|

시장보고서

상품코드

1693553

중동 및 아프리카의 특수 비료 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Middle East & Africa Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

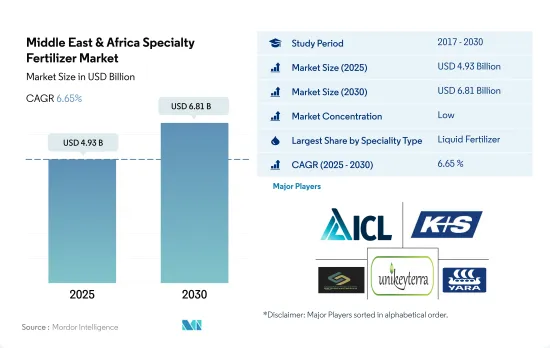

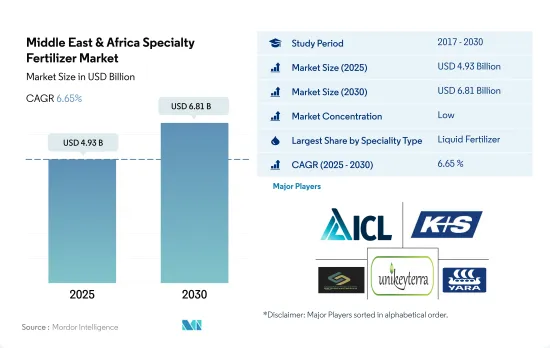

중동 및 아프리카의 특수 비료 시장 규모는 2025년 49억 3,000만 달러로 추정,되고, 2030년에는 68억 1,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR 6.65%로 성장할 것으로 예측됩니다.

영양 공급에 대한 의식 증가와 효율성이 시장 성장을 가속할 가능성

- 중동 및 아프리카의 특수 비료 시장은, 2022년에는 시장 전체의 7.6%의 점유율을 차지하며, 예측 기간 중 CAGR은 6.4%로 예측됩니다.

- 2022년에는 남아프리카, 나이지리아, 튀르키예가 시장의 11.4%, 8.3%, 4.9%를 차지하여 지배적인 국가로 부상했습니다. 비료 시험이 실시되고 있기 때문에 비료 제조업체에 초점이 되고 있습니다. 이 제조업체는 이러한 시장 특유의 요건을 채우도록 특수 제품을 조정해, 시장의 추가 확대에 박차를 가하고 있습니다.

- 2022년 중동 및 아프리카의 특수 비료 시장에서는 액체 비료가 48.5%로 큰 점유율을 차지했습니다. 이 비료는 지면에 살포할 수도, 엽면 살포할 수도 있습니다.

- 2022년에는 중동 및 아프리카의 특수 비료 시장에서 수용성 비료가 47.3%의 점유율을 차지하고 있었습니다.

- 최근 특수 비료에 대한 농가의 의식이 현저하게 높아지고 있습니다.

양분 공급에 대한 의식 증가와 효율성이 조사 기간 동안 시장 성장을 가속할 가능성

- 중동 및 아프리카의 특수 비료 시장은 2022년에는 시장 전체의 7.6%의 점유율을 차지했고, 2023년부터 2030년까지 CAGR은 6.4%로 예측됩니다.

- 2022년에는 남아프리카, 나이지리아, 튀르키예가 각각 11.4%, 8.3%, 4.9%의 점유율을 획득하여 시장의 지배적 국가로 부상했습니다. 정부가 비료시험을 지원하고 있기 때문에 비료 제조업체에 있어서 좋은 표적이 되고 있습니다.

- 액체 비료는 2022년 중동 및 아프리카의 특수 비료 시장의 48.5%를 차지하고 있으며 큰 점유율을 차지했습니다.

- 2022년에 특수 비료 시장의 47.0%를 차지한 수용성 비료는 용출의 영향을 받지 않기 때문에 영양 관리가 간소화됩니다.

- 이 시장에서는 특수 비료에 대한 농가의 의식이 급상승하고 있어 액체 비료, 수용성 비료, 방출 제어형 비료 수요가 높아지고 있기 때문에 시장의 견조한 성장이 전망되고 있습니다.

중동 및 아프리카 특수 비료 시장 동향

이 지역에서는 바람과 물에 의한 침식으로 농지가 황폐해 농작물의 재배가 과제가 되고 있습니다.

- 중동 및 아프리카 국가에서는 옥수수, 쌀, 사탕수수, 콩 등의 농작물은 통상 4-5월에 파종되어, 9-10월에 수확됩니다. 천수 관개의 땅은 바람과 물에 의한 침식으로 인해 열화되어 지속 불가능한 농법에 의해 더욱 악화되고 있습니다. 2022년, 이 지역의 농작물 재배 면적은 2억 4,900만 헥타르에 달했고, 2017년부터 3.9% 증가했습니다. 특히 밀의 재배 면적은 2017년부터 2022년까지 4.6% 증가했습니다.

- 아프리카에서는 나이지리아가 수수 생산으로 선도하고, 에티오피아가 이어집니다.의 약 45%를 차지하고 있습니다. 수수는 가뭄이나 홍수에 강하고, 다양한 토양 조건에 적응해, 중동 및 아프리카의 건조지대에서 선호되는 주식 작물이며, 식량과 소득의 안정을 보증하고 있습니다.

- 이 지역에서는 지난 10년간 인구가 23% 이상 증가했습니다.

건조한 기후는 토양의 질소 고갈을 가속화하고 농업 생산성에 중요한 영양소가 되었습니다.

- 질소, 인, 칼륨은 식물의 성장에 빠뜨릴 수 없는 주요 영양소입니다. 질소와 인은 식물 조직의 주요 성분인 단백질과 핵산에 필수적입니다.

- 구체적으로 중동 및 아프리카의 농작물에서 질소, 인, 칼륨의 평균 시용량은 각각 234.8kg/헥타르, 127.4kg/헥타르, 161.0kg/헥타르였습니다. 중동 및 아프리카에서는 밀, 수수, 쌀, 옥수수와 같은 주요 농작물이 주로 재배되고 있습니다.

- 1차 영양소 중 중동 및 아프리카에서의 소비량은 질소가 압도적으로 많아 2022년에는 170만 톤에 달했습니다. 이 우위성은 이 지역의 밭 면적이 크고, 전체의 약 95.0%를 차지하고 있기 때문이며, 그 결과로서 1차 영양소에 대한 수요가 높은 것에 이유가 있습니다.

중동 및 아프리카의 특수 비료 산업 개요

중동 및 아프리카의 특수 비료 시장은 단편화되어 있으며 상위 5개사에서 16.78%를 차지하고 있습니다. 이 시장 주요 기업은 ICL Group Ltd, K+S Aktiengesellschaft, Safsulphur, Unikeyterra Chemical, Yara International ASA입니다(알파벳순).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 주요 작물의 작부 면적

- 밭 작물

- 원예 작물

- 평균 양분 시용률

- 미량 영양소

- 밭 작물

- 원예 작물

- 1차 영양소

- 밭 작물

- 원예 작물

- 2차 다량 영양소

- 밭 작물

- 원예 작물

- 미량 영양소

- 관개 농지

- 규제 프레임워크

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 스페셜리티 유형

- CRF

- 폴리머 코트

- 폴리머 유황 코팅

- 기타

- 액체 비료

- SRF

- 수용성

- CRF

- 시비 모드

- 시비

- 엽면 살포

- 토양

- 작물 유형

- 밭작물

- 원예작물

- 잔디 및 관상용

- 생산국

- 나이지리아

- 사우디아라비아

- 남아프리카

- 튀르키예

- 기타 중동 및 아프리카

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Azra Group AS

- Foskor

- Gavilon South Africa(MacroSource, LLC)

- ICL Group Ltd

- KS Aktiengesellschaft

- Kynoch Fertilizer

- Safsulphur

- Unikeyterra Chemical

- Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Middle East & Africa Specialty Fertilizer Market size is estimated at 4.93 billion USD in 2025, and is expected to reach 6.81 billion USD by 2030, growing at a CAGR of 6.65% during the forecast period (2025-2030).

Growing awareness and efficiency in nutrient supply may drive market growth

- The Middle East & Africa's specialty fertilizers market held a 7.6% share of the total market value in 2022, with a projected CAGR of 6.4% during the forecast period. The relatively lower adoption of specialty fertilizers by farmers, coupled with their higher costs compared to conventional options, explains this modest market share.

- In 2022, South Africa, Nigeria, and Turkey emerged as dominant players, capturing 11.4%, 8.3%, and 4.9% of the market, respectively. These countries, with their sizable populations, ample land availability, and government-led fertilizer trials, have become focal points for fertilizer manufacturers. These manufacturers are tailoring specialty products to meet the specific requirements of these markets, fueling further market expansion.

- Liquid fertilizers held a significant share of 48.5% in the Middle East & Africa's specialty fertilizers market in 2022. Growers in this region have recognized the benefits of liquid fertilizers, including their easy soil penetration, fast nutrient absorption by plants, and reduced wastage. These fertilizers can be applied either to the ground or as a foliar spray. This presents a lucrative opportunity for manufacturers eyeing the liquid fertilizers segment over the study period.

- In 2022, water-soluble fertilizers commanded a 47.3% share in the Middle East & Africa's specialty fertilizers market. These fertilizers offer a simplified nutrition management approach as their nutrient levels remain unaffected by leaching.

- A notable uptick in farmers' awareness regarding specialized fertilizers has occurred in recent years. This, coupled with a growing demand for liquid, water-soluble, and controlled-release fertilizers, is expected to be the driving force behind the market's growth.

Growing awareness and efficiency in nutrient supply may drive market growth during the study period

- The Middle East & Africa's specialty fertilizers market held a 7.6% share of the total market value in 2022, with a projected CAGR of 6.4% from 2023 to 2030. Specialty fertilizers face a lower market share, primarily due to limited farmer awareness and their relatively higher cost compared to conventional alternatives.

- In 2022, South Africa, Nigeria, and Turkey emerged as the dominant players in the market, capturing shares of 11.4%, 8.3%, and 4.9%, respectively. These countries, with their sizable populations, ample land availability, and government-backed fertilizer trials, have become prime targets for fertilizer manufacturers. These manufacturers are tailoring their offerings to the specific requirements of these nations, further fueling market growth.

- Liquid fertilizers held the lion's share, accounting for 48.5% of the Middle East & Africa's specialty fertilizers market in 2022. Growers in the region have recognized the advantages of liquid fertilizers, such as better soil penetration, enhanced nutrient absorption, and reduced wastage. These fertilizers can be applied either to the ground or as foliar sprays, presenting a significant growth opportunity for manufacturers in this segment.

- Water-soluble fertilizers, capturing 47.0% of the specialty fertilizers' market value in 2022, offer simplified nutrition management as they are not affected by leaching.

- The market has witnessed a surge in farmer awareness about specialized fertilizers and a rising demand for liquid, water-soluble, and controlled-release fertilizers, setting the stage for robust market growth.

Middle East & Africa Specialty Fertilizer Market Trends

Deterioration of agricultural lands due to erosion caused by wind and water will pose a challenge in cultivating crops in the region.

- In countries in the Middle East & Africa, field crops such as corn, rice, sorghum, and soybeans are typically sown in April-May and harvested between September and October. Agriculture in the region faces significant challenges, including scarcity of land and water. Both rain-fed and irrigated lands are deteriorating due to erosion from wind and water, exacerbated by unsustainable farming practices. Field crops occupy a dominant position, accounting for 90% of the region's agricultural land. In 2022, the total area under field crop cultivation in the region reached 249 million hectares, marking a 3.9% increase from 2017. Corn alone commands a significant share, covering 17.8% of the total field crop area. Wheat cultivation area witnessed a 4.6% rise from 2017 to 2022. Specifically, the region's corn cultivation area was 44.3 million hectares in 2022.

- Nigeria leads in sorghum production, followed by Ethiopia in Africa. Sorghum, a vital cereal crop, constitutes 50% of Nigeria's total cereal output and occupies approximately 45% of the land dedicated to cereal production. Sorghum's resilience to drought and waterlogging, along with its adaptability to diverse soil conditions, makes it a preferred staple crop in the drier regions of the Middle East & Africa, ensuring food and income security.

- The region has witnessed a population growth of over 23% in the last decade. Despite limited production capacity, the forecast indicates a rise in food imports. However, the agricultural sector has consistently expanded, paralleled by an increase in cultivated land.

The arid climate leads to a faster depletion of nitrogen in the soil, making it a crucial nutrient for agricultural productivity.

- Nitrogen, phosphorous, and potassium are primary nutrients crucial for plant growth. Nitrogen and phosphorous are integral to proteins and nucleic acids, key components of plant tissue. Meanwhile, potassium significantly influences the quality of harvested crops. Field crops, on average, receive an application rate of 174.4 kg per hectare for these primary nutrients.

- Specifically, the average application rates for nitrogen, phosphorous, and potassium in field crops across the Middle East & Africa stood at 234.8 kg/hectare, 127.4 kg/hectare, and 161.0 kg/hectare, respectively. The Middle East & Africa predominantly cultivate major field crops like wheat, sorghum, rice, and corn. In 2022, the average application rates for primary nutrients in these crops were 144.5 kg/hectare, 162.9 kg/hectare, 152.6 kg/hectare, and 245.24 kg/hectare, respectively.

- Of the primary nutrients, nitrogen dominates consumption in the Middle East & Africa, reaching 1.7 million metric tons in 2022. Nitrogen is the most crucial nutrient for crop yields, and given the prevalent deficiency of nitrogen in regional soils, it has become the most widely applied fertilizer. This dominance is driven by the region's substantial field crop area, comprising around 95.0% of the total, and the resulting high demand for primary nutrients. This emphasis on self-sufficiency and reducing import reliance underscores the growing market for field crops in the region.

Middle East & Africa Specialty Fertilizer Industry Overview

The Middle East & Africa Specialty Fertilizer Market is fragmented, with the top five companies occupying 16.78%. The major players in this market are ICL Group Ltd, K+S Aktiengesellschaft, Safsulphur, Unikeyterra Chemical and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 Nigeria

- 5.4.2 Saudi Arabia

- 5.4.3 South Africa

- 5.4.4 Turkey

- 5.4.5 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Azra Group AS

- 6.4.2 Foskor

- 6.4.3 Gavilon South Africa (MacroSource, LLC)

- 6.4.4 ICL Group Ltd

- 6.4.5 K+S Aktiengesellschaft

- 6.4.6 Kynoch Fertilizer

- 6.4.7 Safsulphur

- 6.4.8 Unikeyterra Chemical

- 6.4.9 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms