|

시장보고서

상품코드

1639528

바이오 PET : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Bio-PET - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

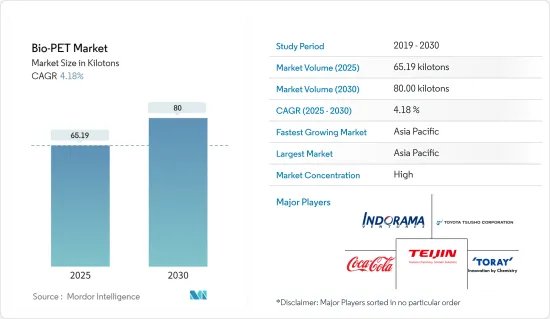

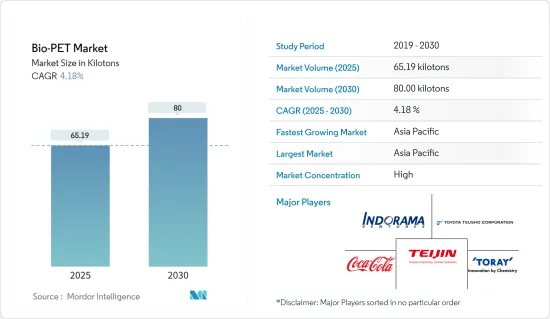

바이오 PET 시장 규모는 2025년에 65.19 킬로톤으로 추정되며, 2030년에는 80.00 킬로톤에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 4.18%의 CAGR을 기록할 것으로 예상됩니다.

COVID-19의 발생으로 인해 2020년에는 전 세계 봉쇄, 제조 활동 및 공급망 중단, 생산 중단으로 인해 시장에 부정적인 영향을 미쳤습니다. 그러나 2021년에는 상황이 회복되기 시작하면서 시장의 성장 궤도가 회복되었습니다.

주요 하이라이트

- 온실가스(GHG) 배출에 대한 우려가 높아지는 것이 시장을 주도하는 주요 요인 중 하나입니다.

- 그러나 PEF(폴리에틸렌 푸라노에이트)의 개발과 바이오 PET의 낮은 융점이 시장을 억제할 가능성이 높습니다.

- 패러다임 전환을 촉진하는 환경적 요인이 예측 기간 동안 바이오 PET에 대한 수요를 증가시킬 가능성이 높습니다.

- 재생 가능 자원에 대한 관심은 향후 시장 성장의 기회가 될 것으로 보입니다.

- 아시아태평양이 세계 시장을 주도하고 북미가 근소한 차이로 그 뒤를 이을 것으로 예상됩니다. 예측 기간 동안 아시아태평양이 가장 높은 성장률을 보일 것으로 예상됩니다.

바이오 PET 시장 동향

병 용도가 시장을 독점

- 바이오 PET는 병 용도에 널리 사용되고 있습니다. 화석연료 기반 제품에 대한 의존도를 줄이고자 하는 기업의 의지로 인해 전 세계적으로 수요가 급증하고 있습니다. 또한, 바이오 기반 제품에 대한 소비자의 수요도 증가하고 있습니다.

- 바이오 PET는 10억 명의 사람들에게 깨끗한 식수를 제공함으로써 음료 산업의 발전에 기여한 포장재입니다. 이 소재는 안전성이 높고, 가볍고 투명하며, 재밀봉이 가능하고, 성형이 가능하며, 100% 재활용이 가능하고, 우수한 기계적 특성과 장벽 특성을 가지고 있습니다.

- 바이오 PET는 수년 전부터 시장에 존재해 왔습니다. 이 플라스틱은 30%는 재생 가능하고 70%는 석유 기반 원료로 만들어집니다. 바이오 PET의 기계적 특성과 열적 특성은 다른 석유 기반 PET 제품과 유사하여 버진 PET를 대체할 수 있는 이상적인 소재입니다.

- 바이오 PET(폴리에틸렌 테레프탈레이트)는 부분적으로 재생 가능한 원료로 만들어집니다. 그 장점은 분명합니다. 재생 가능한 원료를 더 많이 사용함으로써 석유에서 추출한 원료를 더 적게 사용할 수 있습니다. 소비자들이 점점 더 중요시하고 차별화를 가능하게 하는 주제입니다. 바이오 PET는 브랜드 소유자가 자신의 입장을 강조하고 제품에 대한 관심을 끌 수 있습니다.

- 국제 생수 협회(IBWA)의 보고서에 따르면 생수는 미국에서 가장 많이 소비되는 음료 제품입니다. 아시아태평양에서도 비슷한 추세가 지속되고 있으며, 최근 몇 년 동안 포장된 식수 소비가 증가하고 있습니다. 소규모 제조업체들이 병 제조를 위한 방대한 생산능력으로 시장에 넘쳐나면서 바이오 PET 시장을 적극적으로 지원하고 있습니다.

- 위와 같은 이유로 병 용도가 시장을 독점할 가능성이 높습니다.

아시아태평양이 시장을 장악

- 아시아태평양에는 세계 인구의 절반이 살고 있으며, PET병 소비량도 많습니다.

- 이 지역은 섬유, 포장 등 다양한 용도에서 바이오 PET가 널리 수용되는 데 크게 기여하고 있어 바이오 PET 사용량 성장에 중요한 역할을 할 것으로 예상됩니다.

- 바이오 PET의 높은 가격은 소비자의 높은 비용 의식으로 인해 이 지역에서 널리 수용되는 데 장애가 되고 있습니다.

- 대형 제조업체들은 바이오 PET의 저가화에 주력하고 있으며, 저가화의 성공은 바이오 PET로의 시장 전환에 큰 영향을 미치고 있습니다.

- 아시아태평양에서는 라이프스타일의 변화, 가처분 소득의 증가, 직장인의 증가, 패스트푸드에 대한 선호도 증가로 인해 포장 식품에 대한 수요가 증가하고 있습니다. 소비자들은 조리 시간이 짧고, 신선하며, 매력적이고 견고한 포장으로 조리된 식품을 선호하고 있으며, 이는 조사 대상 시장의 수요를 뒷받침하고 있습니다.

- 중국은 일인당 소득 증가와 E-Commerce 대기업의 부상 등의 요인으로 인해 세계 최대의 포장 소비국이며, FMCG 및 포장 산업의 꾸준한 성장으로 중국은 아시아태평양에서 가장 높은 시장 점유율을 차지하고 있습니다.

- 또한, 중국의 포장 산업은 경제 성장과 구매력이 높은 중산층의 증가로 인해 최근 몇 년 동안 지속적으로 빠르게 성장하고 있습니다. Interpak에 따르면, 2023년 중국의 식품 포장 카테고리의 총 포장량은 4,470억 개에 달할 것으로 예상되며, 이는 포장 산업에서 연구 시장에 대한 수요가 증가하고 있다는 것을 보여줍니다.

- 인도의 포장 산업은 세계 5위의 규모를 자랑하며, 인도 플라스틱 산업 협회에 따르면 연간 약 22-25%의 성장률을 보이고 있습니다. 고도로 숙련된 노동력과 저렴한 인건비로 인해 포장 및 가공식품의 비용은 유럽보다 40% 낮게 책정될 수 있습니다. 인구 증가와 포장 수요 증가가 시장을 견인할 것으로 예상됩니다.

- 인도포장 산업협회(PIAI)에 따르면 인도의 포장 산업은 예측 기간 동안 22% 성장할 것으로 예상됩니다. 또한, 인도 포장 시장은 2020-2025년 동안 26.7%의 CAGR을 기록하여 2025년에는 2,048억 1,000만 달러에 달할 것으로 예상됩니다. 따라서 바이오 PET 시장은 이 지역에서 성장할 것으로 예상됩니다.

- 따라서 위의 이유로 예측 기간 동안 아시아태평양이 바이오 PET 시장을 독점할 가능성이 높습니다.

바이오 PET 산업 개요

바이오 PET 시장은 부분적으로 통합되어 있습니다. 시장 점유율의 대부분은 소수의 진입 기업에 의해 분할되어 있습니다. 바이오 PET 시장의 주요 기업으로는 THE COCA-COLA COMPANY, Indorama Ventures Public Company Limited, Toyota Tsusho Corporation, TEIJIN LIMITED, TORAY INDUSTRIES INC. 등이 있습니다(순서에 관계없이).

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 패러다임 전환을 촉진하는 환경요인

- GHG(온실가스) 배출에 대한 우려 상승

- 기타 촉진요인

- 성장 억제요인

- PEF(폴리에틸렌 퓨라노에이트) 개발

- 저융점이 일부 용도에서의 사용을 저해

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 정도

제5장 시장 세분화(시장 규모(수량 기준))

- 용도

- 보틀

- 포장

- 내구소비재

- 가구

- 필름

- 기타

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 시장 점유율(%)**/순위 분석

- 주요 기업의 전략

- 기업 개요

- Toyota Tsusho Corporation

- Far Eastern New Century Corporation

- Indorama Ventures

- THE COCA-COLA COMPANY

- TORAY INDUSTRIES, INC.

- Plastipak Holdings, Inc.

- Ford Motors

- Gevo Inc.

- TEIJIN LIMITED

제7장 시장 기회와 향후 동향

- 재생에너지에 대한 주목

- 기타 기회

The Bio-PET Market size is estimated at 65.19 kilotons in 2025, and is expected to reach 80.00 kilotons by 2030, at a CAGR of 4.18% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

Key Highlights

- One of the major factors driving the market studied is the growing GHG (Greenhouse Gases) emission concerns.

- However, the development of PEF (Polyethylene Furanoate) and a low melting point of bio PET is likely to restrain the market.

- Environmental factors encouraging a paradigm shift will likely boost the demand for Bio-PET during the forecast period.

- Focus on renewable sources is likely to act as an opportunity for market growth in the future.

- Asia-Pacific dominated the market across the world, closely followed by North America. Asia-Pacific is likely to witness the highest growth rate during the forecast period.

Bio-Based PET Market Trends

Bottles Application to Dominate the Market

- Bio-PET is widely used in bottling applications. The demand for these is increasing rapidly worldwide as companies want to reduce their dependency on fossil-fuel-based products. In addition, the demand from consumers for bio-based products is also increasing.

- Bio-PET is a packaging material that helped advance the beverage industry by providing billions of people access to clean drinking water. The material offers safety and is lightweight, transparent, resealable, moldable, and 100% recyclable, with exceptional mechanical and barrier properties.

- Bio-PET is present in the market for many years. The plastic is made from 30% renewable and 70% petroleum-based raw materials. Bio-PET's mechanical and thermal properties are similar to other oil-based PET products, thus making it an ideal replacement for virgin PET.

- Bio-based PET (polyethylene terephthalate) is made from partially renewable raw materials. The benefits are clear. By using more renewable raw materials, fewer petroleum-based raw materials are required. Topics that consumers increasingly value and allow for differentiation. Bio-PET allows brand owners to highlight their position and draw attention to their products.

- As per the International Bottled Water Association (IBWA) reports, bottled water is the most consumed beverage product in the United States in terms of volume. A similar trend is being followed in the Asian-Pacific region, where the consumption of packaged drinking water is triggered in the past few years. Small-scale manufacturers flooded the market with vast production capacities for bottle production, thus positively supporting the bio-PET market.

- The bottle application will likely dominate the market due to the abovementioned reasons.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is home to half of the population in the world, and its consumption of PET bottles is high.

- This region is expected to play a prominent role in the growth of bio-PET usage, as it massively helps the wide-scale acceptance of bio-PET in multiple applications, like textile, packaging, etc.

- The high cost of bio-PET is a deterrent to its wide acceptance in this region due to the cost-conscious nature of the consumer.

- Major manufacturers are focusing on lowering the price of bio-PET, and the success in lowering the prices massively affects the market shift toward bio-PET.

- In Asia-Pacific, the demand for packaged food is growing, owing to lifestyle changes, the growing disposable income of people, the increasing number of working professionals, and the growing preference for fast food. Consumers prefer ready-to-consume foods because they require considerably less time for cooking, are fresh, and include attractive and sturdy packaging, supporting the demand for the market studied.

- China is the world's largest packaging consumer globally owing to factors such as growing per capita income and rising e-commerce giants in the country. Due to the steady growth of its FMCG and packaging industries, China accounts for the highest market share in the Asia-Pacific region.

- Furthermore, the Chinese packaging industry grew rapidly and consistently in recent years, owing to the expanding economy and rising middle class with greater purchasing power. Food packaging is a major player in the packaging industry, accounting for roughly 60% of the total market share in China. According to Interpak, in China, total packaging in the foodstuff packaging category is expected to reach 447 billion units in 2023, indicating an increased demand for the studied market from the packaging industry.

- India's packaging industry is the fifth-largest in the world, growing at about 22-25% per year, as per the Plastics Industry Association of India. Packaging and processing food costs can be 40% lower than in Europe because of highly skilled labor and cheap labor costs. The growing population and increasing demand for packaging are expected to drive the market.

- According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% between 2020 and 2025. Therefore, the Bio-PET market is expected to grow in the region.

- Hence, for the reasons above, Asia-Pacific will likely dominate the bio-PET market during the forecast period.

Bio-Based PET Industry Overview

The bio-PET market is partially consolidated. The majority of the market share is divided among a few players. Some of the key players in the bio-PET market include THE COCA-COLA COMPANY., Indorama Ventures Public Company Limited., Toyota Tsusho Corporation, TEIJIN LIMITED, and TORAY INDUSTRIES INC., among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Environmental Factors Encouraging a Paradigm Shift

- 4.1.2 Growing GHG (Greenhouse Gases) Emission Concerns

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Development of PEF (Polyethylene Furanoate)

- 4.2.2 Low Melting Point Hinders Usage in Some Applications

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Bottles

- 5.1.2 Packaging

- 5.1.3 Consumer Durables

- 5.1.4 Furniture

- 5.1.5 Films

- 5.1.6 Other Applications

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 France

- 5.2.3.3 United Kingdom

- 5.2.3.4 Italy

- 5.2.3.5 Rest of the Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Toyota Tsusho Corporation

- 6.4.2 Far Eastern New Century Corporation

- 6.4.3 Indorama Ventures

- 6.4.4 THE COCA-COLA COMPANY

- 6.4.5 TORAY INDUSTRIES, INC.

- 6.4.6 Plastipak Holdings, Inc.

- 6.4.7 Ford Motors

- 6.4.8 Gevo Inc.

- 6.4.9 TEIJIN LIMITED

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Focus toward Renewable Sources

- 7.2 Other Opportunities