|

시장보고서

상품코드

1640500

소매 분야 데스크톱 가상화 : 시장 점유율 분석, 업계 동향, 성장 예측(2025-2030년)Retail Desktop Virtualization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

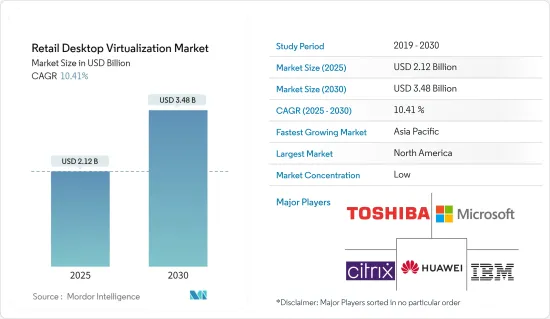

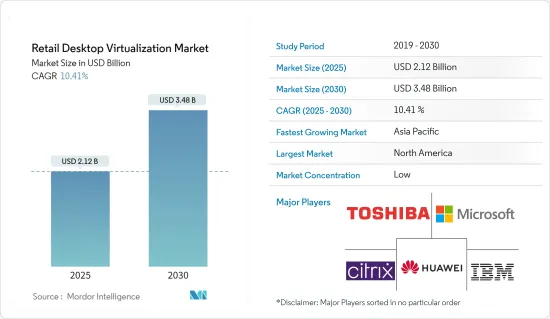

소매 분야 데스크톱 가상화 시장 규모는 2025년에 21억 2,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 10.41%로, 2030년에는 34억 8,000만 달러에 달할 것으로 예측됩니다.

소매 데스크톱 가상화 시장은 클라우드 컴퓨팅의 급속한 보급과 다양한 부문에서의 자동화의 진전에 의해 큰 견인력을 얻고 있습니다. 데스크톱 가상화는 중앙 집중식 서버에서 호스팅되는 가상 머신(VM) 내에서 데스크톱 OS를 실행하는 것으로, 유연성, 보안 및 비용 효율성 향상을 목표로 하는 기업에게 매우 중요한 솔루션이며 가상 데스크톱 인프라(VDI) 및 DaaS(Desktop-as-a-Service)와 같은 플랫폼을 통해 제공되는 경우가 많습니다.

산업 분석에 따르면 데스크톱 가상화는 특히 멀티클라우드 환경의 상승과 최종 사용자 컴퓨팅(EUC) 솔루션에 대한 수요가 증가함에 따라 최신 IT 인프라에 있어서 점점 더 중요해지고 있습니다. VM(Virtual Machine)과 SDDC(Software-Defined Data Center)도 이 상황에서 매우 중요한 역할을 하고 있으며 기업으로 하여금 가상 데스크톱을 효율적으로 배포할 수 있게 합니다. Citrix Systems, VMware, Microsoft 등 주요 기업들이 시장을 선도하는 가운데 하이퍼 컨버지드 인프라(HCI)와 씬 클라이언트에서 큰 혁신이 일어나고 있으며 이는 치열한 경쟁으로 이어지고 있습니다.

엔터프라이즈가 유연성과 원격 근무 기능을 계속 선호하는 동안 가상 데스크톱 배포에 대한 수요가 커질 것으로 예상됩니다. 시장 전망에서는 특히 데이터 보안 및 접근성이 가장 중시되는 산업에서 클라우드 데스크톱 채택이 꾸준히 증가하고 있습니다. 이러한 변화는 시장 세분화에도 반영되어 특히 북미 및 유럽과 같은 지역에서는 온프레미스 솔루션보다 클라우드 배포 솔루션에 대한 경향이 더 두드러집니다.

데스크톱 가상화를 촉진하는 클라우드 컴퓨팅의 역할

주요 하이라이트

- IT 인프라 변화 : 클라우드 컴퓨팅은 기존의 IT 인프라를 변화시켜 데스크톱 가상화를 모든 규모의 기업에게 실현 가능한 솔루션으로 만들었습니다. 클라우드 기반 서비스를 활용함으로써 기업은 가상 데스크톱을 보다 효율적으로 배포하고 대규모 물리 인프라의 필요성을 줄일 수 있습니다. 이 전환은 가상 데스크톱 인프라(VDI) 및 DaaS(Desktop-as-a-Service) 솔루션의 확장성을 실현하는데 큰 힘이 되고 있습니다. 클라우드 데스크톱이 제공하는 유연성을 통해 기업은 리소스를 동적으로 관리할 수 있으며, 이는 워크로드 분산 및 재해 복구가 중요한 멀티클라우드 환경에서 특히 유리합니다.

- 접근성 및 비용 효율성 향상 : 클라우드 컴퓨팅은 접근성과 비용 효율성 향상을 촉진하며 기업은 상당한 선행 투자 없이 원격 데스크톱 솔루션 및 애플리케이션 가상화를 지원할 수 있습니다. 가상 머신(VM)의 보급으로 기업은 위치에 관계없이 직원에게 가상 작업 공간에 대한 안전하고 일관된 액세스를 제공할 수 있습니다. 이 기능은 모빌리티와 데이터 보안이 최우선 순위인 오늘날의 '어디에서나 작업할 수 있는' 문화에 필수적입니다. 또한 클라우드 데스크톱은 기존 데스크톱 설정과 비교하여 관리 및 업데이트를 더 간편하게 하고 총 소유 비용(TCO)을 줄입니다.

소매업의 자동화가 가상화 수요를 뒷받침

주요 하이라이트

- 소매업무의 합리화 : 소매업에서의 자동화의 진전은 데스크톱 가상화 수요에 크게 기여하고 있습니다. 소매업에서는 업무의 합리화, 고객 경험의 향상, 공급사슬의 효율화를 목적으로 자동화 기술 도입이 진행되고 있습니다. 데스크톱 가상화는 여러 지점에서 애플리케이션, 인벤토리 시스템 및 고객 데이터를 관리하는 중앙 플랫폼을 제공함으로써 이러한 노력을 지원합니다. 소매업체는 원격 데스크톱 솔루션을 도입하여 업무 동기화를 보장하고 속도가 빠른 환경에서 필수적인 실시간 데이터 액세스 및 처리 기능을 제공합니다.

- 옴니채널 전략 지원 : 소매업체가 옴니채널 전략을 계속 개발함에 따라 물리적 플랫폼과 디지털 플랫폼을 원활하게 통합할 필요성이 두드러지고 있습니다. 데스크톱 가상화를 통해 소매 업체는 POS(판매 시점 정보 관리) 시스템에서 CRM(고객 관계 관리) 도구에 이르기까지 다양한 기능을 지원하는 통합 작업 공간을 구축할 수 있습니다. 이 통합은 채널 간에 일관된 고객 경험을 제공하는 데 필수적입니다. 또한, 가상 데스크톱 배포 증가로 소매 기업은 민감한 고객 정보를 다룰 때 필수적인 견고한 보안 프로토콜과 데이터 보호 대책을 유지할 수 있습니다.

소매 데스크톱 가상화 시장 동향

데스크톱 가상화에서 클라우드 배포의 등장

- 클라우드 배포 동향 : 클라우드 배포는 데스크톱 가상화 시장에서 매우 중요한 동향이 되고 있으며, 그 배경에는 비용 효율적이고 확장성이 뛰어나며 관리가 용이한 솔루션에 대한 요구가 있습니다. 가상 데스크톱 인프라(VDI)와 DaaS(Desktop as a Service)를 필두로 기존의 온프레미스형에서 클라우드 기반으로의 마이그레이션이 진행되고 있습니다. 이 마이그레이션을 통해 기업은 가상 데스크톱을 신속하게 배포할 수 있을 뿐만 아니라 초기 비용을 절감하고 유연성을 높일 수 있습니다. 멀티클라우드 환경 채택은 이러한 추세를 더욱 가속화하고 있습니다. 기업은 벤더 종속을 피하고 운영 탄력성을 강화하려고 노력하고 있으며, 다양한 클라우드 플랫폼에서 가상 머신(VM)의 보급을 촉진하고 있습니다.

- 클라우드 구축을 뒷받침하는 주요 요인 : 클라우드 컴퓨팅의 보급으로 데스크톱 가상화 상황이 변화하고 기업이 리소스를 보다 효율적으로 관리할 수 있게 되었습니다. 하이퍼 컨버지드 인프라(HCI)가 제공하는 컴퓨팅, 스토리지 및 네트워크 리소스의 원활한 통합은 클라우드 배포에 대한 선호도를 높이고 있습니다. 또한 SDDC(Software-Defined Data Centers)의 부상으로 기업은 가상화 워크로드를 쉽게 관리할 수 있어 운영 효율성이 크게 향상되었습니다. 결과적으로 IT 리소스를 최적화하기 위해 클라우드 데스크톱 솔루션을 채택하는 중소기업이 늘어나고 있으며 이는 시장 성장을 더욱 촉진하고 있습니다.

북미가 큰 점유율을 차지할 전망

- 세계 시장을 선도하는 북미 : 북미는 첨단 기술 인프라와 디지털 전환 전략의 높은 도입률로 인해 데스크톱 가상화 시장을 독점할 것으로 보입니다. 이 지역은 기술 혁신에 주력하고 있으며 신기술을 신속하게 통합할 수 있기 때문에 시장 성장의 중요한 거점으로 자리잡고 있습니다. 리모트 워크와 재택 근무 증가로 인한 리모트 데스크톱 솔루션 수요 증가가 이 우위성을 뒷받침하는 중요한 요인이 되고 있습니다. 이 지역의 기업이 VDI, DaaS, 클라우드 데스크톱 솔루션을 채택함에 따라 북미 시장 점유율이 크게 성장할 것으로 예상됩니다.

- 주요 기업으로서의 미국 : 북미 최대의 데스크톱 가상화 소비국인 미국은 이 지역 시장 리더로서 중요한 역할을 하고 있습니다. 미국에는 주요 클라우드 서비스 제공업체가 있으며 호스팅 서버의 수가 늘어나면서 클라우드 기반 데스크톱 가상화의 성장을 가속하고 있습니다. 게다가 캐나다에 가깝고 새로운 작업 공간에서 환경친화적인 실천이 중요하다는 점도 이 지역 시장 확대를 더욱 강화하고 있습니다. 이러한 지역 간의 상호 연결성은 데스크톱 가상화 솔루션의 광범위한 채택을 지원하고 북미 리더로서의 입지를 강화하고 있습니다.

소매 데스크톱 가상화 산업 개요

세분화된 시장 : 소매 데스크톱 가상화 시장은 매우 세분화되어 있으며 단일 기업이 압도적인 시장 점유율을 갖고 있지 않습니다. 이 세분화는 세계 대기업과 소규모 전문 기업 모두가 사업을 전개하는 경쟁 환경을 보여줍니다. 기본 가상화부터 복잡한 맞춤형 배포에 이르기까지 다양한 솔루션을 제공합니다.

다양한 접근 방식으로 시장을 선도하는 기업 데스크톱 가상화 시장의 선도 기업은 Citrix Systems Inc., Toshiba Corporation, Red Hat Inc., IBM Corporation, Huawei Technologies, Microsoft Corporation 등입니다. 이러한 기업들은 강력한 세계적 존재감, 광범위한 제품 포트폴리오, 지속적인 혁신을 통해 두드러집니다. Citrix와 Microsoft는 종합적인 가상화 플랫폼에서 특히 주목을 받고 있으며, Red Hat(IBM 산하)과 Huawei는 오픈소스와 클라우드 기반 솔루션의 통합에 주력하고 있습니다. Toshiba Corporation의 존재 또한 틈새 시장을 형성하여 특정 산업의 요구를 충족시키고 있습니다.

혁신과 통합을 바탕으로 한 향후 성공 전략 : 데스크톱 가상화 시장의 주요 동향으로는 클라우드 기반 솔루션, 보안 강화, 기존 IT 인프라와의 원활한 통합에 대한 수요 증가를 들 수 있습니다. 시장 진출 기업이 성공을 거두기 위해서는 이러한 부문에 주력하고 변화하는 기업의 요구를 충족시킬 수 있는 유연하고 안전한 솔루션을 제공해야 합니다. 지속적인 혁신, 전략적 파트너십 및 서비스 제공의 확대가 이 세분화된 시장에서 경쟁을 유지하기 위한 중요한 전략이 될 수 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요(COVID-19의 영향 포함)

- 산업의 매력 - Porter's Five Forces 분석

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 역학

- 촉진요인

- 클라우드 컴퓨팅 도입 확대

- 소매 분야 자동화의 성장

- 억제요인

- 인프라 도입의 제약

제6장 시장 세분화

- 데스크톱 전송 플랫폼별

- 호스트형 가상 데스크톱(HVD)

- 호스트형 공유 데스크톱(HSD)

- 도입 형태별

- 온프레미스

- 클라우드

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Citrix Systems Inc.

- Toshiba Corporation

- Red Hat Inc.(IBM Corporation)

- Huawei Technologies Co. Ltd.

- Microsoft Corporation

- Parallels International GmbH

- Dell Inc.

- Ncomputing, Inc.

- Ericom Software Inc.

- Tems, Inc

- Vmware Inc.

제8장 투자 분석

제9장 시장의 미래

CSM 25.02.13The Retail Desktop Virtualization Market size is estimated at USD 2.12 billion in 2025, and is expected to reach USD 3.48 billion by 2030, at a CAGR of 10.41% during the forecast period (2025-2030).

The desktop virtualization market has gained significant traction, driven by the rapid adoption of cloud computing and increasing automation across various sectors. Desktop virtualization, which involves running a desktop operating system within a virtual machine (VM) hosted on a centralized server, has become a crucial solution for businesses aiming to enhance flexibility, security, and cost efficiency. This technology, often delivered through platforms like Virtual Desktop Infrastructure (VDI) or Desktop as a Service (DaaS), enables remote desktop solutions and application virtualization, fostering a seamless virtual workspace.

Industry analysis reveals that desktop virtualization is becoming increasingly integral to modern IT infrastructures, especially with the rise of multi-cloud environments and the growing demand for end-user computing (EUC) solutions. Virtual machines (VMs) and software-defined data centers (SDDCs) are also playing a pivotal role in this landscape, enabling organizations to deploy virtual desktops efficiently. With companies like Citrix Systems Inc., VMware Inc., and Microsoft Corporation leading the market, the competition is intense, with significant innovation occurring in hyper-converged infrastructure (HCI) and thin clients.

As businesses continue to prioritize flexibility and remote work capabilities, the demand for virtual desktop deployment is expected to grow. The market outlook suggests a steady rise in the adoption of cloud desktops, particularly in industries where data security and accessibility are paramount. This shift is reflected in the market's segmentation, with a noticeable trend towards cloud deployment modes over on-premise solutions, particularly in regions like North America and Europe.

Cloud Computing's Role in Driving Desktop Virtualization

Key Highlights

- Transformation of IT Infrastructure: Cloud computing has transformed traditional IT infrastructures, making desktop virtualization a feasible solution for businesses of all sizes. By leveraging cloud-based services, companies can deploy virtual desktops more efficiently, reducing the need for extensive physical infrastructure. This shift has been instrumental in enabling the scalability of virtual desktop infrastructure (VDI) and Desktop as a Service (DaaS) solutions. The flexibility offered by cloud desktops allows organizations to manage resources dynamically, which is particularly advantageous in multi-cloud environments where workload distribution and disaster recovery are critical.

- Enhanced Accessibility and Cost Efficiency: Cloud computing facilitates greater accessibility and cost efficiency, enabling organizations to support remote desktop solutions and application virtualization without significant upfront investment. With the proliferation of virtual machines (VMs), businesses can provide employees with secure and consistent access to virtual workspaces, regardless of location. This capability is essential in today's work-from-anywhere culture, where mobility and data security are top priorities. Moreover, cloud desktops allow for more straightforward management and updates, which reduces the total cost of ownership (TCO) compared to traditional desktop setups.

Automation in Retail Boosting Virtualization Demand

Key Highlights

- Streamlining Retail Operations: The growth in automation within the retail sector is significantly contributing to the demand for desktop virtualization. Retailers are increasingly adopting automation technologies to streamline operations, enhance customer experience, and improve supply chain efficiency. Desktop virtualization supports these efforts by providing a centralized platform for managing applications, inventory systems, and customer data across multiple locations. By implementing remote desktop solutions, retailers can ensure that their operations are synchronized, with real-time data access and processing capabilities that are critical in a fast-paced environment.

- Supporting Omnichannel Strategies: As retailers continue to develop omnichannel strategies, the need for seamless integration across physical and digital platforms becomes more pronounced. Desktop virtualization enables retailers to create a unified workspace that supports various functions, from point-of-sale (POS) systems to customer relationship management (CRM) tools. This integration is vital for delivering a consistent customer experience across channels. Additionally, with the rise of virtual desktop deployment, retailers can maintain robust security protocols and data protection measures, which are essential in handling sensitive customer information.

Retail Desktop Virtualization Market Trends

The Rise of Cloud Deployment in Desktop Virtualization

- Cloud Deployment Trends: Cloud deployment has become a pivotal trend in the desktop virtualization market, driven by the need for cost-effective, scalable, and easily managed solutions. Businesses are increasingly transitioning from traditional on-premise setups to cloud-based models, with Virtual Desktop Infrastructure (VDI) and Desktop as a Service (DaaS) leading the way. This shift allows companies to deploy virtual desktops swiftly while reducing upfront costs and enhancing flexibility. The adoption of multi-cloud environments is further accelerating this trend, as businesses seek to avoid vendor lock-in and enhance operational resilience, driving the proliferation of virtual machines (VMs) across various cloud platforms.

- Key Factors Boosting Cloud Deployment: The widespread adoption of cloud computing is transforming the desktop virtualization landscape, offering organizations the ability to manage resources more efficiently. The growing preference for cloud deployment is due to the seamless integration of computing, storage, and networking resources provided by hyper-converged infrastructure (HCI). Additionally, the rise of Software-Defined Data Centers (SDDCs) is making it easier for enterprises to manage virtualized workloads, significantly improving operational efficiency. As a result, small to medium-sized enterprises (SMEs) are increasingly embracing cloud desktop solutions to optimize their IT resources, further driving market growth.

North America is Expected to Hold Major Share

- North America Leading the Global Market: North America is set to dominate the desktop virtualization market, driven by its advanced technological infrastructure and high adoption rates of digital transformation strategies. The region's strong focus on innovation and its ability to rapidly integrate new technologies have positioned it as a critical hub for market growth. The increasing demand for remote desktop solutions, fueled by the rise in remote work and telecommuting, is a key factor supporting this dominance. As businesses across the region adopt VDI, DaaS, and cloud desktop solutions, North America's market share is expected to grow significantly.

- United States as a Key Player: The United States, as the largest consumer of desktop virtualization in North America, plays a crucial role in the region's market leadership. The presence of major cloud service providers and an increasing number of hosted servers in the U.S. are driving the growth of cloud-based desktop virtualization. Additionally, the proximity to Canada and the emphasis on eco-friendly practices in new workspaces are further bolstering the market's expansion across the region. This regional interconnectivity supports the broader adoption of desktop virtualization solutions, reinforcing North America's leadership position.

Retail Desktop Virtualization Industry Overview

Highly Fragmented Market: The desktop virtualization market is highly fragmented, with no single company holding a dominant market share. This fragmentation indicates a competitive environment where both large global corporations and smaller specialized companies operate. The market's nature reflects the diversity of end-user needs, with players offering a wide range of solutions from basic virtualization to complex, customized deployments.

Market Leaders with Diverse Approaches: The leading players in the desktop virtualization market include Citrix Systems Inc., Toshiba Corporation, Red Hat Inc. (IBM Corporation), Huawei Technologies Co. Ltd., and Microsoft Corporation. These companies are distinguished by their strong global presence, extensive product portfolios, and continuous innovation. Citrix and Microsoft are particularly noted for their comprehensive virtualization platforms, while Red Hat (under IBM) and Huawei focus on integrating open-source and cloud-based solutions. Toshiba's presence is more niche, catering to specific industry needs.

Future Success Strategies Revolve Around Innovation and Integration: Key trends in the desktop virtualization market include the growing demand for cloud-based solutions, security enhancements, and seamless integration with existing IT infrastructures. For market players to succeed, they must focus on these areas, providing flexible and secure solutions that can adapt to the changing needs of businesses. Continuous innovation, strategic partnerships, and expanding service offerings will be crucial strategies for staying competitive in this fragmented market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview ( Includes the Impact due to COVID-19)

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Cloud Computing

- 5.1.2 Growth in Automation in Retail

- 5.2 Market Restraints

- 5.2.1 Infrastructure Deployment Constraints

6 MARKET SEGMENTATION

- 6.1 By Desktop delivery platform

- 6.1.1 Hosted Virtual Desktop (HVD)

- 6.1.2 Hosted Shared Desktop (HSD)

- 6.2 By Deployment Mode

- 6.2.1 On-premise

- 6.2.2 Cloud

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Citrix Systems Inc.

- 7.1.2 Toshiba Corporation

- 7.1.3 Red Hat Inc. (IBM Corporation )

- 7.1.4 Huawei Technologies Co. Ltd.

- 7.1.5 Microsoft Corporation

- 7.1.6 Parallels International GmbH

- 7.1.7 Dell Inc.

- 7.1.8 Ncomputing, Inc.

- 7.1.9 Ericom Software Inc.

- 7.1.10 Tems, Inc

- 7.1.11 Vmware Inc.