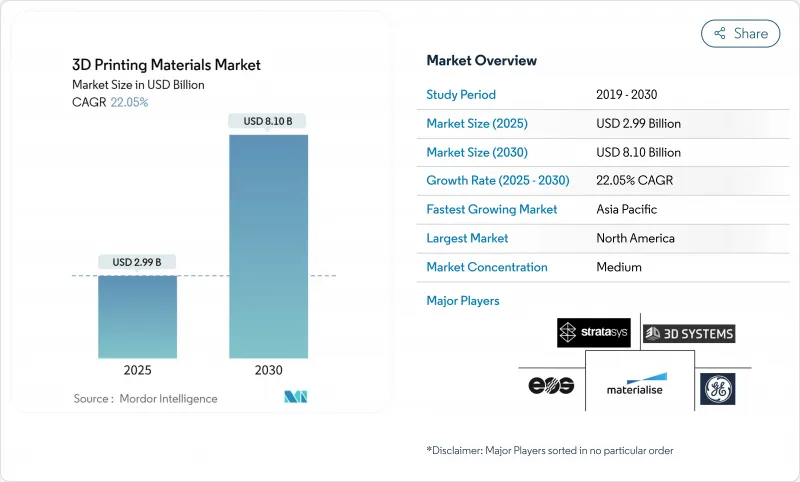

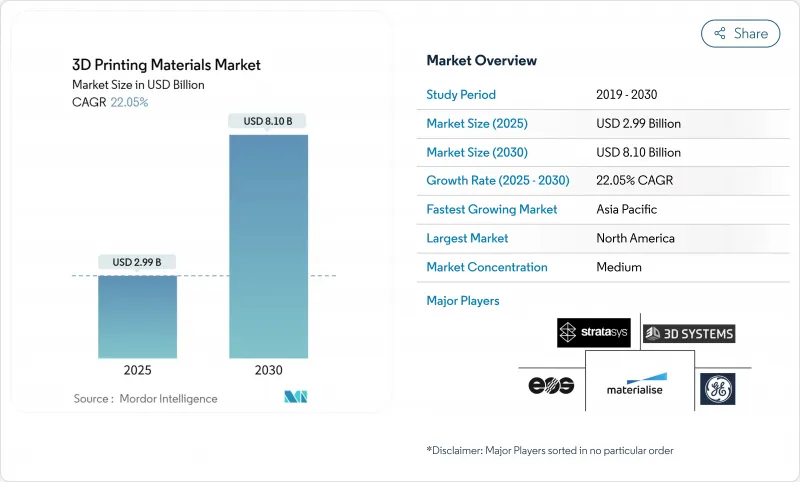

3D 프린팅 재료 시장은 2025년에 29억 9,000만 달러로 추정되고, 2030년에는 81억 달러로 확대될 전망이며, CAGR 22.05%로 성장할 것으로 예측됩니다.

이 확장은 항공우주, 자동차 및 헬스케어 공급망에서 적층 모델링이 프로토타이핑 리소스에서 검증된 생산 도구로 이동하고 있음을 반영합니다. 항공우주 산업의 주요 기업은 티타늄, 니켈 및 알루미늄 분말을 지속적으로 생산하기 위해 인증을 계속하고 의료기기 제조업체는 환자 고유의 고분자 및 금속 규제 클리어런스를 보장합니다. 자동차 OEM은 경량 전기자동차 부품과 금형 효율의 채택을 가속화합니다. 급속한 재료 혁신은 사이클 시간을 단축하고 부품 성능을 향상시키고 화학 기업 및 프린터 공급업체에 새로운 수익원을 엽니다. 경쟁 전략의 핵심은 하드웨어, 소프트웨어 및 소모품을 긴밀하게 통합하고 반복 재료 수입을 보장하는 것입니다.

세계의 3D 프린팅 재료 시장 동향 및 인사이트

연속 항공우주 및 의료 생산에서 금속 분말 사용 급증

항공우주 OEM은 실증 프로젝트에 그치지 않고 티타늄, 니켈, 알루미늄 합금을 비행 크리티컬한 부품으로 인증하고 있으며, Ti-6Al-4V는 높은 강도 대 중량비와 내식성으로 인해 항공우주용 분말 소비의 대부분을 차지하고 있습니다. 생체적합성이 있는 티타늄과 코발트 크롬 분말은 현재 감법법으로는 달성할 수 없는 내부 격자를 가진 두개판, 척추 케이지, 인공 관절을 지원합니다. Honeywell의 6K Additive Nickel 718 2025 인증은 재활용 원료가 원료 폐기물을 줄이면서 엄격한 터빈 엔진 요구 사항을 충족하는 방법을 보여줍니다. 2년이라는 장기간에 걸친 인정제도는 높은 진입 장벽을 만들어 내고, 기존의 분말 제조업체를 가격 파괴로부터 보호하며, 3D 프린팅 재료 시장 내 통합 동향을 강화합니다.

