|

시장보고서

상품코드

1549956

자동차 보증 관리 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Automotive Warranty Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

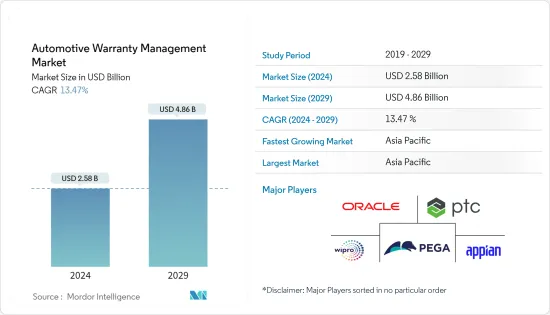

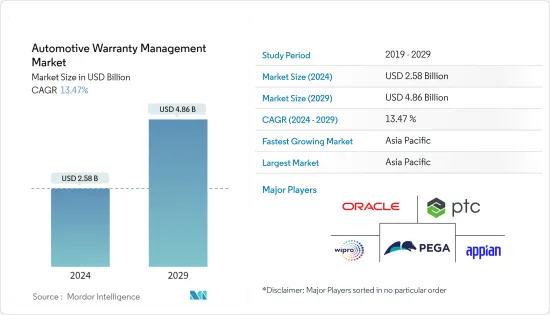

자동차 보증 관리 시장 규모는 2024년 25억 8,000만 달러로 추정되며, 2029년에는 48억 6,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 13.47%의 CAGR로 성장할 것으로 예상됩니다.

자동차 산업과 공급망 산업이 보증 소프트웨어 채택에서 가장 큰 점유율을 차지하고 있기 때문에 자동차 산업의 생산량 증가가 시장을 이끄는 중요한 요인으로 작용하고 있습니다. 또한, 커넥티드카에 대한 소비자의 선호도가 높아지면서 세계 자동차 수요에 영향을 미쳐 시장을 견인할 것으로 예상됩니다.

현재 OEM이 보증 관리와 관련하여 가장 중요하게 생각하는 것은 자체 정책과 절차를 준수하고 규정대로 수리를 수행하여 자동차의 품질과 신뢰성을 유지하는 것입니다. 그러나 비용 절감의 달성도 마찬가지로 중요합니다. 따라서 OEM들은 수익성 향상, 고객 만족도 향상, 경쟁력 유지를 위해 보증 관리 솔루션을 도입하는 사례가 늘고 있습니다.

자동차 회사들은 보증 비용 절감, 고객 만족도 향상, 재무 실적 강화를 위해 제품 품질 향상을 위해 끊임없이 노력하고 있습니다. 그러나 신제품 수요 급증, 경쟁 심화, 기술 발전, 공급망 혼란 등의 요인으로 인해 품질이 저해되는 경우가 많습니다. 평균적으로 자동차 회사 및 산업 회사는 연간 매출액의 1.5-2.5%의 보증 클레임 비용이 발생하며, 이는 상당한 수익 손실과 고객 만족도 저하로 이어집니다. 기업들은 고객 충성도를 유지하기 위해 이러한 문제를 완화하기 위해 보증 서비스 및 부품 교환을 더 자주, 더 빠르게 처리하고 있습니다. 이러한 과제를 고려할 때, 자동차 제조업체는 인공지능(AI)과 머신러닝(ML) 같은 기술을 기존 보증 관리 시스템에 통합하는 것이 필수적입니다.

이에 따라 일부 시장 기업들은 AI 및 ML 기반 솔루션을 도입하고 있습니다. 예를 들어, 캘리포니아에 본사를 두고 자동차 업계에 인공지능 및 의사결정 분석 솔루션을 제공하는 소프트웨어 회사인 FrogData는 2023년 8월, 대리점의 보증 청구 프로세스를 최적화하기 위해 설계된 엔드투엔드 원격 보증 관리 서비스인 WarrantyMind AI를 발표했습니다.

그러나 이러한 솔루션은 고객 및 차량의 기밀 데이터를 다루기 때문에 보안 침해는 브랜드 평판과 고객 신뢰에 치명적일 수 있습니다. 따라서 데이터 및 개인정보 도난 문제는 시장 성장의 걸림돌로 작용하고 있으며, 데이터 보호를 위한 사이버 보안 대책에 대한 투자가 필요한 상황입니다.

세계 자동차 보증 관리 시장은 COVID-19 팬데믹으로 인해 도전뿐만 아니라 기회에도 직면했습니다. 봉쇄와 공급망 중단으로 인해 부품 부족과 수리 지연이 발생하여 보증 클레임이 지연되고 보증 관리 시스템에 압박을 가하고 있습니다. 또한, 이 위기는 데이터 기반 의사결정의 가치를 부각시켰고, 트렌드를 파악하고 서비스 센터의 효율성을 높이기 위해 데이터 분석 기능을 갖춘 자동차 보증 시스템에 대한 수요를 부각시켰습니다.

자동차 보증 관리 시장 동향

클라우드 기반 보증 관리 시스템이 시장 성장을 크게 견인할 전망

COVID-19 팬데믹으로 인해 클라우드 기반 보증 관리 솔루션은 원격 근무를 용이하게 하고, 봉쇄 기간 중에도 보증 팀의 데이터에 대한 지속적인 액세스를 보장했습니다. 이러한 클라우드 도입 추세는 팬데믹 이후에도 지속될 것으로 예상되며, 자동차 산업에서 클라우드 기반 보증 관리 솔루션의 채택을 촉진하고 있습니다.

자동차 업계에서 클라우드를 도입하는 것은 확장성, 비용 절감, 전 세계에 배치된 팀, 설계자 및 제조 부서가 실시간으로 데이터에 액세스하고 공유할 수 있는 협업 개선 등 여러 가지 이점이 있어 기술 혁신과 제품 개발 주기를 단축할 수 있습니다. 촉진하고 있습니다. 이러한 장점은 클라우드 기반 보증 관리 솔루션의 채택을 더욱 촉진할 것으로 예상됩니다.

자동차 산업에서 인더스트리얼 클라우드 도입이 증가하고 있으며, 이는 기업들에게 가치사슬 재구축의 기회를 제공하고 있습니다. 대표적인 사례로 독일 자동차 제조업체인 폭스바겐은 2023년 6월 AWS와 포르쉐 산하 IT 컨설팅 업체인 MHP와 협력하여 자동차 제조에 특화된 인더스트리얼 클라우드를 구축한 바 있습니다. 이러한 클라우드 도입의 진전으로 향후 몇 년 동안 클라우드 기반 자동차 보증 관리 솔루션에 대한 수요가 증가할 것으로 예상됩니다.

또한, 자동차를 포함한 제조업 전반에서 클라우드 서비스 도입이 빠르게 진행되고 있어, 클라우드 인프라가 구축된 클라우드 기반 보증 관리 솔루션의 도입이 확대될 것으로 예상됩니다. 예를 들어, 일본 총무성에 따르면 일본 제조업에서 클라우드 서비스를 이용하는 기업의 비율은 2022년 71.6%에서 2023년 79.2%에 달할 것으로 예상하고 있습니다.

아시아태평양이 가장 높은 성장률 기록할 것으로 전망

아시아태평양은 중국, 인도, 일본, 한국 등의 국가들이 자동차 판매량이 크게 증가하면서 세계 자동차 산업의 성장을 주도하고 있습니다. 이러한 급격한 성장은 특히 첨단 기능과 전자장치를 탑재한 최신 자동차의 증가로 인해 더욱 복잡한 보증 관리와 복잡해지는 보증 청구에 대응할 수 있는 첨단 시스템을 필요로 하고 있습니다.

국제자동차산업협회(OICA)에 따르면 2023년 중동 지역을 포함한 아시아태평양에서 약 4,260만 대의 승용차가 판매되었으며, 그 중 2,600만 대 이상이 중국에서 판매되었습니다. 한편, 2022년 아시아태평양에서 판매된 승용차는 약 3,750만 대였습니다. 이러한 자동차 판매 증가로 인해 제조업체와 딜러는 보증 기록을 유지하고 고객 경험을 개선해야 하는 과제를 안고 있습니다.

고객의 기대치가 진화하고 보증 기간이 길어지면서 시장 성장을 견인하고 있습니다. 이 지역의 소비자들은 점점 더 첨단 기술에 익숙해지고 있으며, 원활한 보증 경험을 원하고 있습니다. 여기에는 효율적인 클레임 처리, 투명한 커뮤니케이션, 보증 정보에 대한 온라인 액세스 등이 포함됩니다. 이에 따라 자동차 제조업체들은 경쟁력을 유지하기 위해 보증 연장 옵션을 도입하고 있으며, 이는 더 긴 클레임 수명을 지원하는 고급 보증 관리 솔루션에 대한 수요를 촉진하고 있습니다.

또한, 자동차 제조업체와 딜러는 수리 비용과 부품 가격 상승으로 인해 애프터 세일즈 마진에 압박을 받고 있습니다. 보증 관리 시스템의 도입은 프로세스를 간소화하고 관리 비용을 절감하며 부정 클레임을 식별하는 데 도움이 되고 있습니다. 이에 따라 자동차 제조업체와 딜러들은 비용 절감과 운영 효율성에 점점 더 중점을 두고 있으며, 자동차 보증 관리 솔루션의 채택이 증가하고 있습니다.

자동차 보증 관리 산업 개요

자동차 보증 관리 시장은 적당히 통합되어 있으며, 시장 점유율이 높은 기업은 소수에 불과합니다. 이 시장에서 큰 점유율을 차지하고 있는 주요 기업들은 경쟁 시장 점유율을 확보하기 위해 협업, 사업 확장, 인수합병(M&A) 등 전략적 이니셔티브를 통해 세계 고객 기반을 확대하는 데 주력하고 있습니다.

2024년 6월 - 서비스 라이프사이클 관리 솔루션 제공업체인 타반트(Tavant)와 북미 대형 트럭 제조업체이자 중형 트럭 및 특수상용차 생산업체인 Daimler Truck North America LLC가 고객 경험과 딜러 생산성을 향상시키기 위해 파트너십을 체결했습니다. 고객 경험과 딜러 생산성을 높이기 위해 Daimler Truck의 서비스 업무를 혁신하는 파트너십을 체결했습니다. 이번 파트너십은 Daimler Truck Group과 Tavant와의 장기적인 세계 기술 파트너십의 확장을 의미합니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자/소비자의 협상력

- 신규 참여업체의 위협

- 경쟁 기업 간의 경쟁 관계

- 대체품의 위협

- 업계 이해관계자 분석

- 거시경제 동향의 영향(불황, 러시아·우크라이나 전쟁 등)

제5장 시장 역학

- 시장 성장 촉진요인

- AI, ML, IoT, 빅데이터 등의 테크놀러지의 도입

- 시장의 통합과 구독형 모델

- 보험금 청구 관리 자동화와 수고를 생략하는 요구 상승

- 시장 과제

- 데이터와 개인정보 도난/데이터 누설

제6장 시장 세분화

- 서비스별

- 소프트웨어

- 서비스

- 전개별

- 온프레미스

- 클라우드 기반

- 조직 규모별

- 중소기업(SMEs)

- 대기업

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 상황

- 기업 개요

- Oracle Corporation

- PTC Inc.

- Wipro Limited

- Appian Corporation

- Pegasystems Inc.

- MSX International

- Annata

- SKYLYZE

- IFS Americas Inc.

- SYNCRON HOLDING AB

제8장 투자 분석

제9장 시장 향후 전망

ksm 24.09.13The Automotive Warranty Management Market size is estimated at USD 2.58 billion in 2024, and is expected to reach USD 4.86 billion by 2029, growing at a CAGR of 13.47% during the forecast period (2024-2029).

The growing production in the automotive sector is a significant factor driving the market, as the automotive and supply chain industries account for the largest share in the adoption of warranty software. Moreover, the consumer propensity toward adopting connected vehicles is also expected to influence the global demand for automobiles, thereby driving the market.

Nowadays, the primary focus of OEMs when it comes to warranty management is compliance with their policies and procedures, ensuring repairs are performed as prescribed and maintaining the quality and reliability of their vehicles. However, achieving cost savings is equally important for them. Thus, the adoption of warranty management solutions among OEMs is growing to improve profitability, enhance customer satisfaction, and remain competitive.

Automotive companies are constantly striving to boost product quality, aiming to reduce warranty costs, elevate customer satisfaction, and bolster financial performance. However, the quality is frequently hampered by factors like surging new product demands, heightened competition, technological advancements, and disruptions in the supply chain. On average, automotive and industrial firms witness warranty claims expenses between 1.5-2.5% of their annual revenue, translating to significant revenue losses and poor customer satisfaction. Companies frequently expedite warranty services and part replacements to mitigate these challenges to uphold customer loyalty. Given these challenges, it becomes imperative for automakers to integrate technologies like artificial intelligence (AI) and machine learning (ML) into their traditional warranty management systems.

In response, some market players are introducing AI- and ML-based solutions. For instance, in August 2023, FrogData, a software company based in California that offers artificial intelligence and decision analytics solutions to the automotive industry, introduced WarrantyMind AI, an end-to-end remote warranty administration service designed to optimize the warranty claims process for dealerships.

However, as these solutions handle sensitive customer and vehicle data, security breaches become essential to brand reputation and customer trust. Thus, data and identity theft challenges are hampering market growth, necessitating investment in cybersecurity measures to protect data.

The global automotive warranty management market faced challenges as well as opportunities amid the COVID-19 pandemic. Lockdowns and supply chain disruptions led to a shortage of parts and delays in repair, creating a backlog of warranty claims that strained warranty management systems. Moreover, the crisis underscored the value of data-driven decisions, highlighting the demand for automotive warranty systems equipped with data analytics capabilities to identify trends and enhance service center efficiency.

