|

시장보고서

상품코드

1686263

산업용 수요 반응 관리 시스템 - 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Industrial Demand Response Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

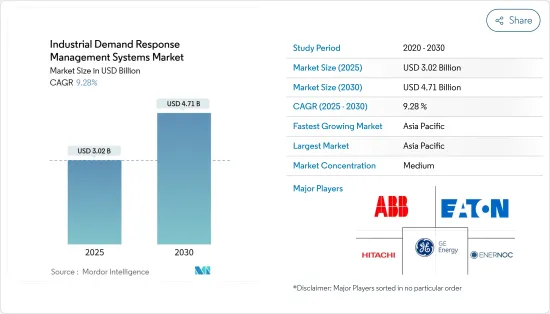

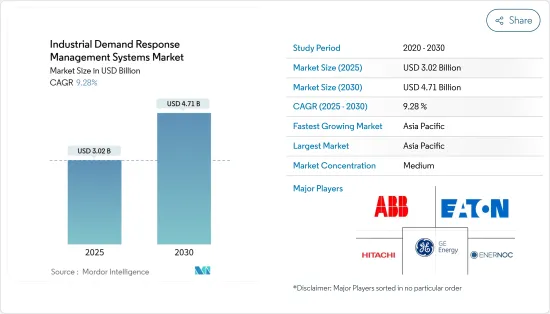

산업용 수요 반응 관리 시스템 시장 규모는 2025년에 30억 2,000만 달러, 2030년에는 47억 1,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025년-2030년) CAGR은 9.28%를 나타낼 전망입니다.

주요 하이라이트

- 중기적으로는 효율적인 에너지 관리 시스템에 대한 요구와 재생 가능 에너지원의 보급 확대가 시장을 견인할 것으로 예측된다

- 한편, 산업용 수요 반응 관리 시스템에 관한 프라이버시에 대한 우려가 시장 성장의 방해가 될 것으로 예상됩니다.

- 하지만 스마트 그리드 기술의 채용이 증가하고 있는 것은 예측 기간 중 시장에 있어서 큰 기회가 될 것으로 예상됩니다.

- 아시아태평양은 재생 가능 에너지원의 채용이 증가하고 있기 때문에 시장에서 큰 점유율을 차지할 것으로 예상됩니다.

산업용 수요 반응 관리 시스템 시장 동향

자동 수요 반응 관리 시스템이 큰 점유율을 차지할 전망

- 매우 중요한 시점에서 자동 수요 반응 관리 시스템(ADRMS) 시장은 다양한 통신 시스템에 의존하면서도 제한적인 규모로 고객에 대한 인센티브가 있지만 ADRMS의 초기 전개를 하고 있습니다. ADRMS는 유틸리티와 소비자 모두에게 비용 최적화를 약속할 뿐만 아니라 정책 입안자와 유틸리티에도 권한을 부여합니다.

- 송전망의 근대화와 스마트 그리드 시스템에 대한 투자는 증가 경향에 있어 가까운 미래의 배치가 급무임을 나타내고 있습니다. 나란히 대규모 ADRMS 도입의 주요 무대가 되고 있습니다.이 급증은 재생 가능 에너지 통합 프로그램과, 효율적인 전력 시스템에의 협조적인 추진이 원동력이 되고 있습니다.

- 주목할만한 움직임으로 Tata Power는 AutoGrid와 제휴하여 AI 중심의 에너지 관리 이니셔티브를 뭄바이에서 전개했습니다.

- 또 하나의 중요한 협력 관계로는 하니웰과 에넬이 2024년 5월, 자동 디맨드 리스폰스 시스템을 통해 에너지 절약의 강화를 도모했습니다. 동화 시스템과 원활하게 통합할 수 있게 되었습니다. 에넬의 플렉스 업은 기업의 자동화 노력에 자금을 제공할 뿐만 아니라, 수요 반응 프로그램에의 참가를 촉진해, 피크시의 전력 사용량을 삭감했을 경우에 보상을 줍니다.

- 2024년 3월 현재 미국의 데이터센터 수는 5,381곳에서 세계 1위를 차지했으며, 이어 독일이 521곳, 영국이 514곳으로 그 뒤를 이었습니다. 에너지 효율화의 대처를 지지해, 재정적으로 지원하는 것으로, 소비자에게 인센티브를 주어, 수요 반응 이니셔티브에의 적극적인 관여를 촉구하고 있습니다.

- 2024년 12월, Energy Vault 및 RackScale Data Centers는 전략적 제휴를 맺고 데이터센터를 위한 2GW의 전력 할당을 시야에 두고 있습니다. 양사의 초점은 2GW/20GWh의 용량을 자랑하는 B-Nest 인프라입니다. 수요 반응 파트너십을 통해 수익의 길을 열어주는 것입니다.

