|

시장보고서

상품코드

1636444

중국의 전기자동차용 배터리 분리막 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)China Electric Vehicle Battery Separator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

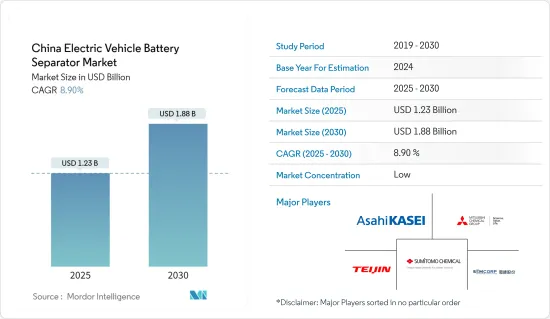

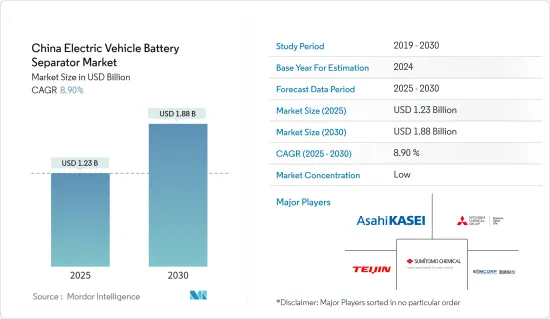

중국의 전기자동차용 배터리 분리막 시장 규모는 2025년 12억 3,000만 달러, 2030년 18억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 8.9%에 이를 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 전기자동차 수요 증가나 정부의 지원책 등의 요인이 예측기간 중 시장을 견인할 것으로 전망됩니다.

- 반면에 공급망 문제는 예측 기간 동안 시장 성장을 방해할 가능성이 높습니다.

- 그럼에도 불구하고 기술 혁신과 지속 가능한 재료의 개발은 앞으로 몇 년동안 시장에 큰 기회를 가져올 것으로 예상됩니다.

중국 전기자동차용 배터리 분리막 시장 동향

전기차 수요 증가

- 중국은 세계 최대의 전기자동차(EV) 시장으로 EV 배터리 수요 급증이 배터리 분리막 시장의 성장을 뒷받침하고 있습니다. 국제에너지기구(IEA)의 보고에 따르면 중국은 2023년에 810만대의 전기자동차를 판매하며, 이는 배터리 전기자동차(BEV)와 플러그인 하이브리드 전기자동차(PHEV)를 모두 포함합니다.

- EV 수요 증가에 따라 배터리 성능을 높이는 고기능 분리막의 요구가 높아지고 있습니다. 이러한 분리막은 특히 자동차 제조업체가 항속거리, 효율성, 안전성 향상에 주력하는 가운데 단락을 방지하고 배터리의 안정성을 확보하는데 중요한 역할을 하고 있습니다.

- 중국은 세계 전기차의 절반 이상을 차지하며 신에너지 차량(NEV)의 2025년 판매 목표를 웃돌고 있습니다. 이 약진은 정부의 인센티브와 지원 정책에 의해 뒷받침됩니다.

- 예를 들어 2023년 6월 국내 EV 판매를 더욱 자극하는 것을 목적으로 재정부(MOF), 국가세무총국(STA), 공업정보화부(MIIT)의 연합은 "신에너지차에 대한 자동차 구매세 감면정책"의 연장을 발표했습니다. 이 면세 조치는 2024년 1월 1일부터 적용되며 2027년 12월 31일까지 계속됩니다.

- 게다가 정부의 강력한 백업을 지원하는 중국의 야심찬 EV 도입 목표는 배터리 제조 부문의 성장에 박차를 가하고 있습니다. 이 급성장은 생산능력 확대, 선구적인 연구개발, 배터리 기술 한계에 대한 과제를 향한 많은 투자로도 분명합니다.

- 주목할만한 움직임으로 2024년 8월 중국의 유명한 하이테크 기업인 Xiaomi가 베이징에서 두 번째 EV 공장을 착공했습니다. 베이징시 당국의 문서에 따르면 이미 스마트폰 분야에서 압도적인 힘을 자랑하는 Xiaomi는 7월 25일 토지를 확보하고 다음날에 곧바로 건설에 착수했습니다. 전략적으로 이 새로운 시설은 Xiaomi의 첫 번째 EV 공장 바로 옆에 지어졌습니다. 증가하는 EV 수요에 대응하기 위해, 제조업체 각사가 증산에 나서는 가운데, 배터리 분리막의 중요성은 점점 밝혀지고 있습니다.

- 이와 같이 EV 산업이 혁신과 성능에 중점을 두고 진화함에 따라 배터리 분리막이 매우 중요한 선수로 부상하고 중국 시장 성장에 박차를 가하고 있습니다. EV 시장이 상승 기조에 있는 가운데, 이러한 중요한 배터리 부품 수요는 급증할 전망입니다.

시장을 독점하는 리튬 이온 배터리 부문

- 중국에서는 급성장하는 전기자동차(EV) 생태계에서 리튬 이온 배터리 부문이 중요한 역할을 하고 있습니다. 2023년에는 전기차 신규 등록 대수의 60%를 중국이 차지합니다. 세계 최대 수준의 전기자동차의 생산국 및 소비국인 중국의 영향력은 전기자동차의 에너지원으로서 필수적인 리튬이온 배터리의 진화와 수용에 있어서 가장 중요합니다.

- 에너지 밀도와 효율로 알려진 리튬 이온 배터리는 안전성과 신뢰성에서 고성능 분리막에 의존합니다. 이러한 분리막은 음극과 양극 사이의 단락을 방지할 뿐만 아니라 충방전 동안 효율적인 이온 이동을 촉진합니다.

- 중국에서는 폴리에틸렌(PE)과 폴리프로필렌(PP)과 같은 분리막 소재의 발전으로 리튬 이온 배터리의 성능, 내구성 및 열 안정성이 향상되었습니다.

- 예를 들어 2024년 1월 중국 과학원(CAS)의 현대 물리학 연구소(IMP)와 선진 에너지 과학 기술 광동 연구소의 팀이 새로운 폴리에틸렌 테레프탈레이트(PET) 분리막을 발표했습니다. 리튬 이온 배터리용으로 설계된 이 분리막는 고온에 견딜 수 있어 전기자동차의 성능과 소비자의 매력을 직접적으로 향상시킵니다.

- 주목할만한 것은 리튬 이온 배터리의 평균 가격이 일관되게 하락함에 따라 2023년에는 1kWh당 약 139달러에 달할 전망입니다. 이는 2013년 이후 82% 이상의 하락을 의미합니다. 이 추세는 앞으로도 계속되고 2025년에는 113달러/kWh를 밑돌고 2030년에는 80달러/kWh에 이를 가능성이 있을 것으로 예측됩니다. 리튬 이온 배터리의 가격이 떨어지고 전기자동차가 더 친숙해지면서 배터리 분리막 수요도 급증합니다. 비용 최적화와 성능 향상에 열성적인 제조업체가 이 수요를 이끌고 있습니다.

- 또한 자동차 판매량의 40%를 전기차로 만드는 중국의 야망은 전기자동차용 배터리와 부품(분리막 포함) 수요 증가를 더욱 두드러지게 만들고 있습니다.

- 따라서 기술적 진보, 급성장하는 EV 시장, 배터리 가격의 급락으로 중국의 배터리 분리막 시장이 크게 확대되고 있습니다.

중국 전기자동차용 배터리 분리막 산업 개요

중국의 전기자동차용 배터리 분리막 시장은 세분화되어 있습니다. 주요 기업(순부동)에는 Shanghai Energy New Materials Technology Co., Ltd. (SEMCORP), Teijin Limited, Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, Asahi Kasei Corporation 등이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2029년까지 시장 규모 및 수요 예측(단위: 10억 달러)

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 전기자동차 수요 증가

- 정부의 지원책

- 억제요인

- 공급망의 과제

- 성장 촉진요인

- 공급망 분석

- PESTLE 분석

- 투자 분석

제5장 시장 세분화

- 전지 유형별

- 리튬 이온 배터리

- 납축전지

- 기타

- 재료 유형별

- 폴리프로필렌

- 폴리에틸렌

- 기타 재료 유형

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Shanghai Energy New Materials Technology Co., Ltd.(SEMCORP)

- Teijin Limited

- Sumitomo Chemical Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Asahi Kasei Corporation

- Entek International

- Shanghai PTL New Energy Technology Co., Ltd.

- Toray Industries Inc.

- UBE Corp

- SK Innovation Co. Ltd

- 시장 랭킹/점유율 분석

- 기타 유명 기업 일람

제7장 시장 기회와 앞으로의 동향

- 신흥 배터리 재료의 확대

The China Electric Vehicle Battery Separator Market size is estimated at USD 1.23 billion in 2025, and is expected to reach USD 1.88 billion by 2030, at a CAGR of 8.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing demand for electric vehicles and suppotive government initiatives are expected to drive the market during the forecast period.

- On the other hand, supply chain challanges are likely to hinder the market growth during the forecast period.

- Nevertheless, technological innovations and development of sustainable materials are expected to provide significant opportunities for the market in the coming years.

China Electric Vehicle Battery Separator Market Trends

Increasing Demand for Electric Vehicles

- China stands as the world's largest electric vehicle (EV) market, with the surging demand for EV batteries propelling the growth of the battery separator market. The International Energy Agency reported that in 2023, China sold 8.1 million electric vehicles, encompassing both Battery Electric Vehicles (BEV) and Plug-in Hybrid Electric Vehicles (PHEV).

- With the rising demand for EVs comes an increased need for sophisticated separators that enhance battery performance. These separators play a crucial role in preventing short circuits and ensuring battery stability, especially as automakers focus on improving vehicle range, efficiency, and safety.

- China dominates the global EV landscape, boasting over half of the world's electric automobiles and surpassing its 2025 sales target for new energy vehicles (NEVs). This surge is bolstered by government incentives and supportive policies.

- For example, in June 2023, aiming to further stimulate domestic EV sales, a coalition of the Ministry of Finance (MOF), State Taxation Administration (STA), and Ministry of Industry and Information Technology (MIIT) announced an extension of the "Vehicle Purchase Tax Reduction and Exemption Policy for New Energy Vehicles." This tax exemption, effective from January 1, 2024, is set to continue until December 31, 2027.

- Furthermore, China's ambitious EV adoption targets, underpinned by robust government backing, have catalyzed the growth of its battery manufacturing sector. This surge is evident in substantial investments directed towards expanding production capacities, pioneering research & development, and pushing the boundaries of battery technologies.

- In a notable move, in August 2024, Xiaomi, the renowned Chinese tech titan, broke ground on its second EV plant in Beijing. Documents from the Beijing city authorities reveal that Xiaomi, already a dominant player in the smartphone arena, secured the land on July 25 and promptly initiated construction the very next day. Strategically, this new facility is rising right next to Xiaomi's inaugural EV plant. As manufacturers ramp up to cater to the escalating EV demand, the significance of battery separators becomes increasingly evident.

- Thus, as the EV industry evolves with a keen focus on innovation and performance, battery separators emerge as pivotal players, fueling market growth in China. With the EV market on an upward trajectory, the demand for these critical battery components is set to soar.

Lithium-Ion Batteries Segment to Dominate the Market

- In China, the lithium-ion battery segment plays a crucial role in the burgeoning electric vehicle (EV) ecosystem. In 2023, China accounted for 60% of all new electric car registrations. As a leading global producer and consumer of electric vehicles, China's influence is paramount in the evolution and acceptance of lithium-ion batteries, which are indispensable for energizing these vehicles.

- Lithium-ion batteries, known for their energy density and efficiency, depend on high-performance separators for safety and reliability. These separators not only prevent short circuits between the anode and cathode but also facilitate efficient ion transfer during charging and discharging.

- In China, advancements in separator materials like polyethylene (PE) and polypropylene (PP) have enhanced the performance, durability, and thermal stability of lithium-ion batteries.

- For example, in January 2024, a team from the Institute of Modern Physics (IMP) at the Chinese Academy of Sciences (CAS) and the Advanced Energy Science and Technology Guangdong Laboratory unveiled new polyethylene terephthalate (PET) separators. These separators, designed for lithium-ion batteries, can endure high temperatures, directly boosting electric vehicle performance and consumer appeal.

- Notably, the average price of lithium-ion batteries has consistently fallen, hitting approximately USD 139 per kWh in 2023. This marks an over 82% drop since 2013. Projections suggest this trend will persist, with prices potentially dipping below USD 113/kWh by 2025 and reaching USD 80/kWh by 2030. As lithium-ion battery prices decline, making electric vehicles more accessible, there's a corresponding surge in demand for battery separators. Manufacturers, keen on optimizing costs and boosting performance, are driving this demand.

- Moreover, China's ambition to have 40% of all vehicle sales be electric further underscores the rising demand for EV batteries and their components, including separators.

- Thus, with technological strides, a burgeoning EV market, and plummeting battery prices, China's battery separator landscape is set for significant expansion.

China Electric Vehicle Battery Separator Industry Overview

The Chinese electric vehicle battery separator market is semi-fragmented. Some of the major players (not in particular order) include Shanghai Energy New Materials Technology Co., Ltd. (SEMCORP), Teijin Limited, Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, and Asahi Kasei Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand of Electric Vehicles

- 4.5.1.2 Supportive Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Challanges

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Others

- 5.2 Material Type

- 5.2.1 Polypropylene

- 5.2.2 Polyethylene

- 5.2.3 Other Material Types

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shanghai Energy New Materials Technology Co., Ltd. (SEMCORP)

- 6.3.2 Teijin Limited

- 6.3.3 Sumitomo Chemical Co., Ltd.

- 6.3.4 Mitsubishi Chemical Group Corporation

- 6.3.5 Asahi Kasei Corporation

- 6.3.6 Entek International

- 6.3.7 Shanghai PTL New Energy Technology Co., Ltd.

- 6.3.8 Toray Industries Inc.

- 6.3.9 UBE Corp

- 6.3.10 SK Innovation Co. Ltd

- 6.4 Market Ranking/Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion in Emerging Battery Materials