|

시장보고서

상품코드

1690700

용제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Solvents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

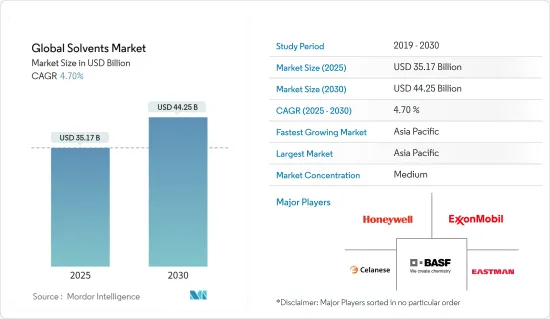

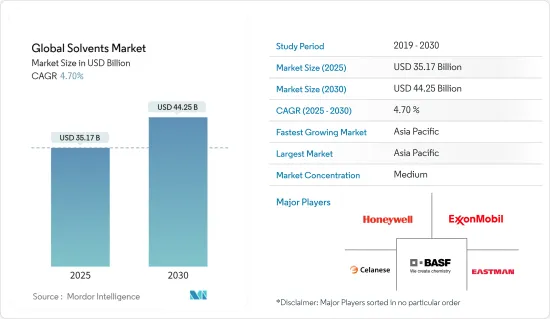

세계 용제 시장 규모는 2025년에 351억 7,000만 달러, 2030년에는 442억 5,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025년-2030년) CAGR은 4.7%를 나타낼 전망입니다. 2

용제 시장은 COVID-19 팬데믹의 영향을 받아 페인트나 코팅제, 폴리머, 접착제 등의 업계가 봉쇄 대책이나 경제적 혼란에 의해 생산의 지연을 강요받는 등, 생산과 이동에 감속이 보였습니다.

주요 하이라이트

- 단기적으로는 페인트 및 코팅 분야에서의 수요의 급증과, VOC 배출을 최소한으로 억제하기 위한 엄격한 규제가, 조사 대상 시장 수요를 견인하는 주된 요인이 되고 있습니다.

- 그러나 높은 제조 비용, 용제의 성능 문제, 화학 용제의 유해 작용이 시장 성장의 방해가 될 것으로 예상됩니다.

- 그럼에도 불구하고 산소 기반 산업용 용매의 개발과 바이오 제품에 대한 수요 증가는이 시장에 새로운 기회를 가져올 것으로 기대됩니다.

- 아시아태평양이 세계 시장을 독점할 것으로 예상되며, 수요의 대부분은 중국과 인도에서 가져옵니다.

용제 시장 동향

시장을 독점하는 페인트 및 코팅제 부문

- 용제는 페인트 및 코팅제의 조합에 필수적이며, 그 성능과 용도에 큰 영향을 미칩니다.

- 용제는 페인트 및 코팅제 수지, 안료 및 기타 성분을 녹이는 데 도움이 되며 균일한 혼합물을 만들고 페인트 및 코팅제를 부드럽고 균일하게 도포할 수 있습니다.

- 케톤계 용제는 점도가 낮고 고형분이 많기 때문에 업계에서 선호되고 있습니다. 에스테르계 용매는 페인트의 경화제로서의 역할과 공업용 세정제로서의 역할의 2가지 역할을 합니다.

- 바이오 용제는 페인트 및 코팅제의 바인더와 색상을 용해시켜 일관성을 보장합니다. 글리콜 에테르 에스테르는 장식 페인트와 스프레이 페인트에 배합되어 조기 건조를 방지합니다.

- 용제는 페인트 및 코팅제의 점도를 조정하여 적용 및 레벨링을 용이하게 합니다.

- WPCIA(Worlds Paint and Coatings Industry Association)에 따르면 세계의 페인트 및 코팅 시장은 2023년에 1,855억 달러의 평가액을 달성하여 전년대비 3.2% 증가했습니다. 이 상승의 주요 요인은 건설, 자동차 및 제조 분야에서 수요가 증가하는 것입니다.

- 또한 WPCIA의 데이터에 따르면 아시아태평양은 세계 최대의 페인트 및 코팅제 생산국으로 2023년 세계 생산량의 54.7%를 차지한 다음 유럽(19.6%), 북미(15.6%), 라틴아메리카(6.4%), 중동 및 아프리카(3.6%)가 되고 있습니다. 따라서, 페인트 및 코팅 산업의 확대는 조사된 시장을 촉진할 것으로 예상됩니다.

- 미국은 세계에서 가장 크고 가장 기술적으로 발전한 경제 중 하나입니다. 이 압도적인 지위에 의해 이 나라는 페인트 및 코팅 시장의 핫스팟의 하나가 되었습니다. 미국은 세계에서도 톱 클래스의 페인트 및 코팅 제조업체이며, 1,400사 이상의 제조회사가 있습니다.

- 미국 페인트 협회에 따르면 미국의 페인트 및 코팅 산업의 생산량은 2023년에 약 13억 1,000만 갤런이었습니다. PPG, Sherwin-Williams Company, Axalta Coating Systems,RPM Inc.Diamond Paints는 미국의 주요 페인트 및 코팅제 제조업체 및 공급업체입니다

- 프랑스의 페인트 및 코팅 업계에서 최근의 동향은 용제에 대한 수요 증가를 시사하고 있습니다.

- 이러한 역학을 근거로 하면, 페인트 및 코팅 분야에서는 용제 수요가 높아져, 향후 수년간 시장 성장을 견인할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 아시아태평양은 접착제, 페인트 및 코팅제, 퍼스널케어, 의약품, 기타 용도 등 다양한 용도로 소비량이 증가하고 있기 때문에 세계의 용제 시장의 대부분을 차지하고 있습니다.

- 도료나 코팅제의 배합에 있어서, 용제는 불가결합니다. 용제는 성분을 용해, 분산, 안정화시켜, 점도나 유동성을 조정해 매끄러운 마무리를 실현합니다.

- European Coatings의 보고에 의하면, 세계의 공업화의 거점인 중국에는 1만 개의 도료 제조업체가 있습니다.

- 중국 도료공업협회의 통계에 따르면 2023년 중국의 도료 생산량은 3,577만 2천 톤에 이르렀고, 전년 대비 4.5% 늘어났습니다.

- 제조업체 각 사는 신공장을 설립하거나 기존 설비의 능력을 증강하고 있습니다.

- 예를 들어, 2024년 1월 벨제 페인트 인디아는 오디샤의 새로운 그린필드 복합 공장에 1,000캐롤 루피(약 1억 2,060만 달러) 이상을 투입할 계획을 발표했습니다.

- 용제는 접착제의 배합에 있어서 매우 중요하며, 재료의 효과적인 접착을 보증합니다.

- 예를 들어, 2023년 6월에 Henkel AG&Co.KGaA는 중국 산동성의 연대화학공업원에 접착제의 새로운 제조시설을 개설한다고 발표했습니다.

- 화장품 분야에서는 용제는 성분의 용해와 안정화에 도움이 되고 있습니다.

- 중국국가통계국의 보고에 따르면 화장품 부문은 지난 10년간 급속히 확대되었습니다.

- 한국은 세계의 미용 시장의 톱 10에 랭크되어 그 혁신성, 천연 성분의 사용, 매력적인 패키징으로 칭찬되고 있습니다.

- 의약품 분야에서는 용제는 의약품 유효성분(API)과 의약품의 제조 공정을 촉진합니다.

- 인도의 제약업계는 저렴한 가격으로 고품질의 의약품을 세계적으로 공급하고 있는 것으로 유명하며, 급속한 과학의 진보를 목격하고 있습니다. 2030년에는 1,300억 달러, 2047년에는 4,500억 달러로 급증할 것으로 전망되고 있습니다.

- 이러한 역학을 생각하면, 아시아태평양의 용제 수요는 향후 수년에 걸쳐 상승할 것으로 예상됩니다.

용제 산업 개요

용제 시장은 부분적으로 통합되어 있습니다. 주요 기업은 Eastman Chemical Company, BASF SE, Exxon Mobil Corporation, Honeywell International Inc., Celanese Corporation 등입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 성과

- 조사의 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 페인트 및 코팅 분야에서의 수요 급증

- VOC 배출을 최소화하기 위한 엄격한 규제

- 기타 촉진요인

- 억제요인

- 높은 제조 비용과 용매의 성능 문제

- 화학용제의 유해한 영향

- 기타 억제요인

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 원료별

- 바이오 베이스 용제

- 석유화학계 용제

- 유형별

- 산소계 용제

- 탄화수소계 용제

- 할로겐계 용제

- 용도별

- 접착제

- 페인트

- 퍼스널케어

- 의약품

- 폴리머 제조

- 기타 용도(인쇄 잉크, 농약, 금속 세정)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 튀르키예

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 카타르

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)**, 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- ADM

- Arkema

- Ashland

- BASF SE

- Bharat Petroleum Corporation Limited

- Celanese Corporation

- Dow

- Eastman Chemical Company

- Exxon Mobil Corporation

- Gandhar Oil Refinery(India) Limited

- GROUPE BERKEM

- Honeywell International Inc.

- Huntsman International LLC

- INEOS

- LyondellBasell Industries Holdings BV

- Sasol Limited

- Shell PLC

- Solvay

제7장 시장 기회와 앞으로의 동향

- 산소계 공업용제의 개발

- 바이오 베이스 제품 수요 증가

- 기타 기회

The Global Solvents Market size is estimated at USD 35.17 billion in 2025, and is expected to reach USD 44.25 billion by 2030, at a CAGR of 4.7% during the forecast period (2025-2030).

The solvents market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries such as paints and coatings, polymers, and adhesives, etc., were forced to delay their production due to containment measures and economic disruptions. However, the conditions recovered in 2021, restoring the market's growth trajectory.

Key Highlights

- Over the short term, surging demand from the paints and coatings sector and stringent regulations in place to minimize VOC emissions are the major factors driving the demand for the market studied.

- However, high manufacturing costs, performance issues of solvents, and detrimental effects of chemical solvents are expected to hinder the market's growth.

- Nevertheless, the development of oxygenated-based industrial solvents and increasing demand for bio-based products are expected to create new opportunities for the market studied.

- Asia-Pacific is expected to dominate the global market, with the majority of demand coming from China and India.

Solvents Market Trends

Paints and Coatings Segment to Dominate the Market

- Solvents are integral to formulating paints and coatings, significantly influencing their performance and applications.

- Solvents help to dissolve the resin, pigment, and other components of the paint or coating, creating a uniform mixture and ensuring that the paint or coating can be applied smoothly and evenly.

- Ketones are favored in the industry for their low-viscosity properties and high solid content. Ester solvents serve a dual purpose: acting as hardeners in paints and functioning as industrial cleaners.

- Bio-based solvents dissolve binders and colors in paints and coatings and ensure consistency. Glycol ether esters are incorporated into decorative and spray paints to prevent premature drying.

- Solvents adjust the viscosity of paints and coatings, facilitating easier application and leveling, which is especially crucial for spray or brush-on coatings.

- According to the Worlds Paint and Coatings Industry Association (WPCIA), the global paint and coatings market achieved a valuation of USD 185.5 billion in 2023, marking a 3.2% increase from the prior year. This uptick was largely fueled by heightened demand across the construction, automotive, and manufacturing sectors.

- Furthermore, Asia-Pacific is the largest producer of paint and coatings globally, accounting for 54.7% of global production in 2023, followed by Europe (19.6%), North America (15.6%), Latin America (6.4%), and Middle East and Africa (3.6%) as per the data from WPCIA. Thus, expansion in the paints and coatings industry is anticipated to drive the market studied.

- The United States represents one of the largest and most technologically advanced economies globally. This dominant position enabled the country to become one of the hotspots for the paints and coatings market. It is one of the top global paints and coatings producers, with more than 1,400 manufacturing companies.

- According to the American Coatings Association, the paint and coatings industry's production volume in the United States was approximately 1.31 billion gallons in 2023. Moreover, the industry's production is estimated to surpass 1.34 billion gallons in 2024. PPG, Sherwin-Williams Company, Axalta Coating Systems, RPM Inc., and Diamond Paints are a few major paints and coatings manufacturers and suppliers in the United States.

- Recent developments in the French paints and coatings industry hint at a growing demand for solvents. A notable example is PPG's USD 17 million aerospace application support center (ASC), inaugurated in Toulouse, France, in December 2023. This center provides filling and packaging for aerospace materials, encompassing coatings and sealants for diverse aircraft.

- Given these dynamics, the paints and coatings sector is expected to see a rising demand for solvents, driving the market's growth in the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific commands a significant portion of the global solvents market, driven by rising consumption across diverse applications, including adhesives, paints and coatings, personal care, pharmaceuticals, and other applications. This trend positions the region as a likely market leader in the coming years.

- In the formulation of paints and coatings, solvents are essential. They dissolve, disperse, and stabilize components, adjusting viscosity and flow to ensure a smooth finish. With major manufacturers expanding production capacities and the paints and coatings sector growing, the demand for solvents is set to rise.

- China, a global hub for industrialization, boasts a staggering 10,000 coatings manufacturers, as reported by European Coatings. Notably, major players like Nippon Paint, AkzoNobel, and PPG Industries have established manufacturing bases in the country.

- Figures from the China Coatings Industry Association revealed that in 2023, China's coatings production hit 35,772 million tons, a 4.5% increase from the previous year. Exports surged by 19.6% to 262,000 tons, while domestic consumption rose by 4.2% to 35,663 million tons, underlining the sector's robust growth.

- Manufacturers are either setting up new plants or ramping up the capacities of their existing facilities. These strategic moves bolster the demand for paints and coatings and underpin the market growth.

- For instance, in January 2024, Berger Paints India announced plans to inject over INR 1,000 crore (~ USD 120.6 million) into a new greenfield composite plant in Odisha, focusing on decorative and industrial paints. This bold investment is poised to catalyze the demand for paints and coatings in the near future, thus benefiting the market studied.

- Solvents are pivotal in adhesive formulations, ensuring effective bonding of materials. The expansion projects in the adhesives industry are expected to boost market growth.

- For instance, in June 2023, Henkel AG & Co. KGaA announced that it would be opening a new manufacturing facility for adhesives in Yantai Chemical Industry Park in Shandong Province, China. The company aims to manufacture high-impact adhesive products in China through this expansion project, thereby supporting the market's growth.

- In the cosmetics sector, solvents are instrumental in dissolving and stabilizing ingredients. As the cosmetic industry in the region flourishes, the demand for solvents is expected to rise.

- The National Bureau of Statistics of China reported that the cosmetics sector has expanded rapidly over the past decade. In 2023, retail cosmetics sales in China reached approximately CNY 414.17 billion (~USD 58.4 billion), marking a modest uptick from the prior year.

- South Korea ranks among the top ten global beauty markets and is celebrated for its innovation, use of natural ingredients, and attractive packaging. According to the Ministry of Food and Drug Safety (MFDS) data, South Korea's cosmetics exports hit USD 8.5 billion in 2023, securing the fourth position globally.

- In the pharmaceutical sector, solvents facilitate processes in manufacturing active pharmaceutical ingredients (APIs) and drug products. With the region's pharmaceutical industry on the rise, the demand for solvents is set to grow.

- The Indian pharmaceutical industry, renowned for supplying affordable, high-quality medicines globally, is witnessing rapid scientific advancements. Government projections estimate the industry's value will soar from USD 50 billion today to USD 130 billion by 2030 and an ambitious USD 450 billion by 2047. Such growth is anticipated to drive the demand for solvents in pharmaceutical drug production during the forecast period.

- Given these dynamics, the demand for solvents in Asia-Pacific is poised for an upswing in the coming years.

Solvents Industry Overview

The solvents market is partially consolidated in nature. The major players include Eastman Chemical Company, BASF SE, Exxon Mobil Corporation, Honeywell International Inc., and Celanese Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Surging Demand from the Paints & Coatings Sector

- 4.1.2 Stringent Regulations in Place to Minimize VOC Emissions

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Manufacturing Costs and Performance Issues of Solvents

- 4.2.2 Detrimental Effects of Chemical Solvents

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Source

- 5.1.1 Bio-based Solvents

- 5.1.2 Petrochemical-based Solvents

- 5.2 By Type

- 5.2.1 Oxygenated Solvents

- 5.2.2 Hydrocarbon Solvents

- 5.2.3 Halogenated Solvents

- 5.3 By Application

- 5.3.1 Adhesives

- 5.3.2 Paints and Coatings

- 5.3.3 Personal Care

- 5.3.4 Pharmaceuticals

- 5.3.5 Polymer Production

- 5.3.6 Other Applications (Printing Inks, Agricultural Chemicals, and Metal Cleaning)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 BASF SE

- 6.4.5 Bharat Petroleum Corporation Limited

- 6.4.6 Celanese Corporation

- 6.4.7 Dow

- 6.4.8 Eastman Chemical Company

- 6.4.9 Exxon Mobil Corporation

- 6.4.10 Gandhar Oil Refinery (India) Limited

- 6.4.11 GROUPE BERKEM

- 6.4.12 Honeywell International Inc.

- 6.4.13 Huntsman International LLC

- 6.4.14 INEOS

- 6.4.15 LyondellBasell Industries Holdings BV

- 6.4.16 Sasol Limited

- 6.4.17 Shell PLC

- 6.4.18 Solvay

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Oxygenated Based Industrial Solvents

- 7.2 Increasing Demand for Bio-based Products

- 7.3 Other Opportunities