- 이러한 개발에 의해 자동 수요 반응 관리 시스템 부문은 산업용 수요 반응 관리 시스템 시장에서 큰 점유율을 획득할 전망입니다.

아시아태평양이 현저한 성장을 이루

- 아시아태평양의 산업용 수요 반응 관리 시스템 시장은 예측 기간 중에 큰 성장이 예상됩니다.

- 중국은 피크 전력 수요를 삭감하고 재생 가능 에너지를 수요에 적합시키는 수단으로 수요측 관리(DSM) 프로그램의 실시에 점점 힘을 쏟고 있습니다.

- 중국은 또한 세계 최대급의 석유 및 가스 정제 능력을 갖고 있습니다.

- 게다가 인도에서는 경제 성장에 의해 전력 수요가 증가하고 있지만, 에너지 자원이 한정되어 있기 때문에 자원을 과잉 개발하여 그 결과 전력 수요가 증가하고 있습니다.

- 2023년 2월 가상 발전소와 분산 에너지 관리 시스템(DERMS)공급자인 오토그리드사는 인도 최대의 종합 전력회사 중 하나인 타타 파워사와의 공동 이니셔티브를 발표했습니다.

- 또한 타타 파워는 2025년 여름까지 인도 최대의 도시인 뭄바이 고객을 위한 새로운 수요 반응 관리 프로그램을 전개할 예정입니다.

- 이 지역에서의 산업 부문의 개발과 수요 반응 프로그램의 채용을 고려하면, 이 지역은 장래에 DRMS의 대규모 수요를 눈에 띄게 될 것으로 예상됩니다.

산업용 수요 반응 관리 시스템 산업 개요

산업용 수요 반응 관리 시스템 시장은 반쯤 분열되어 있습니다. 시장의 주요 기업(특별한 순서 없음)에는 Eaton Corporation PLC, 히타치 제작소, EnerNOC Inc., General Electric Company, ABB Ltd. 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2030년까지 시장 규모 및 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 시장 역학

- 성장 촉진요인

- 효율적인 에너지 관리 시스템에 대한 요구

- 재생 가능 에너지원의 보급 확대

- 억제요인

- 산업용 수요 반응 관리 시스템에 대한 프라이버시 우려

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협 제품 및 서비스

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 세분화

- 유형

- 기존 디맨드 리스폰스

- 자동 수요 반응

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 북유럽

- 튀르키예

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 칠레

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 카타르

- 이집트

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Schneider Electric SE

- Siemens AG

- Hitachi Ltd

- Mitsubishi Electric Corporation

- ABB Ltd.

- Alstom SA

- General Electric Company

- Eaton Corporation PLC

- Itron Inc

- EnerNOC Inc.

- Uplight, Inc.

- List of Other Prominent Companies(Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 시장 랭킹 분석

제7장 시장 기회와 앞으로의 동향

- 스마트 그리드 기술 채용 확대

The Industrial Demand Response Management Systems Market size is estimated at USD 3.02 billion in 2025, and is expected to reach USD 4.71 billion by 2030, at a CAGR of 9.28% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the need for efficient energy management systems and the growing penetration of renewable energy sources are expected to drive the market

- On the other hand, privacy concerns about industrial demand response management systems are expected to hamper the market's growth.

- Nevertheless, the rising adoption of smart grid technologies is expected to be a significant opportunity for the market in the forecast period.

- Asia-Pacific is expected to have a significant share of the market due to the increasing adoption of renewable energy sources.

Industrial Demand Response Management Systems Market Trends

Automated Demand Response Management System is Expected to have Significant Share

- At a pivotal moment, the Automated Demand Response Management System (ADRMS) market is witnessing the initial deployment of ADRMS, albeit on a limited scale and incentivized for customers, all while relying on diverse communication systems. Looking ahead, these systems hold the potential to disrupt the electricity landscape. ADRMS not only promise cost optimization for both utilities and consumers but also empower policymakers and utilities. With ADRMS, they can craft intelligent strategies for grid modernization, set achievable targets, and devise robust solutions to counter global warming's impacts.

- Investment in grid modernization and smart grid systems is on the rise, signaling a pressing need for deployment in the near future. Developed markets, including the U.S., Japan, and Germany, alongside emerging giants like China, are becoming prime arenas for large-scale ADRMS implementation. This surge is driven by renewable integration programs and a concerted push towards efficient electricity systems.

- In a notable move, Tata Power, in partnership with AutoGrid, rolled out an AI-centric energy management initiative in Mumbai. This program, targeting Tata Power's diverse clientele, aims to tackle peak demand issues, resonate with India's clean energy ambitions, and bolster Net Zero objectives.

- In another significant collaboration, Honeywell and Enel, in May 2024, sought to enhance energy savings through automated demand response systems. Their partnership allows Enel North America's FlexUp solutions to seamlessly integrate with Honeywell's automation systems. Enel's FlexUp not only finances businesses' automation endeavors but also boosts their participation in demand response programs, rewarding them for reducing electricity use during peak times.

- As of March 2024, the U.S. led the world with 5,381 data centers, followed by Germany with 521 and the U.K. with 514. Many governments view energy efficiency as pivotal for demand response. By endorsing and financially backing energy efficiency efforts, they incentivize consumers, fostering active engagement in demand response initiatives.

- In December 2024, Energy Vault and RackScale Data Centers forged a strategic alliance, eyeing a 2GW power allocation for data centers. Their focus is on the B-Nest infrastructure, boasting a capacity of 2 GW/20 GWh. This collaboration not only accelerates their portfolio expansion but also opens avenues for revenue through demand response partnerships with local utilities. By engaging in these demand response events, particularly during peak periods, RackScale Data Centers bolster grid stability, aiding local utilities in their renewable energy integration endeavors.

- Given these developments, the Automated Demand Response Management System segment is poised to capture a substantial share of the Industrial Demand Response Management Systems Market.

Asia-Pacific to Witness a Significant Growth

- The market for industrial demand response management systems in the Asia-Pacific region is expected to witness significant growth during the forecast period.

- China is making increasing efforts to implement demand-side management (DSM) programs as a means of reducing peak electricity demand and matching renewable energy with demand. In addition to reducing emissions, integrating renewable energy sources, shaving peak power, improving load factor, and pursuing net zero energy, these efforts are motivated by the country's commitment to address multiple challenges.

- China also has one of the world's largest oil & gas refining capacities. In 2023, it had an oil refining capacity of about 18,484 thousand barrels per day, witnessed a 7% increase from 2022. Besides, China contributes to close to 18% of the global refining capacity. Further, the country has also been constructing new refineries and upgrading and adding capacity to older ones.

- Moreover, Power demand has increased in India owing to the economic growth, but the country's limited energy resources have resulted in overexploitation of these resources, resulting in a rise in power demand. The focus in India is shifting towards restructuring the power sector so that rather than generation adapting to demand, demand can be tailored to meet generation requirements to maintain demand-supply balance, thus reducing strain on power infrastructure.

- In February 2023, AutoGrid, a provider of virtual power plants and distributed energy management systems (DERMS), announced a collaborative initiative with Tata Power, one of India's largest integrated power companies. In addition to supporting India's clean energy transition, this pioneering program will help address peak demand in residential, commercial, and industrial areas.

- Also, by the summer of 2025, Tata Power plans to roll out a new Demand Response Management Program to serve its customers in Mumbai, India's largest city. The program will involve 6,000 large commercial and industrial customers to attain 75 MW of peak capacity decrease within the first six months and then continue to rise to 200 MW.

- Considering the development of the industrial sector in the region and the adoption of demand response programs, the region is expected to witness a massive demand for DRMS in the future.

Industrial Demand Response Management Systems Industry Overview

The industrial demand response system market is semi-fragmented. Some of the major players in the market (in no particular order) include Eaton Corporation PLC, Hitachi Ltd, EnerNOC Inc., General Electric Company, ABB Ltd., and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, until 2030

- 4.3 Recent Trends and Developments

- 4.4 Market Dynamics

- 4.4.1 Drivers

- 4.4.1.1 Need for Efficient Energy Management Systems

- 4.4.1.2 Growing Penetration of Renewable Energy Sources

- 4.4.2 Restraints

- 4.4.2.1 Privacy Concerns on the Industrial Demand Response Management Systems

- 4.4.1 Drivers

- 4.5 Supply-Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes Products and Services

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Conventional Demand Response

- 5.1.2 Automated Demand Response

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Asia-Pacific

- 5.2.2.1 China

- 5.2.2.2 India

- 5.2.2.3 Japan

- 5.2.2.4 Australia

- 5.2.2.5 Malaysia

- 5.2.2.6 Thailand

- 5.2.2.7 Indonesia

- 5.2.2.8 Vietnam

- 5.2.2.9 Rest of Asia-pacific

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 France

- 5.2.3.3 United Kingdom

- 5.2.3.4 Italy

- 5.2.3.5 Spain

- 5.2.3.6 Nordic

- 5.2.3.7 Turkey

- 5.2.3.8 Russia

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Chile

- 5.2.4.4 Colombia

- 5.2.4.5 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Qatar

- 5.2.5.5 Egypt

- 5.2.5.6 Nigeria

- 5.2.5.7 Rest of Middle East & Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Schneider Electric SE

- 6.3.2 Siemens AG

- 6.3.3 Hitachi Ltd

- 6.3.4 Mitsubishi Electric Corporation

- 6.3.5 ABB Ltd.

- 6.3.6 Alstom SA

- 6.3.7 General Electric Company

- 6.3.8 Eaton Corporation PLC

- 6.3.9 Itron Inc

- 6.3.10 EnerNOC Inc.

- 6.3.11 Uplight, Inc.

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Adoption of Smart Grid Technologies