Automotive Warranty Management Market Trends

Cloud-based Warranty Management Systems is Expected to Drive Market Growth Significantly

As a result of the COVID-19 pandemic, the cloud-based warranty management solutions facilitated remote work and ensured continued access to data for warranty teams during lockdowns. This trend toward cloud adoption is expected to continue post-pandemic, driving the adoption of cloud-based warranty management solutions in the automotive industry.

The growing adoption of the cloud in the automotive industry, owing to several benefits such as scalability, reduced costs, and improved collaboration between globally located teams, designers, and manufacturing units to access and share data in real time, is driving innovation and faster product development cycles. Such advantages are further expected to drive the adoption of cloud-based warranty management solutions.

The adoption of industry cloud in the automotive sector is on the rise, offering enterprises an opportunity to reconstruct their value chains. A notable example is Volkswagen, the German automaker that collaborated with AWS and MHP, an IT consultant under Porsche, to establish its industry cloud tailored for automobile manufacturing in June 2023. These advancements in cloud adoption are anticipated to drive the demand for cloud-based automotive warranty management solutions in the coming years.

Furthermore, the rapidly growing adoption of cloud services across the manufacturing industries, including automotive, is expected to support the adoption of cloud-based warranty management solutions with established cloud infrastructure. For instance, according to the Ministry of Internal Affairs and Communications Japan, the share of manufacturing companies in Japan that use cloud services reached 79.2% in 2023 from 71.6% in 2022.

Asia-Pacific is Expected to Register the Highest Growth Rate

Asia-Pacific leads the global automobile industry in growth, driven by countries such as China, India, Japan, and South Korea, witnessing a significant surge in vehicle sales. This surge has resulted in a larger pool of vehicles, particularly modern cars equipped with advanced features and electronics, necessitating more intricate warranty management and sophisticated systems to handle the rising complexity of warranty claims.

According to the International Organization of Motor Vehicle Manufacturers (OICA), in 2023, about 42.6 million passenger cars were sold within Asia-Pacific, including the Middle East, of which over 26 million were sold in China. Comparatively, approximately 37.5 million passenger cars were sold in Asia-Pacific in 2022. This rise in vehicle sales challenges manufacturers and dealers to maintain warranty records and enhance customer experience.

Evolving customer expectations and longer warranty durations are bolstering market growth. Consumers in the region are becoming increasingly tech-savvy, so they now demand a seamless warranty experience. This includes efficient claim processing, transparent communication, and online access to warranty information. Consequently, automakers are rolling out extended warranty options to stay competitive, driving the demand for advanced warranty management solutions to handle these longer claim lifespans.

In addition, automakers and dealers are experiencing pressure on after-sales margins due to rising repair costs and parts prices. Implementing warranty management systems is helping them streamline processes, reduce administrative costs, and identify fraudulent claims. Thus, automakers and dealers are increasingly focusing on cost reduction and operational efficiency, leading to increased adoption of automotive warranty management solutions.

Automotive Warranty Management Industry Overview

The automotive warranty management market is moderately consolidated, with few market players holding significant market share. The major players with prominent shares in the market are focusing on expanding their global customer base through strategic initiatives such as collaboration, expansion, mergers & acquisitions, and others to gain competitive market share.

June 2024 - Tavant, a provider of Service Lifecycle Management solutions, and Daimler Truck North America LLC, the heavy-duty truck manufacturer in North America and a producer of medium-duty trucks and specialized commercial vehicles, formed a partnership to transform Daimler Truck's service operations to enhance customer experience and dealer productivity. This partnership marks the expansion of a longer global technology partnership between Daimler Truck Group and Tavant.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Stakeholder Analysis

- 4.4 Impact of Macroeconomic Trends (Recession, Russia-Ukraine war, etc.)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Implementation of Technologies Such as AI, ML, IoT and Big Data

- 5.1.2 Market Consolidation and Subscription-based Model

- 5.1.3 Rising Automation and Need for Hassle-free Claim Management

- 5.2 Market Challenges

- 5.2.1 Data and Identity Theft/Data Breaches

6 MARKET SEGMENTATION

- 6.1 By Offering

- 6.1.1 Software

- 6.1.2 Services

- 6.2 By Deployment

- 6.2.1 On Premise

- 6.2.2 Cloud-based

- 6.3 By Organization Size

- 6.3.1 Small and Medium Enterprises (SMEs)

- 6.3.2 Large Enterprises

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Oracle Corporation

- 7.1.2 PTC Inc.

- 7.1.3 Wipro Limited

- 7.1.4 Appian Corporation

- 7.1.5 Pegasystems Inc.

- 7.1.6 MSX International

- 7.1.7 Annata

- 7.1.8 SKYLYZE

- 7.1.9 IFS Americas Inc.

- 7.1.10 SYNCRON HOLDING AB