고성능 폴리머의 급속한 진보

폴리에테르 에테르 케톤(PEEK), 폴리에테르 케톤 케톤(PEKK), 탄소섬유 강화 블렌드는 인공위성용 브래킷, 정형외과용 외상 플레이트, 석유 및 가스 유량 제한 장치로 알루미늄을 대체하고 있습니다. 스트라타시스는 2025년에 VICTREX AM 200을 발표하여 1회의 조형으로 수백개의 부품을 조형할 수 있어 150℃의 사용 온도에서도 치수 정밀도를 유지할 수 있게 되었습니다. 듀얼 노즐 용융 성막 시스템은 면내 열전도율을 4.54W/(m*K)까지 높이는 연속 탄소 로빙을 내장하여 히트 싱크나 EMI 실드의 이용 사례를 확대했습니다. 이러한 진보로 생산 리드 타임은 36시간 이하로 단축되고, 후가공은 50% 절감되어 3D 프린팅 재료 시장 전체의 반복 폴리머 수요를 자극하고 있습니다.

높은 장비 및 재료 비용

산업용 금속 프린터의 가격은 10만-100만 달러로 특수 분말과 필라멘트가 부품 비용 전체의 30-40%를 차지하기 때문에, 중소 제조업체에의 보급은 한정적입니다. 불안정한 니켈과 희토류 가격은 서비스 뷰로의 예산 편성 위험을 높입니다. 선도적인 통합 업체는 다년간의 원료 계약을 체결하고 사내에서 재활용을 개척함으로써 대항하고 있지만, 자본 집약도가 3D 프린팅 재료 시장 전체로의 보급을 방해하는 요인이 되고 있습니다.

부문 분석

플라스틱의 2024년 점유율은 47.25%로 3D 프린팅 재료 시장을 선도했습니다. 이 부문에는 ABS 및 PLA와 같은 범용 등급 외에 멸균 및 고온에서의 사용을 견디는 엔지니어링 폴리머도 포함됩니다. 수요는 데스크톱 프린터의 출하 대수 및 업무용 용융 필라멘트의 설치 대수와 연동하여 확대됩니다. 플라스틱 부서는 색상의 충실도, 난연성 및 기계적 성능의 지속적인 개선으로 혜택을 누리고 데스크톱 사용자를 유치하며 산업용 사용자를 유효한 데이터 세트로 만족시킵니다.

베이스는 작지만 금속은 2030년까지의 CAGR이 23.24%로, 3D 프린팅 재료 시장에서 가장 빠릅니다. 인증된 티타늄, 알루미늄, 니켈의 초합금 분말은 무게가 중요한 항공 엔진 브래킷, 정형외과용 임플란트, 레이싱 카의 브레이크 캘리퍼를 허용합니다. 세라믹과 왁스는 인베스트먼트 주조 쉘과 고온 전자 제품과 같은 특수 틈새 시장을 차지합니다.

지역 분석

북미는 2024년 3D 프린팅 재료 시장의 39.46%를 차지해 선두를 유지했습니다. 이 시장을 지원하는 것은 견고한 항공우주 공급망, 외과 의사 주도 임플란트 혁신, 아메리카 메이크스 컨소시엄과 같은 연방 정부의 자금 제공 경로입니다. 재료 공급업체는 Tier-1 항공기 제조업체 및 의료기기 클러스터와의 근접성을 활용하여 용도 분야에 특화된 파우더 및 폴리머를 공동 개발하고 있습니다. 또한 이 지역에는 금속 절분을 회수하여 적격한 첨가제 원료로 변환하여 버진 수입에 대한 의존을 완화하는 분체 리사이클 업자도 있습니다.

