|

시장보고서

상품코드

1692145

전기자동차 고전압 DC-DC 컨버터 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Electric Vehicle High-Voltage DC-DC Converter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

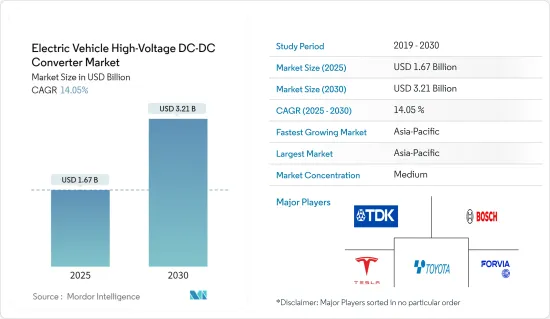

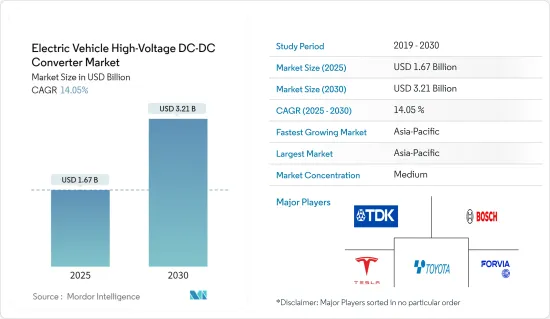

전기자동차 고전압 DC-DC 컨버터 시장 규모는 2025년에 16억 7,000만 달러, 2030년에는 32억 1,000만 달러에 달할 것으로 예측됩니다. 예측기간(2025-2030년)의 CAGR은 14.05%를 보일 것으로 예상됩니다.

장기적으로는 전기자동차로의 이동 증가, 엄격한 배기 가스 규제, 전기자동차 판매를 촉진하기 위한 정부의 이니셔티브, 충전 인프라 확대, 배터리 기술 및 EV 부품의 진보 등의 요인이 시장 성장에 기여하고 있습니다. 예를 들어,

국제에너지기구(IEA)에 따르면 2024년 1분기 전기차 판매 대수는 2023년 1분기에 비해 약 25% 증가했으며, 전기차 판매 대수에서는 중국이 45%로 최대 점유율을 차지했으며 유럽(25%)이 뒤를 이었습니다.

세계 전기자동차 판매가 증가함에 따라 최근 고전압 DC-DC 컨버터 기술의 발전은 효율성 향상, 소형 경량화 및 신뢰성 향상에 중점을 둡니다. 탄화규소(SiC)나 질화갈륨(GaN) 반도체 등의 기술 혁신에 의해 보다 높은 주파수로 동작하는 효율적인 컨버터가 개발되어, 수동 부품의 소형화가 진행되고 있습니다.

이 시나리오를 고려하여 다양한 제조업체들이 전기자동차와 그 부품(컨버터 등)의 기술 향상에 주력하고 있습니다.

삼성전기는 2024년 6월 DC-DC 컨버터 등 전기자동차 용도에 맞춘 고전압 적층 세라믹 커패시터(MLCC) 'CL32B104KHU6PN#'을 발표했습니다. CL32B104KHU6PN#은 소형화, 고내압, 안정성, 고용량 등의 특징을 가지고 자동차에서 MLCC의 사용을 촉진하고 있습니다.

클라우드 컴퓨팅 및 IoT(사물 인터넷)와 같은 기술이 전기자동차 배터리 관리 시스템에 도입되어 안정적인 출력 전압을 보장하는 DC-DC 컨버터와 함께 전기자동차에서 컨버터의 사용이 증가하고 있습니다.

전기자동차 고전압 DC-DC 컨버터 시장에서는 인도나 중국과 같은 국가가 EV 판매에서 가장 큰 점유율을 차지하기 때문에 아시아태평양이 돌출한 점유율을 차지할 것으로 추정됩니다. 북미와 유럽은 전기자동차의 보급이 진행되고 있으며 정부가 미래의 배기 가스 목표 달성에 힘을 쏟고 있기 때문에 급성장이 예상됩니다.

