|

시장보고서

상품코드

1683948

자동차용 LED 조명 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

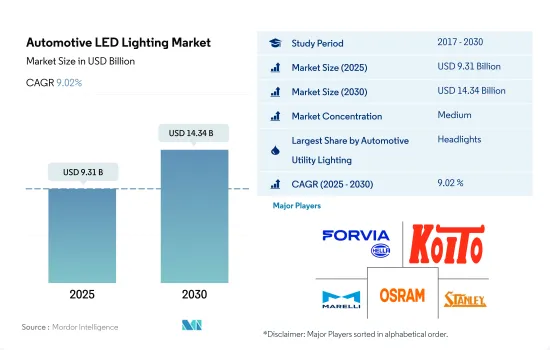

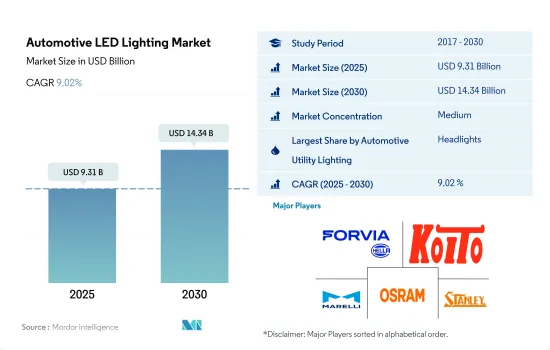

자동차용 LED 조명 시장 규모는 2025년에 93억 1,000만 달러에 달할 것으로 추정됩니다. 2030년에는 143억 4,000만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 9.02%를 나타낼 것으로 전망됩니다.

사고율 상승, EV 수요 증가, 정부 지원 정책이 시장 성장 견인

- 금액 점유율은 2022년 전조등이 시장 점유율의 대부분(51.8%)을 차지한 다음, 기타(소형 LED 라이트, LED 번호판 라이트, 안개등, 실내 LED 라이트), 방향지시등(DSL), 주간 주행등, 정지등 등이 뒤를 이었습니다. 전조등 부문은 향후 높은 시장 점유율을 획득할 것으로 예상됩니다. 사고 건수가 증가함에 따라 안개 LED 램프와 헤드 램프의 보급률도 상승할 것으로 예상됩니다. 세계에서는 매년 약 130만명이 교통사고로 사망하고 있습니다.

- 수량 점유율은 2023년에 DSL이 시장 점유율의 대부분(27.9%)을 차지한 다음 전조등(17.7%), 기타(소형 LED 라이트, LED 넘버 플레이트 라이트, 안개등, 실내 LED 라이트)(16.4%), 스톱 램프의 순이었습니다. 예측 기간 동안 시장 점유율은 모든 부문에서 평평할 것으로 예상되지만, 기타 및 정지등 부문이 약간 감소하고 DSL 및 전조등 부문이 증가할 것으로 보입니다. 외부 라이트(주로 신호등)는 모든 유형의 자동차에서 경미한 사고에서 심각한 사고까지 영향을 받을 가능성이 높고 교체가 필요합니다.

- EV는 세계적으로 자동차용 LED 수요가 급증하는 주요 요인 중 하나입니다. 중국이 EV 시장을 선도해 2022년 세계 전기차 판매 대수의 60%를 차지한 다음 유럽과 미국이 각각 15%와 55%의 높은 성장세를 보였습니다.

- 유럽연합(EU)의 Fit for 55 패키지와 미국의 인플레이션 억제법 등 주요 국가의 야심적인 정책 프로그램이 EV 시장 점유율을 높일 것으로 예상됩니다. 시장의 주요 기업는 선진국에서 EV 공장의 확대에 주력하고 있습니다.

EV 성장, 자율주행차, 정부 인센티브는 자동차 산업에서 LED 조명의 채용을 촉진할 것으로 예상됩니다.

- 금액 점유율에서 2022년 자동차용 LED 조명 시장은 아시아태평양이 대부분을 차지했고 북미와 유럽이 각각 그 뒤를 이었습니다. 중국, 일본, 태국, 대만, 말레이시아, 인도 등 아시아 6개국의 대부분이 국내 시장의 보호와 자동차 산업 진흥에 있어서의 자동차 제조업체에의 우대 조치 등의 인센티브를 도입하고 있기 때문에 2029년의 아시아태평양 시장 점유율은 증가할 것으로 예상됩니다.

- 수량 점유율에서는 아시아태평양의 자동차용 LED 조명 시장이 2022년 대부분의 점유율을 차지한 다음 유럽, 북미가 되었습니다. 유럽에서는 전기자동차의 상승과 자동차에 사용되는 연료 유형의 기술 발전이 지역의 자동차 산업을 변화시키고 있습니다. 유럽 연합에서 배터리 전기자동차의 판매는 현재도 빠르게 성장하고 있습니다. 예를 들어, 2022년 EU 시장에서 판매된 910만대의 자동차 중 12.1%가 순수한 배터리 전기자동차였습니다. 반면 2019년에는 이 점유율은 1.9%, 2021년에는 9.1%였습니다.

- 전동화는 업계가 세계적으로 발전하고 있는 가장 큰 변화입니다. 또 다른 동향은 자율주행차입니다. 기술이 자동차 회사의 탄소 중립 목표에 기여하는 것이 중요합니다. 중동은 닛산에게 중요한 시장입니다. 현대의 많은 자동차는 더 똑똑하고 연결되어 왔습니다. 닛산 알리야와 같은 지능형 이동성과 자율 주행이 탑재될 것입니다. 이러한 변화는 이 지역의 다른 지역에서도 이루어지고 있습니다. 따라서 이 지역의 자동차 부문 성장으로 LED 시장 침투가 진행될 수 있습니다.

세계의 자동차용 LED 조명 시장 동향

EV 수요 증가가 시장 가치를 높일 것으로 예측

- 2022년 세계 자동차 생산 대수는 1억 4,396만 대로, 2023년에는 1억 5,092만 대에 달했습니다. 수집된 데이터에 따르면 이미 세계 자동차 생산 대수가 약 5% 감소한 2019년에 이어 2020년에도 자동차 생산 대수가 16% 감소하는 것으로 나타났습니다. 유럽 전체의 평균 감소율은 21% 이상이었습니다. 모든 주요 생산국의 급격한 감소는 11%에서 약 40%에 이르렀습니다. 유럽 제조업은 총 생산량의 약 22%를 차지했습니다. 아메리카의 자동차 생산은 2020년 세계 생산의 20%를 차지했습니다. 아프리카 대륙의 제조업은 35% 이상으로 급감했습니다. 한편 아시아는 10% 감소에 머물렀습니다. 제공된 숫자에 따르면 COVID-19의 유행은 자동차 산업에 큰 영향을 주었고 LED 수요를 줄였습니다.

- 폭스바겐 그룹, 스텔란티스, 메르세데스 벤츠, BMW, 포르쉐, Hurtan, GTA 모터스, 아우디, TATA 모터스, 마힌드라 & 마힌드라, 상하이 기차, 현대 자동차, 기아 자동차, KG 모빌리티, 르노 한국 자동차가 세계 주요 자동차 제조 기업입니다. 2022년 세계 전기차 판매 대수는 1,000만대를 넘어, 2023년의 판매 대수는 더욱 35% 증가한 1,400만대에 달했습니다. 이러한 급속한 확대로 전기차 시장 점유율은 2020년 4%에서 2022년 14%로 증가했습니다. 또한 전기자동차의 보급에 따라 기존 자동차보다 1대당 프로세서 수가 늘어나 차내용 반도체 칩 수요가 높아지고 있습니다. LED 조명 시장은 자동차 산업의 반도체 수요 증가로 혜택을 누릴 것으로 예상됩니다.

배터리 교환 스테이션과 배터리 리사이클 서비스 점포 증가, EV 수요 증가가 시장 성장의 원동력이 될 것으로 예상됩니다.

- EV 시장은 급격한 기세로 확대되고 있으며, 2022년에는 판매 대수가 1,000만대를 넘어섰습니다. 2022년에는 전기차가 전체 차 판매 대수의 14%를 차지하고 2021년의 약 9%, 2020년의 5% 미만에서 증가했습니다. 세계의 판매 대수는 3개 시장이 견인했습니다. 중국이 톱으로 세계의 전기자동차 판매 대수의 60% 가까이를 차지했습니다. 중국은 세계에서 주행하는 전기차의 절반 이상을 차지하고 있으며, 정부는 이미 신에너지차 판매의 2025년 목표를 웃돌고 있습니다.

- 2022년까지 중국에는 1,973곳의 배터리 교환 스테이션(2022년에 건설된 675곳 포함)이 있었으며, 1만개 이상의 전원 배터리 재활용 서비스 점포가 있었습니다. 이처럼 충전시설의 급속한 증가는 이 나라의 신에너지차(NEV) 부문의 활황을 보여줍니다. 2022년 10월 독일 정부는 전기차 충전 인프라를 강화할 계획을 발표했습니다. 이 계획은 63억 유로(61억 7,000만 달러)의 제안으로 구성되어 있으며, 2030년까지 전국의 충전 포인트를 100만 곳으로 늘린다는 것이었습니다.

- 주요 시장에서 2022년 전기자동차 판매는 예년 낮은 수준이었지만 인도, 태국, 인도네시아에서는 성장의 해가 되었습니다. 이들 국가에서 전기차 판매량은 2021년에서 3배 이상으로 증가하여 8만대에 달했습니다. 미국에서는 인플레이션 억제법(IRA)과 캘리포니아 주 선진 클린카Ⅱ규칙을 채용하는 많은 주가 함께 2030년에는 전기차 시장 점유율이 국가 목표에 맞추어 50%가 될 가능성이 높습니다. 위의 사례를 고려하면 세계 주요 제조업체들은 자동차용 LED 개발 및 생산에 더 많은 투자를할 것으로 예상됩니다.

자동차용 LED 조명 산업 개요

자동차용 LED 조명 시장은 적당히 통합되어 상위 5개사에서 51.31%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. HELLA GmbH & Co. KGaA(FORVIA), KOITO MANUFACTURING, Marelli Holdings, OSRAM GmbH. and Stanley Electric(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 자동차 생산 대수

- 인구

- 1인당 소득

- 자동차 대출 금리

- 충전소 수

- 자동차 주행 대수

- LED 총 수입량

- 가구수

- 도로 네트워크

- 보급률

- 규제 프레임워크

- 아르헨티나

- 브라질

- 중국

- 프랑스

- 독일

- 걸프 협력 회의

- 인도

- 일본

- 남아프리카

- 한국

- 스페인

- 영국

- 미국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 자동차용 유틸리티 조명

- 주간 주행등(DRL)

- 방향지시등

- 전조등

- 후진등

- 정지등

- 후미등

- 기타

- 자동차용 조명

- 이륜차

- 상용차

- 승용차

- 지역

- 아시아태평양

- 유럽

- 중동 및 아프리카

- 북미

- 남미

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- GRUPO ANTOLIN IRAUSA, SA

- HELLA GmbH & Co. KGaA(FORVIA)

- 현대모비스

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Signify(Philips)

- Stanley Electric Co., Ltd.

- Valeo

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Automotive LED Lighting Market size is estimated at 9.31 billion USD in 2025, and is expected to reach 14.34 billion USD by 2030, growing at a CAGR of 9.02% during the forecast period (2025-2030).

The rising accident rates, growing demand for EVs, and supportive government policies drive the market's growth

- In terms of value share, in 2022, headlights accounted for most of the market share (51.8%), followed by others (miniature LED lights, LED license plate lights, fog Lights, and interior LED lights), directional signal lights (DSLs), day time running lights, and stop lights. The headlights segment is expected to gain a higher market share in the future. Along with the rising number of accidents, the penetration rate of fog LED lamps and headlamps is anticipated to rise. Approximately 1.3 million people die each year as a result of road traffic crashes globally.

- In terms of volume share, in 2023, DSLs accounted for most of the market share (27.9%), followed by headlights (17.7%), others (miniature LED lights, LED license plate lights, fog Lights, and interior LED lights) (16.4%), and stop lights. The market share is expected to remain the same for all the segments during the forecast period, with a slight reduction in the others and stop lights segment and an increase in the DSLs and headlights segments. External lights (primarily signal lights) are highly likely to be affected in minor to major accidents in all types of vehicles and require replacement.

- EVs are one of the primary drivers for the surging demand for automotive LEDs globally. China led the EV market, accounting for 60% of global electric car sales in 2022, followed by Europe and the United States, which saw strong sales growth of 15% and 55%, respectively.

- The ambitious policy programs in major economies, such as the Fit for 55 package in the European Union and the Inflation Reduction Act in the United States, are expected to boost the market share of EVs. Key players in the market are also focusing on expanding their EV plants in developed nations.

Growth in EVs, autonomous vehicles, and government incentives are expected to boost the adoption of LED lights in the automotive industry

- In terms of value share, the Asia-Pacific automotive LED lighting market accounted for the majority share in 2022, followed by North America and Europe, respectively. The market share is expected to increase for Asia-Pacific in 2029, as most of the six Asian countries, such as China, Japan, Thailand, Taiwan, Malaysia, and India, have introduced incentives such as protecting their domestic markets and giving preferential treatment to automakers in promoting their automobile industries.

- In terms of volume share, the Asia-Pacific automotive LED lighting market accounted for the majority share in 2022, followed by Europe and North America. In Europe, the rise of electric vehicles and technological advances in the types of fuels used in vehicles are transforming the region's automotive industry. Sales of battery electric vehicles in the European Union are still growing rapidly. For example, 12.1% of the 9.1 million cars sold on the EU market in 2022 were pure battery electric vehicles. By contrast, in 2019, this share was just 1.9%, and in 2021 it was 9.1%.

- Electrification is the most significant transformation the industry is undergoing worldwide. Another trend rising is autonomous vehicles. It is important to note that technology contributes to auto companies' carbon-neutral goals. The Middle East is an important market for Nissan. Many modern vehicles are getting smarter and more connected. It will be equipped with intelligent mobility and autonomous driving, similar to the Nissan Ariya. Such transformations are undertaken in other parts of the region. Thus, growth in the regional automotive segment may increase the penetration of LEDs in the market.

Global Automotive LED Lighting Market Trends

The increasing demand for EVs is anticipated to raise the market value

- The total automobile production globally was 143.96 million units in 2022, and it was expected to reach 150.92 million units in 2023. The gathered data indicated a 16% reduction in the manufacturing of automotive cars in 2020, following a dismal 2019, which already showed a noticeable decline of roughly 5% in global auto output. The average decline across all of Europe was more than 21%. Sharp decreases in all major producing nations ranged from 11% to roughly 40%. Manufacturing in Europe accounted for roughly 22% of the total production. Vehicle manufacturing in the Americas accounted for 20% of global production in 2020. The African continent had a severe decrease of more than 35% in manufacturing. Asia, on the other hand, held up very well, with a decline of only 10%. According to the numbers provided, the COVID-19 pandemic had a tremendous impact on the automotive industry, which decreased the demand for LEDs.

- Volkswagen Group, Stellantis, Mercedes-Benz, BMW, Porsche, Hurtan, GTA Motors, Audi, TATA Motors, Mahindra & Mahindra, SAIC Motor, Hyundai Motor Company, Kia Corporation, KG Mobility, and Renault Korea Motors are the major automotive manufacturing companies globally. In 2022, there were more than 10 million electric vehicle sales worldwide, and the sales in 2023 were anticipated to increase by another 35% to a total of 14 million. Due to this rapid expansion, the market share of electric automobiles increased from 4% in 2020 to 14% in 2022. In addition, as more electric vehicles are being used, there is a rising demand for automotive semiconductor chips because they require more processors per vehicle than conventional cars. The market for LED lighting is expected to benefit from the increase in semiconductor demand in the automobile industry.

The increasing number of battery swapping stations and battery recycling service outlets and the rising demand for EVs are expected to drive the growth of the market

- The EV markets are expanding at an exponential rate, with sales exceeding 10 million in 2022. In 2022, electric vehicles accounted for 14% of all new vehicle sales, up from roughly 9% in 2021 and less than 5% in 2020. Global sales were led by three markets. China was the leader, accounting for almost 60% of global electric vehicle sales. China accounts for more than half of all the electric vehicles on the road worldwide, and the government has already exceeded its 2025 target for new energy vehicle sales.

- By 2022, China had 1,973 battery swapping stations, including 675 built in 2022 and over 10,000 power battery recycling service outlets. Thus, the rapid growth of charging facilities indicates the booming new energy vehicle (NEV) sector in the country. In October 2022, the German government unveiled plans to boost charging infrastructure for electric vehicles. The plan consisted of a EUR 6.3 billion (USD 6.17 billion) proposal that would increase the number of charging points across the country to 1 million by 2030.

- In major markets, electric car sales were normally low in 2022, but it was a growth year in India, Thailand, and Indonesia. Sales of electric vehicles in these countries more than tripled since 2021, reaching 80,000 units. In the United States, the Inflation Reduction Act (IRA), combined with a number of states adopting California's Advanced Clean Cars II rule, is likely to produce a 50% market share for electric cars in 2030, in line with the national target. Considering the abovementioned instances, key manufacturers across the world are expected to invest more in developing and producing automotive LEDs.

Automotive LED Lighting Industry Overview

The Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 51.31%. The major players in this market are HELLA GmbH & Co. KGaA (FORVIA), KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH. and Stanley Electric Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 Argentina

- 4.11.2 Brazil

- 4.11.3 China

- 4.11.4 France

- 4.11.5 Germany

- 4.11.6 Gulf Cooperation Council

- 4.11.7 India

- 4.11.8 Japan

- 4.11.9 South Africa

- 4.11.10 South Korea

- 4.11.11 Spain

- 4.11.12 United Kingdom

- 4.11.13 United States

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.2 Europe

- 5.3.3 Middle East and Africa

- 5.3.4 North America

- 5.3.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Signify (Philips)

- 6.4.9 Stanley Electric Co., Ltd.

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms