|

시장보고서

상품코드

1937301

자동차용 DC-DC 컨버터 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Dc-Dc Converter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

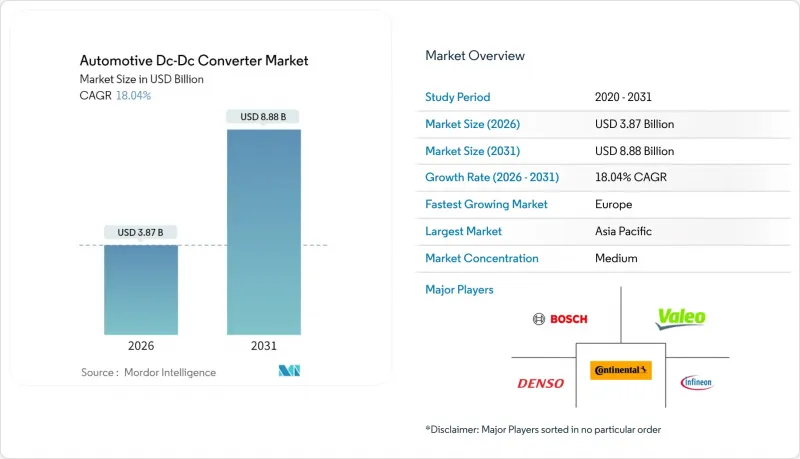

자동차용 DC-DC 컨버터 시장은 2025년 32억 8,000만 달러에서 2026년에는 38억 7,000만 달러에 이르고, 2026-2031년 CAGR 18.04%로 성장을 지속하여 2031년에는 88억 8,000만 달러에 달할 것으로 예측됩니다.

급속한 전기화, 48V 마일드 하이브리드 아키텍처로의 전환, 400V에서 800V로 구동용 배터리의 전환이 이러한 대폭적인 확장을 뒷받침하고 있습니다. 고전압 영역과 저전압 영역 사이의 에너지 흐름을 관리하는 양방향 토폴로지는 차세대 전기 플랫폼의 설계 기반을 형성하고 있습니다. SiC 및 GaN과 같은 광대역 갭 반도체는 전력 밀도와 효율을 지속적으로 향상시켜 소형 경량 컨버터 모듈을 실현하고 차량용 패키징 요구 사항을 단순화합니다. 지역별로는 중국의 생산 규모로 인해 아시아태평양이 선두를 달리고 있으며, 유럽은 엄격한 CO2 목표와 탄소중립 의무로 인해 가장 빠르게 성장하고 있습니다. 경쟁 환경은 전체 시스템 공급업체와 전문 반도체 제조업체 간의 협력으로 정의되며, 성능의 한계를 높이고 첨단 파워 일렉트로닉스 시장 출시를 가속화하고 있습니다.

세계 자동차용 DC-DC 컨버터 시장 동향과 전망

급증하는 BEV 및 PHEV 생산량

세계 전기차 생산 계획이 확대됨에 따라 자동차 제조업체들이 급속 충전 시간을 단축하는 800V 파워트레인으로 전환함에 따라 고효율 컨버터에 대한 수요가 증가하고 있습니다. 테슬라가 전 차종에 48V 배전을 채택한 것은 배선 간소화 및 효율 향상으로의 전환을 뒷받침합니다. 상용차 제조업체들도 이에 발맞추어 맥트럭은 신뢰성 저하 없이 구동계, 보조장치, 운전자 편의성을 제공하기 위해 멀티존 컨버터를 통합하고 있습니다. 양방향 토폴로지를 통해 일상적인 V2G(차량에서 그리드로의 전력 공급)가 가능해져 주차된 차량이 에너지 자산으로 탈바꿈합니다. 이는 고급 컨버터 설계에 대한 대량 생산 수요를 더욱 강화할 것입니다. 생산규모의 확대는 실리콘 단가를 더욱 낮추고, 첨단 기술의 양산 시장으로의 보급을 용이하게 합니다. BYD가 2024년에 테슬라를 능가하는 판매량을 기록했다는 사실은 생산량이 차량 가격대에 관계없이 컨버터 수요를 직접적으로 증폭시킨다는 것을 보여줍니다.

전 세계 48V 마일드 하이브리드 의무화 추세

유럽의 CO2 규제 시한과 북미의 CAFE 기준 강화로 인해 OEM 업체들은 완전한 전동화 투자 없이 배출량을 단계적으로 줄이는 48V 시스템을 도입해야 하는 상황에 직면해 있습니다. 유럽자동차부품산업협회(ACEA)는 2025년까지 새로운 마일드 하이브리드 차량에 48V 아키텍처가 거의 보편적으로 채택될 것으로 예측했습니다. 대형차 부문도 그 뒤를 따르고 있습니다. 국내 완성차 업체들도 규제 시장에서의 수출 경쟁력을 유지하기 위해 유사한 기술을 확대하고 있습니다. ISO 21780에 기반한 통일된 표준은 크로스 플랫폼 구현을 용이하게 하여 개발 기간을 크게 단축하고 단기적으로 컨버터 출하량 증가를 촉진하고 있습니다.

전력 밀도의 열 관리 한계

수 kW 이상의 컨버터는 특히 상용차 섀시의 제한된 공간에서 기존의 알루미늄 방열판으로는 대응할 수 없는 실리콘 소자 및 자기 코어의 온도 상승이 발생합니다. 벨파스사는 중장비 가동 사이클의 접합부 온도 제약에 대응하기 위해 액체 냉각식 4kW 유닛을 도입했습니다. SiC 및 GaN 소자는 효율적이지만, 400kHz 스위칭 시 여전히 충분한 열을 방출하며, 고급 냉각판 또는 유전체 오일 채널이 필요합니다.

부문 분석

상용 플랫폼은 2026년부터 2031년까지 19.50%의 연평균 복합 성장률(CAGR)을 나타내고, 승용차 모델보다 더 높은 성장세를 보였습니다. 2025년에는 자동차 DC-DC 컨버터 시장의 63.55%를 차지할 것으로 예측됩니다. 차량 구매자들은 연료 및 유지보수 비용 절감으로 인한 e-모빌리티의 투자 회수를 계산하고 있으며, 이는 보조 유압 펌프, 리프트 및 공조 시스템을 구동하는 견고한 컨버터에 대한 수요를 가속화하고 있습니다. 상용차 DC-DC 컨버터 시장 규모는 정부의 무공해 트럭에 대한 지원책에 힘입어 2031년까지 21억 8,000만 달러 이상에 달할 것으로 예측됩니다. 승용차는 2025년 세계 경차 생산량이 8,000만 대를 돌파하고, 각 차량에 인포테인먼트, 조명, ADAS 도메인 컨트롤러를 위한 저전력 컨버터가 2-4개씩 탑재되면서 수량 기준으로 선도적인 위치를 유지할 것입니다.

채용 패턴에는 차이가 있습니다. 승용차 제조업체들은 차량 평균 배출량 목표 달성을 위해 48V 마일드 하이브리드 시스템을 우선시하는 반면, 트럭 제조업체들은 도심 공회전 금지 구역에 대응하기 위해 고전압 배터리 전기차(BEV)나 연료전지차(FCEV)로 직접 전환하는 사례가 증가하고 있습니다. 상용차의 운행 주기는 냉각판과 포팅 재료에 대한 부하를 더욱 증가시켜 열 계면 재료 공급업체에게 애프터마켓의 기회를 열어주고 있습니다. 차량에서 전력망으로의 전력 공급(V2G)을 통한 수익원은 야간 창고 충전 시 고정 전원 용량을 집약하는 물류 사업자를 끌어들여 양방향 컨버터의 출하량을 더욱 증가시키고 있습니다.

2025년 배터리 전기자동차(BEV)가 자동차 DC-DC 컨버터 시장의 73.12%를 차지할 것으로 예측됩니다. 이는 모든 BEV가 차량 내 부하를 위해 최소 1대의 고전압 컨버터가 필요하기 때문입니다. 그러나 마일드 하이브리드 차량 출하와 연동된 자동차 DC-DC 컨버터 시장 규모는 비용에 민감한 부문이 충전 인프라 제약을 피하기 위해 48V 시스템을 채택하는 움직임에 따라 2031년까지 연평균 복합 성장률(CAGR) 21.95%를 나타낼 것으로 예측됩니다. 양방향 토폴로지는 12V 납축전지 액세서리와 48V 리튬 팩을 연결하기 때문에 기존 전자기기를 보호하기 위해 엄격한 전압 조정 정밀도가 요구됩니다. 플러그인 하이브리드 차량은 구매 우대 혜택이 있는 시장에서는 여전히 존재 의의가 있지만, 컨버터 수량과 등급은 마일드 하이브리드와 BEV의 중간 정도에 위치합니다.

연료전지 전기자동차는 여전히 틈새 시장이지만, 각 스택은 고전압 직류를 공급하기 때문에 이를 12V로 강압 변환하고, 경우에 따라서는 배터리 부하 평준화를 위해 승압해야 합니다. 이에 컨버터 공급업체들은 제어용 ASIC의 재설계 없이 350V, 450V, 800V 버스에 대응할 수 있는 자기 부품을 교체할 수 있는 모듈형 기판을 개발하여 전체 추진 시스템 변형의 설계 기간을 단축하고 있습니다.

절연형 컨버터는 2025년 54.62%의 점유율을 차지할 것으로 예상되며, 이는 구동 회로와 보조 회로를 전기적으로 분리하는 안전 요구 사항에 의해 보장됩니다. 한편, 양방향 유닛은 22.05%의 연평균 복합 성장률(CAGR)을 기록했으며, V2L(Vehicle to Load) 및 V2G(Vehicle to Grid) 기능이 프리미엄 사양에서 주류 사양으로 전환됨에 따라 점유율을 확대할 것으로 예측됩니다. 이 제품들은 양방향의 원활한 전력 흐름을 실현하기 위해 2상 인터리브 토폴로지를 통합하고, 디지털 제어 루프와 실시간 진단 기능을 필요로 합니다. 비절연형 백부스트 단은 팩 전압이 60V 미만으로 억제되고 연면거리 확보가 용이한 비용 제약이 있는 마일드 하이브리드를 타겟으로 하고 있습니다.

실리콘 카바이드(SiC) 채용으로 스위칭 주파수가 200kHz 이상으로 상승하여 변압기의 권선 수와 자기 부피를 줄입니다. Wolfspeed의 22kW 레퍼런스 제품은 SiC 모듈이 양방향 패키지를 소형화하고 피크 효율을 향상시키는 실례를 보여줍니다. 고급 펌웨어를 통해 컨버터는 데이터 노드 역할을 하며, CAN-FD를 통해 효율, 온도, 고장 코드를 보고합니다. 예지보전 서비스 기반을 구축합니다.

지역별 분석

아시아태평양은 중국의 자동차 생산 규모와 일본의 파워일렉트로닉스 기술력을 바탕으로 2025년 자동차 DC-DC 컨버터 시장에서 46.92%의 매출 점유율을 차지하며 세계 1위를 차지할 것으로 예측됩니다. 중국의 전기차 판매량은 2024년 690만 대에서 2025년 1,100만 대로 급증할 것으로 예상되며, 승용차 및 소형 상용차 부문의 컨버터 탑재량이 크게 증가할 것으로 예측됩니다. TDK 등 일본 기업들은 높이를 30% 줄인 소형 평면 자기 부품을 제공하여 지역의 기술 혁신 우위를 강화하고 있습니다. 국내 OEM 업체들은 정부 로드맵에 따라 2030년까지 450만대의 무공해차 도입을 목표로 하고 있으며, 이에 따라 국내 반도체 생태계는 자동차 양산용 SiC 웨이퍼의 인증을 추진하고 있습니다. 보조금은 단계적으로 축소될 것이며, 도시 단위의 무공해 지역과 유럽 수출 수요로 인해 국내 수요는 견조하게 유지될 것입니다.

유럽에서는 2030년까지 차량 CO2 배출량 규제가 57.5g/km로 강화되는 것을 배경으로 2031년까지 연평균 복합 성장률(CAGR)이 21.24%로 가장 빠른 성장세를 보이고 있습니다. 독일 공급업체는 800V 작동에 최적화된 컨버터와 결합된 희토류가 없는 전기 모터를 공동 설계하여 전체 시스템의 효율성에 중점을 두었습니다. EU 대체연료 인프라 규정에서는 그리드 서비스 프로토콜 대응을 위해 양방향 충전기가 의무화되어 컨버터 사양이 복잡해지고 있습니다. 발레오와 로옴의 제휴 등으로 열 시뮬레이션 소프트웨어와 SiC 웨이퍼 기술이 결합되어 산업화 일정이 가속화됩니다. UNECE R-100에 기반한 표준화된 시험 절차로 컨버터 국경을 초월한 인증이 효율화되어 신규 진출기업 시장 진입이 용이해집니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

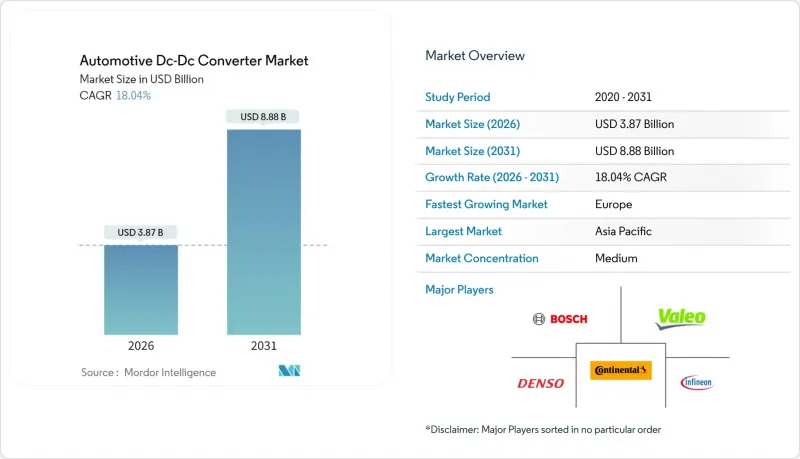

LSH 26.03.10The automotive DC-DC converter market is expected to grow from USD 3.28 billion in 2025 to USD 3.87 billion in 2026 and is forecast to reach USD 8.88 billion by 2031 at 18.04% CAGR over 2026-2031.

Rapid electrification, the shift to 48 V mild-hybrid architectures, and the move from 400 V to 800 V traction batteries underpin this substantial expansion. Bidirectional topologies that manage energy flow between high- and low-voltage domains now form the design baseline for next-generation electric platforms. Wide-bandgap semiconductors such as SiC and GaN continue to raise power density and efficiency, enabling smaller, lighter converter modules that simplify vehicle packaging requirements. Regionally, Asia-Pacific dominates due to Chinese production scale, while Europe grows fastest due to stringent CO2 targets and carbon-neutral mandates. Competitive dynamics are defined by collaboration between full-system suppliers and specialized semiconductor houses, pushing the performance envelope and accelerating time-to-market for advanced power electronics.

Global Automotive Dc-Dc Converter Market Trends and Insights

Surging BEV and PHEV Production

Global electric-vehicle build plans amplify demand for high-efficiency converters as automakers migrate to 800 V powertrains that shorten fast-charging times. Tesla's adoption of 48 V power distribution across its portfolio validates the shift toward slimmed-down wiring and better efficiency . Commercial players follow suit; Mack Trucks integrates multi-zone converters to supply traction, auxiliaries, and driver comforts without sacrificing reliability. Bidirectional topologies enable routine vehicle-to-grid export, turning parked fleets into energy assets and reinforcing volume pull for sophisticated converter designs. Higher production scale further drives down per-unit silicon cost, easing the pathway for advanced technology diffusion into mass-market segments. BYD's surge past Tesla in 2024 revenue underlines how production volume directly multiplies converter demand across vehicle price tiers.

Global 48 V Mild-Hybrid Mandates

CO2 compliance deadlines in Europe and tightening Corporate Average Fuel Economy targets in North America push OEMs to deploy 48 V systems that incrementally cut emissions without full electrification investment. The European Association of Automotive Suppliers projects the near-ubiquity of 48 V architectures in new mild-hybrid models by 2025. Heavy-duty segments follow: Eaton's 40-amp 48 V converters already power start-stop and e-PTO features in Class-8 trucks . Korean automakers are scaling similar technology to maintain export competitiveness in regulated markets. Harmonized standards under ISO 21780 ease cross-platform implementation, slashing development timelines and bolstering near-term converter shipments.

Thermal-Management Limits on Power Density

Converters exceeding a few kilowatts face silicon and magnetic core temperatures that can outpace traditional aluminum heat-sink solutions, especially in confined commercial-vehicle chassis. Bel Fuse introduced liquid-cooled 4 kW units to cope with junction-temperature constraints in heavy-equipment duty cycles. SiC and GaN devices, though efficient, still dissipate enough heat at 400 kHz switching to require advanced cooling plates or dielectric oil channels.

Other drivers and restraints analyzed in the detailed report include:

- Lower SiC/GaN Device Costs

- Vehicle-to-Load Functionality

- Automotive-Grade Passive-Component Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial platforms recorded a 19.50% CAGR between 2026 and 2031, outpacing passenger models, holding 63.55% automotive DC-DC converter market share in 2025. Fleet buyers calculate payback on e-mobility through reduced fuel and maintenance bills, accelerating demand for rugged converters that power auxiliary hydraulic pumps, lifts, and climate control. The automotive DC-DC converter market size for commercial vehicles is projected to cross USD 2.18 billion by 2031, supported by state incentives for zero-emission trucks. Passenger cars retain volume leadership due to global light-vehicle output topping 80 million units in 2025, each embedding two to four low-power converters for infotainment, lighting, and ADAS domain controllers.

Adoption patterns differ: passenger car OEMs favor 48 V mild-hybrid systems to hit fleet-average emission targets, whereas truck makers leapfrog directly to high-voltage battery electrics or fuel cells to comply with urban no-idle zones. Commercial duty cycles also intensify stress on cooling plates and potting compounds, opening after-sales opportunities for thermal-interface material suppliers. Vehicle-to-grid revenue streams attract logistics operators that aggregate stationary power capacity during nightly depot charging, further lifting bidirectional converter shipments.

Battery electrics captured 73.12% of the automotive DC-DC converter market share in 2025 because every BEV needs at least one high-voltage converter for cabin loads. However, the automotive DC-DC converter market size tied to mild-hybrid shipments will post a 21.95% CAGR through 2031 as cost-sensitive segments adopt 48 V systems to skirt charging-infrastructure constraints. Bidirectional topologies bridge 12 V lead-acid accessories and 48 V lithium packs, demanding tight voltage-regulation accuracy to protect legacy electronics. Plug-in hybrids maintain relevance in markets with purchase incentives, but their converter count and rating sit between mild-hybrid and BEV extremes.

Fuel-cell electrics remain niche, yet each stack feeds high-voltage DC that must be down-converted to 12 V and sometimes boosted for battery load-leveling. Converter suppliers, therefore, develop modular boards that swap magnetics to suit 350 V, 450 V, or 800 V buses without re-spinning the control ASICs, compressing engineering timelines across propulsion variants.

Isolated converters held a 54.62% share in 2025, assured by safety requirements that galvanically separate traction and accessory circuits. Bidirectional units, however, will log a 22.05% CAGR, capturing incremental share as V2L and V2G features shift from premium to mainstream trims. These products integrate dual-phase interleaved topologies for smooth power flow in both directions, demanding digital control loops and real-time diagnostics. Non-isolated buck-boost stages target cost-constrained mild-hybrids where pack voltage stays below 60 V, easing creepage clearances.

Silicon carbide raises switching frequency above 200 kHz, trimming transformer turns and magnetic volume. Wolfspeed's 22 kW reference showcases how SiC modules shrink the bidirectional package, boosting peak efficiency. Firmware sophistication turns converters into data nodes that report efficiency, temperature, and fault codes over CAN-FD, laying the groundwork for predictive maintenance services.

The Automotive DC-DC Converter Market Report is Segmented by Vehicle Type (Passenger Vehicle, and More), Propulsion Type (BEV, and More), Product Type (Isolated Converter, and More), Input-Voltage Range (Below 40V, and More), Output-Power Rating (Below 3kW, and More), Application (12V Auxiliary Loads, and More), End-User (OEM Factory-Fit and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific leads the automotive DC-DC converter market with a 46.92% revenue share in 2025, driven by China's vehicle manufacturing scale and Japan's power-electronics expertise. China's electric-vehicle sales jumped from 6.9 million units in 2024 to an expected 11 million units by 2025, multiplying converter content across passenger and light-commercial segments. Japanese firms such as TDK present miniaturized planar magnetics that cut height by 30%, reinforcing the region's innovation edge. South Korean OEMs target 4.5 million zero-emission vehicles by 2030 under government roadmaps, spurring local semiconductor ecosystems to qualify SiC wafers for automotive volume. Though subsidies taper, domestic demand remains buoyed by city-level zero-emission zones and export pull to Europe.

Europe records the fastest 21.24% CAGR through 2031 on the back of fleet CO2 caps tightening to 57.5 g/km 2030. German suppliers co-design rare-earth-free e-motors with converters optimized for 800 V operation, emphasizing full-system efficiency. The EU Alternative Fuels Infrastructure Regulation requires bidirectional chargers to support grid-service protocols, elevating converter specification complexity. Partnerships like Valeo-ROHM bring together thermal-simulation software and SiC wafer leadership to accelerate industrialization schedules . Standardized test procedures under UNECE R-100 streamline cross-border homologation for converters, easing market access for new entrants.

- Bosch

- Denso

- Valeo

- Continental

- Infineon Technologies

- BorgWarner

- Toyota Industries

- TDK

- Panasonic

- Hella

- Aptiv

- Alps Alpine

- Marelli

- Hyundai Mobis

- Vicor

- Delta Electronics

- ZF Friedrichshafen

- onsemi

- Texas Instruments

- Littelfuse

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging BEV and PHEV Production

- 4.2.2 Global 48 V Mild-Hybrid Mandates

- 4.2.3 Lower Sic / Gan Device Costs

- 4.2.4 Shift To Zonal E/E Architectures.

- 4.2.5 Vehicle-To-Load (V2L) Functionality

- 4.2.6 On-Board E-Power (ePTO) Demand in Commercial EVs

- 4.3 Market Restraints

- 4.3.1 Thermal-Management Limits on Power Density

- 4.3.2 Automotive-Grade Passive-Component Shortages

- 4.3.3 Cyber-Security Homologation Overheads

- 4.3.4 Electromagnetic-Interference (EMI) Compliance At 400 Khz

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Vehicle Type

- 5.1.1 Passenger Vehicle

- 5.1.2 Commercial Vehicle

- 5.2 By Propulsion Type

- 5.2.1 Battery Electric Vehicle (BEV)

- 5.2.2 Plug-in Hybrid EV (PHEV)

- 5.2.3 Fuel-Cell EV (FCEV)

- 5.2.4 Mild-Hybrid (48 V MHEV)

- 5.3 By Product Type

- 5.3.1 Isolated Converter

- 5.3.2 Non-Isolated Converter

- 5.3.3 Bi-directional Converter

- 5.4 By Input-Voltage Range

- 5.4.1 Below 40 V

- 5.4.2 40 - 70 V

- 5.4.3 Above 70 V

- 5.5 By Output-Power Rating

- 5.5.1 Below 3 kW

- 5.5.2 3 - 6 kW

- 5.5.3 Above 6 kW

- 5.6 By Application

- 5.6.1 12 V Auxiliary Loads

- 5.6.2 48 V/12 V Bidirectional Systems

- 5.6.3 High-Voltage Traction Support

- 5.6.4 ADAS and Infotainment Power

- 5.6.5 Thermal-Management Systems

- 5.7 By End-User

- 5.7.1 OEM Factory-Fit

- 5.7.2 Aftermarket Retrofit

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Rest of North America

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Russia

- 5.8.3.6 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 South Korea

- 5.8.4.5 Rest of Asia-Pacific

- 5.8.5 Middle-East and Africa

- 5.8.5.1 United Arab Emirates

- 5.8.5.2 Saudi Arabia

- 5.8.5.3 Turkey

- 5.8.5.4 Egypt

- 5.8.5.5 South Africa

- 5.8.5.6 Rest of Middle-East and Africa

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Bosch

- 6.4.2 Denso

- 6.4.3 Valeo

- 6.4.4 Continental

- 6.4.5 Infineon Technologies

- 6.4.6 BorgWarner

- 6.4.7 Toyota Industries

- 6.4.8 TDK

- 6.4.9 Panasonic

- 6.4.10 Hella

- 6.4.11 Aptiv

- 6.4.12 Alps Alpine

- 6.4.13 Marelli

- 6.4.14 Hyundai Mobis

- 6.4.15 Vicor

- 6.4.16 Delta Electronics

- 6.4.17 ZF Friedrichshafen

- 6.4.18 onsemi

- 6.4.19 Texas Instruments

- 6.4.20 Littelfuse