|

시장보고서

상품코드

1636217

모터 스타터 시장 전망 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Motor Starter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

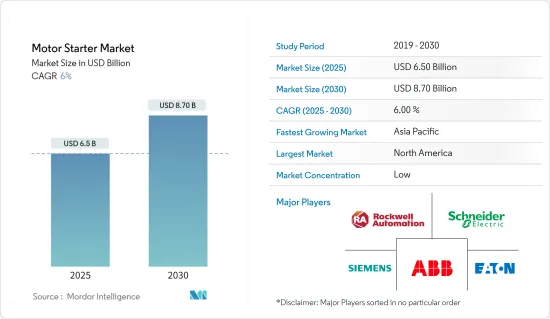

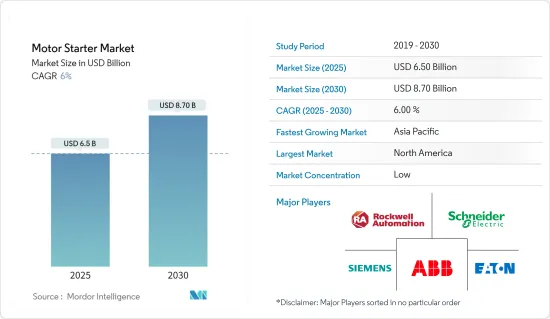

모터 스타터 시장 규모는 2025년에 65억 달러로 추계되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 6%로, 2030년에는 87억 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 환경에 대한 우려가 커지면서 업계에서는 에너지 소비를 줄이고 모터 수명을 연장하기 위해 소프트 스타터와 같은 에너지 효율적인 모터 스타터를 점점 더 많이 채택하고 있습니다. 동시에 사물 인터넷(IoT)의 부상으로 원격 모니터링 및 제어가 가능한 지능형 모터 스타터 개발이 촉진되어 시장이 진화하고 있습니다.

- 전 세계적으로 전기 자동차(EV)로의 전환이 가속화되면서 자동차 용도의 모터 스타터를 비롯한 정교한 모터 제어 솔루션에 대한 수요가 증가했습니다. 전기차에서 모터 스타터는 배터리 관리 시스템과 협력하여 성능을 최적화하고 안전을 보장합니다. 전 세계적으로 내연기관에서 전기차로 전환하는 국가가 증가함에 따라 모터 스타터에 대한 수요도 급증할 것으로 예상됩니다.

- 최근 모터 스타터 시장의 혁신으로 과부하 보호, 열 모니터링, 프로그래밍 가능한 설정과 같은 고급 기능을 갖춘 제품이 출시되어 신뢰성과 성능이 향상되었습니다. 제조업체들은 다양한 전압 레벨, 전력 등급 및 산업별 요구 사항에 맞는 모터 스타터를 포함하도록 제품 라인을 확장하고 있습니다.

- 모터 스타터 시장은 경쟁이 치열하고 많은 제조업체들이 시장 점유율을 다투고 있습니다. 이 치열한 경쟁은 종종 가격 압력과 제품 차별화의 과제로 이어집니다.

- 거시 경제 동향, 특히 신흥 시장의 견고한 경제 성장은 제조 및 건설 부문에서 모터 스타터에 대한 수요를 촉진합니다. 또한 에너지 효율과 환경 지속 가능성에 대한 규제가 강화되면서 시장 역학 관계에 영향을 미치고 있습니다. 그럼에도 불구하고 시장은 지속적으로 성장할 것으로 전망됩니다.

모터 스타터 시장 동향

제조업이 시장 성장을 주도할 것으로 예측

- Industry 4.0(4차 산업혁명)으로의 전환은 제조업에서 자동화 기술의 광범위한 채택을 촉진했습니다. 공장에서 첨단 로봇과 자동화 시스템을 도입하면서 효율적인 모터 제어가 필요해졌습니다. 이러한 발전은 다양한 부하를 관리하고 전반적인 성능을 향상시킬 수 있는 정교한 모터 스타터에 대한 수요를 촉진하고 있습니다.

- IoT와 스마트 기술이 제조업에 도입되면서 시설 운영이 혁신적으로 변화하고 있습니다. 실시간 모니터링, 진단 및 원격 제어 기능을 갖춘 스마트 모터 스타터가 각광받고 있습니다. 이러한 발전은 운영 효율성과 예측 유지보수를 강화하여 시장을 촉진하고 있습니다.

- 제조업체들은 각기 다른 용도와 작동 조건에 맞게 특별히 설계된 맞춤형 모터 스타터를 점점 더 많이 찾고 있습니다. 이러한 수요로 인해 모터 스타터 생산업체와 최종 사용자 간의 협업 이니셔티브가 촉진되어 고유한 성능 표준에 부합하는 솔루션을 개발하는 것이 목표입니다.

- 제조업체들이 시설을 현대화하면서 모터 스타터를 포함한 자동화 장비에 대한 자본 지출이 눈에 띄게 증가했습니다. FRED의 데이터에 따르면 미국의 신규 제조 시설에 대한 총 건설 투자는 2023년에 1,930억 달러로 2022년의 1,243억 달러에서 크게 증가하여 사상 최대치를 기록할 것으로 예상됩니다.

- 인플레이션 감소법(IRA), 초당적 인프라법(BIL), 칩스 및 과학법(CHIPS 법) 등의 입법 조치는 미국 내 반도체, 전기자동차(EV) 배터리, 풍력 터빈 등 국내 제조 부문에 대한 투자를 촉진하고 있습니다. 이러한 투자는 미국에만 국한된 것이 아니며, 신흥 경제국에서도 급속한 산업화를 목격하면서 모터 스타터에 대한 수요가 급증하고 있습니다.

높은 성장률이 기대되는 아시아태평양

- 중국과 인도와 같은 국가에서는 급속한 산업화와 도시 확장을 목격하고 있으며, 이로 인해 여러 부문에서 모터 스타터에 대한 수요가 증가하고 있습니다. 이러한 산업이 도시 수요를 충족하기 위해 운영을 확장함에 따라 효율적인 모터 제어 시스템의 중요성이 점점 더 분명해지고 있습니다.

- 아시아 태평양 지역은 특히 전자, 자동차, 기계 분야의 글로벌 제조 거점입니다. 인도, 중국, 일본, 동남아시아 여러 국가를 중심으로 한 이 지역의 성장은 제조 공정 중 전기 모터 제어에 필수적인 모터 스타터에 대한 수요를 촉진하고 있습니다.

- 인도의 제조업 부문은 투자의 대폭적인 급증을 목표로 하고 있으며, 이 나라의 경제 발전에 있어 매우 중요한 국면을 맞이하고 있습니다. Colliers의 보고서에 따르면 인도 제조 시장은 2025-26년까지 1조 달러 규모를 달성할 것으로 예상됩니다. 구자라트가 선두주자로 부상하면서 인도의 제조업 강국으로 자리매김하고 있으며, 마하라슈트라와 타밀 나두가 그 뒤를 바짝 쫓고 있어 이 시장에 상당한 기여를 할 것으로 예상됩니다.

- 특히 중국과 일본에서 자동차 산업이 호황을 누리고 있으며 인도가 큰 발전을 이루면서 전기 자동차의 모터 스타터에 대한 수요를 촉진하고 있습니다. 또한 도시화와 인구 증가로 수처리 시설에 대한 수요가 증가하면서 펌프 및 제어 시스템에서 신뢰할 수 있는 모터 스타터에 대한 수요가 증가하고 있습니다.

- 중국 국가발전개혁위원회에 따르면 2025년까지 중국의 슬러지 양은 9천만 톤에 달할 것으로 예상됩니다. 전문가들은 2021년부터 2025년까지 중국의 신규 슬러지 처리 시설에 약 80억 달러가 투자될 것으로 예상하고 있습니다. 증가하는 오염 수준을 고려할 때 인도도 그 뒤를 따를 것으로 예상됩니다. 이러한 추세에 따라 이 지역의 모터 스타터 시장은 크게 성장할 것으로 예상됩니다.

모터 스타터 산업 개요

이 시장은 다국적 대기업과 지역 기업이 혼합되어 치열한 경쟁을 벌이고 있습니다. 이러한 환경은 빠른 기술 발전, 전략적 협업, 제품 맞춤화, 에너지 효율성 향상, 스마트 기술 통합을 통해 돋보여야 하는 기업의 절실한 요구로 특징지어집니다.

이 분야에서 유명한 기업으로는 Schneider Electric, Siemens AG, ABB, Eaton 등이 있습니다. 이 회사들은 모터 스타터 기술의 개척과 개선에 중점을 두고 R&D에 투자하고 있습니다. 과부하 보호, 열 모니터링, 스마트 연결, 실시간 진단 등의 기능은 이 경쟁 시장에서 매우 중요한 차별화 요인으로 부상하고 있습니다.

Industry 4.0이 기세를 늘리고 있는 동안 IoT 기능, 실시간 모니터링, 예측 유지보수를 자사 제품에 원활하게 통합하는 기업은 자동화 및 디지털 솔루션을 열망하는 고객을 유치할 준비가 되어 있습니다. 또한, 기업은 특정 산업의 고유한 요구 사항을 해결하는 맞춤형 모터 스타터를 제공함으로써 고객과 더 깊은 관계를 구축할 수 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- COVID-19 팬데믹 후유증 및 기타 거시경제 요인이 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 산업 자동화의 성장

- 에너지 효율 규제

- 시장 성장 억제요인

- 가변 주파수 드라이브(VFD)와의 경쟁

제6장 시장 세분화

- 유형별

- 직접 온라인 스타터

- 스테이터 저항 스타터

- 슬립 링 스타터

- 오토 트랜스포머 스타터

- 스타 델타 스타터

- 소프트 스타터

- 정격전력별

- 5kW 미만

- 5-50 kW

- 50 kW 이상

- 업계별

- 제조업

- 석유 및 가스

- 광업

- 상하수도치료

- 자동차

- 음식

- 건축 및 건설

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Schneider Electric SE

- Seimens AG

- ABB Group

- Eaton Corporation

- Rockwell Automation

- Mitsubishi Electric Corporation

- Fuji Electric FA Components & Systems Co. Ltd

- Toshiba Corporation

- Larsen & Toubro Limited

- WEG SA

- WW Grainger Inc.

- Danfoss

제8장 투자 분석

제9장 시장의 미래

HBR 25.02.10The Motor Starter Market size is estimated at USD 6.50 billion in 2025, and is expected to reach USD 8.70 billion by 2030, at a CAGR of 6% during the forecast period (2025-2030).

Key Highlights

- In response to growing environmental concerns, industries are increasingly adopting energy-efficient motor starters, like soft starters, to reduce energy consumption and extend motor lifespan. Concurrently, the rise of the Internet of Things (IoT) has spurred the creation of intelligent motor starters, enabling remote monitoring and control, thus evolving the market.

- The global shift toward electric vehicles (EVs) has heightened the demand for sophisticated motor control solutions, including motor starters in automotive applications. In EVs, motor starters collaborate with battery management systems to optimize performance and ensure safety. As countries pivot from internal combustion engines to EVs across the world, the demand for motor starters is projected to surge.

- Recent innovations in the motor starter market have introduced products with advanced features like overload protection, thermal monitoring, and programmable settings, boosting reliability and performance. Manufacturers are broadening their product lines to encompass motor starters tailored to various voltage levels, power ratings, and industry-specific needs.

- The motor starter market is fiercely competitive, with many manufacturers competing for a market share. This intense competition often results in pricing pressures and challenges in product differentiation.

- Macroeconomic trends, particularly robust economic growth in emerging markets, fuel the demand for motor starters in the manufacturing and construction sectors. Additionally, tightening regulations on energy efficiency and environmental sustainability are influencing market dynamics. Nevertheless, the market is poised for continued growth.

Motor Starter Market Trends

The Manufacturing Sector is Expected to Drive the Market's Growth

- The transition to Industry 4.0 has spurred the widespread adoption of automation technologies in manufacturing. Factories are deploying advanced robotics and automated systems, necessitating efficient motor control. This evolution fuels the demand for sophisticated motor starters capable of managing diverse loads and enhancing overall performance.

- The infusion of IoT and smart technologies into manufacturing is revolutionizing facility operations. Smart motor starters, equipped with real-time monitoring, diagnostics, and remote control features, are gaining traction. These advancements bolster operational efficiency and predictive maintenance, propelling the market.

- Manufacturers are increasingly seeking customized motor starters specifically designed for distinct applications and operating conditions. This demand has fostered collaborative initiatives between motor starter producers and end users, aiming to craft solutions that align with unique performance standards.

- With manufacturers modernizing their facilities, there has been a notable uptick in capital expenditure on automation equipment, including motor starters. Data from FRED highlights this trend: total construction investment in new manufacturing facilities in the United States soared to a record USD 193 billion in 2023, a significant leap from USD 124.3 billion in 2022.

- Legislative measures like the Inflation Reduction Act (IRA), Bipartisan Infrastructure Law (BIL), and CHIPS and Science Act (CHIPS Act) are catalyzing investments in domestic manufacturing sectors, notably semiconductors, electric vehicle (EV) batteries, and wind turbines in the United States. This investment momentum is not confined to the United States, with emerging economies witnessing rapid industrialization, contributing to the surging demand for motor starters.

Asia-Pacific is Expected to Witness a High Growth Rate

- Countries like China and India are witnessing rapid industrialization and urban expansion, leading to a heightened demand for motor starters across multiple sectors. As these industries scale operations to cater to urban needs, the importance of efficient motor control systems becomes increasingly evident.

- Asia-Pacific is a global manufacturing hub, especially in the electronics, automotive, and machinery sectors. With key players like India, China, Japan, and several Southeast Asian nations, the region's growth propels the demand for motor starters, which are vital for controlling electric motors during manufacturing processes.

- The Indian manufacturing sector is witnessing a significant surge in investments, marking a pivotal moment in the country's economic journey. A report by Colliers highlights that the Indian manufacturing market is on track to hit the USD 1 trillion mark by 2025-26. Gujarat is emerging as the frontrunner, establishing itself as India's manufacturing powerhouse, closely trailed by Maharashtra and Tamil Nadu, which are expected to make substantial contributions to the market.

- The automotive industry, particularly booming in China and Japan, with India making significant strides, is fueling the demand for motor starters in electric vehicles. Furthermore, as urbanization and population grow, there is a rising need for water treatment facilities, underscoring the demand for dependable motor starters in pumps and control systems.

- According to the PRC's National Development and Reform Commission, China's sludge volume could hit 90 million tons by 2025. Experts project an investment of around USD 8 billion in new sludge processing facilities in China from 2021 to 2025. Given the escalating pollution levels, India is anticipated to follow suit. With such trends, the motor starter market in the region is poised for significant growth.

Motor Starter Industry Overview

The market is fiercely competitive, featuring a blend of large multinational corporations and regional players. This landscape is marked by rapid technological advancements, strategic collaborations, and a pressing need for companies to stand out through product customization, enhanced energy efficiency, and the integration of smart technologies.

Prominent players in the arena include Schneider Electric, Siemens AG, ABB Ltd, and Eaton Corporation. These companies are channeling investments into R&D, focusing on pioneering and refining motor starter technologies. Features like overload protection, thermal monitoring, smart connectivity, and real-time diagnostics have emerged as pivotal differentiators in this competitive market.

As Industry 4.0 gains momentum, companies that seamlessly weave in IoT capabilities, real-time monitoring, and predictive maintenance into their offerings are poised to attract a clientele eager for automated and digital solutions. Furthermore, companies can foster deeper relationships with their clients by providing tailored motor starters that address the distinct requirements of specific industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of the Aftereffects of the COVID-19 Pandemic and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Industrial Automation

- 5.1.2 Energy Efficiency Regulation

- 5.2 Market Restraints

- 5.2.1 Competition From Variable Frequency Drives (VFDs)

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Direct-on-Line Starter

- 6.1.2 Stator Resistance Starter

- 6.1.3 Slip Ring Starter

- 6.1.4 Auto Transformer Starter

- 6.1.5 Star Delta Starter

- 6.1.6 Soft Starter

- 6.2 By Power Rating

- 6.2.1 Up to 5 kW

- 6.2.2 5 - 50 kW

- 6.2.3 Above 50 kW

- 6.3 By End-user Vertical

- 6.3.1 Manufacturing

- 6.3.2 Oil and Gas

- 6.3.3 Mining

- 6.3.4 Water and Wastewater Treatment

- 6.3.5 Automotive

- 6.3.6 Food and Beverage

- 6.3.7 Building and Construction

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Seimens AG

- 7.1.3 ABB Group

- 7.1.4 Eaton Corporation

- 7.1.5 Rockwell Automation

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Fuji Electric FA Components & Systems Co. Ltd

- 7.1.8 Toshiba Corporation

- 7.1.9 Larsen & Toubro Limited

- 7.1.10 WEG SA

- 7.1.11 W.W. Grainger Inc.

- 7.1.12 Danfoss