|

시장보고서

상품코드

1636443

인도의 전기자동차 전지 분리막 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)India Electric Vehicle Battery Separator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

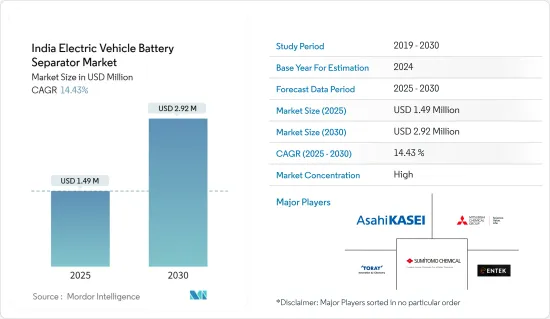

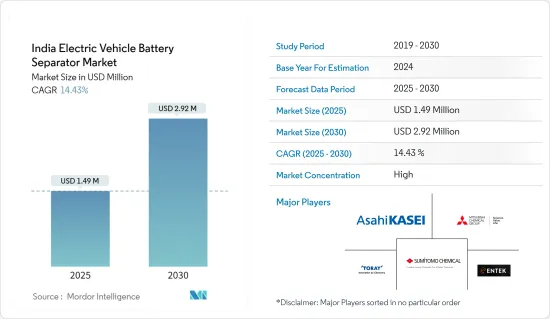

인도의 전기자동차 전지 분리막 시장 규모는 2025년에 149만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 14.43%로, 2030년에는 292만 달러에 이를 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 전기자동차 수요 증가나 정부의 지원책 등의 요인이 예측 기간 중 시장을 견인할 것으로 예상됩니다.

- 한편 자국기업 진입이 한정적이며, 이는 예측 기간 중 시장 성장을 방해할 것으로 보입니다.

- 기술 혁신과 지속가능한 재료 개발은 앞으로 수년간 시장에 큰 기회를 가져올 것으로 예상됩니다.

인도 전기자동차 전지 분리막 시장 동향

전기차 수요 증가

- 인도는 세계의 CO2 배출량 상위 5개국에 위치하고 있습니다. 대기오염이라는 시급한 과제에 대응하기 위해 인도 정부는 전기자동차(EV) 보급을 촉진하는 시책을 적극적으로 추진하고 있습니다. 인도전기자동차제조자협회(SMEV)는 인도가 2023년 167만대의 EV 판매를 달성할 것이라고 보고했습니다.

- 충전소 설치를 원하는 기업은 정부로부터 적극적인 지원을 받고 있습니다. 또한 정부는 2030년까지 모든 신차 판매를 완전 전기자동차로 대체하는 야심찬 목표를 세우고 있습니다.

- 인도 정부는 2030년까지 자가용 차량 판매 대수의 30%, 상용차 판매 대수의 70%, 이륜차 및 삼륜차 판매 대수의 80%를 전기차로 만드는 것을 목표로 하고 있습니다. 이러한 야심찬 목표에 의해 인도에서는 전지 수요가 높아지고, 전지의 효율과 수명을 확보하는데 중요한 고품질 전지 분리막의 필요성이 높아지고 있습니다.

- 2019년 4월, 인도는 "인도 내 전기자동차 신속한 도입 및 제조"(FAME 인도) 계획 2단계를 시작했습니다. 이 구상은 하이브리드 자동차 및 전기자동차의 구매 가격을 낮추는 것을 목표로 하며 특히 공공 운송(버스, 인력거, 택시 등)과 자가용 오토바이에 중점을 두고 있습니다.

- 2024년 2월 정부는 FAME II 계획에 대한 투자액을 1,000억 루피(12억 650만 달러)에서 1,150억 루피(13억 8,740만 달러)로 늘릴 것이라고 발표했습니다. 이 계획은 전기자동차의 보급을 촉진할 뿐만 아니라 전기자동차에 필수적인 충전 인프라 정비에 중점을 둡니다. 또한 정부는 보조금 인센티브를 1kWh당 1만 루피에서 1만 5,000루피로 인상하였습니다. 이러한 조치는 인도에서 전기자동차의 도입을 크게 촉진하고 이에 따라 리튬 이온 전지 수요도 증가할 것으로 예상됩니다.

- 이러한 수요 급증을 바탕으로 각 전지 제조업체는 전지 부품 생산 설비를 적극적으로 설치하고 있습니다. 예를 들어, 인도의 Himadri Speciality Chemicals는 2024년 2월, 연간 2,000톤급 리튬 이온 전지 부품 제조시설 계획을 발표했습니다. 이 프로젝트는 480억 루피(5억 7,910만 달러)로 추정되며 약 6년에 걸쳐 시행될 예정입니다.

- 기술 혁신과 성능에 강력하게 초점을 맞춘 EV 산업의 역동적인 발전을 감안할 때, 전지 분리막은 인도 시장 성장을 가속하는 매우 중요한 기업 진출분야로 부상하고 있습니다. EV 시장이 상승 기조를 계속하고 있는 가운데, 이러한 주요 전지 부품 수요는 급증할 것으로 보입니다.

시장을 독점하는 리튬 이온 전지 부문

- 기존 리튬 이온 전지는 휴대폰이나 PC 등의 소비자용 전자 기기 제품에 전력을 공급하였으나 역할이 확대되어 하이브리드 자동차와 완전 전기자동차(EV)의 전원으로 높은 선호도를 얻게 되었습니다. 이 변화는 CO2나 질소산화물 등의 온실가스를 배출하지 않는 EV의 환경상 이점을 바탕으로 이루어지고 있습니다.

- 리튬 이온 전지는 높은 용량 대 중량비 덕분에 다른 유형의 전지에 비해 널리 사용됩니다. 리튬 이온 전지 도입은 뛰어난 성능, 긴 수명, 가격 하락으로 더욱 가속화되고 있습니다. 에너지 밀도가 높고 수명이 긴 리튬 이온 전지는 EV 제조업체에게 최적의 선택입니다. 세계 EV 시장을 선도하는 인도에서는 리튬 이온 전지, 그리고 나아가 전지 분리막에 대한 수요가 증가하고 있습니다.

- 이 동향을 뒷받침하는 큰 요인은 리튬 이온 전지의 가격이 일관되게 하락하고 있다는 점입니다. 지난 10년간 기술의 진보, 경제 규모 성장, 제조 공정의 발전이 비용을 낮췄습니다.

- 전 세계적으로 볼 때 리튬 이온 전지의 가격은 지난 10년간 크게 하락했습니다. 2023년 평균 리튬 이온 전지 가격은 1kWh당 약 139달러로 2013년 수준에서 82%나 하락했습니다.

- Bloomberg NEF는 2025년 이후 전지 비용이 다시 떨어질 것으로 예측했습니다. 이는 새로운 채굴 및 정제 능력이 활성화되어 리튬 가격이 하락하기 때문입니다. 동사의 2023년 전지 가격 조사는 2025년까지 평균 팩 가격이 113달러/kWh를 밑돌고, 2030년까지 80달러/kWh까지 낮아질 것으로 예측했습니다.

- 이러한 가격 하락으로 전기자동차는 적절한 예산으로 구매하기 쉬워지고 인도 내 보급이 증가하고 있습니다. 전기차를 도입하는 소비자와 기업이 증가하는 가운데, 리튬 이온 전지의 생산과 수요가 급증하고, 전지 분리막 시장은 더욱 활성화되고 있습니다.

- 그 결과, 리튬 이온 전지는 인도의 전기자동차 전지의 중심이며, 최첨단 분리막 수요를 촉진하고 시장에서 우위를 확고하게 하는 요소입니다.

인도 전기자동차 전지 분리막 산업 개요

인도 전기자동차 전지 분리막 시장은 부분 통합되어 있습니다. 주요 진출기업(순서부동)으로는 Sumitomo Chemical, Mitsubishi Chemical Group Corporation, Asahi Kasei Corp., Toray Industries, Inc., Entek International LLC 등을 들 수 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 전제조건

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 서문

- 2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 촉진요인

- 전기자동차 수요 증가

- 정부의 지원책

- 억제요인

- 기업 진입 한계

- 촉진요인

- 공급망 분석

- PESTLE 분석

- 투자 분석

제5장 시장 세분화

- 전지 유형

- 리튬 이온 전지

- 납축전지

- 기타

- 재료 유형

- 폴리프로필렌

- 폴리에틸렌

- 기타 재료 유형

제6장 경쟁 구도

- 인수합병(M&A), 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Sumitomo Chemical Co., Ltd.

- Asahi Kasei Corporation

- Mitsubishi Chemical Group Corporation

- Entek International

- Toray Industries Inc.

- 24M Technologies

- Celgard LLC

- SK Innovation Co. Ltd

- UBE Corp

- LG Chem Ltd.

- 기타 유력 기업 목록

- 시장 순위/점유율 분석

제7장 시장 기회와 앞으로의 동향

- 신흥 전지 재료의 확대

The India Electric Vehicle Battery Separator Market size is estimated at USD 1.49 million in 2025, and is expected to reach USD 2.92 million by 2030, at a CAGR of 14.43% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing demand for electric vehicles and supportive government initiatives are expected to drive the market during the forecast period.

- On the other hand, limited domestic company participation is likely to hinder market growth during the forecast period.

- Nevertheless, technological innovations and the development of sustainable materials are expected to provide significant opportunities for the market in the coming years.

India Electric Vehicle Battery Separator Market Trends

Increasing Demand for Electric Vehicles

- India ranks among the world's top five CO2 emitters. In response to the pressing issue of air pollution, the Indian government is actively promoting policies to boost the number of electric vehicles (EVs) on the roads. The Society of Manufacturers of Electric Vehicles (SMEV) reported that India achieved sales of 1.67 million EVs in 2023.

- Entities looking to establish charging stations have received clarity from the government: licensing from the ministry may not be necessary. Furthermore, the government has set an ambitious goal: by 2030, all new vehicle sales will be fully electric.

- By 2030, the Indian government aims for electric vehicles to make up 30% of private car sales, 70% of commercial vehicle sales, and a remarkable 80% of sales for two-and three-wheelers. These ambitious targets are poised to boost the demand for batteries in India and heightened the need for high-quality battery separators, which are crucial for ensuring battery efficiency and longevity.

- In April 2019, India rolled out the second phase of its "Faster Adoption and Manufacturing of Electric Vehicles in India" (FAME India) scheme. This initiative aims to lower the purchase price of hybrid and electric vehicles, particularly focusing on public transportation (like buses, rickshaws, and taxis) and private two-wheelers.

- In February 2024, the government announced a boost in investment for the FAME II scheme, raising it from INR 10,000 crore (USD 1206.5 million) to INR 11,500 crore (USD 1387.4 million). This scheme not only focuses on enhancing the adoption of electric vehicles but also emphasizes the establishment of essential charging infrastructure. Additionally, the government has upped the subsidy incentives from Rs 10,000 per kWh to Rs 15,000 per kWh. Such measures are anticipated to significantly bolster the adoption of electric vehicles in India, subsequently driving up the demand for lithium-ion batteries.

- In light of this surging demand, battery manufacturers are proactively setting up facilities for battery component production. For example, in February 2024, Himadri Speciality Chemicals, an Indian firm, unveiled plans for a lithium-ion battery component manufacturing facility, boasting a capacity of 2 lakh tonnes per annum. The project, estimated at INR 4,800 crore (USD 579.1 million), is set to unfold over approximately six years.

- Given the dynamic evolution of the EV industry, with its strong focus on innovation and performance, battery separators are emerging as pivotal players, propelling market growth in India. As the EV market continues its upward trajectory, the demand for these vital battery components is set to surge.

Lithium-Ion Batteries Segment to Dominate the Market

- Traditionally, lithium-ion batteries powered consumer electronics like mobile phones and PCs. However, their role has evolved, becoming the preferred power source for hybrid and fully electric vehicles (EVs). This shift is largely attributed to the environmental benefits of EVs, which produce no CO2, nitrogen oxides, or other greenhouse gases.

- Lithium-ion batteries are outpacing other battery types in popularity, thanks to their favorable capacity-to-weight ratio. Their adoption is further fueled by superior performance, extended shelf life, and plummeting prices. With high energy density and long cycle life, lithium-ion batteries have become the go-to choice for EV manufacturers. As India spearheads the global EV market, the demand for lithium-ion batteries-and by extension, battery separators-is on the rise.

- A major factor bolstering this trend is the consistent drop in lithium-ion battery prices. Over the last decade, technological advancements, economies of scale, and refined manufacturing processes have driven down costs.

- On a global scale, lithium-ion battery prices have seen a dramatic decline over the past decade. In 2023, an average lithium-ion battery was priced at approximately USD 139 per kWh, marking an impressive 82% drop from 2013 levels.

- Looking ahead, BloombergNEF projects a renewed decline in battery costs starting 2025. This is attributed to the activation of new extraction and refinery capacities, leading to a softening of lithium prices. Their 2023 Battery Price Survey forecasts the average pack price to dip below USD 113/kWh by 2025 and further down to USD 80/kWh by 2030.

- This price reduction has made electric vehicles more budget-friendly, spurring their widespread adoption in India. With a growing number of consumers and businesses embracing EVs, the surge in lithium-ion battery production and demand has further bolstered the market for battery separators.

- Consequently, lithium-ion batteries remain central to India's EV battery landscape, propelling the demand for cutting-edge separators and solidifying their dominant market position.

India Electric Vehicle Battery Separator Industry Overview

The Indian electric vehicle battery separator market is semi-consolidated. Some of the major players (not in particular order) include Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, Asahi Kasei Corporation, Toray Industries, Inc., and Entek International LLC among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand of Electric Vehicles

- 4.5.1.2 Supportive Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Limited Company Participation

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Others

- 5.2 Material Type

- 5.2.1 Polypropylene

- 5.2.2 Polyethylene

- 5.2.3 Other Material Types

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Sumitomo Chemical Co., Ltd.

- 6.3.2 Asahi Kasei Corporation

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Entek International

- 6.3.5 Toray Industries Inc.

- 6.3.6 24M Technologies

- 6.3.7 Celgard LLC

- 6.3.8 SK Innovation Co. Ltd

- 6.3.9 UBE Corp

- 6.3.10 LG Chem Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion in Emerging Battery Materials