이러한 요인은 예측 기간 동안 시장 성장에 긍정적인 영향을 미칠 것으로 예상됩니다.

전기자동차 고전압 DC-DC 컨버터 시장 동향

승용차가 시장에서 가장 높은 점유율을 차지

장기적으로는 운전 경험 향상, 편안함, 안전성을 제공하는 자동차에 대한 수요가 증가함에 따라 저연비 엔진 수요가 증가할 수 있습니다. 다양한 국가들이 엄격한 규제, 보조금, 세액공제, 기타 우대조치를 통해 전기차의 보급을 촉진하고 있기 때문에 전기차 판매량 증가가 승용차 판매를 더욱 밀어 올리고 있습니다.

국제에너지기구(IEA)에 따르면 유럽에서 전기차의 신규 등록 대수는 2023년 320만대 가까이에 이르며 2022년 대비 20% 가까이 증가했으며 같은 해 전기차 스톡의 70%를 배터리 전기차가 차지합니다.

세계 각국의 정부도 기존 자동차보다 전기자동차를 구입하도록 장려하기 위해 다양한 제도와 정책을 내세우고 있습니다. 전기자동차 구매를 촉진하는 이러한 노력 중 하나는 캘리포니아주 제로 이미션 차량(ZEV) 프로그램으로 2025년까지 150만대의 전기자동차를 보급하는 것을 목표로 하고 있습니다. 기타에도 인도, 중국, 영국, 한국, 프랑스, 독일, 노르웨이, 네덜란드 등이 다양한 우대 조치를 제공합니다.

마찬가지로 2025년 12월 31일까지 유럽에서 등록된 차량은 10년간 소유세가 면제되며, 이 면제는 2030년 12월 31일까지 유효합니다. 이러한 정책이 전기 승용차 판매를 뒷받침하고 있습니다.

전기 승용차의 판매량이 증가함에 따라 EV용 커넥터를 제조하는 기업은 EV 부문에서 성장 기회를 발견하고 있으며 신제품 개발을 위해 다양한 기술적 진보에 주력하고 있습니다.

2024년 5월, 이튼은 저전압 48 볼트 DC-DC 컨버터의 고출력 버전을 출시했습니다. 새로 출시된 컨버터는 48 볼트 시스템에서 전력을 취하고 액세서리 및 기타 저전력 시스템을 구동하기 위해 12 볼트로 강압합니다.

이러한 요인 외에도 높은 가처분 소득, 브랜드 인지도 상승 및 고전력 구매 평준화가 이 부문의 성장에 기여합니다.

아시아태평양이 시장을 독점

전기자동차 고전압 DC-DC 컨버터 시장에서는 아시아태평양이 대부분의 점유율을 차지하고 있습니다. 중국과 같은 국가가 EV 판매를 이끌고 있기 때문에 예측 기간 동안 시장이 크게 성장할 것으로 예상됩니다.

중국과 일본은 기술 혁신, 기술 및 첨단 전기자동차 개발에 관심을 가지고 있습니다. 또한 인도네시아 등은 대규모 전동 이동성 프로젝트에 종사하고 있습니다.

중국은 세계 전기자동차 산업의 주요 기업입니다. 이 나라 정부는 국민들에게 전기자동차의 도입을 장려하고 있습니다. 중국은 2040년까지 이동성을 완전히 전기차로 전환할 계획입니다. 중국의 전기 승용차 시장도 세계 최대급이며 지난 몇 년동안 급성장하고 있습니다. 예측 기간 동안 더 성장할 것으로 예상되며 전기자동차 고전압 DC-DC 컨버터 시장에 긍정적인 영향을 줄 수 있습니다. 이 시장의 주요 기업 몇사는 다른 기업와 제휴하여 파워 일렉트로닉스 부품을 개발하고 있습니다.

자동차회사에 의한 많은 투자는 전기자동차 수요 증가에 대응하고 자동차 판매량 증가에 기여할 것으로 예상됩니다. OEM은 MG Comet EV와 같은 해치백에서 Tesla Model 3과 같은 고급 세단까지 다양한 부문에서 전기자동차를 제공합니다.

전기자동차로의 전환에는 상당한 투자가 필요하며, 자동차 제조업체는 제조거점 업그레이드에 주력하고 있으며, 이는 기업이 전기화 목표를 달성하는데 중요합니다.

인도의 전기자동차 시장은 성장 단계에 있습니다. TATA, Mahindra, MG와 같은 인도 자동차 제조업체는 저렴한 전기자동차를 제공하기 위해 노력하고 있습니다. 정부는 또한 국내 온실가스 배출을 줄이기 위해 전기 이동성을 지원합니다.

2024년 3월 인도 정부는 EV 정책을 승인했습니다. 이 정책은 최소 투자 5억 달러로 국내에 제조 단위를 설립하는 기업에 수입 관세 양허가 부여됩니다.

인도 자동차 제조업체도 인도에서 저렴한 전기자동차를 제공하기 위한 노력과 연구 개발에 투자하고 있습니다. 예를 들어 현대자동차는 2021년 2월 합리적인 신형 EV를 개발하기 위해 1억 2,000만 달러를 투자할 것이라고 발표했습니다. 차량은 현지에서 제조 될 예정이며, 회사는 부품을 조달하기 위해 현지 공급업체와 협상 중입니다. 현대자동차는 인도에서 EV를 포트폴리오에 추가할 계획이기 때문에 자매 브랜드 기아자동차와의 전략적 제휴를 모색할 수도 있습니다. 기아자동차는 2024년 출시 예정이었던 인도를 위한 대중을 위한 합리적인 가격의 전기차를 개발하기 위해 노력하고 있습니다.

이러한 요인으로 인해 자동차용 DC-DC 컨버터 수요가 증가하고 예측기간 동안 시장 성장을 가속할 가능성이 높습니다.

전기자동차 고전압 DC-DC 컨버터 산업 개요

전기자동차 고전압 DC-DC 컨버터 시장은 세계 및 지역에서 확립된 기업에 의해 통합되고 주도되고 있습니다. 각 회사는 시장에서의 지위를 유지하기 위해 신제품 출시, 제휴, 합병 등의 전략을 채용하고 있습니다.

- 2024년 6월, TDK는 TDK-Lambda 브랜드의 300W 정격 i7C 비절연형 DC-DC 컨버터 시리즈에 전류 제한 조정 가능 모델을 추가한다고 발표했습니다. 새로운 모델은 의료, 무인 운송 차량(AGV) 및 기타 산업에서 12V, 24V, 48V의 시스템 전압에서 더 높은 전력의 DC 출력을 생성하는 데 적합합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 전기자동차의 보급 확대

- 기타 촉진요인

- 시장 성장 억제요인

- 컨버터는 작동 시 노이즈를 발생시켜 타겟 시장을 방해할 수 있습니다.

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자, 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 자동차 유형

- 승용차

- 상용차

- 추진 유형

- 플러그인 하이브리드 자동차

- 배터리 전기자동차

- 연료전지 전기자동차

- 냉각 방식

- 액냉식

- 공냉

- 입력 전압

- 200V-450V

- 450V-800V

- 800V-1000V

- 출력 전압

- 12V-24V

- 24V-48V

- 출력 전력

- 2kW 미만

- 2kW 이상

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 노르웨이

- 폴란드

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 기타 국가

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Continental AG

- Robert Bosch GmbH

- Valeo Group

- ABB Ltd

- DENSO Corporation

- Hella GmbH & Co. KGaA

- Toyota Industries Corporation

- Infineon Technologies AG

- Texas Instruments

- STMicroelectronics

- TDK-Lambda Corporation

- Shinry Technologies

- Delta Electronics

- Vicor Corporation

- Hyundai Mobis Ltd

제7장 시장 기회와 앞으로의 동향

SHW 25.04.09The Electric Vehicle High-Voltage DC-DC Converter Market size is estimated at USD 1.67 billion in 2025, and is expected to reach USD 3.21 billion by 2030, at a CAGR of 14.05% during the forecast period (2025-2030).

Over the long term, factors such as the increasing shift toward electric vehicles, stringent emission regulations, government initiatives to promote sales of electric vehicles, expansions in charging infrastructure, and advancements in battery technology and EV components contribute to the market's growth. For instance,

According to the International Energy Agency, in Q1 2024, electric car sales grew by around 25% compared to Q1 2023, with China holding the largest share of 45% in terms of electric car sales, followed by Europe (25%).

With the rise in EV sales worldwide, recent advancements in high-voltage DC-DC converter technology have focused on increasing efficiency, reducing size and weight, and enhancing reliability. Innovations such as silicon carbide (SiC) and gallium nitride (GaN) semiconductors are leading to more efficient converters that operate at higher frequencies, thus reducing the size of passive components.

Considering the scenario, various manufacturers are focusing on upgrading their technologies for electric vehicles and their components, such as converters.

In June 2024, Samsung Electro-Mechanics introduced the CL32B104KHU6PN#, a high-voltage multi-layer ceramic capacitor (MLCC) tailored for EV applications, such as DC-DC converters. The features include miniaturization, high voltage, stability, and higher capacitance, which are driving the usage of MLCCs in vehicles.

The deployment of technologies like cloud computing and IoT (Internet of Things) in battery management systems of electric cars, coupled with a DC-DC converter to ensure a regulated output voltage, have increased the use of converters in electric vehicles.

Asia-Pacific is estimated to hold a prominent share in the electric vehicle high voltage DC-DC converter market, as countries like India and China hold the largest share in EV sales. North America and Europe are also expected to grow rapidly due to the increasing adoption of electric vehicles and the government's increasing focus on achieving emission goals in the future.

These factors are expected to positively impact the market's growth during the forecast period.

Electric Vehicle High-Voltage DC-DC Converter Market Trends

Passenger Cars Hold the Highest Share in the Market

Over the long term, the growing demand for automobiles that provide enhanced driving experiences, comfort, and safety may increase the demand for fuel-efficient engines. The increasing sales of electric vehicles have further boosted the sales of passenger cars as various countries promote their adoption through strict regulations, subsidies, tax credits, and other incentives.

According to the International Energy Agency, new electric car registrations in Europe reached nearly 3.2 million in 2023, increasing by almost 20% compared to 2022, with battery electric cars accounting for 70% of the electric car stock in the same year.

Governments worldwide have also launched various schemes and policies to encourage buyers to opt for electric vehicles over conventional ones. One such initiative that promotes the purchase of electric vehicles is the California Zero Emission Vehicle (ZEV) program, which aims to have 1.5 million electric vehicles on the road by 2025. Other countries offering various incentives include India, China, the United Kingdom, South Korea, France, Germany, Norway, and the Netherlands.

Similarly, vehicles registered in Europe until December 31, 2025, are exempted from the ownership tax for 10 years, and this exemption is valid until December 31, 2030. Such policies are boosting the sales of electric passenger cars.

Owing to the growth of electric passenger car sales, companies manufacturing EV connectors are seeing a growing opportunity in the EV segment and are focusing on various technological advancements to develop new products.

In May 2024, Eaton launched the higher-power version of its low-voltage 48-volt DC-DC converter. The newly released converter takes power from a 48-volt system and steps it down to 12 volts to run accessories and other low-power systems.

Such factors, along with high disposable income, rising brand awareness, and high-power purchase parity, contribute to the segment's growth.

Asia-Pacific is Dominating the Market

Asia-Pacific holds the majority share in the electric vehicle high voltage DC-DC converter market. With countries like China leading the EV sales, the market is expected to grow significantly during the forecast period.

China and Japan are inclined toward innovation, technology, and the development of advanced electric vehicles. Moreover, countries such as Indonesia are engaged in large electric mobility projects.

China is a key player in the electric vehicle industry worldwide. The country's government is encouraging people to adopt electric vehicles. China plans to switch to electric mobility entirely by 2040. The Chinese electric passenger cars market is also one of the largest worldwide, and it has been growing rapidly over the last few years. It is expected to grow further during the forecast period, which may positively impact the electric vehicle high voltage DC-DC converter market. Several key players in the market are partnering with other players to develop power electronics components.

Heavy investments made by automotive companies are expected to cater to the growing demand for electric vehicles and contribute to the high sales of vehicles. OEMs offer electric vehicles in different segments, ranging from hatchbacks like the MG Comet EV to high-end sedans like Tesla Model 3.

The transition to electric vehicles requires significant investments as carmakers focus on upgrading manufacturing sites, which is important in companies fulfilling electrification targets.

The Indian electric vehicle market is in its growing stage. Automobile manufacturers in India, such as TATA, Mahindra, and MG, are taking initiatives to provide affordable electric driving options. The government is also supporting electric mobility to reduce the exhaust emissions of greenhouse gases in the country.

In March 2024, the Indian government approved an EV policy under which import duty concessions will be given to companies setting up manufacturing units in the country with a minimum investment of USD 500 million, a strategic move to attract major global players like US-based Tesla.

Automobile manufacturers in India are also taking initiatives and investing in R&D practices to provide affordable electric cars in India. For instance, in February 2021, Hyundai announced an investment of USD 0.12 billion to develop new affordable EVs. The vehicles would be manufactured locally, and the company is in talks with local vendors to source the components. Hyundai may also seek a strategic partnership with its sister brand, Kia, as it plans to add EVs to its portfolio in India. The company is working on a mass-market, more affordable electric car for India, which was planned to be launched in 2024.

Due to such factors, the demand for DC-DC converters in vehicles is likely to increase, thus boosting the market's growth over the forecast period.

Electric Vehicle High-Voltage DC-DC Converter Industry Overview

The electric vehicle high voltage DC-DC converter market is consolidated and led by global and regionally established players. The companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions.

- In June 2024, TDK announced the addition of adjustable current limit models to the TDK-Lambda brand 300W-rated i7C non-isolated DC-DC converter series. The new models are suitable for generating additional high-power DC outputs from 12 V, 24 V, and 48 V system voltages in medical, automated guided vehicles (AGV), and other industries.

Some of the major players in the market include Robert Bosch GmbH, TDK Corporation, Toyota Industries Corporation, and HELLA GmbH & Co. KGaA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Adoption of Electric Vehicles

- 4.1.2 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Converters Generate Noise During Operation, Which May Hinder the Target Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD Million)

- 5.1 Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Plug-in Hybrid Vehicles

- 5.2.2 Battery Electric Vehicles

- 5.2.3 Fuel Cell Electric Vehicles

- 5.3 Cooling Method

- 5.3.1 Liquid Cooled

- 5.3.2 Air Cooled

- 5.4 Input Voltage

- 5.4.1 200 V - 450 V

- 5.4.2 450 V - 800 V

- 5.4.3 800 V - 1000 V

- 5.5 Output Voltage

- 5.5.1 12 V - 24 V

- 5.5.2 24 V - 48 V

- 5.6 Output Power

- 5.6.1 Less Than 2 kW

- 5.6.2 2 kW and Above

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Norway

- 5.7.2.7 Poland

- 5.7.2.8 Russia

- 5.7.2.9 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Chile

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Other Countries

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Continental AG

- 6.2.2 Robert Bosch GmbH

- 6.2.3 Valeo Group

- 6.2.4 ABB Ltd

- 6.2.5 DENSO Corporation

- 6.2.6 Hella GmbH & Co. KGaA

- 6.2.7 Toyota Industries Corporation

- 6.2.8 Infineon Technologies AG

- 6.2.9 Texas Instruments

- 6.2.10 STMicroelectronics

- 6.2.11 TDK-Lambda Corporation

- 6.2.12 Shinry Technologies

- 6.2.13 Delta Electronics

- 6.2.14 Vicor Corporation

- 6.2.15 Hyundai Mobis Ltd