|

시장보고서

상품코드

1693654

승용차 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Passenger Cars - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

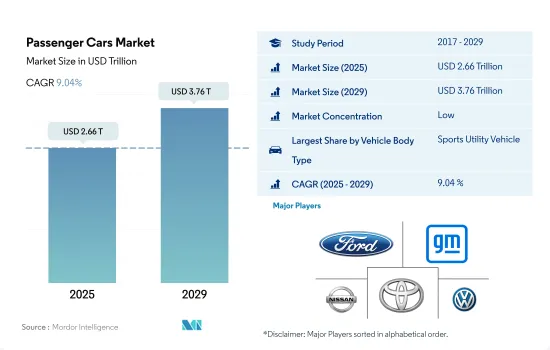

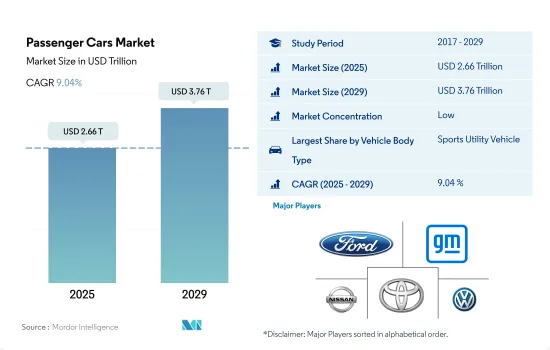

승용차 시장 규모는 2025년에 2조 6,600억 달러로 추정되고, 2029년에는 3조 7,600억 달러에 이를것으로 예측되며, 예측 기간(2025-2029년)의 CAGR은 9.04%를 나타낼 것으로 예측됩니다.

인구 증가, 소비력 증가, 전기차 및 하이브리드 기술 도입이 2024년부터 2030년까지 승용차 시장의 성장에 기여할 것으로 예상됩니다.

- 승용차 시장은 주로 중산층 가구의 수요 증가와 신흥 경제국의 생활 수준 향상에 힘입어 상당한 성장을 보이고 있습니다.

- 각국 정부는 전기자동차(EV) 도입을 촉진하기 위해 적극적인 조치를 취하고 있습니다. 특히 중국, 인도, 프랑스, 영국 등의 국가에서는 2040년까지 휘발유와 디젤 차량을 단계적으로 퇴출하겠다는 목표를 세웠습니다. 주요 업계 기업은 엄격한 배출 규범(예 : 인도의 바라트 6단계)을 준수하면서 생산 능력을 늘리고 있으며, 중국, 인도, 일본, 한국과 같은 국가에서는 2040년까지 내연기관(ICE) 차량의 신규 판매를 금지할 계획을 발표했습니다.

- 포드 자동차, 현대자동차, 닛산 자동차, 도요타 자동차, 폭스바겐 등 이 분야의 선도 기업들은 합작 투자, 합병, 신제품 출시, R&D 등의 전략적 움직임을 통해 시장 입지를 강화하고 있습니다. 이들 자동차 제조업체는 향후 5-10년 동안 배터리 구동 차량 개발 및 생산에 무려 5,150억 달러를 투자하여 전통적인 연소 엔진에서 벗어나는 변화를 예고하고 있습니다.

세계의 승용차 시장은 전기자동차로의 전환, 기술 혁신, 소비자 행동의 변화로 인해 역동적으로 진화하고 있습니다.

- 세계의 승용차 시시장은 기술 발전, 소비자 선호도 변화, 엄격한 환경 규제 등으로 인해 큰 변화를 겪고 있습니다. 최근에는 탄소 배출을 줄이기 위한 전 세계적인 노력과 지속 가능성에 대한 소비자들의 인식이 높아지면서 전기자동차로의 전환이 두드러지게 나타나고 있습니다. 전 세계 정부는 전기차 구매에 대한 인센티브와 충전 인프라에 대한 투자로 이러한 변화를 지원하고 있으며, 이는 잠재적 구매자들의 주행 거리에 대한 불안감을 극복하는 데 중요한 역할을 하고 있습니다.

- 경제적 요인은 승용차 시장을 형성하는 데 중추적인 역할을 합니다.

- 향후 몇 년 동안 승용차 시장은 자율주행 기술, 커넥티드 카 기능, 첨단 안전 시스템과 같은 혁신이 더욱 보편화되면서 계속 발전할 것으로 예상됩니다. 이러한 기능은 운전 경험을 향상시킬 뿐만 아니라 도로 안전을 개선하고 교통 혼잡을 줄일 수 있을 것으로 기대됩니다. 또한 서비스형 모빌리티(MaaS)의 부상으로 사람들이 차량 소유에 대한 인식이 바뀌면서 공유 교통 솔루션을 선호하는 개인 차량 소유가 감소할 가능성이 있습니다.

세계의 승용차 시장 동향

전 세계적인 수요 증가와 정부 지원으로 전기차 시장 성장 촉진

- 전기자동차(EV)는 에너지 효율성을 높이고 온실가스 및 공해 배출을 줄일 수 있는 잠재력에 힘입어 자동차 산업에서 필수 불가결한 존재가 되었습니다. 이러한 급증은 주로 환경에 대한 관심이 높아지고 정부의 지원 노력에 기인합니다. 특히 전 세계의 전기차 판매량은 2021년에 비해 2022년에 10.82%의 견고한 성장세를 보였습니다.

- 런던 경찰청 및 소방청과 같은 선도적인 제조업체와 기관들은 전기 모빌리티 전략을 적극적으로 추진하고 있습니다. 예를 들어, 이들은 2025년까지 무공해 차량 목표를 설정하고 2030년까지 밴의 40%를 전기화하고 2040년까지 완전 전기화를 달성한다는 목표를 세웠습니다.

- 아시이평양과 유럽은 배터리 기술 및 차량 전기화의 발전에 힘입어 전기차 생산을 주도할 것으로 보입니다. 2020년 5월, 기아자동차 유럽은 전기화로의 전략적 전환을 알리는 '플랜 S'를 발표했습니다. 이 결정은 유럽에서 기아자동차의 전기차 판매량이 기록적으로 증가한 이후 내려진 것입니다. 기아는 2025년까지 승용차, SUV, MPV 등 다양한 부문에 걸쳐 11개의 전기차 모델을 전 세계에 출시한다는 야심찬 계획을 세우고 있습니다.

승용차 산업 개요

승용차 시장은 세분화되어 있으며 상위 5개 기업이 35.10%를 점유하고 있습니다. 이 시장의 주요 업체는 Ford Motor Company, General Motors Company, Nissan Motor Co. Ltd., Toyota Motor Corporation 및 Volkswagen AG(알파벳 순 정렬)입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 인구

- 아프리카

- 아시이평양

- 유럽

- 중동

- 북미

- 남미

- 1인당 GDP

- 아프리카

- 아시이평양

- 유럽

- 중동

- 북미

- 남미

- 자동차 구입을 위한 소비 지출(CVP)

- 아프리카

- 아시이평양

- 유럽

- 중동

- 북미

- 남미

- 인플레이션율

- 아프리카

- 아시이평양

- 유럽

- 중동

- 북미

- 남미

- 자동차 대출 금리

- 공유 차량 서비스

- 전기화의 영향

- EV 충전소

- 배터리 팩 가격

- 아프리카

- 아시이평양

- 유럽

- 중동

- 북미

- 남미

- Xev 신모델 발표

- 중고차 판매

- 연료 가격

- OEM 생산 통계

- 규제 프레임워크

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 차량 구성

- 승용차

- 해치백

- 세단

- SUV

- 승용차

- 추진 부문

- 하이브리드 자동차 및 전기자동차

- 연료 카테고리별

- BEV

- FCEV

- HEV

- PHEV

- ICE

- 연료 카테고리별

- 천연가스

- 디젤

- 가솔린

- LPG

- 하이브리드 자동차 및 전기자동차

- 지역별

- 아시이평양

- 중국

- 인도

- 일본

- 유럽

- 벨기에

- 체코 공화국

- 프랑스

- 독일

- 이탈리아

- 노르웨이

- 폴란드

- 러시아

- 스페인

- 영국

- 북미

- 캐나다

- 멕시코

- 미국

- 남미

- 아르헨티나

- 브라질

- 아시이평양

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Bayerische Motoren Werke AG

- Daimler AG(Mercedes-Benz AG)

- Ford Motor Company

- General Motors Company

- Honda Motor Co. Ltd.

- Hyundai Motor Coportaion

- Kia Corporation

- Nissan Motor Co. Ltd.

- Toyota Motor Corporation

- Volkswagen AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 출처 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Passenger Cars Market size is estimated at 2.66 trillion USD in 2025, and is expected to reach 3.76 trillion USD by 2029, growing at a CAGR of 9.04% during the forecast period (2025-2029).

Rising population, increasing spending power, and adoption of electric vehicles and hybrid technology are all expected to contribute to the growth of the passenger car market between 2024 and 2030

- The market for passenger cars is witnessing significant growth, primarily driven by the increasing demand from middle-income households and improving living standards in emerging economies. Additionally, the affordability of these vehicles is attracting consumers. Technological advancements, like the integration of all-EV charging stations with the Internet of Things (IoT) and real-time information solutions, have further fueled market expansion.

- Global governments have taken proactive measures to promote the adoption of electric vehicles (EVs). Notably, countries like China, India, France, and the United Kingdom have set targets to phase out petrol and diesel vehicles by 2040. Major industry players are ramping up production capacities, adhering to stringent emission norms (e.g., India's Bharat Stage 6), and countries like China, India, Japan, and South Korea have announced plans to ban the sales of new internal combustion engine (ICE) vehicles by 2040. These developments are driving the sales of passenger cars in the electromobility sector.

- Leading companies in the sector, including Ford Motor Company, Hyundai Motor Company, Nissan Motor Company Ltd, Toyota Motor Corporation, and Volkswagen AG, are bolstering their market presence through strategic moves like joint ventures, mergers, new product launches, and R&D. These automakers have committed a staggering USD 515 billion over the next five to ten years to develop and manufacture battery-powered vehicles, signaling a shift away from traditional combustion engines.

The global passenger car market is dynamically evolving, driven by shifts toward electric vehicles, technological innovations, and changing consumer behaviors

- The global passenger car market is undergoing significant transformations, which are driven by technological advancements, changing consumer preferences, and stringent environmental regulations. In recent years, there has been a marked shift toward electric vehicles, prompted by global efforts to reduce carbon emissions and the growing consumer awareness about sustainability. Governments worldwide are supporting this shift with incentives for EV purchases and investments in charging infrastructure, which are crucial for overcoming range anxiety among potential buyers. However, internal combustion engine vehicles still dominate the market in many regions, supported by improvements in fuel efficiency and emissions reductions.

- Economic factors play a pivotal role in shaping the passenger car market. The global economic slowdown and supply chain disruptions, initially sparked by the COVID-19 pandemic and exacerbated by geopolitical tensions, led to fluctuations in car sales. These disruptions have caused shortages in critical components such as semiconductors, impacting production rates and increasing vehicle prices.

- In the coming years, the passenger car market is expected to continue evolving, with innovations such as autonomous driving technologies, connected car features, and advanced safety systems becoming more prevalent. These features not only enhance the driving experience but also promise to improve road safety and reduce traffic congestion. Additionally, the rise of mobility-as-a-service (MaaS) is changing how people perceive vehicle ownership, potentially leading to decreased private car ownership in favor of shared transportation solutions.

Global Passenger Cars Market Trends

The rising global demand and government support propel electric vehicle market growth

- Electric vehicles (EVs) have become indispensable in the automotive industry, driven by their potential to enhance energy efficiency and reduce greenhouse gas and pollution emissions. This surge is primarily attributed to growing environmental concerns and supportive government initiatives. Notably, global EV sales witnessed a robust 10.82% growth in 2022 compared to 2021. Projections indicate that annual sales of electric passenger cars will surpass 5 million by the end of 2025, accounting for approximately 15% of total vehicle sales.

- Leading manufacturers and organizations, like the London Metropolitan Police & Fire Service, have been actively pursuing their electric mobility strategies. For instance, they have set a target of a zero-emission fleet by 2025, with a goal of electrifying 40% of their vans by 2030 and achieving full electrification by 2040. Similar trends are expected globally, with the period from 2024 to 2030 witnessing a surge in demand and sales of electric vehicles.

- Asia-Pacific and Europe are poised to dominate electric vehicle production, driven by their advancements in battery technology and vehicle electrification. In May 2020, Kia Motors Europe unveiled its "Plan S," signaling a strategic shift toward electrification. This decision came on the heels of record-breaking sales of Kia's EVs in Europe. Kia has ambitious plans to introduce 11 EV models globally by 2025, spanning various segments like passenger vehicles, SUVs, and MPVs. The company aims to achieve annual global EV sales of 500,000 by 2026.

Passenger Cars Industry Overview

The Passenger Cars Market is fragmented, with the top five companies occupying 35.10%. The major players in this market are Ford Motor Company, General Motors Company, Nissan Motor Co. Ltd., Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.1.1 Africa

- 4.1.2 Asia-Pacific

- 4.1.3 Europe

- 4.1.4 Middle East

- 4.1.5 North America

- 4.1.6 South America

- 4.2 GDP Per Capita

- 4.2.1 Africa

- 4.2.2 Asia-Pacific

- 4.2.3 Europe

- 4.2.4 Middle East

- 4.2.5 North America

- 4.2.6 South America

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.3.1 Africa

- 4.3.2 Asia-Pacific

- 4.3.3 Europe

- 4.3.4 Middle East

- 4.3.5 North America

- 4.3.6 South America

- 4.4 Inflation

- 4.4.1 Africa

- 4.4.2 Asia-Pacific

- 4.4.3 Europe

- 4.4.4 Middle East

- 4.4.5 North America

- 4.4.6 South America

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.9.1 Africa

- 4.9.2 Asia-Pacific

- 4.9.3 Europe

- 4.9.4 Middle East

- 4.9.5 North America

- 4.9.6 South America

- 4.10 New Xev Models Announced

- 4.11 Used Car Sales

- 4.12 Fuel Price

- 4.13 Oem-wise Production Statistics

- 4.14 Regulatory Framework

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Configuration

- 5.1.1 Passenger Cars

- 5.1.1.1 Hatchback

- 5.1.1.2 Sedan

- 5.1.1.3 Sports Utility Vehicle

- 5.1.1 Passenger Cars

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.2 Europe

- 5.3.2.1 Belgium

- 5.3.2.2 Czech Republic

- 5.3.2.3 France

- 5.3.2.4 Germany

- 5.3.2.5 Italy

- 5.3.2.6 Norway

- 5.3.2.7 Poland

- 5.3.2.8 Russia

- 5.3.2.9 Spain

- 5.3.2.10 UK

- 5.3.3 North America

- 5.3.3.1 Canada

- 5.3.3.2 Mexico

- 5.3.3.3 US

- 5.3.4 South America

- 5.3.4.1 Argentina

- 5.3.4.2 Brazil

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Bayerische Motoren Werke AG

- 6.4.2 Daimler AG (Mercedes-Benz AG)

- 6.4.3 Ford Motor Company

- 6.4.4 General Motors Company

- 6.4.5 Honda Motor Co. Ltd.

- 6.4.6 Hyundai Motor Company

- 6.4.7 Kia Corporation

- 6.4.8 Nissan Motor Co. Ltd.

- 6.4.9 Toyota Motor Corporation

- 6.4.10 Volkswagen AG

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms