|

시장보고서

상품코드

1690899

동남아시아의 WtE(폐기물 에너지화) 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Southeast Asia Waste-to-Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

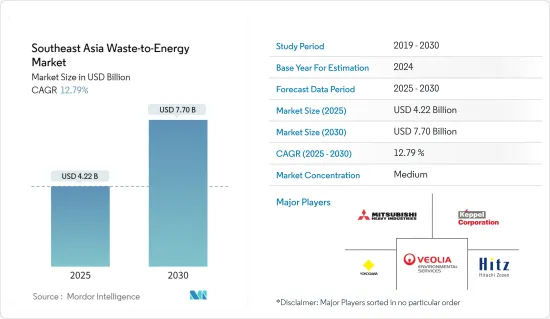

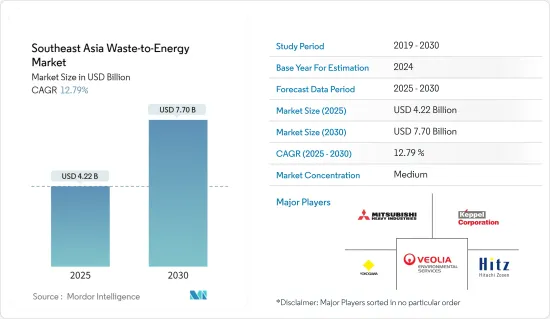

동남아시아의 WtE(폐기물 에너지화) 시장 규모는 2025년 42억 2,000만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR 12.79%로 확대되어, 2030년에는 77억 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 장기적으로는 폐기물 발생량 증가, 지속가능한 도시생활의 요구를 충족시키기 위한 폐기물 관리에 대한 관심 증가, 비화석 연료 에너지원에 대한 주목 증가가 동남아시아 폐기물 에너지 시장 수요를 견인하고 있습니다.

- 반대로, 자본 비용이 높은 것은 조사 기간 동안 시장 성장을 방해할 것으로 예상됩니다.

- 하지만 덴드로 리퀴드 에너지(DLE)와 같은 신흥 WtE(폐기물 에너지화) 기술은 앞으로 수년간 시장 관계자들에게 큰 비즈니스 기회를 가져올 것으로 기대되고 있습니다. DLE는 발전 효율이 4배 높고, 공장 부지 내에서의 배출물이나 폐액의 문제가 없는 특징도 있습니다.

- 말레이시아는 동남아시아 지역에서 가장 빠르게 성장하는 국가 중 하나입니다. 이 나라는 폐기물 관리를 개선하기 위한 노력을 강화하고 있으며, 그 중 WtE(폐기물 에너지화)는 중요한 역할을 하고 있습니다.

동남아시아의 WtE(폐기물 에너지화) 시장 동향

열 기반 폐기물 에너지 변환에 대한 수요 증가

- 열 기반 폐기물 에너지 변환은 열 에너지를 이용하여 폐기물을 전기, 열, 연료 등의 사용 가능한 에너지로 변환하는 것을 말합니다. 이 접근법은 폐기물을 에너지로 전환시키는 촉매로서 열을 이용하는 다양한 기술의 응용을 포함합니다.

- 급속한 인구 증가와 도시화로 폐기물 발생량이 크게 증가하여 폐기물 관리의 과제가 되고 있습니다. 열을 이용한 폐기물의 에너지 전환은 매립 및 소각해야 하는 폐기물의 양을 효과적으로 관리하고 줄입니다.

- 2023년 1월 네덜란드에 본사를 둔 Harvest Waste(전신은 Amsterdam Waste Environmental Consultancy and Technology)는 베트남의 메콩 델타 지방 석창성에서 폐기물 열에너지화 사업의 초기 조사를 시작했습니다. 프로젝트의 총 사업비는 약 1억 달러로 추정됩니다.

- 신뢰성이 높고 지속 가능한 에너지원에 대한 요구가 높아지고 있습니다. 열 기반 WtE(폐기물 에너지화) 기술은 폐기물을 전기 및 열과 같은 사용 가능한 에너지로 변환할 수 있습니다. 에너지 생성에 기여하고 에너지 믹스의 다양화에도 도움이 되므로 화석 연료에 대한 의존도가 저하됩니다.

- 동남아시아는 세계에서 가장 급속하게 도시 인구가 증가하고 있는 지역 중 하나입니다. 도시 인구의 급속한 증가는 이 지역 전체의 도시 인구에서 발생하는 폐기물의 양을 폭발적으로 증가시켰습니다. 이 폐기물의 대부분은 싱가포르를 제외하면 유기물입니다(약 50% 이상).

- 인구가 증가함에 따라 이 지역의 전력 수요는 최근 몇 년간 크게 증가하고 있습니다. 예를 들어 태국에서는 2021년부터 2022년까지 전력 소비량이 3% 이상 증가했습니다.

- 따라서 위의 관점에서 열 기반 WtE(폐기물 에너지화) 시스템 수요는 예측 기간 동안 증가할 것으로 예상됩니다.

현저한 성장이 기대되는 말레이시아

- 말레이시아 정부는 지속 가능한 폐기물 관리 실천과 재생 가능 에너지 개발을 적극적으로 추진하고 있습니다. WtE(폐기물 에너지화) 부문을 지원하기 위해 고정가격임베디드제도, 세제우대조치, 규제제도 등 다양한 대책과 정책을 실시했습니다. 이러한 조치는 이 산업에 대한 투자와 성장을 촉구하는 환경을 조성합니다.

- 다른 많은 국가들과 마찬가지로 말레이시아는 인구 증가, 도시화 및 산업화로 인해 폐기물 발생량이 증가하고 있습니다. 따라서 효율적인 폐기물 관리 솔루션이 시급합니다. WtE(폐기물 에너지화) 프로젝트는 재생가능 에너지를 창출하면서 늘어나는 폐기물량을 다루는 지속 가능한 방법을 제공합니다.

- 2023년 5월 말라카 주정부는 순가이 우단 위생 고형 폐기물 처분장에서 폐기물 에너지화(WTE) 플랜트 또는 소각로의 신속한 건설을 명령했습니다. 그들은 2026년이라는 초기 목표보다 빠른 내년에 시설을 가동시키는 것을 목표로 하고 있습니다.

- 또한 말레이시아에서는 폐기물에서 에너지로의 전환 과정에 적합한 유기 폐기물이 상당한 비율을 차지합니다. 식품 폐기물 및 농업 잔류물과 같은 유기 폐기물은 혐기성 소화 및 퇴비화에 효율적으로 이용될 수 있어 바이오가스 및 비료의 생산으로 이어집니다. 유기 폐기물 자원이 풍부한 것은 WtE(폐기물 에너지화) 프로젝트에 좋은 조건입니다.

- 또한 말레이시아 정부는 국가의 에너지 믹스에서 차지하는 재생 가능 에너지의 비율을 늘리기 위해 재생 가능 에너지 목표를 설정합니다. WtE(폐기물 에너지화) 기술은 폐기물 자원으로부터 재생 가능 에너지를 생성함으로써 이러한 목표 달성에 기여합니다. WtE(폐기물 에너지화) 기술은 국가의 지속가능성 목표에 부합하여 저탄소 경제로의 전환을 지원합니다.

- 국제재생가능에너지기구에 따르면 2022년 재생가능에너지 설비 용량은 9044MW로 2018년부터 2022년까지 20% 이상의 성장률을 기록하고 있습니다.

- 따라서 위의 관점에서 말레이시아는 예측 기간 동안 시장 조사에 중요한 역할을 할 것으로 예상됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2028년까지 시장 규모(MW)와 수요 예측

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 폐기물 발생량 증가

- 환경에 대한 우려와 지속가능성의 목표

- 억제요인

- WtE(폐기물 에너지화) 인프라에 필요한 높은 자본 비용

- 성장 촉진요인

- 공급망 분석

- 업계의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협 제품 및 서비스

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 기술

- 물리적

- 열

- 소각

- 공동처리

- 열분해 및 가스화

- 생물학적

- 혐기성 소화

- 지역별 시장 분석 {2028년까지 시장 규모와 수요 예측(지역별만)}: 말레이시아

- 말레이시아

- 인도네시아

- 태국

- 싱가포르

- 베트남

- 기타 동남아시아 지역

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Mitsubishi Heavy Industries Ltd

- Keppel Corporation

- PT Yokogawa Indonesia

- Veolia Environment SA

- Hitachi Zosen Corp

- MVV Energie AG

- Martin GmbH

- Babcock & Wilcox Volund AS

제7장 시장 기회와 앞으로의 동향

- 국제적인 제휴와 투자

The Southeast Asia Waste-to-Energy Market size is estimated at USD 4.22 billion in 2025, and is expected to reach USD 7.70 billion by 2030, at a CAGR of 12.79% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the increasing amount of waste generation, growing concern for waste management to meet the need for sustainable urban living, and increasing focus on non-fossil fuel sources of energy are driving the demand for the Southeast Asia Waste-to-Energy Market.

- Conversely, the high capital costs are expected to hinder market growth during the study period.

- Nevertheless, emerging waste-to-energy technologies, such as Dendro Liquid Energy (DLE), are expected to create significant opportunities for market players over the coming years. It is four times more efficient in terms of electricity generation, with the additional benefits of no emission discharge and effluence problems at plant sites,

- Malaysia is one of the fastest-growing countries in the Southeast Asian region. The country ramped up its efforts in improving waste management, in which waste-to-energy plays a key role.

Southeast Asia Waste-to-Energy Market Trends

Growing Demand for Thermal-Based Waste-to-Energy Conversion

- Thermal-based waste-to-energy conversion refers to utilizing thermal energy to convert waste materials into usable forms of energy, such as electricity, heat, or fuel. This approach involves the application of various technologies that use heat as a catalyst for converting waste into energy.

- Rapid population growth and urbanization led to a significant increase in waste generation, posing challenges for waste management. Thermal-based waste-to-energy conversion effectively manages and reduces the waste volume that must be landfilled or incinerated.

- In January 2023, Harvest Waste, a company based in the Netherlands (formerly Amsterdam Waste Environmental Consultancy and Technology), commenced initial studies for a thermal waste-to-energy venture in the Mekong Delta province of Soc Trang in Vietnam. The project is estimated to cost around USD 100 million.

- There is a growing need for reliable and sustainable energy sources. Thermal-based waste-to-energy technologies allow waste conversion into usable energy forms, such as electricity and heat. It contributes to energy generation and helps diversify the energy mix, reducing dependence on fossil fuels.

- Southeast Asia includes one of the fastest-growing urban populations globally. The rapid growth in the urban population led to explosive growth in the amount of waste generated by the urban population across the region. Most of this waste is organic (about or more than 50%) except in Singapore.

- With the growing population, the region's electricity demand increased significantly in recent years. For instance, in Thailand, electricity consumption increased by more than 3% between 2021 and 2022.

- Therefore, as per the above points, the demand for thermal-based waste-to-energy systems is expected to increase during the forecasted period.

Malaysia Expected to Witness Significant Growth

- The Malaysian government actively promoted sustainable waste management practices and renewable energy development. They implemented various initiatives and policies to support the waste-to-energy sector, including feed-in tariffs, tax incentives, and regulatory frameworks. These measures create a conducive environment for investment and growth in the industry.

- Like many other countries, Malaysia is experiencing a rise in waste generation due to population growth, urbanization, and industrialization. It creates a pressing need for efficient waste management solutions. Waste-to-energy projects offer a sustainable method to tackle the growing waste volume while generating renewable energy.

- In May 2023, the Melaka state government ordered the expedited construction of the Waste to Energy (WTE) plant or incinerator at the Sungai Udang Sanitary Solid Waste Disposal Site. They aim to include the facility operational next year, earlier than the original target of 2026.

- Furthermore, Malaysia includes a significant proportion of organic waste, which is well-suited for waste-to-energy conversion processes. Organic waste, such as food waste and agricultural residues, can be efficiently utilized for anaerobic digestion or composting, leading to biogas or fertilizer production. The abundance of organic waste resources presents favorable conditions for waste-to-energy projects.

- Additionally, the Malaysian government set renewable energy targets to increase the share of renewable energy in the country's energy mix. Waste-to-energy technologies contribute to fulfilling these targets by generating renewable energy from waste resources. It aligns with the country's sustainability goals and supports the transition to a low-carbon economy.

- According to International Renewable Energy Agency, the total renewable energy installed capacity in 2022 was 9044 MW registering a growth rate of more than 20% between 2018 and 2022.

- Therefore, according to the above points, Malaysia is expected to play a key role in the market studies during the forecasted period.

Southeast Asia Waste-to-Energy Industry Overview

The Southeast Asia waste-to-energy market is moderately consolidated. The key players in the market (in no particular order) include Mitsubishi Heavy Industries Ltd, Keppel Corporation, PT Yokogawa Indonesia, Veolia Environment SA, and Hitachi Zosen Corp, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in MW, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Waste Generation

- 4.5.1.2 Environmental Concerns and Sustainability Goals

- 4.5.2 Restraints

- 4.5.2.1 High Capital Costs Involved in Waste-to-Energy Infrastructure

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Physical

- 5.1.2 Thermal

- 5.1.2.1 Incineration

- 5.1.2.2 Co-processing

- 5.1.2.3 Pyrolysis/gasification

- 5.1.3 Biological

- 5.1.3.1 Anaerobic Digestion

- 5.2 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.2.1 Malaysia

- 5.2.2 Indonesia

- 5.2.3 Thailand

- 5.2.4 Singapore

- 5.2.5 Vietnam

- 5.2.6 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Heavy Industries Ltd

- 6.3.2 Keppel Corporation

- 6.3.3 PT Yokogawa Indonesia

- 6.3.4 Veolia Environment SA

- 6.3.5 Hitachi Zosen Corp

- 6.3.6 MVV Energie AG

- 6.3.7 Martin GmbH

- 6.3.8 Babcock & Wilcox Volund AS

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 International Collaborations and Investments