|

시장보고서

상품코드

1636464

아세안 국가의 전기자동차 전지 분리막 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)ASEAN Countries Electric Vehicle Battery Separator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

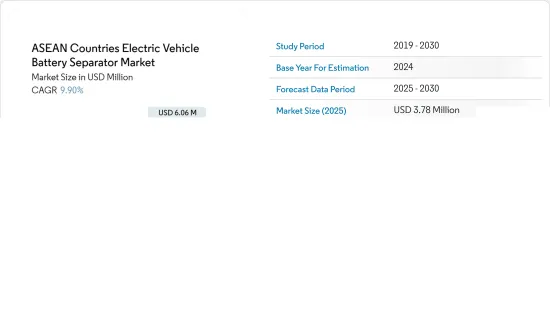

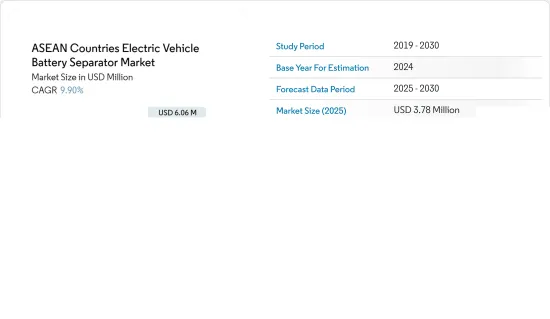

아세안 국가의 전기자동차 전지 분리막 시장 규모는 2025년에 378만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 9.9%로, 2030년에는 606만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 전기자동차 보급과 리튬 이온 전지 가격 하락이 예측 기간 시장을 견인할 것으로 보입니다.

- 한편 일부 국가의 독점으로 인한 전지 재료공급망 격차(원재료 부족 및 유통 병목 현상 등)는 향후 시장 성장을 억제할 것으로 예상됩니다.

- 고체 전지, 첨단 리튬 이온 화학, 나트륨 이온 전지 등 다른 전지화학 연구개발이 진행되면서 향후 시장에 기회를 가져올 것으로 예상됩니다.

- 아세안 국가의 전기자동차 전지 분리막 시장에서는 지역 전체에서 EV의 보급이 진행되고 있기 때문에 태국이 큰 성장을 이룰 것으로 예측되고 있습니다.

아세안 국가의 전기자동차 전지 분리막 시장 동향

리튬 이온 전지 유형이 시장을 독점

- 에너지 밀도가 높고 수명이 길며 자가방전율이 낮은 것으로 알려진 리튬 이온 전지는 전기자동차(EV)에 선호됩니다. 리튬 이온 전지의 압도적인 선호도는 EV용 전지 분리막 시장의 성장을 가속할 뿐만 아니라 EV 산업의 광범위한 궤도를 형성하고 있습니다.

- 주요 시장 진출기업은 R&D 투자와 생산 능력을 강화하고 경쟁을 격화시켜 가격을 인하하고 있습니다. Bloomberg NEF는 EV와 전지 에너지 저장 시스템(BESS) 전지 팩의 평균 가격은 일반적으로 상승하고 있지만, 2023년에는 13%나 크게 하락하여 139달러/kWh가 될 것으로 지적하고 있습니다. 예측에 따르면 이 하락은 앞으로도 계속되어 2025년에는 113달러/kWh에 이르고 2030년에는 80달러/kWh까지 하락할 것으로 예상됩니다.

- 태국, 필리핀, 말레이시아, 인도네시아 및 베트남을 포함한 아세안 국가들은 세계 리튬 이온 전지 공급망의 주요 국가로 부상하고 있으며 전략적 입지, 정부 우대 정책, 풍부한 천연 자원으로 전지 제조 투자를 유치하는 데 성공했습니다.

- 2024년 7월 인도네시아는 최초의 EV용 전지 공장을 건설했습니다. 동남아시아 최대의 경제대국이며 세계 유수의 니켈 매장량을 자랑하는 인도네시아는 세계의 전기차 공급망에서 중요한 역할을 담당하고 있습니다. 한국의 대기업 LG Energy Solution(LGES)과 현대자동차그룹의 합작사업인 이 공장은 전지 셀 생산으로 10기가와트(GWh)의 연간 생산 능력을 자랑합니다. 이러한 노력은 앞으로 몇 년동안 동지역에서 리튬 이온 전지 생산을 강화할 전망입니다.

- 또한 에너지 밀도 향상, 안전 기능 개선, 충전 가속화 등 리튬 이온 전지 기술의 진보가 혁신적인 분리막 재료 개발에 박차를 가하고 있습니다. 리튬 이온 전지의 에너지와 열 수요를 충족시키기 위해 중요한 분리기는 안전성과 신뢰성을 확보하는 데 중요한 역할을 하며, 이에 따라 분리기 시장의 혁신과 수요가 증가하고 있습니다.

- 2023년 6월, ProLogium은 획기적인 전지 아키텍처를 발표하여 30년에 걸친 리튬 이온 기술에 큰 진화를 가져왔습니다. 종래의 폴리머 분리막 필름을 세라믹으로 대체함으로써, ProLogium은 전기자동차용 리튬 이온 전지 부문에 새로운 기준을 제시했습니다. 이러한 기술 혁신은 동지역에서 첨단 리튬 전지용 분리막 수요를 확대하는데 기여하고 있습니다.

- 이러한 개발로 리튬 이온 전지의 생산이 급증하고 예측 기간 동안 전기자동차 전지 분리막의 용량이 대폭 증가할 것으로 예상됩니다.

태국의 현저한 성장

- 탄탄한 자동차 산업과 전략적 위치 및 정부의 지원으로 태국은 아세안 지역에서 최고의 EV용 전지 분리막 생산국으로 부상했습니다. 태국이 청정에너지로 전환하고 전기차를 도입함에 따라 기업은 이 중요한 부문에 집중하고 있습니다. 소비자의 관심이 높아지는 배경으로는 환경 의식이 높아지고 전기자동차 소유의 경제적 이점과 산업의 급속한 기술 진보를 예로 들 수 있습니다.

- 최근 아세안 지역에서는 전기차(EV) 판매가 급증하고 있습니다. 예를 들어 태국 자동차 연구소에 따르면 2023년 전지식 전기자동차(BEV) 등록 대수는 7만 6,360대에 이르며 2022년 대비 6.89배, 2019년 대비 47.6배라는 경이로운 성장을 보였습니다. BEV를 포함한 EV 판매 대수 증가가 예측되는 가운데, 동지역의 전지와 전지 분리막 수요는 확대될 것으로 보입니다.

- 또한 동지역의 전지 분리막은 리튬 이온 전지 가격 하락, 수요 급증, EV 응용 분야에서 중요한 안전과 효율성 등의 과제를 극복하고 있습니다. 최근 주요 세계 기업은 동지역의 EV용 리튬 이온 전지 생산을 강화하는 프로젝트에 투자하고 있습니다.

- 예를 들어 BMW는 2024년 2월 태국 라용에 전기차용 전지 공장을 신설한다고 발표했습니다. 이 구상으로 태국의 전지 공급망이 강화될 것으로 기대됩니다. BMW는 태국을 EV용 전지의 중요한 수출 거점으로 선정하고 보다 큰 아시아태평양 시장을 노리고 있습니다. 이러한 움직임은 태국에서의 전지 생산을 뒷받침하고 향후 몇 년간 리튬 이온 전지용 분리막 수요를 높일 가능성이 높습니다.

- 또한, 태국 자동차 산업은 혁신적인 전기자동차(EV) 모델의 생산을 강화하고 있습니다. 세계 주요 기업들이 EV 제조로 전환하는 가운데 고급 전지 부품, 특히 분리막 수요가 현저하게 급증하고 있습니다. 이 동향은 산업의 혁신과 지속가능성에 대한 노력을 돋보이게 합니다.

- 예를 들어, 2024년 8월 Omoda와 중국의 자동차 제조업체 Chery Automobile의 지사인 Jaecoo Thailand는 전기자동차(EV) 모델 2종을 공개하였는데 컴팩트 SUV Omoda C5 EV와 오프로드 SUV Jaecoo 6 EV을 발표하여 태국 내 입지를 강화했습니다. 이러한 노력으로 동지역에서는 전기자동차 라인업이 확대되고 이는 EV용 전지 분리막 시장의 성장을 뒷받침하고 있습니다.

- 이러한 프로젝트와 대처의 결과 EV 수요가 상승하여 향후 수년간 EV용 전지 분리막의 수요를 대폭 높일 것으로 예상됩니다.

아세안 국가의 전기자동차 전지 분리막 산업 개요

아세안 국가의 전기자동차 전지 분리막 시장은 어느정도 분산된 형태를 띠고 있습니다. 주요 진출기업(순서부동)은 Mitsubishi Chemical Group Corporation, Hitachi Chemical Company Ltd, Toray Industries Inc., Sumitomo Chemical Co. Ltd, Teijin Ltd 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 촉진요인

- 전기자동차 보급 확대

- 전지 원료 비용 저하

- 억제요인

- 공급망 격차

- 촉진요인

- 공급망 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협 제품 및 서비스

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 세분화

- 전지

- 리튬 이온

- 납축전지

- 기타

- 재료 유형

- 폴리프로필렌

- 폴리에틸렌

- 기타 재료 유형

- 지역

- 인도네시아

- 베트남

- 태국

- 미얀마

- 필리핀

- 기타 아세안 국가

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Mitsubishi Chemical Group Corporation

- Hitachi Chemical Company Ltd

- Toray Industries Inc.

- Sumitomo Chemical Co. Ltd

- Teijin Ltd

- SK Nexilis

- Asahi Kasei

- W-Scope Corporation

- Southeast Asia Manufacturing Co., Ltd

- 기타 유력 기업 목록

- 시장 순위 분석

제7장 시장 기회와 앞으로의 동향

- 기타 전지화학 연구개발 증가

The ASEAN Countries Electric Vehicle Battery Separator Market size is estimated at USD 3.78 million in 2025, and is expected to reach USD 6.06 million by 2030, at a CAGR of 9.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, the growing adoption of electric vehicles and the decreasing price of lithium-ion batteries is expected to drive the market in the forecast period.

- On the other hand, the supply chain gap in battery materials created by the monopolies of some countries, such as ingredient shortages or distribution bottlenecks, is expected to restrain market growth in the future.

- Nevertheless, the increasing research and development of other battery chemistries like solid-state batteries, advanced lithium-ion chemistry, Sodium-ion batteries, etc, are expected to create an opportunity for the market in the future.

- Thailand is anticipated to witness significant growth in the ASEAN countries' electric vehicle battery separation market due to the rising adoption of EVs across the region.

ASEAN Countries Electric Vehicle Battery Separator Market Trends

Lithium-Ion Battery Type to Dominate the Market

- Li-ion batteries, known for their high energy density, long cycle life, and low self-discharge rate, are the preferred choice for electric vehicles (EVs). This dominant preference not only propels the growth of the EV battery separator market but also shapes the broader trajectory of the EV industry.

- Key market players are boosting their R&D investments and production capabilities, intensifying competition and driving prices down. Bloomberg NEF highlights that while average battery pack prices for EVs and battery energy storage systems (BESS) have generally risen, 2023 marked a significant 13% drop, bringing prices down to USD 139/kWh. Projections suggest this decline will persist, with prices anticipated to reach USD 113/kWh by 2025 and plummet further to USD 80/kWh by 2030, driven by relentless technological and manufacturing advancements.

- ASEAN nations, including Thailand, the Philippines, Malaysia, Indonesia, and Vietnam, are emerging as key players in the global lithium-ion battery supply chain. Their strategic locations, government incentives, and abundant natural resources have successfully attracted investments into battery manufacturing.

- In July 2024, Indonesia launched its first-ever EV battery plant. As Southeast Asia's largest economy and the custodian of the world's most extensive nickel reserves, Indonesia is carving out a significant role in the global electric vehicle supply chain. This plant, a joint venture between South Korean titans LG Energy Solution (LGES) and Hyundai Motor Group, boasts a robust annual capacity of 10 Gigawatt hours (GWh) for battery cell production. Such initiatives are poised to bolster lithium-ion battery production in the region in the coming years.

- Moreover, advancements in lithium-ion battery technology, such as heightened energy density, improved safety features, and accelerated charging, are spurring the development of innovative separator materials. These separators, crucial for meeting the energy and thermal demands of Li-ion batteries, play a vital role in ensuring safety and reliability, thereby driving innovation and demand in the separator market.

- In June 2023, ProLogium unveiled a groundbreaking battery architecture, marking a significant evolution in three decades of lithium-ion technology. By substituting the traditional polymer separator film with a ceramic alternative, ProLogium has set a new standard in the lithium-ion battery sector for electric vehicles. Such innovations are poised to amplify the demand for advanced lithium battery separators in the region.

- Given these developments, the production of lithium-ion batteries is set to surge, leading to a substantial increase in the capacity of EV battery separators during the forecast period.

Thailand to Witness Significant Growth

- Thailand, with its robust automotive industry, strategic positioning, and government support, has emerged as the top producer of EV battery separators in the ASEAN region. As the country shifts towards clean energy and embraces electric vehicles, companies are sharpening their focus on this crucial segment. Rising consumer interest is driven by increased environmental awareness, the economic advantages of EV ownership, and swift technological progress in the industry.

- Recently, electric vehicle (EV) sales have surged in the ASEAN region. For instance, the Thailand Automotive Institute reported that in 2023, registered battery electric vehicles (BEVs) reached 76.36 thousand units, marking a 6.89-fold increase from 2022 and a staggering 47.6-fold jump since 2019. With EV sales, including BEVs, projected to rise, the demand for batteries and battery separators in the region is set to amplify.

- Additionally, battery separators in the region are navigating challenges like falling lithium-ion battery prices, escalating demand, and the crucial need for safety and efficiency in EV applications. Recently, leading global companies have invested in projects to enhance lithium-ion battery production for EVs in the region.

- For example, in February 2024, BMW announced a new battery factory for electric vehicles in Rayong, Thailand. This initiative is expected to strengthen the country's battery supply chains. BMW sees Thailand as a key export center for its EV batteries, aiming at the larger Asia Pacific market. Such moves are likely to boost battery production in Thailand and heighten the demand for lithium-ion battery separators in the coming years.

- Furthermore, Thailand's automotive industry is ramping up the production of innovative electric vehicle (EV) models. As global leaders pivot to include EV manufacturing, there's a notable surge in demand for premium battery components, especially separators. This trend highlights the industry's commitment to innovation and sustainability.

- For instance, in August 2024, Omoda and Jaecoo Thailand, a branch of the Chinese automaker Chery Automobile, strengthened their presence in Thailand by launching two electric vehicle (EV) models. The debut included two versions for each model: the compact SUV Omoda C5 EV and the rugged off-road SUV Jaecoo 6 EV, making its global debut in a right-hand drive variant. Such initiatives are expanding their electric vehicle offerings in the region, fueling the growth of the EV battery separator market.

- Consequently, these projects and initiatives are poised to boost EV demand and substantially elevate the need for EV battery separators in the coming years.

ASEAN Countries Electric Vehicle Battery Separator Industry Overview

ASEAN Countries' electric vehicle battery separator market is semi-fragmented. Some key players (not in particular order) are Mitsubishi Chemical Group Corporation, Hitachi Chemical Company Ltd, Toray Industries Inc., Sumitomo Chemical Co. Ltd, Teijin Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Electric Vehicles

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 The Supply Chain Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Others

- 5.2 Material Type

- 5.2.1 Polypropylene

- 5.2.2 Polyethylene

- 5.2.3 Other Material Types

- 5.3 Geography

- 5.3.1 Indonesia

- 5.3.2 Vietnam

- 5.3.3 Thailand

- 5.3.4 Myanmar

- 5.3.5 Philippines

- 5.3.6 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Chemical Group Corporation

- 6.3.2 Hitachi Chemical Company Ltd

- 6.3.3 Toray Industries Inc.

- 6.3.4 Sumitomo Chemical Co. Ltd

- 6.3.5 Teijin Ltd

- 6.3.6 SK Nexilis

- 6.3.7 Asahi Kasei

- 6.3.8 W-Scope Corporation

- 6.3.9 Southeast Asia Manufacturing Co., Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Research and Development of Other Battery Chemistries