|

시장보고서

상품코드

1628816

첨단 탄소 소재 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Advanced Carbon Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

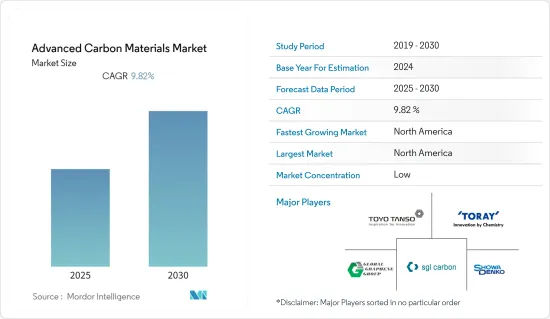

첨단 탄소 소재 시장은 예측 기간 동안 연평균 9.82%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예상됩니다.

코로나19 팬데믹은 시장에 부정적인 영향을 미쳤습니다. 봉쇄와 제한으로 인해 제조 시설과 공장이 폐쇄되었기 때문입니다. 공급망과 운송의 혼란은 시장에 더 많은 장애를 가져왔습니다. 그러나 2021년에는 산업이 회복되고 시장 수요가 회복되었습니다.

주요 하이라이트

- 단기적으로는 건설 산업에서 탄소섬유 강화 플라스틱에 대한 수요 증가, 자동차 및 항공 산업에서 경량 복합재에 대한 관심이 높아지면서 조사 대상 시장의 성장을 가속하는 요인 중 하나입니다.

- 반면, 탄소섬유 복합재료의 높은 비용과 완제품 생산의 낭비가 시장 성장을 저해할 가능성이 높습니다.

- 그러나 바이오 폐기물을 이용한 고급 숯 소재 생산은 예측 기간 동안 많은 기회를 제공할 것으로 예상됩니다.

- 북미가 가장 큰 소비량으로 시장을 장악하고 있으며, 아시아태평양이 근소한 차이로 그 뒤를 잇고 있습니다.

첨단 탄소 소재 시장 동향

시장을 장악하는 항공우주 및 방위산업

- 항공우주 및 방위 산업은 최종 사용자 산업을 기반으로 시장에서 가장 큰 시장 점유율 중 하나를 차지합니다. 지난 몇 년동안 이 부문에는 수많은 신제품이 추가되었습니다. 고급 석탄 소재는 필요에 따라 강도, 내구성 및 안정성을 제공하므로 수많은 항공우주 및 방위 응용 분야에 이상적인 선택입니다.

- 기존의 금속 구조는 가볍지만 강성이 높은 설계 구조로 인해 항공기에서는 탄소섬유강화플라스틱(CFRP)과 같은 탄소섬유로 대체되는 경우가 증가하고 있습니다. 항공기 및 제트기 내부부터 헬리콥터 로터 블레이드에 이르기까지 복합소재는 항공우주산업에 필수적인 부품으로 부상하고 있습니다.

- 아시아태평양에서는 많은 국가들이 국방 플랫폼과 기술에 대한 지출을 늘리면서 항공우주 산업이 빠르게 성장하고 있습니다.

- 인도 민간 및 군용 항공 산업은 최근 몇 년동안 인도에서 가장 빠르게 성장하는 산업 중 하나로 부상했습니다. 인도 정부에 따르면 민간 항공 부문은 2021년 인도 GDP에 300억 달러를 기여했습니다. 이러한 성장으로 인도 국내 항공 시장은 2024년까지 세계 3위를 차지할 것으로 예상됩니다. 항공 운송량은 세계 평균에 비해 빠르게 증가하고 있습니다. 항공기 수는 2024년 중 600대(2022년 10월 기준)에서 1,200대까지 증가할 수 있습니다. 따라서 항공 운항 횟수 증가는 선진 석탄 원료 시장에 대한 수요 증가를 가져올 것으로 예상됩니다.

- 또한, 2022년 4월 HAL과 이스라엘 항공우주산업(IAI)은 인도에서 민간(여객) 항공기를 다중 임무 유조선 수송(MMTT) 항공기로 전환하기 위한 양해각서를 체결하였습니다.

- 코로나19 이후 전자상거래 사업이 급증하면서 항공화물 시장이 확대되면서 2022년 화물기 주문이 증가하고 있습니다. 예를 들어, 룩셈부르크의 Cargolux Airlines는 2022년 10월 보잉에 777-8 화물기 10대와 추가 6대의 옵션을 주문했습니다.

- 중국은 미국에 이어 두 번째로 큰 항공화물 시장으로 보잉의 Commercial Market Outlook 2022에 따르면 중국의 민간 항공기는 2041년까지 3,900대에서 9,600대로 늘어날 것으로 예상됩니다.

- 보잉은 2022년 2월 미 국방부로부터 미화 1억 3,700만 달러 상당의 계약을 체결하고 대외군사판매(FMS) 방식으로 AH-6 경공격정찰헬기 8대를 태국에 납품했습니다. 이 헬리콥터는 태국 왕립 육군에서 사용 중인 노후화된 AH-1F 코브라 헬리콥터의 후속 기종으로 계획되어 있으며, 2024년까지 납품될 예정입니다.

- 또한 유나이티드 항공은 "대서양 횡단 노선의 최대 확장"이라고 표현하며 새로운 노선의 운항을 시작했다고 발표했습니다. 모든 것이 정상화되면서 새로운 항공사도 운항을 시작했으며, 2022년 8월 인도의 새로운 항공사 아카사 에어가 주 28회 운항하는 1개 노선을 시작으로 점차 2개 노선을 추가했으며, 2022년 10월 알래스카 항공은 보잉 737 MAX를 52대 주문했습니다. 이 항공사는 2023년 말까지 전 기종을 보잉사의 주력 기종으로 도입할 계획을 발표했습니다.

- 위의 모든 요인은 예측 기간 동안 고급 석탄 재료 시장의 성장을 가속할 것으로 예상됩니다.

북미가 시장을 독식합니다.

- 미국, 캐나다, 멕시코와 같은 국가의 존재로 인해 예측 기간 동안 북미가 시장을 지배할 것으로 예상됩니다.

- 미국은 세계 최대의 경제대국입니다. 탄소섬유, 탄소나노튜브, 그래핀, 특수흑연, 탄소발포체, 나노결정다이아몬드(NCD), 다이아몬드 유사 탄소(DLC), 풀러렌 등 다양한 첨단소재에 대한 수요가 항공우주 및 방위, 전자, 자동차, 에너지 등 다양한 최종사용자 산업에서 증가하고 있어 예측기간 동안 첨단탄 소재료 수요가 높은 비율로 촉진될 것으로 예상됩니다.

- 예를 들어, OICA에 따르면 2022년 미국의 자동차 생산량은 1,006만대로 2021년 대비 10%, 2020년 대비 14% 증가할 것으로 예상됩니다. 따라서 자동차 생산량 증가는 고급 석탄 재료비에 대한 수요 증가를 가져올 것으로 예상됩니다.

- 또한 NATO 국가들의 국방비에 따르면 2022년 미국은 국방비로 약 8,220억 달러를 지출했습니다. 이로 인해 미국의 국방 예산은 NATO 회원국 중 가장 큰 규모입니다. 따라서 미국의 국방비 증가는 북미의 고급 석탄 재료비에 대한 수요 증가를 가져올 것으로 예상됩니다.

- 위의 요인으로 인해 북미의 고급 석탄 재료 시장은 예측 기간 동안 크게 성장할 것으로 예상됩니다.

첨단 탄소 소재 산업 개요

첨단 탄소 소재 시장은 그 특성상 부분적으로 세분화되어 있습니다. 이 시장의 주요 기업(무순서)으로는 TORAY INDUSTRIES INC., Toyo Tanso, Global Graphene Group, SGL Carbon, SHOWA DENKO K.K. 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 산업 밸류체인 분석

- Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 정도

제5장 시장 세분화

- 제품 유형

- 탄소섬유

- 특수 흑연

- 탄소나노튜브

- 그래핀

- 카본 폼(카본 나노폼 포함)

- 기타(풀러렌, 다이아몬드 유사 카본(DLC), Nanocrystalline Diamond(NCD))

- 용도

- 항공우주 및 방위

- 일렉트로닉스

- 스포츠

- 자동차

- 건설

- 에너지

- 기타

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카공화국

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 인수합병(M&A)/합작투자(JV)/협업/협정

- 시장 점유율(%)**/순위 분석

- 주요 기업의 전략

- 기업 개요

- Arkema

- Arry International Group Limited

- CFOAM LLC

- FutureCarbon GmbH

- Formosa Plastics Corporation

- Global Graphene Group

- GrafTech International

- Graphenea, Inc.

- Graphite India Limited

- Antolin

- Grupo Graphenano

- Haydale Graphene Industries plc

- Hexcel Corporation

- Hyperion Catalysis International

- Jiangsu Cnano Technology Co., Ltd.

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- Ningbo Morsh Technology

- Nano-C

- Nanocyl SA

- Nippon Graphite Fiber Co., Ltd

- Perpetuus Advanced Materials PLC

- POCO

- SGL Carbon

- Shenzhen Sanshun Nano New Materials Co. Ltd

- SHOWA DENKO K.K.

- Solvay

- TEIJIN LIMITED

- The Sixth Element(Changzhou) Materials Technology Co.,Ltd

- Thomas Swan & Co. Ltd.

- Tokai Carbon Co., Ltd.

- TORAY INDUSTRIES, INC.

- Toyo Tanso Co.,Ltd.

- XG Sciences, Inc.

제7장 시장 기회와 향후 동향

- 바이오 폐기물로부터 첨단 숯재료료 생산

- 에너지 부문 잠재적 용도

The Advanced Carbon Materials Market is expected to register a CAGR of 9.82% during the forecast period.

The COVID-19 pandemic negatively impacted the market. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, increasing demand for carbon fiber-reinforced plastic in the construction industry and increasing focus on lightweight composites in the automotive and aviation industries are some of the factors driving the growth of the market studied.

- On the flip side, the high cost of carbon fiber composites and wastage in the production of finished products is likely to hinder the growth of the market studied.

- However, the production of advanced carbon materials from bio-waste is anticipated to provide numerous opportunities over the forecast period.

- North America dominated the market with the largest consumption, followed closely by Asia-Pacific.

Advanced Carbon Materials Market Trends

Aerospace and Defense to Dominate the Market

- Aerospace and defense accounts for one of the largest shares in the market, based on the end-user industry. Over the past few years, there have been a number of new products added to this field. Advanced carbon materials are perfect choices for numerous aerospace and defense applications, as they provide strength, endurance, and stability, as required.

- Conventional metal structures are increasingly being replaced by carbon fibers, such as carbon fiber-reinforced plastics (CFRP) in aircraft, owing to their light yet stiff design structures. From the interior of an airplane or a jet to the rotor blades of a helicopter, composite materials are emerging as integral parts of the aerospace industry.

- In Asia-Pacific, the aerospace industry is growing at a fast rate, as many countries have increased their spending on defense platforms and technologies.

- The civil and military aviation industry in India emerged as one of the fastest-growing industries in the country in the past few years. According to the Indian government, the commercial aviation sector contributed USD 30 billion to India's GDP in 2021. With this growth, the domestic aviation market is projected to rank third globally by 2024. As air traffic has been growing rapidly in the country as compared to the global average. The air fleet number may rise from 600 (as of October 2022) to 1,200 during 2024. Therefore, increasing in the number of air fleet is expected to created an upside demand for advanced carbon materials market.

- Moreover, in April 2022, to transform Civil (Passenger) aircraft into Multi-Mission Tanker Transport (MMTT) aircraft in India, HAL and Israel Aerospace Industries (IAI) have signed a Memorandum of Understanding.

- With the e-commerce operations increasing rapidly since COVID-19, the air cargo market has increased, and thus the orders for freighter aircraft have increased in 2022. For instance, in October 2022, Luxembourg's Cargolux airlines placed an order with Boeing for 10 777-8 freighters along with options for 6 additional aircraft.

- China holds the position of second largest air freight market only next to the United States. According to Boeing's Commercial Market Outlook 2022, China's commercial airfleet is expected to grow from 3,900 to 9,600 by 2041.

- In February 2022, Boeing was awarded a contract worth USD 103.7 million by the US Department of Defense to deliver eight AH-6 light attack reconnaissance helicopters to Thailand under foreign military sale (FMS). The helicopters are planned to replace the aging AH-1F Cobra helicopters in service of the Royal Thai Army, and deliveries are expected to run through 2024.

- Furthermore, United Airlines has announced that it has started operating on new routes, describing it as its "largest transatlantic expansion." With everything returning to normal, new airlines have started operations. Akasa Air, a new Indian airline, has started its operations in August 2022, starting with one route with 28 flights a week and gradually adding two more routes. In October 2022, Alaska Airlines placed an order for 52 Boeing 737 MAX aircraft with a plan to expand its fleet. The airline announced plans to have an all-Boeing mainline fleet by the end of 2023.

- All factors above are likely to fuel the growth of the advanced carbon materials market over the forecast period.

North America Region to Dominate the Market

- The North American region is expected to dominate the market during the forecast period due to the presence of countries like the United States, Canada, and Mexico.

- The United States is the world's largest and most powerful economy. With the growing demand for various advanced materials such as (carbon fibers, carbon nanotubes, graphene, special graphite, carbon foams, nanocrystalline diamond (NCD), diamond-like-carbon (DLC), and fullerenes) in different end-user industries, including aerospace and defense, electronics, automotive, and energy, among others, is expected to propel the demand for advanced carbon materials at high rates through the forecast period.

- For instance, according to OICA, in 2022, automobile production in the United States amounted to 10.06 million units, which showed an increase of 10% compared to 2021 and 14% compared to 2020. Therefore, increasing automobile production is expected to create an upside demand for advanced carbon materials.

- Moreover, according to the Defence Expenditure of NATO Countries, in 2022, the United States spent an estimated USD 822 billion on defence. This makes their defence budget, by far, the biggest out of all the NATO members. Therefore, increasing expenditure on defense from the United States is expected to create an upside demand for advanced carbon materials in North America region.

- Owing to the above-mentioned factors, the market for advanced carbon materials in North America region is projected to grow significantly during the forecast period.

Advanced Carbon Materials Industry Overview

The advanced carbon materials market is partially fragmented in nature. The major players in this market (not in a particular order) include TORAY INDUSTRIES INC., Toyo Tanso Co. Ltd, Global Graphene Group, SGL Carbon, and SHOWA DENKO K.K.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand for Carbon Fiber Reinforced Plastic in the Construction Industry

- 4.1.2 Technological Advancements in Carbon Nanotubes

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High-cost of Carbon Fiber Composites

- 4.2.2 Wastage in the Production of Finished Products

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Carbon Fibers

- 5.1.2 Special Graphite

- 5.1.3 Carbon Nanotubes

- 5.1.4 Graphene

- 5.1.5 Carbon Foams (Includes Carbon Nanofoams)

- 5.1.6 Others (Fullerenes, Diamond-like Carbon (DLC), Nanocrystalline Diamond (NCD))

- 5.2 Application

- 5.2.1 Aerospace and Defence

- 5.2.2 Electronics

- 5.2.3 Sports

- 5.2.4 Automotive

- 5.2.5 Construction

- 5.2.6 Energy

- 5.2.7 Others

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 Arry International Group Limited

- 6.4.3 CFOAM LLC

- 6.4.4 FutureCarbon GmbH

- 6.4.5 Formosa Plastics Corporation

- 6.4.6 Global Graphene Group

- 6.4.7 GrafTech International

- 6.4.8 Graphenea, Inc.

- 6.4.9 Graphite India Limited

- 6.4.10 Antolin

- 6.4.11 Grupo Graphenano

- 6.4.12 Haydale Graphene Industries plc

- 6.4.13 Hexcel Corporation

- 6.4.14 Hyperion Catalysis International

- 6.4.15 Jiangsu Cnano Technology Co., Ltd.

- 6.4.16 Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- 6.4.17 Ningbo Morsh Technology

- 6.4.18 Nano-C

- 6.4.19 Nanocyl SA

- 6.4.20 Nippon Graphite Fiber Co., Ltd

- 6.4.21 Perpetuus Advanced Materials PLC

- 6.4.22 POCO

- 6.4.23 SGL Carbon

- 6.4.24 Shenzhen Sanshun Nano New Materials Co. Ltd

- 6.4.25 SHOWA DENKO K.K.

- 6.4.26 Solvay

- 6.4.27 TEIJIN LIMITED

- 6.4.28 The Sixth Element (Changzhou) Materials Technology Co.,Ltd

- 6.4.29 Thomas Swan & Co. Ltd.

- 6.4.30 Tokai Carbon Co., Ltd.

- 6.4.31 TORAY INDUSTRIES, INC.

- 6.4.32 Toyo Tanso Co.,Ltd.

- 6.4.33 XG Sciences, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Production of Advanced Carbon Materials from Biowaste

- 7.2 Potential Uses in Energy Sector