|

시장보고서

상품코드

1693587

중동 및 아프리카의 군용기 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Middle-East and Africa Military Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

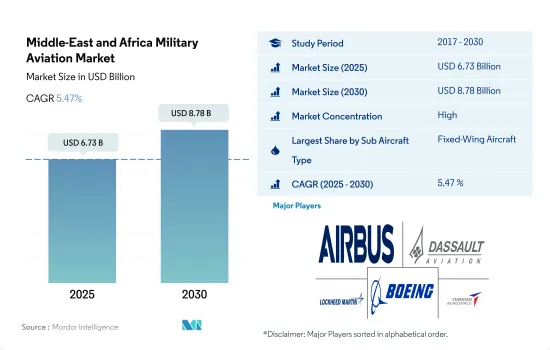

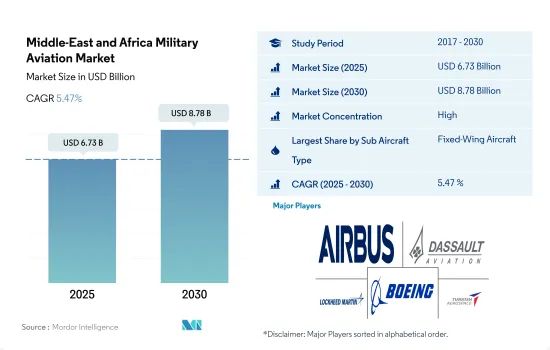

중동 및 아프리카의 군용기 시장 규모는 2025년에 67억 3,000만 달러로 추계되며, 2030년에는 87억 8,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR 5.47%로 성장할 것으로 예측됩니다.

예측기간 동안 고정익기가 시장을 독점할 전망

- 중동에서는 지난 수십 년간 시리아, 이라크, 예멘, 리비아에서 내전이 계속되고 있습니다. 이란, 이라크, 쿠웨이트, 오만, 사우디아라비아, 바레인, 아랍에미리트(UAE)으로 구성되어 있습니다.

- 사우디아라비아 정부는 '비전 2030' 하에 현지 생산을 강화하기 위해 2030년까지 현지 군비 지출을 50%까지 늘릴 계획입니다.

- 예측 기간 동안 고정익군용기의 멀티롤 부문이 가장 높은 성장을 이룰 것으로 예상됩니다. 예를 들어, UAE는 80대의 Rafael을, 카타르는 72대의 F-15를 조달할 예정입니다.

- 헬리콥터 분야에서는 멀티미션 헬리콥터가 예측 기간 동안 가장 높은 성장이 예상됩니다. 이집트는 24대의 EW-149 멀티미션 헬리콥터를 구입할 예정입니다.

노후화된 기체의 업그레이드와 갱신 계획이 수요를 견인

- 중동의 2022년 국방비는 약 1,840억 달러로 2022년 대비 3.2% 이상 감소했습니다.

- 사우디아라비아(11%), 이집트(5.7%), 카타르(4.6%), UAE(2.8%), 알제리(2.6%) 등 국가들은 2017-2021년간 세계적으로 주요 무기 수입국으로 고정 날개기 및 회전익기 부문의 다기능기 및 실용기 조달을 위한 활발한 프로그램을 가지고 있습니다.

- 아랍에미리트(UAE)에 의한 Lockheed Martin F-35 전투기 50기, 이집트에 의한 Rafale 전투기 30기(45억 달러 상당), 사우디아라비아에 의한 개량형 UH-60M 헬리콥터 25기 등의 조달은 2017-2022년에 이 지역에서 일어난 주요 한 조달의 일부입니다.이 지역에서는 항공기의 능동 함대가 증가할 것으로 예상됩니다.

- 2017-2022년 동안 중동 및 아프리카에서는 조달이 약 4% 증가했습니다. 미국, 프랑스, 러시아는 이 지역의 멀티롤 항공기의 주요 공급국입니다.

중동 및 아프리카 군용기 시장 동향

이 지역의 주요 군사 강국은 국방비를 급증시키고 있습니다.

- 중동의 2022년 국방 지출은 약 1,840억 달러로, 2021년에 비해 3.2% 이상 감소했습니다. 사우디아라비아, 이집트, 카타르, 아랍에미리트(UAE), 알제리 등 국가들은 2017년부터 2022년까지 국방 지출이 많았던 지역의 주요 국가입니다.

- 사하라 이남의 아프리카 군사비 합계는 2022년 203억 달러로 2021년 대비 7.3%, 2013년 대비 18% 감소했습니다. 이 지역의 2대 지출국인 나이지리아와 남아프리카가 2022년 군사비 감소를 주도했습니다. 2022년 이스라엘의 군사비는 2009년 이후 처음으로 감소했습니다. 총 234억 달러는 2021년보다 4.2% 감소했습니다.

- 사우디아라비아의 군사비 전년대비(YoY) 성장률은 2022년에는 2021년 대비 16% 증가하여 2018년 이후 전년 대비 증가했습니다. 사우디아라비아의 작년 군사비는 750억 달러로 추정되었습니다. 이 감소는 사우디아라비아가 예멘에서 군인을 철수하기 시작했다는 비난과 겹쳤습니다. 그러나 사우디 정부는 이 의혹을 부인하고, 인원은 재배치되고 있다고 주장했습니다. 2015년 이후 사우디아라비아는 전쟁에서 황폐한 예멘에 대한 군사 작전으로 연합국을 이끌고 있어 전투는 2022년까지 이어졌습니다. 사우디아라비아의 군사 예산은 GDP 대비 7.4%로 2022년 우크라이나에 이어 세계 2위였습니다.

구식 항공기의 대체 계획이 중동 군용기의 주요 원동력이 될 것으로 예측됨

- 2022년 현재 중동 및 아프리카의 현역 항공기 보유수는 9,460대였습니다. 이 지역의 총 활동 항공기 보유 수는 2017년에 비해 1% 증가했습니다. 남아프리카, 알제리, 아랍에미리트(UAE), 사우디아라비아, 튀르키예, 이집트, 카타르는 이 지역의 총 활성 플릿의 58%를 차지했습니다.

- 중동에서는 2022년 국방비가 1,570억 달러로 각각 2020년에서 8.6%, 2012년에서 5.6% 증가했습니다. 북아프리카가 49%를 차지하는 반면 사하라 이남의 아프리카는 총 지출의 51%를 차지했습니다.

- 사우디아라비아, 카타르, 아랍에미리트(UAE) 등의 국가들은 근대전 수요를 충족하기 위해 항공기 보유수를 확대하고 있습니다.

- 아프리카의 현역 기체 수는 2017년에 비해 2022년에는 1% 감소했습니다. 아랍에미리트(UAE), 카타르, 튀르키예와 같은 국가들이 약 400대의 항공기 조달을 계획하고 있기 때문에 이 지역의 액티브 항공기 보유수는 증가할 가능성이 있습니다.

중동 및 아프리카 군용기 산업 개요

중동 및 아프리카의 군용기 시장은 상당히 통합되어 있으며 상위 5개사에서 80.37%를 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 국내총생산

- 액티브 플릿 데이터

- 국방 지출

- 규제 프레임워크

- 밸류체인 분석

제5장 시장 세분화

- 서브 항공기 유형

- 고정익기

- 멀티롤 항공기

- 훈련용 항공기

- 수송기

- 기타

- 회전익기

- 멀티미션 헬리콥터

- 수송용 헬리콥터

- 기타

- 고정익기

- 국가명

- 알제리

- 이집트

- 카타르

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Airbus SE

- ATR

- Bombardier Inc.

- Dassault Aviation

- Embraer

- General Dynamics Corporation

- Leonardo SpA

- Lockheed Martin Corporation

- The Boeing Company

- Turkish Aerospace Industries

- United Aircraft Corporation

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Middle-East and Africa Military Aviation Market size is estimated at 6.73 billion USD in 2025, and is expected to reach 8.78 billion USD by 2030, growing at a CAGR of 5.47% during the forecast period (2025-2030).

Fixed-wing aircraft is expected to dominate the market during the forecast period

- There have been ongoing civil wars in Syria, Iraq, Yemen, and Libya in the Middle East during the past few decades. For instance, the nations in and around the Persian Gulf engage in border conflicts and spend a considerable amount on the procurement of defense equipment, including aircraft and rotorcraft. These nations consist of Iran, Iraq, Kuwait, Oman, Saudi Arabia, Bahrain, and the United Arab Emirates (UAE).

- The government of Saudi Arabia is planning to increase local military equipment spending to 50% by 2030 to strengthen local manufacturing under Vision 2030. The government is encouraging local manufacturing through contracts and other support initiatives. Although the country does not have indigenous aircraft development capabilities, it manufactures foreign aircraft under license.

- During the forecast period, the multi-role segment in fixed-wing military aircraft is expected to witness the highest growth. The major reason behind this growth is that several countries, such as the UAE, Egypt, Nigeria, and Turkey, are procuring next-generation combat aircraft and replacing their aging fleets. For instance, the UAE plans to procure 80 Rafael, and Qatar will procure 72 F-15s. Egypt, Algeria, and Turkey are likely to procure a total of around 40 combat aircraft.

- In the helicopter segment, multi-mission helicopters are expected to see the highest growth during the forecast period. Countries in this region will procure multi-mission helicopters to enhance overall combat capabilities. By 2024, Egypt will purchase 24 EW-149 multi-mission helicopters. Algeria intends to buy 42 Mi-28 attack helicopters by 2024, and Turkey plans to buy over 160 helicopters.

Fleet upgradation and replacement programs for the aging fleet driving the demand

- The defense expenditure in the Middle Eastern region was around USD 184 billion in 2022, with a decline of over 3.2% compared to 2022. In contrast, it was around USD 39.4 billion in Africa in 2022, with a decline of around 5% from 2021.

- Countries such as Saudi Arabia (11%), Egypt (5.7%), Qatar (4.6%), UAE (2.8%), and Algeria (2.6%) were major arms importers globally during 2017-2021 and have active programs for procurement of multirole and utility aircraft in the fixed-wing and rotorcraft segment.

- The procurements such as 50 Lockheed Martin F-35 fighter jets by UAE, the 30 Rafale fighter jets by Egypt worth USD 4.5 billion, and the 25 modified UH-60M helicopters by Saudi Arabia were some of the major procurements that happened in the region during 2017-2022. The aircraft's active fleet is expected to increase in the region. Middle Eastern countries like UAE, Saudi Arabia, Qatar, and Turkey are expected to procure newer aircraft for fleet modernization and expansion during the forecast period.

- During 2017-2022, procurement grew around 4% in the Middle East & Africa region. This growth was driven by overt intervention by regional powers and ongoing conflicts between Iran, Saudi Arabia, and UAE. The US, France, and Russia are this region's major supplier nations of multi-role aircraft. Additionally, fleet up-gradation and replacement programs for the aging fleet are expected to grow the region's military aviation market.

Middle-East and Africa Military Aviation Market Trends

Major military powers in the region have surged their defense expenditure

- Defense expenditures in the Middle Eastern region were around USD 184 billion in 2022, a decline of over 3.2% compared to 2021. In contrast, it was around USD 39.4 billion in Africa in 2022, with a decline of over 5% from 2021. Countries such as Saudi Arabia, Egypt, Qatar, United Arab Emirates, and Algeria were the major countries in the region with a high defense expenditure during 2017-22. They have active procurement programs for multi-role and utility aircraft in fixed-wing segments.

- Sub-Saharan Africa's combined military expenditure stood at USD 20.3 billion in 2022, down by 7.3% compared to 2021 and 18% compared to 2013. Nigeria and South Africa, the sub-regions two largest spenders, led the decline in military spending in 2022. In 2022, Israel's military spending fell for the first time since 2009. Its total of USD 23.4 billion was 4.2% lower than in 2021.

- The year-on-year (Y-o-Y) growth in Saudi Arabia's military spending was 16% in 2022 compared to 2021, the first Y-o-Y increase since 2018. Saudi Arabia's military expenditure was estimated at USD 75.0 billion last year. The reduction coincided with accusations that Saudi Arabia had started to remove its military personnel from Yemen. However, the Saudi government denied the allegations and insisted that the personnel were just being redeployed. Since 2015, Saudi Arabia has been leading a coalition in a military campaign against the war-torn nation of Yemen, and the fighting continued into 2022. Saudi Arabia had the second-largest military budget in the world, at 7.4% of GDP, after Ukraine in 2022.

Fleet replacement programs for older aircraft are projected to be the main driver for Middle Eastern military aviation

- As of 2022, the Middle East & Africa had an active fleet of 9,460 aircraft. The total active aircraft fleet increased by 1% in the region compared to 2017. South Africa, Algeria, the United Arab Emirates, Saudi Arabia, Turkey, Egypt, and Qatar accounted for 58% of the total active fleet in the region.

- In the Middle East, defense spending in 2022 totaled USD 157 billion, an increase of 8.6% from 2020 and 5.6% from 2012, respectively. While North Africa accounted for 49%, Sub-Saharan Africa accounted for 51% of the total spending.

- Countries such as Saudi Arabia, Qatar, and the United Arab Emirates are expanding their aircraft fleet size to fulfill the demands of modern warfare. They may continue to produce and acquire next-generation aircraft during the forecast period. The regional armed forces are also enhancing the capabilities of helicopters with cutting-edge technology to obtain military superiority over the external threat.

- Africa's active fleet size decreased by 1% in 2022 compared to 2017. South Africa, Algeria, and Egypt accounted for 45% of the total fleet in Africa. The fleet may increase in the coming years as major countries like Algeria and Egypt plan to procure around 100 aircraft. The Middle East & Africa's active fleet increased by 8% compared to 2017. Saudi Arabia, the United Arab Emirates, Qatar, and Turkey accounted for 59% of the total fleet in the Middle East. During the forecast period, the active aircraft fleet may increase in the region as countries like the United Arab Emirates, Qatar, and Turkey plan to procure around 400 aircraft.

Middle-East and Africa Military Aviation Industry Overview

The Middle-East and Africa Military Aviation Market is fairly consolidated, with the top five companies occupying 80.37%. The major players in this market are Airbus SE, Dassault Aviation, Lockheed Martin Corporation, The Boeing Company and Turkish Aerospace Industries (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Gross Domestic Product

- 4.2 Active Fleet Data

- 4.3 Defense Spending

- 4.4 Regulatory Framework

- 4.5 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Aircraft Type

- 5.1.1 Fixed-Wing Aircraft

- 5.1.1.1 Multi-Role Aircraft

- 5.1.1.2 Training Aircraft

- 5.1.1.3 Transport Aircraft

- 5.1.1.4 Others

- 5.1.2 Rotorcraft

- 5.1.2.1 Multi-Mission Helicopter

- 5.1.2.2 Transport Helicopter

- 5.1.2.3 Others

- 5.1.1 Fixed-Wing Aircraft

- 5.2 Country

- 5.2.1 Algeria

- 5.2.2 Egypt

- 5.2.3 Qatar

- 5.2.4 Saudi Arabia

- 5.2.5 United Arab Emirates

- 5.2.6 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 ATR

- 6.4.3 Bombardier Inc.

- 6.4.4 Dassault Aviation

- 6.4.5 Embraer

- 6.4.6 General Dynamics Corporation

- 6.4.7 Leonardo S.p.A

- 6.4.8 Lockheed Martin Corporation

- 6.4.9 The Boeing Company

- 6.4.10 Turkish Aerospace Industries

- 6.4.11 United Aircraft Corporation

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms