|

시장보고서

상품코드

1684038

유럽의 적층 세라믹 커패시터(MLCC) 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

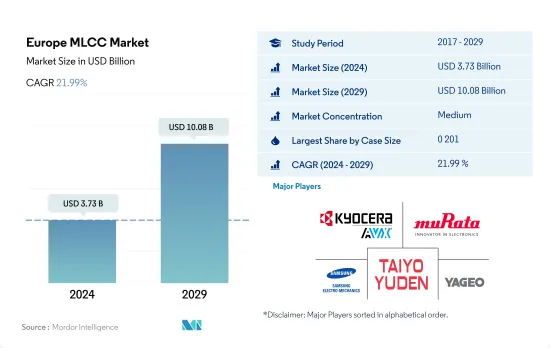

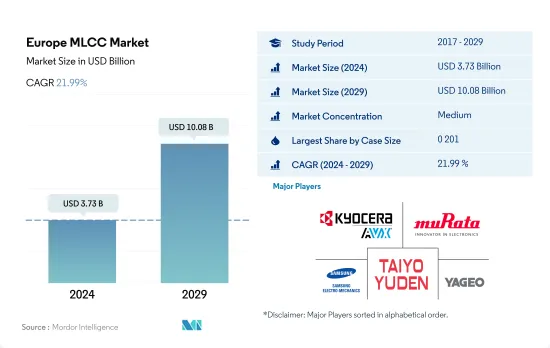

유럽의 적층 세라믹 커패시터(MLCC) 시장 규모는 2024년에 37억 3,000만 달러로 평가되었고, 2029년에는 100억 8,000만 달러에 이를 전망이며, 시장 추계 및 예측 기간인 2024-2029년 CAGR은 21.99%를 나타낼 것으로 예측됩니다.

5G 기지국 전개 및 지역에서 군사비 증가가 적층 세라믹 커패시터(MLCC)의 요구 촉진

- 케이스 크기 0 201이 최고 러너로 부상하고 2022년 수량 기준으로 34.55%의 최대 시장 점유율을 획득했고, 이어서 케이스 크기 0 402가 19.57%, 케이스 크기 0 603이 14.10%이었습니다.

- 케이스 크기 0 402는 가장 컴팩트하며 회로 보드의 부품 밀도를 높일 수 있습니다. 유럽의 항공우주 및 방위 분야가 통신 기기나 무인 항공기(UAV) 등의 첨단 기술이나 시스템에 투자하는 가운데, 100uF-1000uF의 중간 용량을 가지는 X7R 유전체 0 402 적층 세라믹 커패시터(MLCC)는 신뢰성이 높고 효율적인 전력 성능을 유지하는 데 있어서 필수적인 역할을 하기 때문에 필요가 높아집니다. 의료기기의 설계자는 현재 ICD와 페이스메이커의 추가 소형화를 목표로, 혁신적인 디바이스 설계의 개발에 임하고 있습니다. 이러한 장치는 모두 체내에 보관되므로 가능한 한 작아야 합니다. 현재, 무연 페이스메이커의 개발이 진행되고 있으며, 그 크기는 종래의 페이스메이커의 약 10분의 1이 될 것으로 추정되고 있습니다. 따라서 커패시터를 포함하여 이러한 장비에 사용되는 전기 부품의 추가 소형화가 필요할 수 있습니다.

- 0 603 적층 세라믹 커패시터(MLCC) 수요를 견인하는 것은 통신 업계입니다. 유럽의 통신 분야는 5G 기지국의 신속한 개발에 주력하고 있으며, X5R 유전체를 사용한 0603 케이스 크기의 적층 세라믹 커패시터(MLCC) 수요가 증가하고 있습니다.

5G 대응 스마트폰과 같은 소비자용 전자기기의 사용 증가 및 AR, VR과 같은 신기술의 진보가 적층 세라믹 커패시터(MLCC) 수요를 견인하고 있습니다.

- 독일이 톱 러너로 떠오르며, 2022년 수량 기준으로 25.07%의 최대 시장 점유율을 획득한 다음 14.99%의 영국이 이어졌습니다.

- 영국의 가전 제조 부문이 견인역이 되고 있습니다. 영국과 같은 국가의 가전 시장은 향후 몇 년동안 급성장할 것으로 예상됩니다. 5G 네트워크, 스마트홈, AR 및 VR 기술, 기능을 강화한 가전기기의 끊임없는 진화도 이 성장에 기여할 가능성이 있습니다. 그 결과, 100uF 이하의 낮은 커패시턴스를 가지는 0201 케이스 사이즈의 표면 실장 유형의 설치형 적층 세라믹 커패시터(MLCC) 수요가 증가할 것으로 예상됩니다.

- 독일 자동차 산업은 이 나라의 경제 성장에 가장 기여하는 분야 중 하나입니다. 따라서 X7R 적층 세라믹 커패시터(MLCC) 수요는 증가하는 경향이 있습니다. 자동 운전 기능이 없는 엔진차에는 통상 약 3,000개의 적층 세라믹 커패시터(MLCC)가 필요하지만, 전기자동차(EV)에는 통상 8,000-1만 개의 적층 세라믹 커패시터(MLCC)가 필요합니다. 자동차 부문의 현재 상태는 독일에서 진행되는 급속한 기술 개발에서 볼 수 있습니다. 또한 독일 정부의 규제, 인센티브, 할인, 전자 모빌리티에 대한 인식이 높아져 소비자의 EV 구매를 뒷받침하고 있습니다.

유럽의 적층 세라믹 커패시터(MLCC) 시장 동향

엄격한 정부 규제가 전동 LCV의 보급 촉진

- 소형 상용차(LCV)의 생산 대수는 2019년부터 2022년까지 엇갈린 결과를 보였습니다. 2019년 252만 대에서 시작해 2020년에는 211만 대로 약간 감소했습니다. 그러나 2021년에는 218만 대로 회복했고, 2022년에는 214만 대로 안정되어 4년간의 CAGR은 약 4.6%가 되었습니다.

- 2019년까지 몇 년동안 업계는 LCV 생산의 CAGR이 가장 높은 것으로 나타났습니다. 그러나 이후 몇 년동안 COVID-19 팬데믹을 포함한 혼란과 불확실성이 뚜렷해져 자동차 산업 전체에 큰 영향을 미쳤습니다. 공급망 혼란 및 소비자 수요 감소는 생산 감소의 원인이 되었습니다. 그럼에도 불구하고 업계는 일정한 생산 수준을 유지함으로써 탄력성을 보였습니다.

- 유럽 의회가 'Fit for 55' 패키지의 일환으로 승용차와 소형 상용차의 새로운 CO2 배출량 감소 목표를 승인한 것은 적층 세라믹 커패시터(MLCC) 시장을 포함한 자동차 산업에 큰 영향을 미칠 것으로 보입니다. 자동차 산업이 CO2 배출량 제로를 목표로, 전기차의 보급이 진행됨에 따라 적층 세라믹 커패시터(MLCC) 수요는 높아질 것으로 예상됩니다.

- 유럽위원회가 의무화하는 OBFCM의 설치는 적층 세라믹 커패시터(MLCC) 수요를 더욱 밀어올릴 것으로 보입니다. 이러한 구성 요소는 차량 시스템 내에서 정확한 측정, 데이터 처리 및 통신을 가능하게 하며 CO2 배출량과 에너지 소비 모니터링을 지원합니다. 판매 동향을 반영한 ZLEV 인센티브 메커니즘의 적응은 제로 방출 차량의 생산과 구매를 장려하고 적층 세라믹 커패시터(MLCC) 수요를 증가시킵니다.

유럽에서 OBFCM 장비 채택 확대도 승용차 생산을 증가시켰습니다.

- 유럽에서는 승용차 생산량이 감소했습니다. 2019년 생산 대수는 1,870만 대였지만, 2022년에는 1,372만 대로 감소했으며, 4년간의 CAGR은 약 -8.7%였습니다.

- 이 생산량의 감소는 제조 시설의 일시적 폐쇄, 소비자의 구매력의 저하, 유통에 의한 시장 전체의 불확실성 등 다양한 요인에 의한 것으로 예상됩니다. 그러나 유럽의 자동차 부문이 역경에 직면해도 회복력과 적응력을 보인 것은 중요합니다.

- 2019년에는 소형차 CO2 규제가 시행되어 배출가스 감축과 기후 변화 대응에 다시 초점을 맞추었습니다. 이 규제는 거리에서의 연료 소비 및 전기 에너지 소비를 정확하게 모니터링 할 필요성을 강조하여 신차에 차량 탑재 연료 및 에너지 소비 모니터링 장치(OBFCM)를 탑재하게 되었습니다. 이 규제 프레임워크는 유럽의 적층 세라믹 커패시터(MLCC) 시장에서 사업을 전개하는 기업에 기회를 가져옵니다. 적층 세라믹 커패시터(MLCC)는 자동차 전자 장치를 포함한 다양한 용도에 사용되는 필수 전자 부품입니다. OBFCM과 기타 모니터링 장치의 통합으로 자동차가 더욱 진화함에 따라 적층 세라믹 커패시터(MLCC) 수요가 증가할 것으로 예상됩니다. 이러한 부품은 자동차 시스템 내에서 정확한 측정, 데이터 처리 및 통신을 가능하게 하는 데 중요한 역할을 합니다.

- 업계가 OBFCM과 같은 첨단 기술 통합을 위해 노력하고 있는 가운데, 적층 세라믹 커패시터(MLCC)는 실제 CO2 감소를 달성하고 실제 주행 조건 하에서 차량이 예상대로 성능을 발휘하는 데 중요한 역할을 하게 됩니다.

유럽의 적층 세라믹 커패시터(MLCC) 산업 개요

유럽의 적층 세라믹 커패시터(MLCC) 시장은 적당히 통합되어 상위 5개사에서 51.04%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Kyocera AVX Components Corporation(Kyocera Corporation), Murata Manufacturing, Samsung Electro-Mechanics, Taiyo Yuden 및 Yageo Corporation(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 가격 동향

- 구리의 가격 동향

- 니켈 가격 동향

- 은 가격 동향

- 아연 가격 동향

- 가전 판매 대수

- 에어컨 판매 대수

- 데스크톱 PC 판매 대수

- 게임기 판매 대수

- 노트북 판매 대수

- 냉장고 판매 대수

- 스마트폰 판매 대수

- 수납 기기 판매 대수

- 태블릿 판매 대수

- TV 판매 대수

- 자동차 생산

- 버스 생산

- 대형 트럭 생산

- 소형 상용차 생산

- 승용차 생산

- 자동차 생산

- EV 생산

- BEV(배터리 전기자동차)의 생산

- PHEV(플러그인 하이브리드차) 생산

- 산업용 자동화 매출액

- 산업용 로봇 판매

- 서비스 로봇 판매

- 규제 프레임워크

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 유전체 유형별

- 클래스 1

- 클래스 2

- 케이스 사이즈별

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- 기타

- 전압별

- 500V-1000V

- 500V 미만

- 1000V 이상

- 정전 용량별

- 100uF-1,000uF

- 100uF 미만

- 1,000uF 이상

- 적층 세라믹 커패시터(MLCC) 실장 유형별

- 금속 캡

- 레이디얼 리드

- 표면 실장

- 최종 사용자별

- 항공우주 및 방위

- 자동차

- 소비자용 전자 기기

- 산업기기

- 의료기기

- 전력 및 유틸리티

- 통신 기기

- 기타

- 국가별

- 독일

- 영국

- 기타

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe MLCC Market size is estimated at 3.73 billion USD in 2024, and is expected to reach 10.08 billion USD by 2029, growing at a CAGR of 21.99% during the forecast period (2024-2029).

5G base station rollouts and the growing military spending in the region are driving the need for MLCCs

- The 0 201 case size segment emerged as the frontrunner, capturing the largest market share of 34.55%, followed by the 0 402 case size segment with 19.57% and the 0 603 case size segment with 14.10% in terms of volume in 2022.

- The case size of 0 402 is among the most compact available, thus increasing the component density of the circuit board. As the European aerospace and defense sector invests in advanced technologies and systems, such as communication equipment and unmanned aerial vehicles (UAVs), the need for 0 402 MLCCs with X7R dielectric with a mid capacitance of 100uF-1000uF is expected to grow due to their essential role in sustaining dependable and efficient power performance. Medical device designers are currently working to develop innovative device designs to reduce the size of ICDs and pacemakers further. These devices must be as small as possible, as they are both contained within the human body. The development of lead-free pacemakers is currently underway, and they are estimated to be approximately one-tenth the size of a traditional pacemaker. Therefore, further miniaturization of the electrical components used in these devices, including capacitors, may be necessary.

- The demand for 0 603 MLCCs is being driven by the telecommunications industry. The European telecommunications sector is focusing on rapid 5G base station deployment, thus increasing the demand for 0 603 case size MLCCs with X5R dielectric.

The increasing usage of consumer electronics like 5G-enabled smartphones and new technological advancements like AR and VR are driving the MLCC demand

- Germany emerged as the frontrunner, capturing the largest market share of 25.07%, followed by the United Kingdom, with 14.99%, in terms of volume in 2022.

- The United Kingdom's consumer electronics manufacturing sector is gaining traction. Consumer electronics markets in countries like the United Kingdom are expected to grow rapidly in the coming years. 5G networks, smart homes, AR and VR technologies, and the constant evolution of consumer electronics devices with enhanced features may also contribute to this growth. As a result, the demand for installed multi-layer ceramic capacitors (MLCCs) of the surface-mount type of 0 201 case size, with a low capacitance below 100uF, is expected to grow.

- The German automotive sector is one of the biggest contributors to the country's economic growth. As a result, the demand for X7R MLCCs is on the rise. An engine-powered vehicle without an automatic driving feature typically needs around 3,000 MLCCs, whereas an electric vehicle (EV) typically requires 8,000-10,000 MLCCs. The current state of the automotive sector can be seen in the rapid technological development taking place in Germany. In addition, the German government's regulations, incentives, and discounts, as well as the growing awareness of e-mobility, are driving consumers to purchase EVs.

Europe MLCC Market Trends

Stringent government regulations increase the penetration of electric LCVs

- Light commercial vehicles (LCVs) production exhibited a mixed performance between 2019 and 2022. Starting at 2.52 million units in 2019, it experienced a slight decline in 2020 to 2.11 million units. However, there was a rebound in 2021 with a production volume of 2.18 million units, followed by stability at 2.14 million units in 2022, indicating a CAGR of around 4.6% over the four years, reflecting the challenging and volatile nature of the market.

- In the years leading up to 2019, the industry witnessed the highest CAGR in LCV production. However, subsequent years were marked by disruptions and uncertainties, including the COVID-19 pandemic, which significantly impacted the overall automotive industry. Supply chain disruptions and reduced consumer demand contributed to the decline in production. Nonetheless, the industry demonstrated resilience by maintaining a certain level of production.

- The approval of new CO2 emissions reduction targets for passenger cars and light commercial vehicles by the European Parliament as part of the "Fit for 55" package will have a substantial impact on the automotive industry, including the market for MLCCs. As the industry moves towards zero CO2 emissions and increased adoption of electric vehicles, the demand for MLCCs is expected to rise.

- The installation of OBFCMs, as mandated by the European Commission, will further drive the demand for MLCCs. These components enable accurate measurement, data processing, and communication within vehicle systems, supporting monitoring of CO2 emissions and energy consumption. Adapting the ZLEV incentive mechanism to reflect sales trends will incentivize the production and purchase of zero-emission vehicles, increasing demand for MLCCs.

The increased adoption of OBFCM devices in Europe also increased the production of passenger vehicles

- In Europe, the production of passenger vehicles witnessed a decline. Starting at a production volume of 18.70 million units in 2019, it decreased to 13.72 million units in 2022, with a CAGR of approximately -8.7% over the four years, mirroring the difficult market conditions and disruptions encountered by the European automotive sector.

- This decline in production can be attributed to various factors, including the temporary closure of manufacturing facilities, reduced consumer purchasing power, and overall market uncertainty caused by the pandemic. However, it is important to note that the European automotive sector has shown resilience and adaptability in the face of adversity.

- With the implementation of the light-duty vehicle CO2 regulation in 2019, there was a renewed focus on reducing emissions and addressing climate change. This regulation emphasizes the need for accurate monitoring of on-road fuel and electric energy consumption, leading to the installation of onboard fuel and energy consumption monitoring devices (OBFCMs) in new vehicles. This regulatory framework creates opportunities for businesses operating in the European MLCC market. MLCCs are essential electronic components used in various applications, including automotive electronics. As vehicles become more sophisticated with the integration of OBFCMs and other monitoring devices, the demand for MLCCs is expected to increase. These components play a crucial role in enabling accurate measurement, data processing, and communication within the vehicle's systems.

- As the industry works toward the integration of advanced technologies, such as OBFCMs, it will play a crucial role in achieving real-world CO2 reductions and ensuring vehicles perform as expected in real-world driving conditions.

Europe MLCC Industry Overview

The Europe MLCC Market is moderately consolidated, with the top five companies occupying 51.04%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Price Trend

- 4.1.1 Copper Price Trend

- 4.1.2 Nickel Price Trend

- 4.1.3 Silver Price Trend

- 4.1.4 Zinc Price Trend

- 4.2 Consumer Electronics Sales

- 4.2.1 Air Conditioner Sales

- 4.2.2 Desktop PC's Sales

- 4.2.3 Gaming Console Sales

- 4.2.4 Laptops Sales

- 4.2.5 Refrigerator Sales

- 4.2.6 Smartphones Sales

- 4.2.7 Storage Unit Sales

- 4.2.8 Tablets Sales

- 4.2.9 Television Sales

- 4.3 Automotive Production

- 4.3.1 Buses and Coaches Production

- 4.3.2 Heavy Trucks Production

- 4.3.3 Light Commercial Vehicles Production

- 4.3.4 Passenger Vehicles Production

- 4.3.5 Total Motor Production

- 4.4 Ev Production

- 4.4.1 BEV (Battery Electric Vehicle) Production

- 4.4.2 PHEV (Plug-in Hybrid Electric Vehicle) Production

- 4.5 Industrial Automation Sales

- 4.5.1 Industrial Robots Sales

- 4.5.2 Service Robots Sales

- 4.6 Regulatory Framework

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

- 5.3 Voltage

- 5.3.1 500V to 1000V

- 5.3.2 Less than 500V

- 5.3.3 More than 1000V

- 5.4 Capacitance

- 5.4.1 100µF to 1000µF

- 5.4.2 Less than 100µF

- 5.4.3 More than 1000µF

- 5.5 Mlcc Mounting Type

- 5.5.1 Metal Cap

- 5.5.2 Radial Lead

- 5.5.3 Surface Mount

- 5.6 End User

- 5.6.1 Aerospace and Defence

- 5.6.2 Automotive

- 5.6.3 Consumer Electronics

- 5.6.4 Industrial

- 5.6.5 Medical Devices

- 5.6.6 Power and Utilities

- 5.6.7 Telecommunication

- 5.6.8 Others

- 5.7 Country

- 5.7.1 Germany

- 5.7.2 United Kingdom

- 5.7.3 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms