|

시장보고서

상품코드

1852043

유럽의 체외진단 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe In-Vitro Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

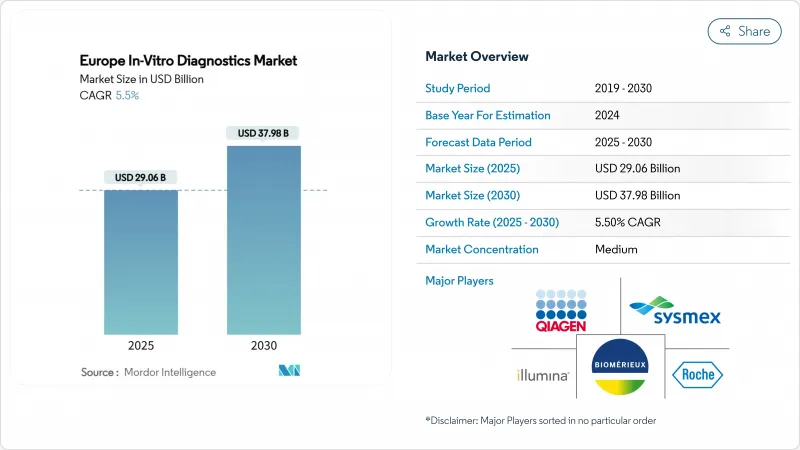

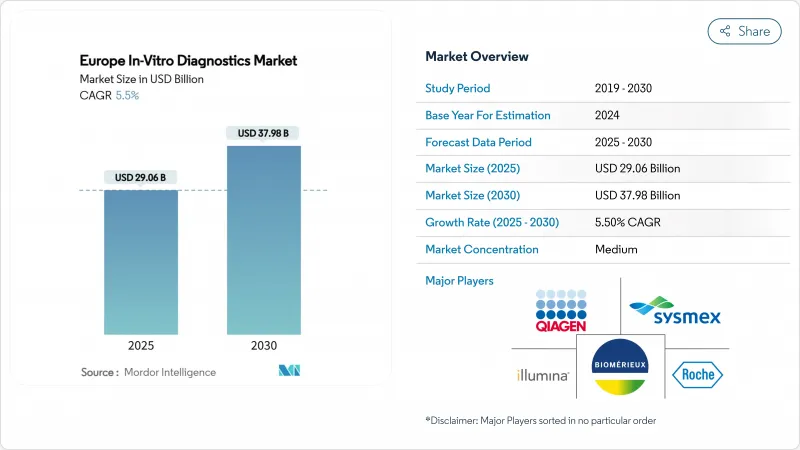

유럽의 체외진단 시장은 2025년에 290억 6,000만 달러로 추정되고, 2030년에는 379억 8,000만 달러에 이를 것으로 예측됩니다.

이 궤도는 이 지역에 첨단 검사 플랫폼의 급속한 보급, 만성 질환의 조기 발견 추진, EU IVDR에 의한 규제 완화를 부각하고 있습니다. 독일의 첨단 헬스케어 인프라, 영국의 디지털 혁신 의제, 포인트 오브 케어 모델로의 강한 이동은 공급업체에게 명확한 확대 노선을 제공합니다. 분자 기술은 전문 시설에서 주류 의료 경로로 이동하고 있으며, 면역 진단 약물은 일상 분석 및 스크리닝의 주요 제품으로 계속되고 있습니다. 소모품은 경상 수익의 기둥이며, 비침습적인 시료 유형은 환자에 대한 접근을 넓히고 있습니다.

유럽의 체외진단 시장 동향 및 인사이트

만성 질환 및 감염의 부담이 조기 진단 수요 증가

다질환 합병증 증가는 입원 환자의 치료 결정에 있어서 거의 70%가 이미 정확한 검사 증거에 의존하고 있음을 의미합니다. 종양학과 심혈관 경로는 현재 바이오마커 패널을 통합하여 위험을 계층화하고 치료하기 위한 지침으로 삼고 있습니다. 대략 5,000만 명의 유럽인이 여러 만성 질환을 앓고 있으며, 한 시료에서 여러 분석물을 다루는 멀티플렉스 검사에 대한 수요가 증가하고 있습니다. 팬데믹 후 모니터링 예산은 2020년 이전의 벤치마크보다 높은 수준을 유지하며, 실험실은 감염성 검사 능력의 확장을 유지할 수 있습니다. 보건부는 검사에 대한 접근성 확대를 범용 커버 목표의 전제조건으로 간주하여 1차 케어 수준에서 높은 처리량 플랫폼과 환자에 가까운 장비 조달을 추진하고 있습니다.

1차 케어 네트워크에서 POC 검사 채택

분산형 장치는 가정 의료 현장에서 진단의 소요 시간을 단축하고 있습니다. 영국의 비용 최소화 연구는 NHS 건강 진단에서 포인트 오브 케어 분석 장치를 사용한 경우, 스크리닝을 받은 환자 100명당 29파운드를 절약할 수 있음을 보여줍니다. 유럽 소아과 의사들은 국가별로 큰 차이가 있다고 보고했으나, 1차 케어에서 소변 검사봉의 이용률은 조사 대상 국가의 3분의 2에서 80%를 초과했습니다. 새로운 장비에 내장된 머신러닝 펌웨어는 저농도 타겟에 대한 감도를 높이고 핵심 실험실에 필적하는 정밀도의 멀티 마커 카드를 가능하게 합니다. 이러한 장점은 특히 만성 질환의 후속 조치에서 지불자에게 받아들여지고 있습니다.

EU IVDR의 긴 규제 일정 및 규정 준수 비용

Association for Molecular Pathology의 보고에 따르면, 유럽 검사 시설의 73%는 IVDR의 의무를 완전히 명확히 하지 않았다고 합니다. 신흥 기업은 법적 절차 및 생물통계학적 연구 비용이 부담되어, 신흥 병원체와 희소질환의 신규 검사가 지연되고 있습니다. 유럽 위원회는 단계적 기한을 인정했지만 인증이 지연되면 병원 공급망이 혼란스러울 수 있습니다.

부문 분석

유럽의 체외진단용 의약품 시장 규모는 호르몬, 감염증, 자가면역 패널에서의 역할을 반영하여 2024년 매출 점유율이 27%가 되었습니다. 고감도 화학 발광 분석은 견조한 판매량을 유지하면서 COVID-19에 대한 투자로 장비 그룹을 지속적으로 업그레이드하고 있습니다. 2030년까지 연평균 복합 성장률(CAGR)이 가장 높은 것은 분자진단제로, 7.2%로 예상되며, 이는 시퀀싱 비용의 저하 및 컴패니언 테스트의 보급이 뒷받침되고 있습니다. 현재 유럽 유전체 검사의 대부분은 종양학이 차지하고 있는데, 호흡기 병원체, 성 감염증, 항균제 스튜어드십을 위한 래피드 사이클 PCR 플랫폼이 대응 가능한 기반을 넓히고 있습니다. AI 중심의 변형 호출 소프트웨어는 분석의 신뢰성을 높이고 보고 시간을 단축합니다.

루틴의 임상 화학은 전해질과 대사의 스크리닝의 기초이며 지속적인 분석 장비의 자동화에 지원됩니다. 혈액학은 전혈구 수를 풍부한 진단 출력으로 바꾸는 디지털 형태학과 통합 응고 모듈로부터 이익을 얻습니다. 한편, 미생물학 워크플로우는 MALDI-TOF와 신드로믹 패널을 통합하여 병원체의 동정과 치료 지침을 가속화합니다. 이러한 검사 범주가 미들웨어를 통해 얽혀 있어 임상의는 적은 검체로부터 종합적인 견해를 얻을 수 있어 유럽의 체외진단 시장 전체에서 효율적인 환자 중심의 치료 추진에 대응할 수 있습니다.

시약 및 소모품은 2024년 매출의 65%를 차지했고, 현금 흐름을 안정시키며 전환 장벽을 높이는 면도날과 같은 경제성을 실증하고 있습니다. 국가 입찰에서 일괄 구매 계약은 기존 기업에 유리하지만 품질 관리 조항은 디지털 추적성 기능을 중시합니다. 분석기는 화학과 면역분석의 모달리티 사이에서 유연한 개방형 채널 아키텍처로 전환하는 경향이 있으며, 실험실이 분석기의 가동 시간을 극대화하는 데 도움이 됩니다. 미들웨어 대시보드는 품질 관리 플래그와 사용 상황을 분석하고 분석기 단위 판매보다 종합적인 플랫폼 거래로 조달을 유도하고 있습니다.

소프트웨어 및 서비스 부문은 규모는 작지만 8.5%의 급확대가 예측되고 있습니다. 실험실은 LIS 통합, AI 결과 해석, 규제 문서 작성 모듈 구독 요금을 지불하는 경향이 커지고 있습니다. 공급업체는 기업의 성능을 벤치마킹하고 외부 품질 평가를 자동화하는 클라우드 기반 애널리틱스를 수익화하고 있습니다. 이 피벗은 핵심 분석 감도 향상이 기술적 한계에 가까워지고 있는 지금 디지털 차별화가 진행되고 유럽의 체외진단 업계에서 경쟁력이 유지되고 있습니다.

디스포저블 디바이스는 2024년에 58%의 매출 점유율을 차지하였고, CAGR 6.9%로 성장이 예측되고 있습니다. 단일 사용 카트리지는 폴리 클리닉의 감염 관리를 보호하고 가정 검사의 편의성을 지원합니다. 래터럴 플로우 스트립은 현재 C-반응성 단백질, 심근 트로포닌, 비타민 D 검정을 커버하고, 마이크로플루이딕스 칩은 최소한의 사용자 단계로 멀티플렉스 패널을 탑재하고 있습니다. 환경 문제에 대한 고려를 통해 공급업체는 생분해성 케이싱의 도입과 플라스틱 폐기물을 줄이기 위한 인수 프로그램의 도입에 박차를 가하고 있습니다.

재사용 가능한 장비는 연간 샘플량이 설비 투자를 정당화하는 높은 처리량의 중앙 실험실 워크플로우를 지배합니다. 업그레이드는 산책로 자동화, 셀프 클리닝 모듈 및 소모품 지출을 억제하는 시약 데드 볼륨의 감소에 중점을 둡니다. 하이브리드 아키텍처는 재사용 가능한 광학 리더와 일회용 유체 시스템을 결합하여 유럽의 체외진단 시장 용도 분야에서 지속가능성 및 성능의 균형을 이룹니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환 및 감염의 부담이 조기 진단 수요 향상

- 1차 케어 네트워크에서 포인트 오브 케어 검사 도입

- 맞춤형 의료로의 시프트가 분자진단약 및 동반진단약 촉진

- 고령화 및 예방 검진 프로그램이 검사량 확대

- EU IVDR은 품질 기준을 끌어올려 고가치 혁신 자극

- 시장 성장 억제요인

- EUIVDR의 긴 규제 일정 및 규정 준수 비용

- 첨단 분자 검사에 대한 상환의 불확실성

- 연구소의 노동력 부족 및 능력 제약

- 공급망 분석

- 규제 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 검사 유형별

- 임상 화학

- 분자진단

- 면역진단

- 혈액학

- 미생물학 및 래터럴 플로우

- 기타 검사

- 제품 및 서비스별

- 시약 및 소모품

- 기기 및 분석 장치

- 소프트웨어 및 서비스

- 사용성별

- 일회용 IVD 디바이스

- 재사용 가능한 IVD 디바이스

- 검체 유형별

- 혈액 및 혈청

- 소변

- 타액

- 조직 및 생검

- 검사 부위별

- 센트럴 랩

- 포인트 오브 케어 검사

- 재택 및 자체 검사

- 레퍼런스 랩

- 용도별

- 감염증

- 당뇨병

- 암 및 종양학

- 심장병학

- 자가면역질환

- 신장 및 신장 패널

- 출생 전 및 유전자 스크리닝

- 최종 사용자별

- 진단 실험실

- 병원 및 클리닉

- 학술기관 및 연구기관

- 재택 케어 및 POC 센터

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- F. Hoffmann-La Roche AG

- Abbott Laboratories

- Siemens Healthineers AG

- Danaher Corp.(Beckman Coulter & Cepheid)

- Thermo Fisher Scientific Inc.

- bioMerieux SA

- Becton, Dickinson & Co.

- Bio-Rad Laboratories Inc.

- QIAGEN NV

- Sysmex Corp.

- Hologic Inc.

- DiaSorin SpA

- Illumina Inc.

- QuidelOrtho Corp.

- Mindray Bio-Medical

- Agilent Technologies Inc.

- Randox Laboratories Ltd.

- Grifols SA

- Werfen

- Gentian Diagnostics ASA

제7장 시장 기회 및 향후 전망

AJY 25.11.26The Europe in vitro diagnostics market stands at USD 29.06 billion in 2025 and is forecast to reach USD 37.98 billion by 2030, reflecting a 5.5% CAGR over the period.

This trajectory highlights the region's rapid uptake of advanced testing platforms, the push for early chronic-disease detection and the regulatory lift provided by the EU IVDR. Germany's leading healthcare infrastructure, the United Kingdom's digital transformation agenda and the strong shift toward point-of-care models are giving suppliers clear expansion avenues. Molecular techniques are moving from specialised centres into mainstream care pathways, while immunodiagnostics remain a workhorse for routine analysis and screening. Consumables continue to anchor recurring revenue, and non-invasive specimen types are broadening patient access.

Europe In-Vitro Diagnostics Market Trends and Insights

Burden of Chronic & Infectious Diseases Elevates Demand for Early Diagnostics

Rising multimorbidity means almost 70% of inpatient treatment decisions already depend on accurate laboratory evidence. Oncology and cardiovascular pathways now integrate biomarker panels to stratify risk and guide therapies. Roughly 50 million Europeans are managing more than one chronic condition, intensifying calls for multiplex tests that handle several analytes from a single sample. Post-pandemic surveillance budgets remain higher than pre-2020 benchmarks, ensuring labs maintain expanded infectious-disease capacity. Health ministries view wider testing access as prerequisite for universal-coverage goals, pushing procurement of high-throughput platforms and near-patient devices at primary-care level.

Adoption of Point-of-Care Testing Across Primary Care Networks

Decentralised devices are cutting diagnostic turnaround in family-medicine settings. A United Kingdom cost-minimisation study showed GBP 29 savings per 100 patients screened when point-of-care analysers were used during NHS Health Checks. European paediatricians report large inter-country differences, yet urine dipstick availability in primary care now exceeds 80% in two-thirds of surveyed nations. Machine-learning firmware embedded in new devices is lifting sensitivity for low-abundance targets and enabling multi-marker cards that rival core-laboratory precision. These benefits are catalysing payer acceptance, especially for chronic-disease follow-up.

Lengthy Regulatory Timelines & Compliance Costs under EU IVDR

The Association for Molecular Pathology reports that 73% of European laboratories still lack full clarity on IVDR obligations, while notified-body queues extend up to two years for some categories. Start-ups face disproportionate legal and biostatistical-study expenses, delaying novel assays for emerging pathogens and rare diseases. Although the Commission granted phased deadlines, any lapse in certification can disrupt hospital supply chains.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Personalised Medicine Boosts Molecular & Companion Diagnostics

- Aging Population & Preventive Screening Programs Expand Test Volumes

- Reimbursement Uncertainty for Advanced Molecular Tests

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Europe in vitro diagnostics market size for immunodiagnostics was bolstered by a 27% revenue share in 2024, reflecting its role in hormone, infectious-disease and autoimmune panels. High-sensitivity chemiluminescent assays keep volumes robust, while COVID-19 investments have permanently upgraded instrument fleets. Molecular diagnostics is expected to generate the highest 7.2% CAGR through 2030, propelled by declining sequencing costs and companion-test uptake. Oncology now accounts for most European genomic testing, but rapid-cycling PCR platforms for respiratory pathogens, sexually transmitted infections and antimicrobial stewardship broaden the addressable base. AI-driven variant-calling software lifts analytical confidence and compresses reporting times.

Routine clinical chemistry remains foundational for electrolyte and metabolic screens, supported by continuous analyser automation. Hematology benefits from digital morphology and integrated coagulation modules that turn full blood counts into rich diagnostic outputs. Meanwhile, microbiology workflows integrate MALDI-TOF and syndromic panels, speeding pathogen ID and therapy guidance. As these test categories intertwine via middleware, clinicians obtain comprehensive views from fewer samples, meeting the drive for efficient patient-centred care across the Europe in vitro diagnostics market.

Reagents and consumables delivered 65% of 2024 revenue, underlining the razor-and-blade economics that stabilise cash flow and raise switching barriers. Bulk purchasing agreements in national tenders favour incumbents, yet quality-management clauses now weigh digital-traceability functions. Instruments are trending toward open-channel architectures that flex between chemistry and immunoassay modalities, helping labs maximise analyser uptime. Middleware dashboards curate quality-control flags and utilisation analytics, nudging procurement towards holistic platform deals rather than isolated analyser sales.

The software and services segment, while smaller, is forecast to post the fastest 8.5% expansion. Labs increasingly pay subscription fees for LIS integration, AI-assisted result interpretation and regulatory documentation modules. Vendors monetise cloud-based analytics that benchmark peer performance and automate external-quality assessments. This pivot elevates digital differentiation at a time when core analytic sensitivity gains are approaching technical ceilings, sustaining competitive edge in the Europe in vitro diagnostics industry.

Disposable devices held 58% revenue share in 2024 and are projected to clock a 6.9% CAGR. Single-use cartridges safeguard infection control in polyclinic settings and support home-testing convenience. Lateral-flow strips now cover C-reactive protein, cardiac troponin and vitamin-D assays, while microfluidic chips mount multiplex panels with minimal user steps. Environmental concerns spur suppliers to introduce biodegradable casings and take-back programs that reduce plastic waste.

Reusable devices dominate high-throughput central-lab workflows, where annual sample volumes justify capital investment. Upgrades focus on walk-away automation, self-cleaning modules and lower reagent dead-volume to curb consumable spend. Hybrid architectures pair reusable optical readers with disposable fluidics, balancing sustainability and performance across Europe in vitro diagnostics market applications.

The Europe In-Vitro Diagnostics Market Report is Segmented by Test Type (Clinical Chemistry, and More), Product & Service (Instrument, and More), Usability (Disposable IVD Devices, and More), Specimen Type (Blood, and More), Site of Testing (Central Laboratories and More), Application (Infectious Diseases and More), End User (Diagnostic Laboratories and More) and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Roche

- Abbott Laboratories

- Siemens Healthineers

- Danaher Corp. (Beckman Coulter & Cepheid)

- Thermo Fisher Scientific

- bioMerieux

- Beckton Dickinson

- Bio-Rad Laboratories

- QIAGEN

- Sysmex Corp.

- Hologic

- DiaSorin

- Illumina

- QuidelOrtho Corp.

- Mindray Bio-Medical

- Agilent Technologies

- Randox Laboratories

- Grifols

- Werfen

- Gentian Diagnostics ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Burden of Chronic & Infectious Diseases Elevates Demand for Early Diagnostics

- 4.2.2 Adoption of Point-of-Care Testing Across Primary Care Networks

- 4.2.3 Shift to Personalized Medicine Boosts Molecular & Companion Diagnostics

- 4.2.4 Aging Population & Preventive Screening Programs Expand Test Volumes

- 4.2.5 EU IVDR Raising Quality Standards and Stimulating High-Value Innovation

- 4.3 Market Restraints

- 4.3.1 Lengthy Regulatory Timelines & Compliance Costs under EUIVDR

- 4.3.2 Reimbursement Uncertainty for Advanced Molecular Tests

- 4.3.3 Laboratory Workforce Shortage and Capacity Constraints

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 Clinical Chemistry

- 5.1.2 Molecular Diagnostics

- 5.1.3 Immunodiagnostics

- 5.1.4 Hematology

- 5.1.5 Microbiology & Lateral Flow

- 5.1.6 Other Tests

- 5.2 By Product & Service

- 5.2.1 Reagents & Consumables

- 5.2.2 Instruments/Analyzers

- 5.2.3 Software & Services

- 5.3 By Usability

- 5.3.1 Disposable IVD Devices

- 5.3.2 Reusable IVD Devices

- 5.4 By Specimen Type

- 5.4.1 Blood/Serum

- 5.4.2 Urine

- 5.4.3 Saliva

- 5.4.4 Tissue/Biopsy

- 5.5 By Site of Testing

- 5.5.1 Central Laboratories

- 5.5.2 Point-of-Care Testing

- 5.5.3 Home/Self-Testing

- 5.5.4 Reference Labs

- 5.6 By Application

- 5.6.1 Infectious Diseases

- 5.6.2 Diabetes

- 5.6.3 Cancer/Oncology

- 5.6.4 Cardiology

- 5.6.5 Autoimmune Disorders

- 5.6.6 Nephrology & Renal Panels

- 5.6.7 Prenatal/Genetic Screening

- 5.7 By End User

- 5.7.1 Diagnostic Laboratories

- 5.7.2 Hospitals & Clinics

- 5.7.3 Academic & Research Institutes

- 5.7.4 Home-Care/POC Centers

- 5.8 By Country

- 5.8.1 Germany

- 5.8.2 United Kingdom

- 5.8.3 France

- 5.8.4 Italy

- 5.8.5 Spain

- 5.8.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 F. Hoffmann-La Roche AG

- 6.3.2 Abbott Laboratories

- 6.3.3 Siemens Healthineers AG

- 6.3.4 Danaher Corp. (Beckman Coulter & Cepheid)

- 6.3.5 Thermo Fisher Scientific Inc.

- 6.3.6 bioMerieux SA

- 6.3.7 Becton, Dickinson & Co.

- 6.3.8 Bio-Rad Laboratories Inc.

- 6.3.9 QIAGEN N.V.

- 6.3.10 Sysmex Corp.

- 6.3.11 Hologic Inc.

- 6.3.12 DiaSorin SpA

- 6.3.13 Illumina Inc.

- 6.3.14 QuidelOrtho Corp.

- 6.3.15 Mindray Bio-Medical

- 6.3.16 Agilent Technologies Inc.

- 6.3.17 Randox Laboratories Ltd.

- 6.3.18 Grifols S.A.

- 6.3.19 Werfen

- 6.3.20 Gentian Diagnostics ASA

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment