|

시장보고서

상품코드

1693554

유럽의 보증 관리 시스템 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Warranty Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

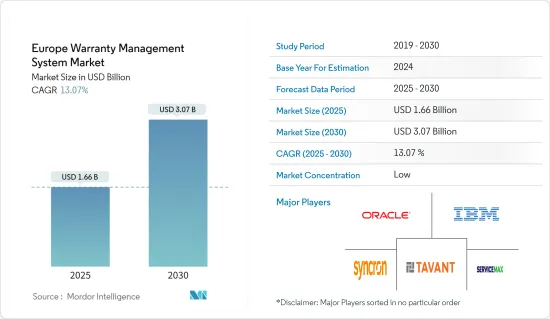

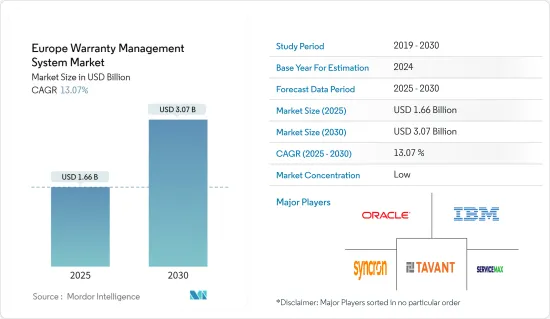

유럽의 보증 관리 시스템 시장 규모는 2025년 16억 6,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 13.07%로 확대되어, 2030년에는 30억 7,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 모든 서비스 사업에서 중요한 것은 보증 관리입니다. 고객 자산의 보증 범위와 데이터를 보고, 액세스하고, 자동으로 추적하는 능력은 중요합니다. 보증 관리를 통해 기업은 판매 손실이나 고객 반감을 사지 않습니다.

- 보증 관리 시스템은 보증 클레임 처리 및 설치 기반 자산 추적을 자동화하여 서비스 운영자가 보증, 클레임, 자산을 설계, 관리, 추적 및 처리할 수 있도록 합니다. 혁신적인 보증 관리 시스템(WMS)은 AI 및 머신러닝 기능과 함께 고객 만족도를 보장하고 유럽 시장을 견인하고 있습니다.

- 자동차 업계의 보증 관리는 공급업체부터 딜러, 최종 소비자에 이르는 모든 프로세스에 걸친 풍부한 데이터가 다양한 수준에서 오류 확률을 높이기 때문에 복잡합니다. 각 딜러와 제조업체는 보증 청구 및 데이터 취급에 대한 고유한 절차를 가지고 있지만, 기존 시스템에서는 신뢰성과 일관된 결과를 얻지 못하는 경우가 많으며, 유럽 보증 관리 시스템의 도입에 박차를 가하고 있습니다.

- 보증 관리 시스템은 광범위한 비즈니스 규칙을 사용하여 모든 혜택 기능을 검증하고 진단 및 모바일 장치의 정보 스트림을 보증 청구 양식에 즉시 통합하여 보증 정보의 정확성과 품질을 향상시킵니다.

- 그러나 유럽의 보증 관리 시스템에서는 경쟁이 격화되고 가격감응도가 높아져 최종 사용자가 보증관리시스템을 선택할 때 가격보다 서비스 기능을 타협할 가능성이 있기 때문에 공급자는 시장의 성장을 제한하고 있습니다.

- COVID-19의 유행에 따라, 자동화 기술로의 시프트가 지역 전체에서 뚜렷해지고 있습니다.

유럽 보증 관리 시스템 시장 동향

클라우드 배포 부문이 주요 시장 점유율을 차지

- 새로운 데이터 스토리지를 구축하고 유지하는 대신 클라우드로 데이터를 마이그레이션함으로써 비용과 리소스를 절약하는 중요성에 대한 기업의 인식이 높아지고 있다는 것이 클라우드 기반 솔루션에 대한 수요, 언디맨드 보증 관리 시스템의 채용을 뒷받침하고 있습니다. 또한, 클라우드 플랫폼과 에코시스템은 복수의 이점이 있기 때문에 향후 수년간, 디지털 혁신의 페이스와 규모를 폭발적으로 확대시키는 발사대로서의 역할을 완수할 것으로 예상됩니다.

- 게다가, 퍼블릭 클라우드 서비스를 도입함으로써, 신뢰성의 경계가 조직의 틀을 넘어 확산되고 클라우드 인프라에 있어서 보안이 필수적인 요소가 되었습니다. Google Cloud, Dropbox, Microsoft Azure 등의 클라우드 서비스의 채용이 증가하고, 이러한 툴이 비즈니스 프로세스의 필수적인 부분으로 대두하는 가운데, 기업은 온디맨드의 보증 관리 솔루션을 도입함으로써 기밀 데이터의 제어를 잃는 등의 보안 문제에 대처해야 합니다.

- 이 지역에서 가장 급성장하고 있는 시장 중 하나가 클라우드이며, 이 분야에 대한 투자 증가는 조사 대상 업계의 영역을 넓히고 있습니다. 대기업 서비스 제공업체는 국내의 광범위한 퍼블릭 클라우드 환경이나 하이브리드 클라우드 환경, 하이퍼스케일 서비스의 관리를 점점 강화하고 있습니다. 예를 들면, Oracle은 독일과 스페인이 EU 최초의 2개의 소블린 구역을 호스팅할 예정이며, 이 지역의 현재의 퍼블릭 OCI 지역과는 논리적으로도 물리적으로 구별됩니다.

- 또한 클라우드 기반 솔루션은 설비 투자 요건이 낮다는 점에서 비즈니스 설득력이 높아집니다. 기업은 용도의 비용을 보다 정확하게 예측할 수 있기 때문에 기업은 기술을 도입하기 위한 초기 비용을 덜 필요로 합니다.

- 게다가 클라우드 기반 시스템의 채용이 확대되고 있는 것도, 시장의 성장에 기여하고 있습니다. 클라우드 컴퓨팅에는 클라우드 인프라와 소프트웨어 용도의 두 가지 구성 요소가 포함되어 있습니다.

독일이 가장 빠른 성장을 기록할 전망

- 독일은 다양한 산업의 정부 규제와 고객의 다양한 요구를 충족시키기 위한 소프트웨어 개발 증가로 이 지역에서 가장 급성장하고 있는 국가 중 하나입니다.

- 최근 독일의 법률가는 고객에게 유리한 보증 규제를 강화하는 새로운 판매법을 통과했습니다. 이 제한이 적용되는 것은 구입 후 4개월이 경과한 후입니다.

- 자동차 제조업체와 보증 회사 간의 파트너십 증가는 시장 연구를 촉진할 것으로 예상됩니다. 이러한 개발은 워크플로우를 간소화하고 클레임을 추적하기 위해 제품 포트폴리오에 새로운 솔루션을 배포하는 것을 지원합니다. 예를 들어, Europe Assistance Germany는 오랜 파트너이며 보증 보험 회사인 Real Garant VersicherungAG에 차량 보증 포트폴리오를 위탁하여 자동차 산업의 주요 사업인 유럽 전역의 이동성 서비스 처리에 전념하고 있습니다.

- 독일 무역투자청에 따르면 밸류체인을 따라 약 6,600개의 기업이 있으며 그 90% 가까이 중소기업이기 때문에 기계·설비는 독일에서 가장 활발한 섹터입니다. 독일의 기계 및 설비(M&E) 부문은 100만 명 이상의 근로자를 보유한 독일 최대 산업 고용주로 계속되고 있습니다. M&E 부문은 국내에서 가장 혁신적인 부문 중 하나이며 작년에는 총 약 170억 유로를 연구 개발에 소비했습니다. 공작기계, 구동기술, 자재관리 기기 부문은 기계공학부문 중에서도 연간 매출이 가장 큰 부문입니다. 장비 제조 업계에서는 이러한 많은 기업들이 구입한 조립 부품별로 보증서를 관리해야 합니다. 보증 관리 시스템은 보증, 클레임 및 수익성을 쉽게 모니터링하고 관리하는 고급 도구를 제공하므로 보증 관리 시스템을 도입하여 이러한 바쁜 작업을 줄일 수 있습니다.

- 독일에서는 인구 증가와 노화, 만성 질환 증가, 인프라 정비, 기술 진보가 이 분야의 확대에 기여하고 있습니다. 보증 관리 시스템은 심박 조율기 및 제세동기와 같은 임베디드 장비의 보증 프로세스를 효율적으로 관리합니다. 보증 기간 동안 장비의 반환을 간소화하고 리콜 시 필요한 서류를 작성합니다. 독일에서는 건강 관리가 공공 의료 및 민간 의료에 의해 제공됩니다. 정부는 헬스케어 산업에 많은 투자를 하고 있으며, 그 결과 양심실 페이스메이커, 이식형 제세동기, 이식형 심장 루프 기록장치, 페이스메이커 등의 혁신적인 수술기구를 이용할 수 있게 되었습니다.

유럽 보증 관리 시스템 산업 개요

- 유럽의 보증 관리 시스템 시장은 Oracle Corporation, IBM Corporation, Syncron AB, Servicemax Inc. 이러한 기업은 고객에게 맞춤형 솔루션을 제공하기 위해 광범위하게 투자하고 있습니다. 또한 시장의 신흥 기업은 투자자로부터 자금을 모으고 있습니다. 시장의 주요 기업은 시장에서의 지위를 유지하기 위해 제휴, 합병, 인수, 투자를 실시했습니다.

- 2022년 11월, 서비스 라이프사이클 관리의 세계 리더 중 하나인 디지털 제품 및 솔루션 기업인 Tavant Technologies Inc.는 상용 제조업체의 세계 리더 중 하나인 Daimler Truck AG(DTAG)와 제휴하여 DTAG의 유럽 브랜드에 대한 보증 및 클레임 관리 솔루션을 제공한다고 발표했으며, 이는 유럽의 자동차 제조업에서 보증 관리 시스템 도입을 보여주는 것입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 제조업과 자동차산업에서 보증관리시스템 채용 증가

- 고객 만족을 확보하기 위한 차세대 보증 관리 시스템에서 AI와 ML 기능의 채용 증가

- 시장 성장 억제요인

- 가격에 민감한 시장에서 독립 서비스 제공업체 간의 치열한 경쟁

제6장 시장 세분화

- 전개별

- 온프레미스

- 클라우드

- 최종 사용자 산업별

- 산업기기

- 자동차 및 운송

- 내구 소비재

- 기타 최종 사용자 산업(의료기기, 항공우주, 방위 등)

- 국가별

- 영국

- 독일

- 프랑스

- 기타 유럽

제7장 경쟁 구도

- 기업 프로파일

- Syncron AB

- IFS AB

- Tavant Technologies Inc.

- ServiceMax Inc.

- SKYLYZE

- Pegasystems Inc.

- PTC Inc.

- Oracle Corporation

- IBM Corporation

- Wipro Limited

제8장 투자 분석

제9장 시장 기회와 앞으로의 동향

JHS 25.05.09The Europe Warranty Management System Market size is estimated at USD 1.66 billion in 2025, and is expected to reach USD 3.07 billion by 2030, at a CAGR of 13.07% during the forecast period (2025-2030).

Key Highlights

- A crucial part of every service business is warranty management. The capacity to view, access, and automatically track client asset warranty coverage and data is critical. With warranty management, companies may be protected by loss of sales and customer displeasure.

- The warranty management system enables service businesses to design, administer, track, and process warranties, claims, and assets by automating warranty claim handling and installed base asset tracking. Innovative warranty management systems (WMS) are linked with AI and machine learning capabilities to guarantee customer satisfaction, driving the European market.

- The automobile sector's management of warranties is complex because the abundance of data, which spans the entire process from suppliers to dealers to final consumers, increases the probability of errors at different levels. Although each dealer and manufacturer has unique procedures for handling warranty claims and data, the traditional systems frequently do not produce reliable or consistent results, fuelling the adoption of warranty management systems in Europe, supported by the region's industrial development in automating.

- The warranty management system improves the accuracy and quality of warranty information by validating all privilege features using broad business rules and immediately incorporating information streams from diagnostic and mobile devices into warranty claim forms. The application handles the authorization of returns, tracking of returns, and creation of RGA/RMA or approvals for returns of material. By managing supplier warranties for parts and components, the warranty tracker enables suppliers and manufacturers to work together to cut warranty costs, fueling market adoption.

- However, due to the increasing competition and the increase in the Price sensitivity in the European warranty management system, providers are limiting the market growth because end users could compromise service features over price while choosing the warranty management system for their business due to the high price sensitivity in the market. Additionally, inaccurate diagnosis, excessive maintenance, fraud, and overcharging resulting from a lack of understanding of the warranty and repair procedure hamper the market growth rate during the forecast period.

- With the COVID-19 pandemic, the shift toward automated technologies has been significant across the region. Considerable advantages like enhanced productivity, data reliability, enhanced claim data validity, quality, etc., are luring customers into adopting automated warranty management systems with AI and ML, contributing to the market's growth rate.

Europe Warranty Management System Market Trends

Cloud Deployment Segment Holds Major Market Share

- The increasing realization among enterprises about the importance of saving money and resources by moving their data to the cloud instead of building and maintaining new data storage drives the demand for cloud-based solutions and, hence, the adoption of on-demand warranty management systems in the region. Moreover, owing to multiple benefits and over the next few years, cloud platforms and ecosystems are anticipated to serve as a launchpad for an explosion in the pace and scale of digital innovation.

- Furthermore, deploying public cloud services extends the boundary of trust beyond the organization, making security a vital part of the cloud infrastructure. However, the increasing usage of cloud-based solutions has significantly simplified enterprises' adoption of warranty management practices. With the increased adoption of cloud services, such as Google Drive, Dropbox, and Microsoft Azure, among others, and with these tools emerging as an integral part of business processes, enterprises must deal with security issues, such as losing control over sensitive data, raises the incorporation of on-demand warranty management solutions.

- One of the country's fastest-growing markets is the cloud, and rising investment in the sector is broadening the area of the industry under study. Large service providers increasingly manage the country's extensive public and hybrid cloud environments and hyper-scale services. For instance, in July 2022, Oracle announced it would introduce new sovereign cloud zones for the European Union in 2023 to serve its clients across the European Union better. Germany and Spain will host the first two EU sovereign cloud regions, which will be logically and physically distinct from the region's current public OCI regions. The new sovereign cloud regions will allow private businesses and government agencies to host sensitive, regulated, or strategically significant regional data and applications.

- Cloud-based solutions also benefit from lower capital expenditure requirements, making the business more compelling. Deploying cloud-based services can significantly reduce the Capex requirement as companies do not need to invest in hardware components. Cloud solutions also enable better prediction of the cost of an application, and companies don't need to incur as much upfront cost to incorporate the technology. Also, hardware and IT support savings make cloud-based solutions much more affordable.

- Furthermore, the growing adoption of cloud-based systems contributes to market growth. For instance, the European Union states that 41% of EU businesses adopted cloud computing last year. In the European Union, cloud computing usage grew, especially in retail. Cloud computing involves two components, which are cloud infrastructure and software applications. The growing demand for software applications in warranty management systems is expected to contribute to the market's growth during the forecast period.

Germany is Expected to Register the Fastest Growth

- Germany is one the fastest-growing countries in the region due to government regulations in different industries and the increasing development of software to satisfy customers' diverse needs. The demand for heavy equipment, automotive, and many more industries is increasing their production, driving the output of warranty management systems in the region so that the sectors may track the warranty periods and claims made on the products sold to customers.

- Recently, German lawmakers passed a new sales law that tightens warranty regulations in favor of customers. The two-year warranty period will be applicable for goods and services from the date of purchase or delivery. If a flaw is discovered near the conclusion of the warranty period, some modifications will be made to the conditions. The limitations are applicable only after the completion of four months after the purchase. This scenario gives the buyer extra time to make warranty claims if the issue materializes just before the expiration of the warranty period.

- The rise in partnerships between the automotive and warranty issuer firms is expected to drive the market studied. Such developments will push them to deploy new solutions in their product portfolio to streamline the workflow and track the claims. For instance, Europe Assistance Germany outsourced its portfolio of vehicle warranties to its long-time partner and warranty insurance Real Garant VersicherungAG to concentrate on its main business in the automotive industry, the processing of mobility services across Europe.

- According to German Trade and Invest, with almost 6,600 enterprises along the value chain, nearly 90% of which are SMEs, machinery and equipment are Germany's most active sector. The German Machinery and Equipment (M&E) sector continues to be the largest industrial employer in Germany, with a workforce of more than one million workers. The M&E sector is one of the most innovative in the nation, which spent about EUR 17 billion on research and development in total in the last year. The machine tools, drive technology, and material handling equipment sectors are some of the most significant in yearly turnover within the mechanical engineering sector. Such a high number of firms in the industry of equipment production have to maintain warranty documents for each assembled part they buy. Such hectic work can be reduced by deploying warranty management systems because they provide advanced tools to easily monitor and manage warranties, claims, and profitability.

- In Germany, population growth and aging, an increase in chronic disease prevalence, infrastructure improvements, and technological advancements have contributed to the sector's expansion. The warranty management systems efficiently manage the warranty processes for implanted devices like pacemakers and defibrillators. They streamline the return of the equipment under warranty and fill out the necessary paperwork in the event of a recall. In Germany, healthcare is made available through public and private healthcare. The government is making significant investments in the healthcare industry, which has led to the availability of innovative surgical tools such as biventricular pacemakers, implantable cardioverter defibrillators, implantable cardiac loop recorders, and pacemakers.

Europe Warranty Management System Industry Overview

- The European warranty management system market is highly fragmented due to various market players like Oracle Corporation, IBM Corporation, Syncron AB, Servicemax Inc., Tavant Technologies Inc., etc. These companies are extensively investing in offering customized solutions to customers. Moreover, the startups in the market are attracting funding from investors. The key players in the market are making partnerships, mergers, acquisitions, and investments to retain their market position.

- In November 2022, Tavant Technologies Inc., a digital products and solutions company, one of the global leaders in service lifecycle management, announced a partnership with Daimler Truck AG (DTAG), one of the global leaders in commercial manufacturers, to offer warranty and claim management solutions for the DTAG European brands, which shows the market adoption of warranty management systems in the European automotive manufacturing industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Adoption of Warranty Management Systems in the Manufacturing and Automotive Industries

- 5.1.2 Increasing Adoption of AI and ML Capabilities in Next-generation Warranty Management Systems to Ensure Customer Satisfaction

- 5.2 Market Restraints

- 5.2.1 Intense Competition Between Independent Service Providers in Price-sensitive Markets

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-Premise

- 6.1.2 Cloud

- 6.2 By End-user Industry

- 6.2.1 Industrial Equipment

- 6.2.2 Automotive and Transportation

- 6.2.3 Consumer Durable

- 6.2.4 Other End-user Industries (Medical Devices, Aerospace, Defense, Etc.)

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Syncron AB

- 7.1.2 IFS AB

- 7.1.3 Tavant Technologies Inc.

- 7.1.4 ServiceMax Inc.

- 7.1.5 SKYLYZE

- 7.1.6 Pegasystems Inc.

- 7.1.7 PTC Inc.

- 7.1.8 Oracle Corporation

- 7.1.9 IBM Corporation

- 7.1.10 Wipro Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

샘플 요청 목록