|

시장보고서

상품코드

1692454

액체 수소 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Liquid Hydrogen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

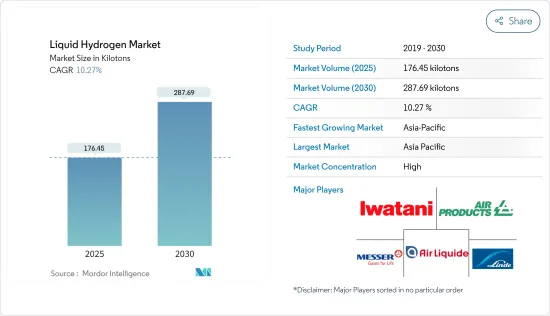

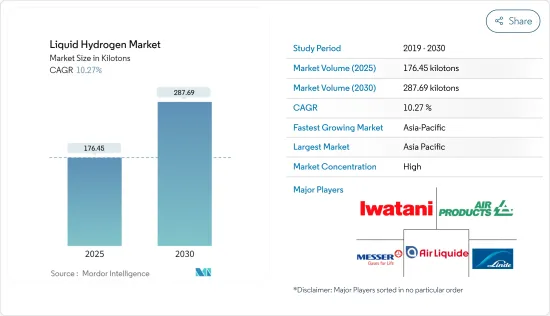

액체 수소 시장 규모는 2025년에 176.45킬로톤으로 추정되고, 2030년에는 287.69킬로톤에 달할 것으로 예측되며, 예측기간(2025-2030년)의 CAGR은 10.27%를 나타낼 전망입니다.

코로나19로 인해 모든 산업이 제조 공정을 중단하면서 시장에 부정적인 영향을 미쳤습니다. 봉쇄, 사회적 거리두기, 무역 제재로 인해 글로벌 공급망 네트워크에 막대한 차질이 발생했습니다. 그러나 2021년에는 상황이 회복되어 예측 기간 동안 시장에 도움이 될 것으로 예상됩니다.

주요 하이라이트

- 중기적으로 연구 대상 시장을 이끄는 주요 요인은 우주 탐사를 위한 액체 수소에 대한 수요 증가와 상업용 차량의 수소 연료 전지 채택 증가입니다.

- 반면에 취급 및 저장과 관련된 높은 비용이 시장 성장을 제한 할 가능성이 높습니다.

- 수소를 해양 연료로 활용하는 것에 대한 강조가 커지고 항공 우주 산업에서 혁신이 증가하는 것은 향후 몇 년 동안 시장에 기회로 작용할 것입니다.

- 아시이평양이 가장 높은 시장 점유율을 차지했으며, 이 지역은 예측 기간 동안 시장을 지배할 것으로 보입니다.

액체 수소 시장 동향

시장을 지배할 항공우주 산업

- 항공우주 산업은 공항 수하물 취급부터 수소 항공기 추진, 우주 산업의 극저온 엔진에 이르기까지 다양한 응용 분야에 액체 수소를 적용하는 것을 의미합니다.

- 추진 용도에서는 액체 수소는 액체 산소와 같은 산화제와 함께 연료로 사용됩니다.

- 국제항공운송협회(IATA)에 따르면 상업용 항공사의 전 세계 매출은 2021년 4,720억 달러, 2022년 7,270억 달러로 전년 대비 43.6%의 성장률을 기록할 것으로 전망됩니다. 또한 2023년 말에는 7,790억 달러에 달할 것으로 예상됩니다.

- 팬데믹 둔화에서 항공 교통량이 회복되면서 항공 부문의 탄소 중립으로의 전환을 앞당기기 위해 여러 국가에서 온실가스 배출량 규제에 대한 규제가 강화되고 있습니다.

- 전 세계의 우주 프로그램은 다양한 항공 우주 작전을 위한 로켓 연료로 액체 수소를 사용하고 있습니다.

- 2022년에는 여러 국가의 우주 프로그램에 대한 글로벌 정부 지출이 크게 증가했습니다.

- 기술 발전의 급속한 성장은 더 많은 첨단 위성에 대한 수요를 창출하고 있습니다.

- 미국 항공우주국(NASA)에 따르면, 발사할 때마다 각 셔틀의 로켓 엔진은 약 50만 갤런의 차가운 액체 수소를 연소하며,또한 23만 9000갤런이 저장의 보일오프나 이송 작업으로 고갈합니다.

- 따라서 예측 기간 동안 항공우주 산업에서 액체 수소에 대한 수요가 증가할 것으로 예상됩니다.

아시이평양이 시장을 독점

- 아시이평양 지역은 중국, 인도, 일본 등의 액체 수소 수요 증가로 인해 예측 기간 동안 가장 큰 액체 수소 시장이 될 것으로 예상됩니다.

- 특히 항공우주 및 자동차 산업에서 대체 연료에 대한 중국의 강한 성향으로 인해 중국은 액체 수소에 대한 견고하고 유리한 시장으로 자리매김하고 있습니다.

- 중국의 연료전지 자동차 판매 및 생산량 증가도 액체 수소 기반 연료전지에 대한 수요 증가에 기여했습니다.

- 수소 연료는 항공기와 자동차에 동력을 공급할 수 있는 기회를 제공하며, 인도에서는 수소 동력 엔진을 발전시키기 위한 상당한 개발과 이니셔티브가 진행되고 있습니다. 예를 들어, 2023년 2월 릴라이언스 인더스트리 리미티드와 아쇼크 레이랜드는 인도 최초의 수소 내연기관(H2-ICE) 구동 대형 트럭을 출시했습니다.

- 자동차 검사 및 등록 정보 협회(AIRIA)에 따르면 2022 회계연도 3월 31일 기준 일본에서 사용되고 있는 수소 연료전지 자동차는 약 7,110대로, 2021년도의 5,280대로부터 증가했습니다.

- 따라서 위에서 언급한 요인으로 인해 아시이평양 지역의 액체 수소에 대한 수요는 예측 기간 동안 증가할 것으로 예상됩니다.

액체 수소 산업 개요

액체 수소 시장은 고도로 통합되어 있습니다. 시장의 주요 기업(특별한 순서 없음)에는 Air Liquide, Air Products and Chemicals Inc., Linde PLC, Iwatani Corporation, Messer Group GmbH 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 우주 탐사를위한 액체 수소에 대한 수요 증가

- 상업용 차량의 수소 연료 전지 채택 증가

- 억제요인

- 취급 및 보관과 관련된 높은 비용

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 유통

- 극저온 탱크

- 고압 튜브 트레일러

- 최종 사용자 산업

- 자동차

- 항공우주(우주 공간 포함)

- 해양

- 기타 최종 사용자 산업

- 지역

- 아시이평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시이평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 세계 기타 지역

- 남미

- 중동 및 아프리카

- 아시이평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%) 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Air Liquide

- Air Products and Chemicals, Inc.

- Iwatani Corporation

- Linde PLC

- Messer Group GMBH

- Nippon Sanso Holdings Corporation

- Universal Industrial Gases Inc.

제7장 시장 기회와 앞으로의 동향

- 해양 연료로서의 수소 이용 중시의 고조

- 항공우주산업에 있어서의 기술 혁신의 진전

The Liquid Hydrogen Market size is estimated at 176.45 kilotons in 2025, and is expected to reach 287.69 kilotons by 2030, at a CAGR of 10.27% during the forecast period (2025-2030).

COVID-19 negatively impacted the market as all the industries halted their manufacturing processes. Lockdowns, social distances, and trade sanctions triggered massive disruptions to global supply chain networks. However, the condition is recovered in 2021, which is expected to benefit the market during the forecast period.

Key Highlights

- In the medium term, the major factors driving the market studied are the growing demand for liquid hydrogen for space exploration and the increasing adoption of hydrogen fuel cells in commercial vehicles.

- On the flip side, the high cost associated with handling and storage is likely to restrain the market growth.

- Growing emphasis on utilizing hydrogen as a marine fuel and increasing innovations in the aerospace industry are likely to act as opportunities for the market in the coming years.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Liquid Hydrogen Market Trends

Aerospace Industry to Dominate the Market

- Aerospace industries imply the application of liquid hydrogen for various applications ranging from airport bagging handling to hydrogen aircraft propulsion to cryogenic engines in the space industry.

- In propulsion applications, liquid hydrogen is used in combination with an oxidizer, such as liquid oxygen, to serve as fuel. This combination yields the highest specific impulse, or efficiency in relation to the amount of propellant consumed, of any known rocket propellant.

- According to the International Air Transport Association (IATA), the global revenue for commercial airlines was valued at USD 472 billion in 2021 and USD 727 billion in 2022, registering a growth rate of 43.6% Y-o-Y. Furthermore, the revenue is expected to reach USD 779 billion by the end of 2023.

- As air traffic recovers from the pandemic slowdown, the regulations on controlling greenhouse gas emissions are being tightened in different economies to head forward with the transition to carbon neutrality in the aviation sector. For instance, the Federal Aviation Administration, in June 2022, proposed new climate rules for curtailing GHG emissions. The new rules will be applied to planes already in service, allowing manufacturers to improve aerodynamics and engine efficiency. The rules would enforce efficiency requirements for new subsonic jet aircraft, large turboprop and propellor planes that are not yet certified, and planes built after January 2028.

- Space programs across the world rely on liquid hydrogen as the rocket fuel for various aerospace operations. The recent growth in space programs has been driving the demand for liquid hydrogen in recent years.

- In 2022, global government expenditure for space programs in various countries increased considerably. For instance, in the United States, government spending grew from USD 54.59 billion in 2021 to USD 61.97 billion in 2022.

- Rapid growth in technological advancements is creating the demand for more advanced satellites. As a result, in 2022, over 186 attempts of orbital launches, of which 180 were successful.

- According to the National Aeronautics and Space Administration (NASA), for each launch, the rocket engines of each shuttle flight burn about 500,000 gallons of cold liquid hydrogen, with another 239,000 gallons depleted by storage boil-off and transfer operations. The large volume of consumption per operation, coupled with the growing frequency of launches, is propelling the demand for liquid hydrogen.

- Therefore, the demand for liquid hydrogen is expected to grow in the aerospace industry during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to be the largest market for liquid hydrogen during the forecast period owing to the growing liquid hydrogen demand in China, India, and Japan, among others.

- China's strong inclination toward alternative fuels, particularly in the aerospace and automotive industries, positions the country as a robust and favorablemarket for liquid hydrogen. With substantial growth in the aerospace sector, including increased satellite launches and rocket missions, the demand for liquid hydrogen has witnessed a positive surge due to its essential role in rocket fuel.

- The rising sales and production of fuel cell vehicles in China have also contributed to the growing demand for liquid hydrogen-based fuel cells. According to the China Association of Automobile Manufacturers, the production and sales of hydrogen fuel cell vehicles in 2022 more than doubled compared to the previous year, with 3,626 and 3,367 units produced and sold, respectively.

- Hydrogen fuel presents opportunities for powering aircraft and automobiles, and significant developments and initiatives are taking place in India to advance hydrogen-powered engines. For instance, in February 2023, Reliance Industries Limited and Ashok Leyland launched India's first Hydrogen Internal Combustion Engine (H2-ICE) powered heavy-duty truck. This truck operates on hydrogen while maintaining a conventional diesel combustion engine architecture. With a 19 to 35 tons loading capacity, the H2-ICE truck enables a swift transition to cleaner energy at a relatively lower cost differential.

- According to the Automobile Inspection & Registration Information Association (AIRIA), as of March 31, FY 2022, Japan had approximately 7.11 thousand hydrogen fuel cell vehicles in use, representing an increase from 5.28 thousand in FY 2021. The majority of these hydrogen-fuel cell vehicles are hydrogen-fueled passenger cars.

- Hence, due to the abovementioned factors, the demand for liquid hydrogen in the Asia-Pacific region is expected to increase over the forecast period.

Liquid Hydrogen Industry Overview

The liquid hydrogen market is highly consolidated in nature. Some of the major companies in the market (not in any particular order) include Air Liquide, Air Products and Chemicals Inc., Linde PLC, Iwatani Corporation, and Messer Group GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Liquid Hydrogen for Space Exploration

- 4.1.2 Increasing Adoption of Hydrogen Fuel Cell in Commercial Vehicle

- 4.2 Restraints

- 4.2.1 High Cost Associated with Handling and Storage

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Distribution

- 5.1.1 Cryogenic Tank

- 5.1.2 High-Pressure Tube Trailers

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace (including Outer Space)

- 5.2.3 Marine

- 5.2.4 Other End-User Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Air Products and Chemicals, Inc.

- 6.4.3 Iwatani Corporation

- 6.4.4 Linde PLC

- 6.4.5 Messer Group GMBH

- 6.4.6 Nippon Sanso Holdings Corporation

- 6.4.7 Universal Industrial Gases Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Emphasis on Utilizing Hydrogen as a Marine Fuel

- 7.2 Increasing Innovations in Aerospace Industry