아시아태평양의 CAGR은 26.25%로 가장 높으며 2030년까지 성장 엔진으로 지속될 것으로 예측됩니다. 중국은 엔트리 레벨 프린터 수출을 독점하고 있으며, 바이오 폴리머에 비용면에서 우위를 부여하고 있습니다. 유럽은 강력한 연구개발 능력과 세계에서 가장 엄격한 환경 규제의 균형을 유지하고 있습니다. EU의 서큘러 이코노미 지령은 재활용 원료의 채용을 장려하고 있으며, 바이오 유래의 PLA와 PA11의 수량 증가는 가속합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 항공우주 및 의료기기의 양산에서 금속 분말 사용량 급증

- 고성능 폴리머의 급속한 진보

- 자동차 용도에서 수요 급증

- 헬스케어 및 소비재에서 매스커스터마이제이션 기세

- 바이오베이스 및 생분해성 원료의 채용 증가

- 시장 성장 억제요인

- 설비비 및 재료비의 상승

- 항공우주 및 의료 등급의 엄격한 인증

- 한정된 유형의 재료의 이용가능성

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 소재 유형별

- 플라스틱

- 아크릴로니트릴부타디엔스티렌(ABS)

- 폴리유산(PLA)

- 나일론

- 폴리아미드

- 폴리카보네이트

- 기타 플라스틱(복합재료, 생분해성 폴리머 등)

- 금속

- 세라믹

- 기타 재료(가스, 왁스)

- 플라스틱

- 형태별

- 분말

- 필라멘트

- 액체 및 수지

- 최종 사용자 업계별

- 항공우주 및 방위

- 자동차

- 의학

- 가전

- 기타(에너지 및 전력, 산업 기계 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 싱가포르

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3D Systems, Inc.

- Arkema

- BASF

- CRP TECHNOLOGY Srl

- Custom Resin Solutions

- EnvisionTEC US LLC

- EOS GmbH

- Evonik Industries AG

- General Electric Company

- Henkel AG & Co. KGaA

- Hoganas AB

- HP Development Company, LP

- Materialise

- Renishaw plc

- Sandvik AB

- Solvay

- Stratasys

- voxeljet AG

제7장 시장 기회 및 향후 전망

AJY 25.11.05The 3D printing materials market reached USD 2.99 billion in 2025 and is forecast to rise to USD 8.10 billion by 2030, advancing at a 22.05% CAGR.

This expansion reflects the migration of additive manufacturing from a prototyping resource to a validated production tool across aerospace, automotive, and healthcare supply chains. Aerospace primes continue to qualify titanium, nickel, and aluminum powders for serial production, while medical device makers secure regulatory clearances for patient-specific polymers and metals. Automotive OEMs accelerate adoption of lightweight electric-vehicle components and tooling efficiencies. Rapid material innovation lowers cycle times, improves part performance, and opens new revenue streams for chemical companies and printer vendors. Competitive strategies now center on tight integrating hardware, software, and consumables to lock in repeat material revenue.

Global 3D Printing Materials Market Trends and Insights

Surge in Metal Powder Usage for Serial Aerospace and Medical Production

Aerospace OEMs have moved beyond demonstration projects to certify titanium, nickel, and aluminum alloys for flight-critical components, with Ti-6Al-4V representing the major portion of the aerospace powder consumption thanks to its high strength-to-weight ratio and corrosion resistance. Medical device firms mirror this shift; biocompatible titanium and cobalt-chrome powders now support cranial plates, spinal cages, and joint replacements with internal lattices unachievable through subtractive routes. Honeywell's 2025 qualification of 6K Additive Nickel 718 illustrates how recycled feedstock can meet stringent turbine-engine requirements while reducing raw-material waste. Lengthy two-year qualification regimes create high entry barriers and shield incumbent powder suppliers from price-based disruption, reinforcing consolidation trends inside the 3D printing materials market.

Rapid Advances in High-Performance Polymers

Polyetheretherketone (PEEK), polyetherketoneketone (PEKK), and carbon-fiber-reinforced blends are replacing aluminum in satellite brackets, orthopedic trauma plates, and oil-and-gas flow restrictors. Stratasys introduced VICTREX AM 200 in 2025, enabling hundreds of parts per build and maintaining dimensional accuracy at 150 °C service temperatures. Dual-nozzle fused deposition systems now embed continuous carbon rovings that lift in-plane thermal conductivity to 4.54 W/(m*K), expanding use cases in heat sinks and EMI shielding. These advances compress production lead times below 36 hours and reduce post-machining by 50%, stimulating recurring polymer demand across the 3D printing materials market.

High Equipment and Material Cost

Industrial metal printers list between USD 100,000 and USD 1 million, while specialty powders and filaments account for 30-40% of total part cost, limiting penetration in small and medium manufacturers. Volatile nickel and rare-earth pricing add budgeting risk for service bureaus. Large integrators counter by signing multi-year feedstock contracts and developing in-house recycling, but capital intensity remains a gating factor for broader adoption across the 3D printing materials market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Demand from Automotive Applications

- Increase in the Adoption of Bio-Based/Biodegradable Feedstocks

- Stringent Certification for Aerospace and Medical Grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics led the 3D printing materials market with a 47.25% share in 2024, reflecting their cost advantage and compatibility with both consumer and industrial printers. The segment covers commodity grades such as ABS and PLA as well as engineering polymers capable of withstanding sterilization or high-temperature service. Demand scales in tandem with desktop printer shipments and professional fused-filament installations. The plastics segment benefits from continued improvements in color fidelity, flame retardancy, and mechanical performance, which keep desktop users engaged and industrial users satisfied with validated data sets.

Although holding a smaller base, metals are on track for a 23.24% CAGR to 2030, the fastest in the 3D printing materials market. Certified titanium, aluminum, and nickel super-alloy powders enable weight-critical aero-engine brackets, orthopaedic implants, and racing-car brake calipers. Ceramics and waxes occupy specialized niches such as investment casting shells and high-temperature electronics.

The 3D Printing Materials Market Report Segments the Industry by Material Type (Plastics, Metals, Ceramics, and Other Materials), Form (Powder, Filament, and Liquid/Resin), End-User Industry (Aerospace and Defense, Automotive, Medical, Consumer Electronics, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained leadership with 39.46% of the 3D printing materials market in 2024, supported by a robust aerospace supply chain, surgeon-led implant innovation, and federal funding channels such as the America Makes consortium. Material vendors leverage proximity to Tier-1 airframers and medical device clusters to co-develop application-specific powders and polymers. The region also hosts several powder recyclers that capture metal swarf and convert it into qualified additive feedstock, reducing dependence on virgin imports.

Asia-Pacific delivered the highest 26.25% CAGR and is projected to remain the growth engine through 2030. China dominates entry-level printer exports, providing cost advantages for bio-based polymers. Europe balances strong research and development capability with some of the strictest environmental regulations worldwide. The EU's circular-economy directives encourage recycled feedstock adoption, positioning bio-derived PLA and PA11 for accelerated volume gains.

- 3D Systems, Inc.

- Arkema

- BASF

- CRP TECHNOLOGY S.r.l.

- Custom Resin Solutions

- EnvisionTEC US LLC

- EOS GmbH

- Evonik Industries AG

- General Electric Company

- Henkel AG & Co. KGaA

- Hoganas AB

- HP Development Company, L.P.

- Materialise

- Renishaw plc

- Sandvik AB

- Solvay

- Stratasys

- voxeljet AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Metal Powder Usage for Serial Aerospace and Medical Production

- 4.2.2 Rapid Advances in High-performance Polymers

- 4.2.3 Surge in Demand from Automotive Application

- 4.2.4 Mass-customization Momentum in Healthcare and Consumer Goods

- 4.2.5 Increase in the Adoption of Bio-based/Biodegradable Feedstocks

- 4.3 Market Restraints

- 4.3.1 High Equipment and Material Cost

- 4.3.2 Stringent Certification for Aerospace and Medical Grades

- 4.3.3 Availability of Limited Types of Materials

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Plastics

- 5.1.1.1 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.1.2 Polylactic Acid (PLA)

- 5.1.1.3 Nylon

- 5.1.1.4 Polyamide

- 5.1.1.5 Polycarbonate

- 5.1.1.6 Other Plastics (Composites, Biodegradable Polymers, etc.)

- 5.1.2 Metals

- 5.1.3 Ceramics

- 5.1.4 Other Materials (Gases, Waxes)

- 5.1.1 Plastics

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Filament

- 5.2.3 Liquid/Resin

- 5.3 By End-user Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Medical

- 5.3.4 Consumer Electronics

- 5.3.5 Others (Energy and Power, Industrial Machinery, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 South Korea

- 5.4.1.4 India

- 5.4.1.5 Singapore

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3D Systems, Inc.

- 6.4.2 Arkema

- 6.4.3 BASF

- 6.4.4 CRP TECHNOLOGY S.r.l.

- 6.4.5 Custom Resin Solutions

- 6.4.6 EnvisionTEC US LLC

- 6.4.7 EOS GmbH

- 6.4.8 Evonik Industries AG

- 6.4.9 General Electric Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Hoganas AB

- 6.4.12 HP Development Company, L.P.

- 6.4.13 Materialise

- 6.4.14 Renishaw plc

- 6.4.15 Sandvik AB

- 6.4.16 Solvay

- 6.4.17 Stratasys

- 6.4.18 voxeljet AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Introduction of New Materials, like Graphene Opens Up New Applications

- 7.3 Adoption of 3D Printing Technology in Home Printing