|

시장보고서

상품코드

1686611

원자로 해체 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Nuclear Power Reactor Decommissioning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

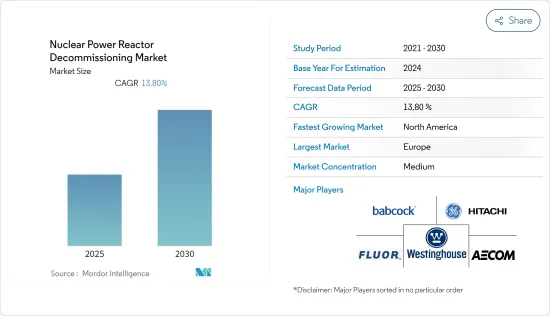

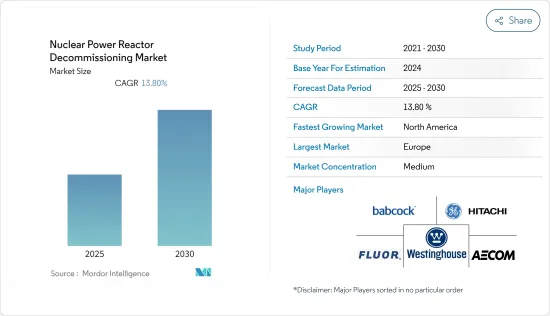

원자로 해체 시장은 예측 기간 동안 13.8%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측됩니다.

이 시장은 2020년 COVID-19 팬데믹에 의해 중간 정도의 영향을 받았지만, 회복되고 있으며, 팬데믹 이전 수준에 이르고 있습니다.

시장의 성장을 가속하는 주요 요인은 운전 정년을 맞이하는 원자로 증가, 신재생 전원(ie 풍력 및 태양광)의 가격 저하, 환경 문제에 대한 감도 증가입니다.

그러나 정부의 호의적인 정책으로 인한 원자력 발전소의 수명 연장은 시장 성장을 방해할 것으로 예상됩니다.

독일, 영국, 한국 등 몇 개국의 탈원발 정책은 폐로시장을 발전시키기 위해 필요한 전문지식을 국가의 요구에 맞추어 제공하는 국내외 기업에 기회를 가져올 것으로 예상됩니다.

북미는 원자로 해체에서 가장 급성장하고 있는 시장이 될 것으로 예상되며, 미국은 이 지역에서 중요한 해체 핫스팟 중 하나입니다.

원자로 해체 시장 동향

상업로 부문이 시장을 독점할 전망

2022년 10월 현재, 32개국에서 437기의 상업용 원자력 발전소가 가동되고 있습니다. 미국은 가장 큰 원자력 발전 능력을 가지고 있으며 다른 어떤 국가보다 원자력 발전량이 더 많습니다. 프랑스는 원자력 발전 용량이 두 번째로 크고 원자력 발전량도 두 번째로 많습니다.

상업용 원자력 발전소의 정지와 폐로에는 경제적 요인, 규제적 요인, 사회적 요인 등 몇 가지 요인이 얽혀 있습니다. 운전 수명의 종료나, 태양광 및 풍력이라고 하는 대체 에너지 발전원의 비용 저하라고 하는 일차 정보가, 원자력 에너지의 비용 경합력을 저하시켰습니다. 2011년의 후쿠시마 원자력 발전 사고 후, 전세계에서 원자력의 안전 프로토콜이 업그레이드되어 인프라 업그레이드, 운전 및 보수 비용 증가에 따른 추가 비용이 발생했습니다. 이 때문에 많은 오래된 상업용 원자로 운전자들은 운전 수명이 40년이고 인프라 업그레이드에 따라 20년 더 연장할 수 있는 오래된 원자로를 해체하는 것을 선택하고 있습니다.

세계 각국의 정부에 의한 정책 수준의 대처도 원자로 해체로 이어지고 있습니다. 많은 국가의 정부가 자국의 에너지 믹스에 있어서의 원자력의 삭감을 계획했습니다. 이러한 규제정책은 재생 에너지가 충실하고 상업용 원자력발전소를 운전하는 것에 따른 환경영향 및 잠재적 위험에 대해 심각한 우려를 갖고 있는 서구 국가들에서 널리 볼 수 있습니다.

독일은 국책으로 2022년 말까지 모든 원자로를 정지할 예정입니다. 2017년 스위스는 국내 원자력 발전소의 단계적 폐지를 결의했습니다. 2020년 9월 벨기에 정부는 2025년까지 단계적으로 원전을 폐지할 것을 재확인하는 협정에 서명했습니다. 스페인은 가동 중인 상업용 원자로 7기 중 4기를 2030년까지 폐쇄하고 나머지 3기를 향후 5년 이내에 폐쇄하며 2035년까지 원자력 발전을 완전히 폐지하겠다고 선언했습니다.

신재생 에너지 기술의 개발과 경제성의 향상으로 원자력 발전은 대규모 발전을 이루고 있습니다. 전 세계 국가들이 신재생 에너지와 관련된 거대한 인프라를 구축하고 있으며, 그것이 원자로의 필요성을 상쇄하고 있습니다. 원자력 발전은 신재생 에너지 발전으로 대체되고 있으며, 그것이 원자로 해체로 이어지고 있습니다. 따라서 신재생 에너지원 개발의 급증은 세계 원자로 해체 시장에 큰 뒷받침이 되고 있습니다.

따라서 앞서 언급한 요인들로부터 예측기간 동안 상업용 원자로가 조사 대상 시장을 독점할 것으로 예상됩니다.

북미가 큰 성장을 이룰 전망

북미는 세계에서 운전할 수 있는 원자로의 수가 가장 많은 지역 중 하나입니다. 원자로 해체 시장은 미국, 캐나다, 멕시코로부터의 수요에 의해 큰 성장이 전망되고 있습니다.

미국은 최대급의 원자력 발전국으로 2021년에는 세계의 원자력 발전량의 30%를 차지했습니다. 이 나라의 원자로는 2021년에 778.15TWh의 전력을 생산했으며, 2020년부터 1.48%로 미감되었습니다.

2022년 8월 현재 미국에서는 30개 주에서 총 94.7GWe의 용량을 가진 92기의 원자로가 가동되고 있으며, 30개사의 전력회사에 의해 사용되고 있습니다. 2기의 원자로가 건설 중이며, 합계 용량은 223만 kWe입니다.

미국에서는 원자력의 시대가 끝나면서 원자력발전소의 폐로는 중요한 산업이 되고 있습니다. 비공개 회사가 이러한 원자력 발전소를 인수하고 라이센스, 배상 책임, 폐로 자금, 폐기물 계약을 인계하고 있습니다. 총 용량 1997만kW의 약 41기의 원자로가 정지되었고, 최신의 것은 2022년 5월에 정지한 미시간주의 팰리세이즈 원전입니다. 2021년 12월, 홀텍 인터내셔널은 미시간주 코버트에 있는 팰리세이즈 원전을 취득해 폐로 및 해체하기 위한 인가를 원자력 규제 위원회로부터 받았습니다. 2030년까지 약 198기의 원자로가 정지할 것으로 예상되고 있습니다.

미국의 원자로는 노후화하고 있습니다.미국 원자력 규제 위원회(NRC)는 후속 라이선스 갱신(SLR) 프로그램에 의해 60년부터 80년을 넘어 운전 라이선스를 연장하는 신청을 검토하고 있습니다. 그러나 최근 2045-2050년 조기 은퇴를 선택한 원전 소유자도 있습니다.

저비용 셰일가스를 이용한 발전과의 격렬한 경쟁이 국내 원자력 산업의 경쟁력을 손상시켰습니다. 기록적인 낮은 도매전력 가격과 고비용연명(PLEX) 업그레이드가 맞물려 원자력 발전소의 조기 은퇴를 앞당겼습니다.

오랜 세월 동안 캐나다는 원자력 연구와 기술의 리더였으며 캐나다에서 개발된 원자로 시스템을 수출해 왔습니다. 2021년 캐나다의 원자력 발전소에 의한 발전량은 92.6TWh로 총 발전량의 약 15%를 차지했습니다. 온타리오주에서는 운전 가능한 원자로 19기(합계용량 13,624MW) 및 원자로 6기(합계용량 214만kW)가 2022년 8월에 정지되었습니다.

2022년 8월 현재 캐나다에는 더 이상 사용되지 않는 다양한 연구용 원자로와 원형로가 있습니다. 이 원자로들은 안전한 보관 상태에 있으며 최종적인 폐로를 기다리고 있습니다. 이러한 원자로에는 WR-1, 초크 리버 연구소(CRL)의 NRX 원자로, CRL의 MAPLE-1 및 MAPLE-2(다목적 용도 물리 격자 실험) 원자로, QC주 베칸쿠르의 젠틸리1 원자력 발전소, ON주 롤프톤의 원자력 발전 실증(NPD) 원자로, ON주 킨카다인의 더글러스 포인트 원자력 발전소 등이 있습니다. 이들은 예측 기간 동안 캐나다 원자로 해체 시장의 수요를 견인할 것으로 예상됩니다.

따라서 북미는 예측 기간 동안 원자로 해체 시장에서 큰 성장을 보일 것으로 기대됩니다.

원자로 해체 업계 개요

원자로 해체 시장은 적당히 단편화되고 있습니다. 이 시장의 주요 기업에는, Babcock International Group PLC, Fluor Corporation, GE Hitachi Nuclear Services, AECOM, Westinghouse Electric Company 등이 있습니다.(순부동)

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 조사 전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 시장 규모 및 수요 예측2027년)

- 원자력 발전량의 예측

- 최근 동향 및 개발

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 원자로 유형별

- 가압수형 원자로

- 가압수형 중수로

- 끓는 물형 원자로

- 고온가스로

- 액체 금속 고속 증식로

- 기타 원자로

- 용도별

- 상업용 동력로

- 프로토타입로

- 연구로

- 용량별

- 100MW 이하

- 100-1000 MW

- 1000MW 이상

- 지역별

- 북미

- 아시아태평양

- 유럽

- 남미

- 중동 및 아프리카

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 주요 기업의 전략

- 기업 프로파일

- Babcock International Group PLC

- James Fisher & Sons PLC

- NorthStar Group Services Inc.

- Fluor Corporation

- GE Hitachi Nuclear Services

- Studsvik AB

- Enercon Services Inc.

- Orano Group

- Aecom

- Bechtel Group Inc.

- Westinghouse Electric Company

제7장 시장 기회 및 향후 동향

AJY 25.04.29The Nuclear Power Reactor Decommissioning Market is expected to register a CAGR of 13.8% during the forecast period.

Although the market studied was moderately impacted by the COVID-19 pandemic in 2020, it has been recovering and reached pre-pandemic levels.

The major factors driving the market's growth are the increasing number of nuclear reactors reaching operational retirement, declining prices of renewable power generation sources (i.e., wind and solar), and growing sensitivity toward environmental issues.

However, the lifetime extension of nuclear power plants with favorable government policies is expected to hinder the market's growth.

Nuclear phase-out policies in several countries, such as Germany, the United Kingdom, and South Korea, are expected to create opportunities for foreign and domestic players to provide the necessary expertise for the country's needs to develop their decommissioning market.

North America is expected to be the fastest-growing market for nuclear power reactor decommissioning, with the United States being one of the significant decommissioning hotspots in the region.

Nuclear Power Reactor Decommissioning Market Trends

Commercial Reactors Segment is Expected to Dominate the Market

As of October 2022, 437 commercial nuclear power plants were in operation across 32 countries. The United States had the largest nuclear electricity generation capacity and generated more nuclear electricity than any other country. France has the second-largest nuclear electricity generation capacity and second-highest nuclear electricity generation.

Several factors are responsible for the shutdown and decommissioning of commercial nuclear power plants, including economic, regulatory, and social factors. Some primary factors, such as the end of operational life and the fall in the cost of alternative energy generation sources, like solar and wind, made nuclear energy less cost-competitive. Following the Fukushima disaster of 2011, nuclear safety protocols have been upgraded across the world, which levied additional costs for the upgradation of infrastructure and increased operations and maintenance costs. Due to this, operators of many older commercial reactors, which have an operating life of 40 years and can be extended by 20 more years with infrastructural upgrades, are opting to decommission older units.

The policy-level initiatives from governments across the world have also led to the shutdown of nuclear power plants. The governments in many countries planned to reduce nuclear power in the energy mix of their countries. Such regulatory policies are prevalent among Western European states with a strong renewable portfolio and serious concerns about the environmental footprint and potential risk of operating commercial nuclear power plants.

As per its national policy, Germany plans to shut down all its reactors by the end of 2022. In 2017, Switzerland voted to phase-out nuclear power plants from the country. In September 2020, the Belgian government signed an agreement reaffirming its commitment to phasing-out nuclear power by 2025. Spain declared that it will close four of its seven operating commercial reactors by 2030 and close the rest three reactors within the next five years, completely phasing out nuclear generation by 2035.

The development of renewable energy technologies and increasing economic viability have led to its massive development. Countries across the world are creating huge infrastructures pertaining to renewable power, which has offset the requirement for nuclear reactors. Nuclear power generation is being replaced by renewable energy sources, which led to the closure of nuclear reactors. Therefore, the surge in the development of renewable energy sources is a big boost for the global nuclear reactor decommissioning market.

Therefore, due to the aforementioned factors, commercial rectors are expected to dominate the market studied during the forecast period.

North America is Expected to Witness Significant Growth

North America is one of the largest regions in terms of operable reactors worldwide. The nuclear power reactor decommissioning market is expected to witness significant growth due to the demand from the United States, Canada, and Mexico.

The United States is one of the largest nuclear power producers, accounting for 30% of the global nuclear power generated in 2021. The country's nuclear reactors produced 778.15 TWh of electricity in 2021, representing a slight decline of 1.48% from 2020.

As of August 2022, the United States has 92 operating nuclear power reactors with a combined capacity of 94.7 GWe in 30 states, used by 30 different power companies. Two reactors are under construction with a total of 2.23 GWe.

As the era of nuclear power winds down in the United States, the decommissioning of nuclear power plants is becoming a significant industry. Private companies are acquiring these plants, taking over their licenses, liability, decommissioning funds, and waste contracts. Around 41 reactors with a combined capacity of 19.97 GW were shut down, the latest being the Palisades nuclear plant in Michigan shut down in May 2022. In December 2021, HoltecInternational received approval from the Nuclear Regulatory Commission to acquire the Palisades plant in Covert, Michigan, to decommission and dismantle the plant. Around 198 reactors are expected to shut down by 2030.

The nuclear reactor fleet of the United States is aging. The United States Nuclear Regulatory Commission (NRC) is considering applications for extending operating licenses beyond 60 to 80 years with its subsequent license renewal (SLR) program. However, some plant owners recently opted for early retirement of their nuclear units at 45 to 50 years old.

Intense competition from electricity generation using low-cost shale gas hurt the competitiveness of the nuclear power industry in the country. Record low wholesale electricity prices and the high cost of life extension (PLEX) upgrades have together driven early nuclear plant retirements.

For many years, Canada has been a leader in nuclear research and technology, exporting reactor systems developed in Canada. In 2021, Canada generated 92.6 TWh of electricity from nuclear power plants, accounting for about 15% of the total electricity generation mix. In Ontario, 19 operable reactors with a combined capacity of 13,624 MW and around six reactors with a combined capacity of 2.14 GW were shut down in August 2022.

As of August 2022, Canada has a variety of research and prototype power reactors that are no longer in use and have been shut down. These reactors are in a safe storage state and awaiting final decommissioning. Some of these reactors include the WR-1, the NRX reactor at Chalk River Laboratories (CRL), the MAPLE-1 and MAPLE-2 (Multipurpose Applied Physics Lattice Experiment) reactors at CRL, the Gentilly-1 nuclear generating station in Becancour, QC, the Nuclear Power Demonstration (NPD) reactor in Rolphton, ON, and the Douglas Point nuclear-generating station in Kincardine, ON. These are expected to drive the demand for the Canadian nuclear power reactor decommissioning market during the forecast period.

Therefore, North America is expected to witness significant growth in the nuclear power reactor decommissioning market during the forecast period.

Nuclear Power Reactor Decommissioning Industry Overview

The nuclear power reactor decommissioning market is moderately fragmented. Some of the major players in the market (in no particular order) are Babcock International Group PLC, Fluor Corporation, GE Hitachi Nuclear Services, AECOM, and Westinghouse Electric Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD million, till 2027

- 4.3 Nuclear Power Generation Forecast in TWh, till 2027

- 4.4 Recent Trends and Developments

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Reactor Type

- 5.1.1 Pressurized Water Reactor

- 5.1.2 Pressurized Heavy Water Reactor

- 5.1.3 Boiling Water Reactor

- 5.1.4 High-temperature Gas-cooled Reactor

- 5.1.5 Liquid Metal Fast Breeder Reactor

- 5.1.6 Other Reactor Types

- 5.2 By Application

- 5.2.1 Commercial Power Reactor

- 5.2.2 Prototype Power Reactor

- 5.2.3 Research Reactor

- 5.3 By Capacity

- 5.3.1 Below 100 MW

- 5.3.2 100-1000 MW

- 5.3.3 Above 1000 MW

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Asia-Pacific

- 5.4.3 Europe

- 5.4.4 South America

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Babcock International Group PLC

- 6.3.2 James Fisher & Sons PLC

- 6.3.3 NorthStar Group Services Inc.

- 6.3.4 Fluor Corporation

- 6.3.5 GE Hitachi Nuclear Services

- 6.3.6 Studsvik AB

- 6.3.7 Enercon Services Inc.

- 6.3.8 Orano Group

- 6.3.9 Aecom

- 6.3.10 Bechtel Group Inc.

- 6.3.11 Westinghouse Electric Company