|

시장보고서

상품코드

1636137

중국의 제3자 물류(3PL) 시장 - 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)China Third-Party Logistics (3PL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

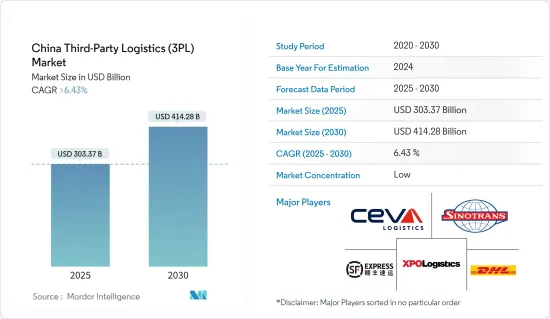

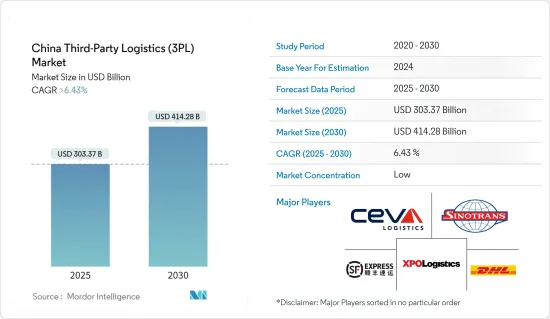

중국의 제3자 물류 시장 규모는 2025년에 3,033억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 6.43%를 넘고, 2030년에는 4,142억 8,000만 달러에 도달할 것으로 예측됩니다.

주요 하이라이트

- 중국의 제3자 물류 시장은 주로 전자상거래 활동 증가와 가처분 소득 증가에 의해 견인되고 있습니다.

- 중국의 전자상거래 시장은 국가의 경제 상황을 재구성하고 있습니다. 디지털 경제는 중국의 GDP를 밀어 올리는 데 점점 더 중요 해지고 있습니다. 2023년에는 온라인 결제가 중국 소비자 매출의 4분의 1 이상을 차지해, 세계 평균을 웃도고 있습니다. 또한, 노동 인구가 풍부한 E-Commerce는 중국의 주요한 고용 엔진으로서 두드러지고 있습니다.

- 2024년 상반기 중국의 전자상거래 부문은 현저한 성장을 이루며 세계 2위 경제대국인 중국의 소비회복세를 강화했습니다. 기간중 온라인 소매 판매액이 전년 대비 9.8% 상승해 7조 1,000억 위안(약 9,960억 달러)에 이르렀습니다.

- 중국의 전자상거래 선두주자인 Alibaba와 JD.com은 2024년 '더블 11' 쇼핑 페스티벌 기간 중 매출이 호조를 보였다고 보고해, 중국 소비시장이 꾸준히 회복되고 있음을 강조 했습니다.

- Alibaba Group의 플랫폼인 Taobao와 Tmall은 '더블 11' 행사 기간 동안 현저한 매출 급증을 발표했습니다. 총 589개 브랜드가 1억 위안 매출을 넘어 2023년부터 46.5% 증가했습니다. 이 회사는 소비자의 참여가 2024년 전례 없는 봉우리에 도달했다고 강조했습니다.

- 베이징에 본사를 둔 JD.com은 실시간 스트리밍 매출이 급증하고 2023년부터 3.8배 성장을 기록했다고 밝혔습니다. 1만 7,000개 이상의 브랜드가 5배가 넘는 매출 성장을 기록했습니다. Taobao와 Tmall의 성장은 다양한 부문에 이르렀으며 특히 소비자 전자 및 장식품에서 두드러졌습니다. 이 기세로 139개가 넘는 브랜드가 매출액 1억위안의 고비를 돌파했고, 9,600개 브랜드가 2023년부터 매출이 두배로 늘어났습니다. 그러므로 전자상거래 매출이 급증함에 따라 국내 3PL 물류 수요도 연동되어 증가하고 있습니다.

중국 제3자물류(3PL) 시장 동향

부가가치가 높은 창고업과 유통업이 크게 성장

- 중국이 인더스트리 4.0 시대를 맞이하는 동안, 제조업은 여전히 물류 성장의 중요한 기폭제가되고 있습니다. 하이테크 제조업체의 급증으로 A 등급 창고 수요가 현저하게 증가하고 있습니다.

- 이 경향을 부각하고 있는 것은 태양전지의 생산이 54.2%라는 현저한 성장률을 나타내고 있는 것, 신에너지 자동차(NEV)가 30.4%도 급증하고 있는 것입니다. China Passenger Car Association (CPCA)에 따르면 중국에서의 NEV의 보급률은 2023년에 36.2%에 달하고, 많은 브랜드가 생산 거점의 설립이나 확대에 나서고 있습니다.

- 리스의 동향은 지역에 따라 다릅니다. 중국 남부의 경공업 기업은 창고 업무의 유연성을 중시하고 있습니다. 탄생하고 있습니다. 한편, 중국 서부에서는 NEV의 급성장이 창고 임대의 안정된 수요를 뒷받침하고 있습니다.

- 2023년에는 31개 주요 도시에서 비보세 A 등급 창고의 스톡이 9,000만 제곱미터를 넘었습니다. 지난 몇 년동안 일관되게 공급이 증가하고 있기 때문에 일부 개발자는 공실률의 상승을 완화하기 위해 임대료의 트레이드 오프에 의지했습니다.

- 중국 북부, 특히 복도, 천진, 베이징 등의 도시에서는 2021년부터 신규 공급이 급증했습니다.

- 중국 남부는 특히 광저우와 동관에서 크로스 보더 E-Commerce에 의한 왕성한 수요에 힘입어 공급의 정점에 이르렀으며, 중국 중부는 운송과 소비를 위해 안정된 수요를 유지하면서도 과거 3년간 공급 유입에 의한 공실 압력에 고민되고 있습니다. 이것은 산업 전체로 창고 스페이스에 대한 수요가 현저하다는 것을 뒷받침하고 있습니다.

전자상거래의 급증이 시장을 견인

- 중국의 전자상거래 시장은 중국 경제를 위한 혁신의 시대를 맞이했습니다. 국가 소비재의 4분의 1 이상이 온라인으로 구매되어 세계 평균을 상당히 웃돌고 있습니다.

- 지난 10년간 중국은 전자상거래의 견인역이 되어, 매출액으로 미국을 4,860억 달러 이상 벌려 놓고 있습니다.현재, 중국은 세계 최대의 디지털 바이어 인구를 자랑하고 있습니다. 기능이 중국의 전자상거래 영역에 통합되어 고객 경험이 더욱 풍부해지고 있습니다.

- 급속한 디지털화가 삶의 모든 면에 침투하는 가운데, 온라인으로 이행하는 중국 기업의 수도 늘어나고 있습니다. 그러나 온라인 소매 부문이 번영하는 반면 B2B E-Commerce의 성장은 최근 감속하고 있습니다. 크로스 보더 거래는 중국의 B2B의 중요한 부문으로서 부상하고, 주로 수출에 기울고 있습니다

- 세계 최대급 e리테일러의 본거지인 중국에서는 E-Commerce 매출이 일관되게 늘어나고 있습니다. 스마트폰이나 태블릿 단말기를 이용한 쇼핑이 일반적으로 되어 있습니다. 온라인 푸드 딜리버리, 커뮤니티 그룹 구매 등 온라인 투 오프라인 벤처의 상승을 가속화했습니다. 증강현실(AR)과 가상현실(VR) 기술의 채용은 쇼핑 체험을 풍부하게하고 고객 만족도 향상과 매출 증가로 이어지고 있습니다.

중국 제3자물류(3PL) 산업 개요

중국의 제3자 물류(3PL) 시장은 많은 지역, 지역 및 세계 진출 기업에 의해 고도로 세분화되어 있습니다.

기업은 거대한 잠재력을 활용하기 위해 경쟁력을 높이고 있습니다. 그 결과 국제 기업은 새로운 물류 센터와 스마트 창고와 같은 지역 물류 네트워크를 구축하기위한 전략적 투자를 수행하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

- 분석 방법

- 조사 단계

제3장 주요 요약

제4장 시장 역학과 인사이트

- 시장 개요

- 시장 역학

- 시장 성장 촉진요인

- 의류와 액세서리의 온라인 판매에 대한 왕성한 수요

- FMCG 제품 수요가 시장을 견인

- 시장 성장 억제요인/과제

- 시장에 영향을 미치는 규제상의 과제

- 노동력 부족과 비용 상승이 시장에 영향

- 시장 기회

- 시장을 견인하는 기술의 진보

- 시장 성장 촉진요인

- 밸류체인/서플라이체인 분석

- 산업의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 정부의 규제와 시책

- 창고 시장의 일반적인 동향

- CEP, Last One Miles Delivery, 콜드체인 물류 등 다른 부문 수요

- 전자상거래 사업에 대한 통찰

- 물류 부문의 기술 개발

- 지정학과 팬데믹이 시장에 미치는 영향

제5장 시장 세분화

- 서비스별

- 국내 수송 관리

- 국제운송관리

- 부가가치형 창고 및 배송

- 최종 사용자별

- 항공우주

- 자동차

- 소비재 및 소매, 에너지

- 의료

- 제조업

- 기술

- 기타

제6장 경쟁 구도

- 시장 집중 개요

- 기업 프로파일

- Ceva Logistics

- Sinotrans

- DHL Supply Chain

- XPO Logistics

- SF Express

- XPO Logistics

- YTO Express

- ZTO Express

- JD Logistics

- Kerry Logistics*

- 기타 기업

제7장 시장의 미래

제8장 부록

- 거시 경제 지표(GDP 분포, 활동별, 운수·창고 부문의 경제에의 기여도)

- 대외무역 통계-수출과 수입(제품별)

- 주요 수출처와 수입원산국에 대한 통찰

The China Third-Party Logistics Market size is estimated at USD 303.37 billion in 2025, and is expected to reach USD 414.28 billion by 2030, at a CAGR of greater than 6.43% during the forecast period (2025-2030).

Key Highlights

- The Chinese third-party logistics market is mainly driven by the rise in e-commerce activities and rising disposable income.

- China's e-commerce market is reshaping the nation's economic landscape. The digital economy is becoming ever more crucial in propelling China's GDP. In 2023, online purchases accounted for more than a quarter of China's consumer goods sales, outpacing the global average. Additionally, with its extensive workforce, e-commerce stands out as a major employment engine in the country.

- In the first half of 2024, China's e-commerce sector experienced significant growth, bolstering the momentum for consumption recovery in the world's second-largest economy. During this period, online retail sales jumped 9.8 percent year-on-year, totaling 7.1 trillion yuan (approximately USD 996 billion). Of this, retail sales of goods accounted for CNY 5.96 trillion, reflecting an 8.8 percent increase, as per data released by the Ministry of Commerce (MOC).

- Chinese e-commerce giants Alibaba and JD.com reported robust sales during the 2024 "Double 11" shopping festival, underscoring the steady recovery of China's consumer market.

- Alibaba Group's platforms, Taobao and Tmall, announced a notable surge in sales during the 'Double 11' event. A total of 589 brands surpassed the CNY 100 million sales mark, marking a 46.5 percent uptick from 2023. The company highlighted that consumer engagement reached an unprecedented peak in 2024.

- Beijing-based JD.com revealed that its live-streaming sales had skyrocketed, boasting a 3.8-fold increase from 2023. Over 17,000 brands celebrated sales growth exceeding five times. Taobao and Tmall's growth spanned various sectors, notably in home appliances and decoration. This momentum propelled over 139 brands past the 100-million-yuan sales milestone, with 9,600 brands experiencing a sales doubling from 2023. Hence, as e-commerce sales surge rapidly, the demand for 3PL logistics in the country is rising in tandem.

China Third-Party Logistics (3PL) Market Trends

Value-added warehousing and distribution experiencing substantial growth

- As China embraces the Industry 4.0 era, its manufacturing sector remains a key catalyst for logistics growth. The surge of high-tech manufacturers is driving a notable uptick in demand for Grade A warehouses.

- Highlighting this trend, solar cell production has seen a remarkable growth rate of 54.2%, while New Energy Vehicles (NEVs) have surged by 30.4%. According to the China Passenger Car Association (CPCA), NEV penetration in China hit 36.2% in 2023, leading many brands to either set up or expand their manufacturing bases.

- Leasing trends differ across regions: Southern China's light manufacturing firms are emphasizing flexibility in their warehouse operations. In Eastern China, a leader in the nation's shift towards a low-carbon economy, a flurry of eco-friendly warehouses boasting LEED certifications are springing up. On the other hand, Western China's rapid NEV growth is bolstering a steady demand for warehouse leases.

- In 2023, the stock of non-bonded Grade A warehouses in 31 major cities exceeded 90 million sqm. Eastern China emerged as a dominant player, representing over a third of the nation's total stock. As supply consistently flowed in recent years, some developers resorted to rental trade-offs to mitigate rising vacancy rates.

- Northern China, especially in cities like Langfang, Tianjin, and Beijing, saw a surge in new supply beginning in 2021. Conversely, Western China has been gradually slowing down since 2020, allowing it to absorb its vacant stock.

- Southern China reached a supply zenith, particularly in Guangzhou and Dongguan, spurred by strong demand from cross-border e-commerce. Meanwhile, Central China maintained steady demand for transportation and consumption, yet still grappled with vacancy pressures due to the influx of supply over the last three years. This underscores a pronounced demand for warehousing spaces across the industry.

Surge in e-commerce activities driving the market

- China's e-commerce market has ushered in a transformative era for the nation's economy. Today, the digital economy plays an increasingly pivotal role in bolstering China's GDP. In 2023, over a quarter of China's consumer goods were purchased online, significantly surpassing the global average. Moreover, e-commerce is a key driver of employment in the country, thanks to its vast workforce.

- For the past decade, China has led the e-commerce charge, outstripping the U.S. by over USD 486 billion in revenue. Currently, China boasts the world's largest population of digital buyers. Recent years have seen the integration of features like live streaming and swift delivery into China's e-commerce realm, further enriching the customer experience.

- With the rapid digitalization permeating every facet of life, a growing number of Chinese businesses are transitioning online. Bolstered by its vast manufacturing sector and governmental backing, China proudly hosts the globe's largest B2B e-commerce market. Yet, while the online retail sector flourishes, B2B e-commerce growth has recently decelerated. Cross-border transactions have emerged as a vital segment of China's B2B landscape, predominantly leaning towards exports, with the U.S. standing out as the primary destination for Chinese B2B goods.

- China, home to some of the world's largest e-retailers, has seen consistent growth in e-commerce sales. Rapid internet adoption has propelled online shopping penetration to over 80%. With the surge in mobile device usage, shopping via smartphones and tablets has become commonplace. The pandemic-induced social restrictions and lockdowns accelerated the rise of online-to-offline ventures, including quick commerce, online food delivery, and community group-buying. AI advancements are reshaping e-retail, optimizing operations and customer interactions. Furthermore, the adoption of augmented reality (AR) and virtual reality (VR) technologies is enriching shopping experiences, leading to heightened customer satisfaction and boosted sales.

China Third-Party Logistics (3PL) Industry Overview

The China third-party logistics (3PL) market is highly fragmented with a lot of local, regional, and global players. Some of the major players include Ceva Logistics, Sinotrans, DHL Supply Chain, XPO Logistics, SF Expres etc.

Companies are getting more competitive to capitalize on the enormous possibility. As a result, international firms are making strategic investments to build a regional logistics network, such as new distribution centers, smart warehouses, and so on.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS & DYNAMICS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Robust demand for online clothing and accessories

- 4.2.1.2 Demand for FMCG products driving the market

- 4.2.2 Market Restraints/challenges

- 4.2.2.1 Regulatory challenges affecting the market

- 4.2.2.2 Labour shortages and rising costs affecting the market

- 4.2.3 Market Opportunities

- 4.2.3.1 Technological advancements driving the market

- 4.2.1 Market Drivers

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Government Policies and Regulations

- 4.6 General Trends in Warehousing Market

- 4.7 Demand From Other Segments, such as CEP, Last Mile Delivery, Cold Chain Logistics Etc.

- 4.8 Insights on Ecommerce Business

- 4.9 Technological Developments in the Logistics Sector

- 4.10 Impact of Geopolitics and Pandemics on the Market

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Domestic Transportation Management

- 5.1.2 International Transportation Management

- 5.1.3 Value-added Warehousing and Distribution

- 5.2 By End User

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Consumer and Retail, Energy

- 5.2.4 Healthcare

- 5.2.5 Manufacturing

- 5.2.6 Technology

- 5.2.7 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Ceva Logistics

- 6.2.2 Sinotrans

- 6.2.3 DHL Supply Chain

- 6.2.4 XPO Logistics

- 6.2.5 SF Express

- 6.2.6 XPO Logistics

- 6.2.7 YTO Express

- 6.2.8 ZTO Express

- 6.2.9 JD Logistics

- 6.2.10 Kerry Logistics*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity, Contribution of Transport and Storage Sector to economy)

- 8.2 External Trade Statistics - Exports and Imports, by Product

- 8.3 Insights into Key Export Destinations and Import Origin Countries