|

시장보고서

상품코드

1685798

중국의 화물 및 물류 시장(2025-2030년) : 시장 점유율 분석, 산업 동향, 통계 및 성장 예측China Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

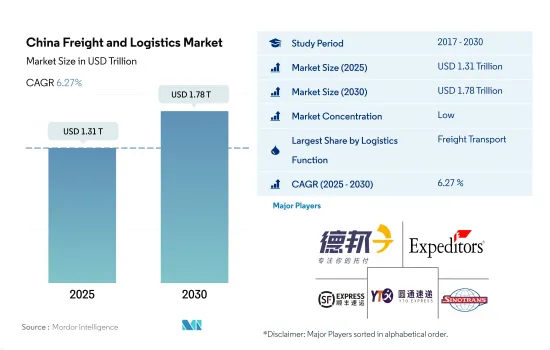

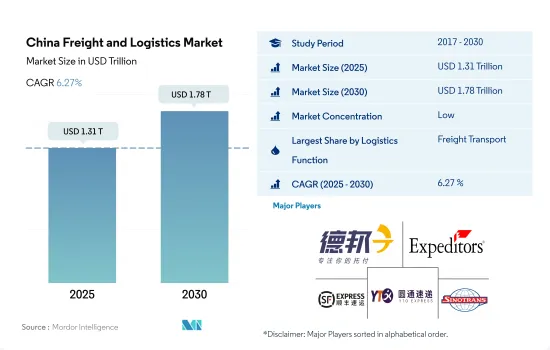

중국의 화물 및 물류 시장 규모는 2025년에 1조 3,100억 달러로 추정 및 예측되고, 2030년에는 1조 7,800억 달러에 이를 전망이며, 예측 기간(2025-2030년) 동안 CAGR 6.27%로 성장할 것으로 예측됩니다.

업계의 왕성한 수요와 완만한 공급으로 자사 물류 서비스 채용 증가

- 2022년, 도시 내 속달편의 누계 취급량은 1,280억건에 달했습니다. 택배 부문은 2022년의 최초 11개월간에 전년 대비 1.6%의 증가를 기록했으며 이는 봉쇄 기간 중 택배 서비스 의존도가 높아진 것에 기인합니다. Cainiao Group은 AliExpress와 협력해, 국제 소포 배송을 신속화할 계획을 발표했습니다.

- 중국은 물류 부문을 강화하고 원활한 공급망을 확보하기 위해 인프라에 대한 투자를 적극적으로 실시했습니다. 개혁위원회는 교통 운수부와 함께 야심찬 도로 확장 목표를 설정하고 있습니다.

중국의 화물 및 물류 시장 동향

제14차 5개년 계획 하에 청정에너지 인프라의 개발과 운수부문에 대한 투자가 성장을 견인합니다.

- 2023년 중국의 청정에너지 부문은 이 나라의 경제 확대에 크게 공헌했습니다. 재생 가능 에너지원, 원자력, 전력망, 에너지저장, 전기자동차(EV), 그리고 철도를 포함한 클린에너지는 2023년에는 중국의 GDP의 9.0%를 차지하면서 전년 대비 7.2%에서 증가했습니다.

- 제14차 5개년 계획(2021-2025년)에서 중국은 교통망 확대 목표를 밝혔으며 고속철도를 38,000km에서 50,000km로 확대하여 인구 50만명 이상의 도시의 95%를 250km 노선으로 연결할 계획입니다. 또한, 철도 노선을 165,000km, 민간공항을 270곳 이상, 도시지하철을 10,000km, 고속도로를 190,000km, 고속 내수로를 18,500km로 증설하는 것을 목표로 하고 있습니다.

러시아-우크라이나 전쟁 중 중국 디젤 가솔린 소매 가격은 역사적으로 높은 수준으로 치솟았습니다.

- 2023년 중국의 원유 수입량은 2022년 대비 11% 증가한 5억 6,399만 톤을 달성했으며 일일 1,128만 배럴에 이르렀습니다. 2024년 1월과 2월에는 5.1% 증가한 8,831만 톤에 이르렀습니다. 이러한 증가는 조기에 낮은 가격으로 원유를 구입하면서 발생했습니다. OPEC+ 그룹이 원유 감산을 6월 말까지 연장한다고 결정하면서 원유가격은 더욱 상승했습니다.

- 중국은 최근 세계적인 원유가격의 변동에 맞추어 가솔린과 경유의 소매가격을 조정할 예정입니다. 중국의 가솔린과 디젤의 가격은 2024년에 톤당 28달러 상승했습니다.

중국의 화물 및 물류 산업 개요

중국의 화물 및 물류 시장은 단편화되고 있으며, 이 시장의 주요 기업은 Deppon Logistics Co., Ltd., Expeditors International of Washington, Inc., SF Express (KEX-SF), Shanghai YTO Express (Logistics) Co., Ltd., 그리고 SINOTRANS(알파벳순)의 5개 사입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 인구 동태

- 경제활동별 GDP 분포

- 경제활동별 GDP 성장률

- 인플레이션율

- 경제성과 및 프로파일

- 전자상거래 산업의 동향

- 제조업의 동향

- 운수 및 창고업의 GDP

- 수출 동향

- 수입 동향

- 연료 가격

- 트럭 운송 비용

- 유형별 트럭 보유 대수

- 물류 실적

- 주요 트럭 공급업체

- 수단 분담률

- 해상화물 운송 능력

- 정기선 해운 연계

- 기항지 및 실적

- 운임 동향

- 화물 톤수 동향

- 인프라

- 규제 프레임워크(도로 및 철도)

- 중국

- 규제 프레임워크(해상 및 항공)

- 중국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 농업, 어업, 임업

- 건설업

- 제조업

- 석유 및 가스, 광업, 채석업

- 도매 및 소매업

- 기타

- 물류 기능

- 택배, 특급 및 소포(CEP)

- 목적지별

- 국내

- 국제

- 화물 수송

- 수송 수단별

- 항공

- 해상 및 내수로

- 기타

- 화물 수송

- 수송 수단별

- 항공

- 파이프라인

- 철도

- 도로

- 해상 및 내수로

- 창고 보관

- 온도 제어 기능별

- 온도 제어 가능

- 온도 제어 불가능

- 기타 서비스

- 택배, 특급 및 소포(CEP)

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Deppon Logistics Co., Ltd.

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- Dimerco

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Expeditors International of Washington, Inc.

- Kuehne Nagel

- SF Express(KEX-SF)

- Shanghai YTO Express(Logistics) Co., Ltd.

- SINOTRANS

- United Parcel Service of America, Inc.(UPS)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(시장 성장 촉진요인, 억제요인 및 기회)

- 기술의 진보

- 정보원과 참고문헌

- 도표 목록

- 주요 인사이트

- 데이터 팩

- 용어집

- 환율

The China Freight and Logistics Market size is estimated at 1.31 trillion USD in 2025, and is expected to reach 1.78 trillion USD by 2030, growing at a CAGR of 6.27% during the forecast period (2025-2030).

Rising adoption of in-house logistics services owing to booming demand and moderate supply in the industry

- In 2022, intra-city express deliveries reached a cumulative volume of 128 billion. The parcel delivery sector saw a 1.6% Y-o-Y revenue increase in the first 11 months of 2022. This uptick was driven by heightened reliance on parcel services during lockdowns, as consumers increasingly turned to online shopping, even for daily essentials. This surge in e-commerce bolstered domestic demand and volume for courier, express, and parcel (CEP) services. In June 2023, Cainiao Group, in collaboration with AliExpress, announced plans to expedite cross-border parcel deliveries, aiming to cut delivery times to five working days, a 30% acceleration from the industry average.

- China is actively investing in infrastructure to bolster its logistics sector and ensure a seamless supply chain. In 2022 alone, the country allocated over USD 3.4 billion for road transport infrastructure improvements. Looking ahead, the National Development and Reform Commission, along with the Ministry of Transport, has set ambitious goals for road expansion. By 2035, they aim to extend the national road network to 299,000 kilometers of highways and 162,000 kilometers of expressways.

China Freight and Logistics Market Trends

Rising focus on developing clean energy infrastructure and transport sector investment under 14th Five-Year Plan driving growth

- In 2023, China's clean energy sector significantly contributed to the country's economic expansion. According to Energy and Clean Air (CREA), China's investment in renewable energy infrastructure amounted to USD 890 billion, almost matching global investments in fossil fuel supply for the same year. Clean energy, including renewable energy sources, nuclear power, electricity grids, energy storage, electric vehicles (EVs), and railways, constituted 9.0% of China's GDP in 2023, up from 7.2% YoY. EV production grew by 36% YoY in 2023.

- In the 14th Five-Year Plan (2021-2025), China revealed goals for expanding its transportation network. By 2025, high-speed railways will extend to 50,000 kms, up from 38,000 kms in 2020, with 95% of cities with populations above 500,000 covered by 250-km lines. The country aims to increase its railway length to 165,000 kms, civil airports to over 270, subway lines in cities to 10,000 kms, expressways to 190,000 kms, and high-level inland waterways to 18,500 kms by 2025. The primary objective is to achieve integrated development by 2025, emphasizing advancements in the transformation of the transportation system and its contribution to GDP.

China's retail diesel and gasoline prices were soared to historically high levels amid the Russia-Ukraine War

- In 2023, China imported 11% more crude oil than in 2022, totaling 563.99 mn metric tons (MMT), or 11.28 mn barrels per day. This surge was due to increased global crude oil prices amid the Russia-Ukraine War, causing fuel prices in China to reach historic highs. In Jan-Feb 2024, crude oil imports rose by 5.1% YoY, reaching 88.31 MMT. This increase was driven by purchasing crude oil at lower prices earlier. Brent futures peaked at USD 97.69 in September 2023, fell to USD 72.29 in December, and rose to USD 84.05 by March 2024. The decision made by the OPEC+ group in March 2024 to extend output cuts until the end of June has further boosted crude prices. This move has raised concerns about global oil demand, as the group is reducing production by nearly 6% of world demand. The recent increase in crude prices may also dampen China's imports starting from H2 2024.

- China plans to adjust retail prices for gasoline and diesel to align with recent shifts in global crude oil prices. The price hike reflects a tightening of global supply and a positive forecast for demand. According to NDRC, gasoline and diesel prices in China will increase by USD 28 per ton in 2024. Although there's expectation of declining demand for fuels, oil-based fuels will remain the primary choice until 2035.

China Freight and Logistics Industry Overview

The China Freight and Logistics Market is fragmented, with the major five players in this market being Deppon Logistics Co., Ltd., Expeditors International of Washington, Inc., SF Express (KEX-SF), Shanghai YTO Express (Logistics) Co., Ltd. and SINOTRANS (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 China

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 China

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Deppon Logistics Co., Ltd.

- 6.4.2 Deutsche Bahn AG (including DB Schenker)

- 6.4.3 DHL Group

- 6.4.4 Dimerco

- 6.4.5 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.6 Expeditors International of Washington, Inc.

- 6.4.7 Kuehne+Nagel

- 6.4.8 SF Express (KEX-SF)

- 6.4.9 Shanghai YTO Express (Logistics) Co., Ltd.

- 6.4.10 SINOTRANS

- 6.4.11 United Parcel Service of America, Inc. (UPS)

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate