|

시장보고서

상품코드

1690090

유럽의 소형 위성 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Small Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

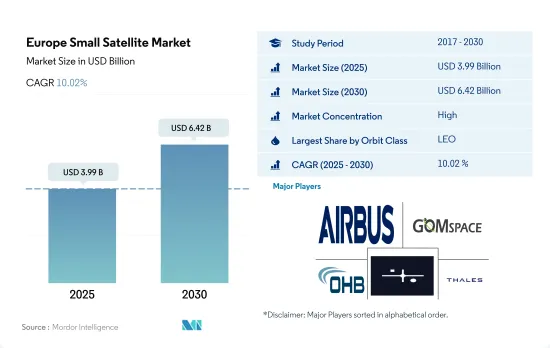

유럽의 소형 위성 시장 규모는 2025년에 39억 9,000만 달러에 이를 것으로 추정됩니다. 2030년에는 64억 2,000만 달러에 달하고, 예측 기간 중(2025-2030년)의 CAGR은 10.02%를 나타낼 것으로 전망됩니다.

2029년에는 LEO 위성이 98.8%의 주요 시장 점유율을 차지할 것으로 전망

- 소형 위성은 과학연구에서 상업·군사이용에 이르기까지 폭넓은 용도로 우주에 대한 저비용 접근을 가능하게 하여 최근 우주산업에 혁명을 가져왔습니다. 소형 위성의 가능성을 충분히 발휘하기 위해서는 발사 가능한 궤도의 유형을 이해하는 것이 필수적입니다.

- 예를 들어, LEO는 소형 위성에 가장 흔한 궤도이며, 지상과의 저지연 통신 링크를 제공하고, 전송, 원격 감지, 지구 관측 등 실시간 데이터 전송이 필요한 용도에 이상적인 등 많은 이점이 있습니다. 이 지역에서는 2017년부터 2022년까지 총 504대의 위성이 LEO로 발사되었습니다. 이들 531기의 위성 중 443기 가까이 통신 목적으로 발사되었습니다.

- 한편, GEO 궤도에 있는 위성은 지상에서는 거치형으로 보이기 때문에 GEO는 주로 통신·방송 용도에 사용됩니다. 따라서 대륙과 해역 등 특정 지역을 지속적으로 커버할 수 있습니다. 유럽에서는 인텔 새트와 같은 기업이 소형 위성의 별자리를 발사하여 고객에게 통신 서비스를 제공합니다.

- MEO는 소형 위성의 궤도로는 많이 사용되지 않는 궤도입니다. MEO는 고도가 높기 때문에 LEO에 비해 커버 영역이 넓고, 기술 실증이나 네비게이션/GPS와 같이 전 지구를 커버할 필요가 있는 용도에 중요합니다. 이러한 진보로 2029년까지 이 부문의 성장률은 88%에 달하고 2023년의 숫자를 상회할 것으로 예측되고 있습니다.

유럽의 소형 위성 시장 동향

연료 효율과 운영 효율 향상이 주요 동향이 될 전망

- 우주선의 질량별 분류는 로켓의 크기와 위성을 궤도에 발사하는 비용을 결정하는 주요 지표 중 하나입니다. 위성 임무의 성공은 비행 전의 질량 측정의 정확성과 한계 내에서 질량을 발생시키는 위성의 적절한 균형에 크게 의존합니다.

- 위성은 질량에 따라 분류됩니다. 질량이 500kg 미만인 위성을 소형 위성이라고 합니다. 이 지역에서는 2017-2022년에 약 460대의 소형 위성이 발사되었습니다. 개발 기간이 짧기 때문에 전체 임무 비용을 줄일 수 있기 때문에이 지역에서는 소형 위성에 대한 경향이 커지고 있습니다. 이를 통해 과학적 및 기술적 성과를 얻는 데 필요한 시간을 대폭 단축할 수 있게 되었습니다. 소형 위성의 임무는 유연하기 때문에 새로운 기술적 기회와 요구에 더 잘 대응할 수 있는 경향이 있습니다. 유럽의 소형 위성 시장은 특정 용도에 맞는 소형 위성을 설계 및 제조하기 위한 견고한 틀의 존재에 의해 지원되고 있습니다. 유럽에서의 운영 횟수는 상업 및 군사 우주 분야에서 수요 증가로 견인되어 2023년에서 2029년까지 증가할 것으로 예상됩니다.

각 우주 기관의 우주 개발비 증가가 유럽의 소형 위성 시장에 긍정적인 영향을 미칠 전망

- 유럽의 소형 위성 시장은 기술 발전, 투자 증가, 소형 위성 서비스 수요 증가로 최근 급성장하고 있습니다. 초소형 위성과 초소형 위성은 기존 위성보다 작고 비용 효율적이어서 광범위한 조직과 기업이 쉽게 이용할 수 있습니다.

- 예를 들어, 2020년 12월 IABG와 BMW Wi는 고해상도 카메라, 이미지 센서, 이미지 컨버터를 탑재한 위성을 제작하기 위해 2억 3,000만 유로의 계약을 체결했습니다. 이 신기술은 2022년 말까지 뮌헨에서 양산되었고 세계 지도 작성 및 네비게이션에 필요한 위성 설치에 사용됩니다. 독일은 위성 관측 능력도 서서히 개발하고 있습니다. 새로운 관측위성기술이 궤도에 발사되어 국가 전체의 환경부하를 경감하기 위한 중요한 대처가 되었습니다.

- 영국 우주청은 영국의 우주 부문을 뒷받침하는 18개 프로젝트를 지원하기 위해 650만 유로를 자금 제공한다고 발표했습니다. 이 기금은 영향력 있는 지역 주도 계획과 우주 클러스터 개발 관리자를 지원함으로써 영국 우주 분야의 성장을 자극합니다. 18개 프로젝트는 공공 서비스 향상을 위한 지구 관측(EO) 데이터 활용 등 지역의 다양한 문제를 해결하기 위한 다양한 혁신적 우주 기술을 개척할 것으로 기대됩니다. 2022년 11월, 스페인 정부는 향후 5년간 15억 유로를 ESA에 할당하여 스페인 우주에서 리더십을 강화할 것이라고 발표했습니다. 우주 프로그램에 대한 지출은 예측 기간 동안 확대될 것으로 예상됩니다.

유럽의 소형 위성 산업 개요

유럽의 소형 위성 시장은 상당히 통합되어 있으며 상위 5개사에서 99.59%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Airbus SE, GomSpaceApS, OHB SE, SatRev and Thales(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 위성의 질량

- 우주 프로그램에 대한 지출

- 규제 프레임워크

- 프랑스

- 독일

- 러시아

- 영국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 용도

- 통신

- 지구 관측

- 내비게이션

- 우주 관측

- 기타

- 궤도 등급

- GEO

- LEO

- MEO

- 최종 사용자

- 상업

- 군사 및 정부

- 기타

- 추진 기술

- 전기

- 가스

- 액체 연료

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Airbus SE

- Alba Orbital

- Astrocast

- FOSSA Systems

- GomSpaceApS

- Information Satellite Systems Reshetnev

- OHB SE

- SatRev

- Thales

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe Small Satellite Market size is estimated at 3.99 billion USD in 2025, and is expected to reach 6.42 billion USD by 2030, growing at a CAGR of 10.02% during the forecast period (2025-2030).

LEO satellites occupies a major market share of 98.8% in 2029

- Small satellites have revolutionized the space industry in recent years as they have enabled low-cost access to space for a wide range of applications, from scientific research to commercial and military applications. To fully realize the potential of small satellites, it is essential to understand the different types of orbits they can be launched into.

- For instance, LEO is the most common orbit for small satellites, as it provides a number of advantages, such as providing a low-latency communication link with the ground and making it ideal for applications that require real-time data transmissions, including telecommunication, remote sensing, or Earth observation. In the region, during 2017-2022, a total of 504 satellites were launched into LEO. Of these 531 satellites, nearly 443 satellites were launched for communication purposes.

- On the other hand, GEO is used primarily for communication and broadcast applications, as satellites in GEO orbit appear stationary from the ground. This allows continuous coverage of a specific area, such as a continent or ocean region. In Europe, companies such as Intelsat have launched a constellation of small satellites to provide telecommunication services to their customers.

- MEO is a less frequently used orbit for small satellites. It offers some unique advantages as the higher altitude of MEO facilitates a larger coverage area compared to LEO, which is important for applications like technology demonstration and navigation/GPS that require global coverage. These advancements are projected to result in a 88% growth rate for this segment by 2029, surpassing the figures in 2023.

Europe Small Satellite Market Trends

The trend for better fuel and operational efficiency are expected to be major drivers

- The classification of spacecraft by mass is one of the main metrics for determining the size of the launch vehicle and the cost of launching satellites into orbit. The success of a satellite mission depends heavily on the accuracy of its pre-flight mass measurement and the proper balance of the satellite to generate mass within limits.

- Satellites are classified according to their mass. Satellites with a mass of less than 500 kg are considered small satellites. About 460 small satellites were launched in this region during 2017-2022. There is a growing trend toward smaller satellites in the region due to their shorter development times, which can reduce overall mission costs. They have made it possible to significantly reduce the time required to obtain scientific and technological results. Small spacecraft missions tend to be flexible and thus can better respond to new technological opportunities or needs. The small satellite market in Europe is supported by the presence of a robust framework for the design and manufacture of small satellites tailored to serve specific application profiles. The number of operations in Europe is expected to increase between 2023 and 2029, driven by growing demand in commercial and military space sectors.

Increasing space expenditures of different space agencies are expected to positively impact the European small satellite market

- The European small satellite market has grown rapidly in recent years due to technological advancements, increased investment, and growing demand for small satellite services. Nano and microsatellites are smaller and more cost-effective than traditional satellites, making them more accessible to a wide range of organizations and businesses.

- For instance, in December 2020, IABG and BMWi signed a EUR 230 million contract to create satellites with high-resolution cameras, image sensors, and image converters. The new technology began mass production in Munich by the end of 2022 and will be used to install satellites needed for mapping and navigation around the world. Germany is also gradually developing its satellite observation capabilities. New observation satellite technologies were launched into orbit in a significant effort to reduce the environmental impact across the nation.

- The UK Space Agency announced that it would be funding EUR 6.5 million to support 18 projects to boost the UK space sector. The funding will stimulate growth in the UK space sector by supporting high-impact, locally-led schemes and space cluster development managers. The 18 projects are expected to pioneer a range of innovative space technologies to combat various local issues, such as utilizing Earth observation (EO) data to enhance public services. In November 2022, the Government of Spain announced that it would allocate EUR 1.5 billion to the ESA over the next five years, thereby reinforcing Spain's leadership in space. The spending on space programs is anticipated to grow in the forecast period.

Europe Small Satellite Industry Overview

The Europe Small Satellite Market is fairly consolidated, with the top five companies occupying 99.59%. The major players in this market are Airbus SE, GomSpaceApS, OHB SE, SatRev and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Russia

- 4.3.4 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.3.3 Other

- 5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 Alba Orbital

- 6.4.3 Astrocast

- 6.4.4 FOSSA Systems

- 6.4.5 GomSpaceApS

- 6.4.6 Information Satellite Systems Reshetnev

- 6.4.7 OHB SE

- 6.4.8 SatRev

- 6.4.9 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록