|

시장보고서

상품코드

1683166

북미의 종자 처리 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)North America Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

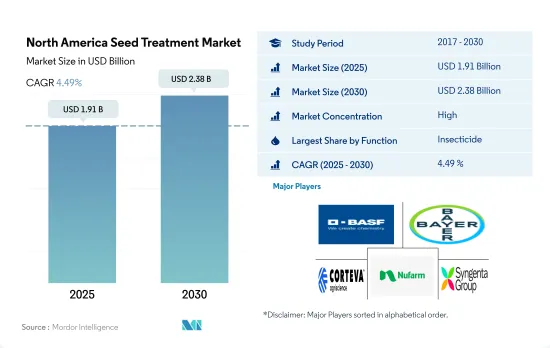

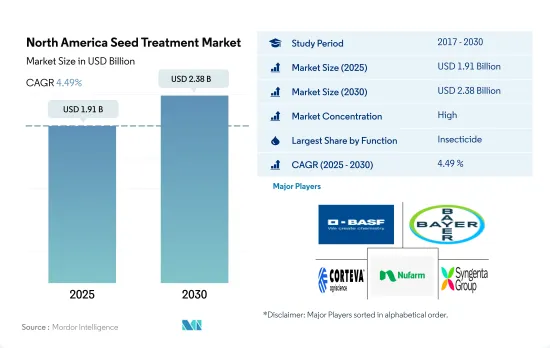

북미의 종자 처리 시장 규모는 2025년 19억 1,000만 달러로 추정되고, 2030년에는 23억 8,000만 달러에 이를 전망이며, 예측 기간 2025년부터 2030년까지의 CAGR은 4.49%를 나타낼 것으로 예측됩니다.

건전한 모종의 보호와 정착에서 종자 적용 기술의 이점에 대한 인식 증가가 시장을 뒷받침하고 있습니다.

- 북미의 종자 처리 산업은 현저한 성장을 이루고 있습니다. 시장 규모는 2020년에 비해 2022년에는 9.8% 증가했습니다. 이 성장의 원동력은 건강한 모종의 보호와 정착에서 종자 적용 기술의 이점에 대한 인식 증가와 전반적인 생산성 향상의 필요성입니다.

- 미국과 캐나다는 다양한 균류 병해와 해충으로부터 작물을 보호하기 위해 종자 처리제를 널리 사용하는 주요 농업 국가입니다. 이 두 국가는 이 지역에서 종자 처리의 큰 시장 점유율을 차지합니다. 미국은 이 지역 시장액의 약 82.6%를 차지하고 캐나다는 시장 점유율의 약 3.7%를 차지하고 있습니다.

- 중요한 초기 성장 기간 동안 병해충과 불확실한 토양 조건에 대한 고급 보호 기능을 갖춘 종자 처리 제품을 사용할 수 있으므로 효과가 향상되고 소비가 촉진되고 시장 성장에 기여합니다.

- 종자 처리 시장은 2023년부터 2029년까지 예측 기간 동안 36.2%의 성장이 예상됩니다. 이 성장의 주요 요인은 인구 증가의 요구를 충족시키기 위해 식량 생산 수요 증가입니다. 작물의 수율을 최적화하고 질병과 해충으로 인한 손실을 최소화하기 위해 농업 종사자들은 점점 종자 처리를 채택하고 있으며, 이는 묘목의 활력과 작물 전체의 생산성을 향상시키는 데 중요한 역할을 합니다.

- 따라서 종자 처리의 장점에 대한 의식이 높아지고, 혁신적인 제품의 이용가능성, 종자 처리 채용률의 상승은 예측기간 동안 시장의 성장을 가속할 것으로 예상됩니다.

농업 종사자는 작물의 건강 증진에서 종자 처리의 가치를 인식하게 되어, 이것이 시장의 확대로 이어지고 있습니다.

- 북미의 종자 처리 시장은 농업 종사자가 작물의 건강과 생산성 향상에 있어서 종자 처리의 가치를 인식하게 되어 종자 처리 소비가 증가하고 급속히 확대되고 있습니다.

- 종자 처리 시장은 광범위한 작물을 포함합니다. 그 중에서도 곡물 및 곡류는 2022년 시장 점유율의 43.8%를 차지했습니다. 병해충 발생률의 상승이 이러한 작물에 악영향을 미치고 있으며, 이것이 곡물 및 곡류에 있어서의 종자 처리제의 채용을 촉진하고 있습니다.

- 미국은 북미 최대의 종자 처리 시장으로 2022년에는 82.6%의 점유율을 차지했습니다. 이 나라는 식량안보에 대한 수요 증가와 종자처리 제품 채용 증가 등의 요인에 의해 대폭적인 성장을 이루고 있습니다.

- 이 지역 시장액은 2017년부터 2022년까지 30.8% 증가했습니다. 지속 가능한 농업 추진과 식량 증산을 목표로 한 정부의 이니셔티브는 미국과 캐나다를 중심으로 지역의 종자 처리 시장을 밀어 올렸습니다. 예를 들어, 국립식량농업실(NIFA)은 자금제작 이니셔티브를 통해 지속가능한 농업 추진에 중요한 역할을 했습니다. 그 중 하나가 지속 가능 농업 조사 및 교육(SARE) 프로그램으로 농업 종사자, 생산자, 농촌 커뮤니티를 크게 지원해 왔습니다.

- 종자 처리 시장의 성장에 기여하는 또 다른 요인은 지속 가능한 농업 관행의 확대입니다. 종자 처리는 병해충에 대한 표적을 좁힌 보호를 제공하므로 광범위한 살충제에 대한 의존성을 줄이고 환경에 미치는 영향을 최소화할 수 있습니다.

- 따라서 예측기간 중 2023년부터 2029년까지 이 시장의 CAGR은 4.8%를 나타낼 것으로 예상됩니다.

북미의 종자 처리 시장 동향

토양 전염성 병해와 선충에 의한 주요 작물의 작물 손실 증가로 인해 더 높은 용량의 종자 처리제의 사용이 필요합니다.

- 북미에서는 헥타르당 종자 처리제 소비량이 현저히 증가했으며, 2017년 수치와 비교하여 2022년에는 53g 증가를 기록했습니다. 이 소비량의 상당한 성장은 이 지역의 농업 관행에 영향을 미치는 몇 가지 요인에 기인합니다. 중요한 요인 중 하나는 기후 변화의 영향이기 때문에 기상 패턴이 변화하고 농업 종사자에게 새로운 과제가 나타났습니다. 이러한 변화의 결과로서, 작물의 건강 상태나 수율에 대한 예측 불가능한 날씨의 악영향을 경감하기 위한, 효과적인 종자 처리 제품에 대한 요구가 높아지고 있습니다.

- 게다가, 곰팡이와 선충의 만연이 농작물에 큰 위협이 되고 있으며, 식물의 건강을 지키고 최적의 수율을 확보하기 위해 보다 높은 살포율로 종자 처리제를 사용할 필요가 발생하고 있습니다.

- 종자 처리제 소비량 증가는 북미 농업 상황의 변화에 대한 대응입니다. 농업 종사자는 예방 조치로 종자 처리 솔루션을 적극적으로 채택하고 있습니다. 이 지역의 주요 농업국인 미국과 캐나다는 현재 식물 기생성 선충, 토양 전염성 병해 및 기타 다양한 해충이 초래하는 심각한 과제를 다루고 있습니다.

- 콩, 옥수수, 면화, 옥수수는 이 지역에서 재배되는 주요 작물이지만 다양한 선충류와 토양 전염성 병해로 인한 큰 과제를 겪고 있습니다. 이러한 과제는 근립선충, 뿌리썩음병, 후사리움종, 곡류시스트선충, 콩시스트선충, 리조토니아, 피슘종, 호모병, 묘립고병 등을 포함합니다. 이러한 병해와 선충에 의한 처리가 증가하고 있기 때문에 보다 고용량의 종자 처리제가 필요합니다.

종자 처리에 대한 수요 증가는 유효 성분의 가격을 올릴 것으로 예상됩니다.

- 북미에서 일반적으로 사용되는 종자 처리제의 활성 성분은 시페르메트린, 메탈락실, 말라티온, 아바멕틴, 아조시스트로빈 등을 포함합니다. 종자 처리는 종자 파종시 방어층을 형성하여 종자와 유묘를 병해충으로부터 초기 보호합니다. 이 보호 장벽은 씨앗이 토양에서 성장을 시작할 때 잠재적인 해로부터 씨앗을 보호합니다.

- 살충제로서의 Cypermethrin은 주로 처리된 씨앗과 식물의 표면에 머물며 광범위한 해충에 대한 신속한 넉다운 작용을 위한 보호 장벽을 형성하였습니다. 그 가격은 2022년에 톤당 2만 1,000달러에 달했습니다. 시펠 메트린의 작용기전은 곤충의 신경계를 혼란시키고 마비를 일으키고 결국 죽음을 초래합니다.

- 말라티온의 전신작용에 의해 진딧물, 대양벌레, 엉겅퀴벌레, 비늘벌레, 특정 벌레 등 폭넓은 해충의 제거에 성공했습니다. 2022년 가격은 톤당 12만 4,000달러였습니다. 말라티온은 곤충의 신경 기능에 필수적인 효소인 아세틸 콜린 에스테라아제를 억제하고 곤충을 무력화시킵니다.

- 아바멕틴은 이버멕틴 시스템에 속하며 선충에 대해 높은 고유 활성을 가지고 있습니다. 옥수수, 콩, 면화의 생산에서 뿌리를 공격하는 선충으로부터 어린 식물을 보호하는 데 사용됩니다. 2022년 가격은 톤당 8,800달러였습니다.

- 메탈락실을 종자 처리제로 살포함으로써, 농업 종사자는 식물의 수명주기의 시작부터 병해 문제를 적극적으로 대처할 수 있습니다. 이 조기 개입은 보다 건강하고 활력 있는 묘목을 보장하고 작물 수율을 향상시킵니다. Metalaxyl의 2022년 가격은 톤당 4,400달러였습니다.

북미의 종자 처리 산업 개요

북미의 종자 처리 시장은 상당히 통합되어 있으며 상위 5개사에서 76.44%를 차지하고 있습니다. 이 시장의 주요 기업은 BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd, Syngenta Group입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 농약 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 캐나다

- 멕시코

- 미국

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 기능별

- 살균제

- 살충제

- 살선충제

- 작물 유형별

- 상업 작물

- 과일 및 야채

- 곡물

- 콩류 및 지방종자

- 잔디 및 관상용

- 국가별

- 캐나다

- 멕시코

- 미국

- 기타 북미

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- Albaugh LLC

- BASF SE

- Bayer AG

- Corteva Agriscience

- Nufarm Ltd

- Sharda Cropchem Limited

- Syngenta Group

- Upl Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The North America Seed Treatment Market size is estimated at 1.91 billion USD in 2025, and is expected to reach 2.38 billion USD by 2030, growing at a CAGR of 4.49% during the forecast period (2025-2030).

The market is fueled by increasing awareness of the benefits of seed-applied technologies in protecting and establishing healthy seedlings

- The seed treatment industry in North America is experiencing significant growth. The market value increased by 9.8% in 2022 compared to 2020. This growth is driven by growing awareness of the benefits of seed-applied technologies in protecting and establishing healthy seedlings and the need to improve overall productivity.

- The United States and Canada are leading agricultural nations that extensively use seed treatment chemicals to safeguard their crops against various fungal diseases and pests. These two countries hold a significant market share for seed treatments in the region. The United States constitutes approximately 82.6% of the regional market value, while Canada contributes around 3.7% of the market share.

- The availability of seed treatment products with advanced protection against pests, disease, and uncertain soil conditions during the critical early growth period results in improved effectiveness, which drives consumption, thereby contributing to the growth of the market.

- The seed treatment market is expected to witness a growth of 36.2% during the forecast period of 2023-2029. This growth is primarily driven by the rising demand for food production to meet the needs of a growing population. In order to optimize crop yields and minimize losses due to diseases and pests, farmers are increasingly adopting seed treatment, which plays a crucial role in improving seedling vigor and overall crop productivity.

- Therefore, growing awareness about the benefits of seed treatment, the availability of innovative products, and the rising adoption rate of seed treatment are expected to fuel the growth of the market during the forecast period.

Farmers are increasingly recognizing the value of seed treatments in improving crop health, which is leading to the expansion of the market

- The North American seed treatment market is expanding rapidly due to the rising consumption of seed treatment as farmers increasingly recognize the value of seed treatments in improving crop health and productivity.

- The seed treatment market includes a wide range of crops. Among all, grains and cereals accounted for 43.8% of market share in 2022. The rising incidence of pests and diseases is negatively affecting these crops, which is driving the adoption of seed treatments in grains and cereals.

- The United States is the largest seed treatment market in North America, accounting for a share of 82.6% in 2022. The country has been witnessing substantial growth driven by factors such as increasing demand for food security and rising adoption of seed treatment products.

- The market value increased in the region by 30.8% between 2017 and 2022. Government initiatives aimed at promoting sustainable agriculture and increasing food production boosted the seed treatment market in the region, mainly in the United States and Canada. For instance, the National Institute of Food and Agriculture (NIFA), through its funding initiatives, played a crucial role in advancing sustainable agriculture. One such program is the Sustainable Agriculture Research and Education (SARE) program, which has significantly supported farmers, growers, and rural communities.

- Another factor contributing to the growth of the seed treatment market is the growing sustainable agricultural practices. Seed treatments offer targeted protection against pests and diseases, reducing the reliance on broad-spectrum pesticides and minimizing the environmental impact.

- Therefore, the market is expected to register a CAGR of 4.8% during the forecast period (2023-2029).

North America Seed Treatment Market Trends

Increased crop losses in major crops due to soilborne diseases and nematodes necessitate the use of seed treatments with higher dosages

- North America experienced a noteworthy upsurge in seed treatment consumption per hectare, with a recorded increase of 53 grams in 2022 compared to the figures from 2017. This substantial growth in consumption can be attributed to several factors that have influenced agricultural practices in the region. One significant factor is the impact of climate changes, which have resulted in shifts in weather patterns and the emergence of new challenges for farmers. As a consequence of these changes, there has been a greater need for effective seed treatment products to mitigate the adverse effects of unpredictable weather on crop health and yield.

- Additionally, the rise in fungal and nematode infestations has posed significant threats to crops, necessitating the use of seed treatments at higher application rates to safeguard plant health and ensure optimal yields.

- The increase in seed treatment consumption is a response to the changing agricultural landscape in North America. Farmers are proactively adopting seed treatment solutions as a precautionary measure. The United States and Canada, as major agricultural countries in the region, are currently grappling with significant challenges posed by plant parasitic nematodes, soil-borne diseases, and various other insect pests.

- Soybeans, maize, cotton, and corn are the prominent crops grown in the region, but they encounter significant challenges from various nematodes and soilborne diseases. These challenges include root-lesion nematodes, root rots, fusarium species, cereal cyst nematodes, soybean cyst nematodes, rhizoctonia, pythium species, phomosis, seedling blights, and others. The increasing damage by these diseases and nematodes necessitates the seed treatment application method with higher dosages.

The growing demand for Seed treatment is anticipated to fuel the prices of the active ingredients.

- In North America, commonly utilized active ingredients for seed treatment chemicals include cypermethrin, metalaxyl, malathion, abamectin, and azoxystrobin. Seed treatment offers initial protection to seeds and young plants from pests and diseases by establishing a defensive layer upon seed sowing. This protective barrier shields the seed from potential harm as it begins its growth in the soil.

- Cypermethrin, as an insecticide, remained primarily on the surface of treated seeds or plants, forming a protective barrier for quick knockdown action against a wide range of insect pests. Its price stood at USD 21.0 thousand per metric ton in 2022. The mode of action of Cypermethrin involves disrupting the nervous systems of insects, leading to paralysis and, ultimately, their death.

- Malathion's systemic effect allowed for the successful management of a wide range of insect pests, such as aphids, leafhoppers, thrips, scales, and specific caterpillar types. It was priced at USD 124 thousand per metric ton in 2022. Malathion inhibits acetylcholinesterase, a vital enzyme for nerve function in insects, leading to their incapacitation.

- Abamectin belongs to the Ivermectin chemical class and has high intrinsic activity against nematodes. It is used to protect young plants from the root-attacking nematodes in corn, soybeans, and cotton production. It was priced at USD 8.8 thousand per metric ton in 2022.

- By applying metalaxyl as a seed treatment, farmers can proactively address disease issues right from the start of the plant's life cycle. This early intervention helps ensure healthier and more vigorous seedling establishment, which can lead to improved crop yields. Metalaxyl was priced at USD 4.4 thousand per metric ton in 2022.

North America Seed Treatment Industry Overview

The North America Seed Treatment Market is fairly consolidated, with the top five companies occupying 76.44%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Insecticide

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Albaugh LLC

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Nufarm Ltd

- 6.4.6 Sharda Cropchem Limited

- 6.4.7 Syngenta Group

- 6.4.8 Upl Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록