|

시장보고서

상품코드

1685958

모빌리티 관리 서비스 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Global Managed Mobility Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

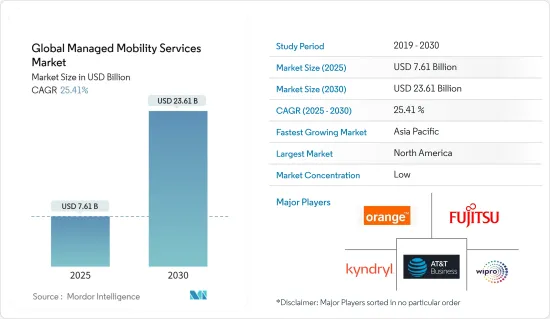

세계의 모빌리티 관리 서비스 시장 규모는 2025년에 76억 1,000만 달러로 추정되고, 2030년에는 236억 1,000만 달러에 달할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 25.41%를 나타낼 전망입니다.

주요 하이라이트

- 모빌리티 관리 서비스 제공업체는 다양한 디바이스 플랫폼의 복잡한 관리를 전문 모바일 애플리케이션에 맞게 해석된 콘텐츠를 통해 처리함으로써 기업 IT 부서의 부담을 덜어주는 솔루션을 제공합니다. 따라서 모빌리티 관리 서비스는 관리, 서버, 데이터베이스와 연결하여 모바일 오피스 직원과 쉽게 커뮤니케이션할 수 있도록 지원합니다. 따라서 기업은 비즈니스 이메일, 데이터베이스 및 기타 기업 콘텐츠에 대해 PC를 통해서만 소통하는 기존 커뮤니케이션의 한계를 극복할 수 있습니다.

- 또한 모빌리티 관리 서비스 솔루션은 전체 모바일 디바이스 수명주기를 관리할 수 있는 단일 파트너를 제공함으로써 기업 담당자의 복잡한 모바일 디바이스 기술 요구사항을 간소화합니다.

- 성숙한 조직이 디지털 연결로 전환함에 따라 직원의 50% 이상이 중앙 집중식 관리가 필요한 업무에 두 개 이상의 디바이스를 사용하고 있습니다.

- 전 세계적으로 의사, 간호사, 환자 및 기타 지원 직원들의 모바일 디바이스 사용이 증가하고 있습니다.

- 고객들은 타사 모빌리티 관리 서비스에 투자하면서 여전히 비용 가시성에 대한 어려움을 겪고 있습니다.

- 전반적으로 코로나19가 전 세계 모빌리티 관리 서비스 시장에 미친 영향은 엇갈리고 있습니다. 팬데믹으로 인해 원격 근무로의 전환으로 인해 MMS 서비스에 대한 수요가 증가한 반면, 공급망에 차질이 생기고 경제 불확실성이 커지면서 일부에서는 투자 감소로 이어지기도 했습니다. 그러나 팬데믹은 전 세계 MMS 시장의 기술 발전을 가속화하여 새롭고 혁신적인 솔루션으로 이어졌습니다.

모빌리티 관리 서비스 시장 동향

IT 및 통신 최종 사용자 산업 부문이 상당한 시장 점유율을 차지

- IT 및 통신 분야는 매니지드 서비스의 중요한 시장입니다. 다양한 기술 도입률이 높기 때문에 엔터프라이즈 모빌리티 트렌드가 수년에 걸쳐 부상했습니다. 오늘날 기업들은 주로 비즈니스 전략과 핵심 역량에 초점을 맞추면서 BYOD(Bring-Your-Own-Device)의 활용과 도입을 촉진하고 있습니다.

- 게다가 중국, 인도, 브라질과 같은 신흥 국가에서 모바일 가입자 기반이 증가함에 따라 업무 효율성과 운영의 유연성을 향상시키는 BYOD 정책 도입이 촉진되고 있습니다.

- 코로나19 팬데믹으로 인한 정부 규제와 봉쇄 조치로 인해 전 세계적으로 관리형 클라우드 서비스에 대한 수요가 증가하면서 모빌리티 관리 서비스가 더욱 활성화되고 기업들이 원격 근무 모드로 전환하면서 기업들이 클라우드 기반 솔루션을 도입하여 요구 사항을 확대하고 있습니다.

- 주 및 지방 정부, 규제 기관에서 요구하는 사이버 보안 규정 준수 요건 또한 모빌리티 관리 서비스 애플리케이션 서비스가 보안에 중점을 두어야 할 필요성을 높이고 있습니다.

- 하드웨어 장치, 임베디드 소프트웨어, 통신 서비스를 연결하는 모빌리티 관리 서비스에 IoT 솔루션을 도입하면 스마트 통신 환경, 스마트 교통, 스마트 홈, 스마트 헬스케어가 제공되며 예측 기간 동안 시장을 주도할 것으로 예상됩니다.

예측 기간 동안 주요 점유율을 차지할 북미 지역

- Cisco의 연례 인터넷 보고서에 따르면 2023년 말에는 전 세계 1인당 평균 디바이스 및 연결 수가 3.6개로 증가할 것으로 예상됩니다.

- 또한, 미국 내 5G 보급률은 향후 IoT 디바이스에 대한 수요를 촉진할 것으로 예상됩니다. AT&T, 스프린트, T 모바일, 버라이즌과 같은 국내 모바일 사업자들이 5G 구축에 집중하면서 수년 동안 상당한 발전을 이루었습니다. GSMA에 의하면, 5G는 2023년 초에 1억건의 모바일 접속에 도달해, 2025년에는 1억 9,000만건 이상의 5G 접속으로 국내를 리드하는 모바일 네트워크 기술이 됩니다.

- 클라우드와 디지털 혁신으로 인해 데이터 유출로 인한 총 비용이 증가했습니다. 포네몬 연구소의 '데이터 유출 비용 연구'에 따르면 데이터 유출로 인한 전 세계 평균 피해액은 383만 달러였습니다. 그러나 미국의 평균 데이터 유출 비용은 864만 달러로 상당히 높았습니다.

- 캐나다 모빌리티 관리 서비스 시장은 코로나19 팬데믹으로 인한 업무 문화로 인해 투자가 더욱 증가하고 있습니다. 예를 들어, 2021년 9월 MSP Corp Investments Inc.는 캐나다 전역의 관리형 IT 서비스 제공업체(MSP)를 인수하고 투자하기 위해 3,500만 달러의 성장 자본을 조달했습니다.주요 재정 후원자로는 CIBC와 BDC Capital의 Growth Equity Partners - Fund II가 있습니다. 이 회사는 캐나다의 우수한 MSP와 파트너십을 맺고 인수하여 기술, 리소스, 비즈니스 지원을 제공함으로써 MSP 팀의 역량을 강화합니다. 이 회사의 주요 중점 분야로는 관리형 네트워크 서비스, 모빌리티 관리, 사이버 보안, 클라우드 호스팅 등이 있습니다.

- 인더스트리 4.0 구상이 세계적으로 가져온 디지털 트렌드는 산업용 IoT의 필요성을 주도하고 있습니다. 예를 들어, 2021년 5월 토론토에 본사를 둔 스타트업인 BehrTech는 2020년에 개발한 IoT용 무선 연결 제품으로 상을 받았습니다.

모빌리티 관리 서비스 업계 개요

모빌리티 관리 서비스 시장은 세분화되어 AT&T Intellectual Property, 후지쯔, Kyndryl Inc., Wipro, Orange SA 등 대기업이 존재합니다.

- 2023년 2월 : 킨들리랜드 노키아가 글로벌 네트워크 및 에지 컴퓨팅 연합을 확장했습니다. 3년간의 계약을 통해 유연하고 신뢰할 수 있으며 안전한 LTE 및 5G 사설 무선 연결 서비스와 인더스트리 4.0 솔루션에 대한 협력 계획을 확대하고 배포를 가속화할 계획입니다.

- 2023년 3월 : Wipro가 '5G Def-I' 플랫폼을 공식 출시했습니다. 모빌리티 시장의 기업들이 인프라, 네트워크, 서비스를 원활하게 혁신할 수 있도록 지원하는 이 통합 플랫폼은 MWC 바르셀로나 패널에서 첫 선을 보이며 커넥티드 엔터프라이즈의 목표를 실현했습니다. 또한 실행 가능한 비즈니스 인사이트를 창출하기 위한 인텔리전스 계층도 포함되어 있습니다. 또한 엔드포인트 디바이스에 대한 가시성 및 데이터 인사이트, 네트워크 사업자를 위한 빠른 서비스 구현, 새로운 엔터프라이즈 애플리케이션의 신속한 배포도 포함됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자 및 소비자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업간 경쟁 관계

- 대체품의 위협

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 여러 산업에서 BYOD 채택 증가

- IT 활동을 아웃소싱하는 기업

- 시장 성장 억제요인

- 운영 및 비용 가시성에 대한 통제력 부족

제6장 시장 세분화

- 기능별

- 모바일 디바이스 관리

- 모바일 애플리케이션 관리

- 모바일 보안

- 기타 기능

- 전개별

- 클라우드

- 온프레미스

- 최종 사용자 업계별

- IT 및 통신

- BFSI

- 헬스케어

- 제조업

- 소매

- 교육

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 아르헨티나

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제7장 경쟁 구도

- 기업 프로파일

- AT&T Intellectual Property

- Fujitsu

- Kyndryl Inc.

- Wipro

- Orange SA

- Telefonica SA

- Samsung Electronics Co. Ltd

- Hewlett Packard Enterprise

- Vodafone Group PLC

- Microsoft Corporation

- Tech Mahindra

제8장 투자 분석

제9장 시장의 미래

HBR 25.04.24The Global Managed Mobility Services Market size is estimated at USD 7.61 billion in 2025, and is expected to reach USD 23.61 billion by 2030, at a CAGR of 25.41% during the forecast period (2025-2030).

Key Highlights

- The managed mobility service providers offer solutions that ease the burden on enterprise IT departments by dealing with complex managing of various device platforms, with the help of interpreted content for specialized mobile applications. Therefore, managed mobility services enable easy communication with mobile office workers by connecting them with management, servers, and databases. Thus, it allows enterprises to overcome the traditional communications that involve PC only for business emails, databases, and other corporate content.

- Furthermore, mobility as a service solution simplifies corporate personnel's complex mobile device technology needs by offering a single partner to manage the whole mobile device lifecycle. Thus, these companies take the hassle of managing mobile technology so that IT teams can save resources and time to focus on the strategic initiatives that are helping them to transform their businesses.

- The growing shift of mature organizations toward digital connectivity drives at least 50% of employees to use more than one device for work that demands centralized management. Thus, the rise of new types of carrier devices continues to flood workplaces and expand the mobility ecosystem, driving the need for experienced MMS providers to handle the complexity of communication across organizations.

- The use of mobile devices among doctors, nurses, patients, and other supporting staff has increased worldwide. Moreover, organizations in the healthcare end-user industry must adhere to HIPAA regulations for data sharing and storage. These factors are expected to drive the adoption of managed mobility services in the healthcare industry.

- Customers are still witnessing challenges for cost visibility as they invest in the third-party managed mobility service. Some vendors lack the expertise to estimate the total costs or the capacity or resources in order to add individual parameters to arrive at an estimated cost manually. Such challenges add a drawback to the market.

- Overall, the impact of COVID-19 on the global managed mobility services market has been mixed. While the pandemic has increased demand for MMS services due to the shift toward remote work, it has also caused disruptions to supply chains and economic uncertainties, leading to a decrease in investment in some cases. However, the pandemic has also accelerated technological advancements in the global MMS market, leading to new and innovative solutions. The market for MMS services is expected to grow in the long term as companies look for ways to increase efficiency and adapt to changing business environments.

Managed Mobility Services Market Trends

IT and Telecom End-user Industry Segment Holds Significant Market Share

- The IT and telecom sector is a significant market for managed services. Due to the high rate of various technological adoptions, the enterprise mobility trend has emerged over the years. Today, companies primarily focus on business strategies and core competencies, fueling the utilization and adoption of bring-your-own-device (BYOD). This increases the requirement for streamlined mobility services, likely to boost the demand for managing these mobile devices.

- Furthermore, the growing mobile subscriber base in emerging countries, such as China, India, and Brazil, has been propelling the adoption of BYOD policies, enhancing work efficiency and flexibility in operations. According to a Cisco report, enterprises with a BYOD policy save, on average, USD 350 per year per employee. Moreover, reactive programs can boost these savings to USD 1,300 per year per employee.

- The demand for managed cloud services has increased across the globe due to government regulations and lockdown measures due to the COVID-19 pandemic, further boosting the managed mobility services and forcing businesses to move towards remote working modes, which has led companies to adopt cloud-based solutions to expand their requirements.

- Cybersecurity compliance requirements mandated by the state and local governments and regulatory bodies also drive the need for managed mobility application services to be security-focused. Additionally, as dedicated, on-premise hardware for computing purposes will decrease, and most of the functionality will become cloud-based, privacy and security issues will become more intense.

- Adopting IoT solutions in managed mobility services, which connect hardware devices, embedded software, and communication services, offers smart communication environments, smart transportation, smart homes, and smart healthcare and is expected to drive the market during the forecast period.

North America to Hold Major Share over the Forecast Period

- According to the annual internet report by Cisco, the average number of devices and connections per capita worldwide is anticipated to increase to 3.6 by the end of the year 2023. Among the countries with the highest average per capita devices and connections by 2023, the United States is expected to remain at the top with an average of 13.6 devices and connections per capita, followed by South Korea and Japan.

- Moreover, the 5G penetration in the country also encourages the demand for IoT devices in the future. The focus on deploying 5G by national mobile operators, like AT&T, Sprint, T mobile, and Verizon, has led to significant developments over the years. According to the GSMA, 5G will reach 100 million mobile connections in early 2023 and become the country's leading mobile network technology by 2025, with more than 190 million 5G connections.

- Cloud and digital transformation have increased the total cost of a data breach. The use of mobile platforms, extensive cloud migration, and IoT devices are the drivers increasing the cost. According to the Ponemon Institute's "Cost of Data Breach Study," the global average for a data breach was USD 3.83 million. However, the average data breach cost in the United States was significantly high at USD 8.64 million. The high potential of data breaches is expected to drive the managed mobile services market as enterprises focus more on IT security.

- The Canadian managed mobility services market is witnessing increased investments further driven by the COVID-19 pandemic-induced work culture. For instance, in September 2021, MSP Corp Investments Inc. raised USD 35 million in growth capital to acquire and invest in managed IT services providers (MSPs) across Canada. Major financial backers include CIBC and BDC Capital's Growth Equity Partners - Fund II. The company partners and acquires high-performing MSPs in the country to deliver technology, resources, and business support to empower MSP teams. Key areas of focus of the company include managed network services, mobility management, cybersecurity, and cloud hosting.

- The digital trends brought globally by the Industry 4.0 initiatives also drive the need for industrial IoT. For instance, in May 2021, Toronto-based BehrTech, a startup, was awarded for its wireless connectivity products for the IoT that the company developed in 2020, and the company also received a USD 3 million grant from a joint funding program between the federal government and a non-profit organization to build an Industry 4.0 lab.

Managed Mobility Services Industry Overview

The managed mobility services market is fragmented, with the presence of major players like AT&T Intellectual Property, Fujitsu, Kyndryl Inc., Wipro, and Orange SA. Players in the market are adopting strategies such as partnerships, agreements, innovations, and acquisitions to enhance their service offerings and gain sustainable competitive advantage.

- February 2023: Kyndryland Nokia expanded its global network and edge computing alliance. The three-year agreement extends plans to collaborate on and accelerate the deployment of flexible, dependable, and secure LTE and 5G private wireless connectivity services, as well as Industry 4.0 solutions. Furthermore, Kyndryl increases its strategic investment in Nokia by achieving the highest tier Nokia Digital Automation Cloud (DAC) accreditation status, increasing expert resources and skilled practitioners ready to support customers worldwide. Kyndryland Nokia opened a partner innovation lab in Raleigh, North Carolina. The lab will integrate advanced wireless connectivity and edge computing with a multi-factor zero trust model, converging IT and OT for enterprises.

- March 2023: Wipro officially launched its "5G Def-I" platform. The integrated platform, which enables businesses in the mobility market to transform their infrastructure, networks, and services seamlessly, debuted at the MWC Barcelona panel, realizing the connected enterprise's goals. Wipro's 5G Def-iplatform, built on open standards, offers the cloud-native environment, network APIs, and third-party integrations required for businesses to onboard existing infrastructure, incubate new apps and services, and keep up with technological changes. The integrated suite combines cloud scalability with 5G speed and capacity. It also includes an intelligence layer for creating actionable business insights. It also includes visibility into endpoint devices and data insights, faster service implementation for network operators, and rapid deployment of new enterprise applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of BYOD in Multiple Industries

- 5.1.2 Companies Outsourcing IT Activities

- 5.2 Market Restraints

- 5.2.1 Lack of Control over Operations and Cost Visibility

6 MARKET SEGMENTATION

- 6.1 By Function

- 6.1.1 Mobile Device Management

- 6.1.2 Mobile Application Management

- 6.1.3 Mobile Security

- 6.1.4 Other Functions

- 6.2 By Deployment

- 6.2.1 Cloud

- 6.2.2 On-premise

- 6.3 By End-user Industry

- 6.3.1 IT and Telecom

- 6.3.2 BFSI

- 6.3.3 Healthcare

- 6.3.4 Manufacturing

- 6.3.5 Retail

- 6.3.6 Education

- 6.3.7 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AT&T Intellectual Property

- 7.1.2 Fujitsu

- 7.1.3 Kyndryl Inc.

- 7.1.4 Wipro

- 7.1.5 Orange SA

- 7.1.6 Telefonica SA

- 7.1.7 Samsung Electronics Co. Ltd

- 7.1.8 Hewlett Packard Enterprise

- 7.1.9 Vodafone Group PLC

- 7.1.10 Microsoft Corporation

- 7.1.11 Tech Mahindra