|

시장보고서

상품코드

1913315

승용차 ADAS 시장 예측 : 기회, 성장 요인, 업계 동향 분석(2026-2035년)Passenger Vehicle ADAS Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

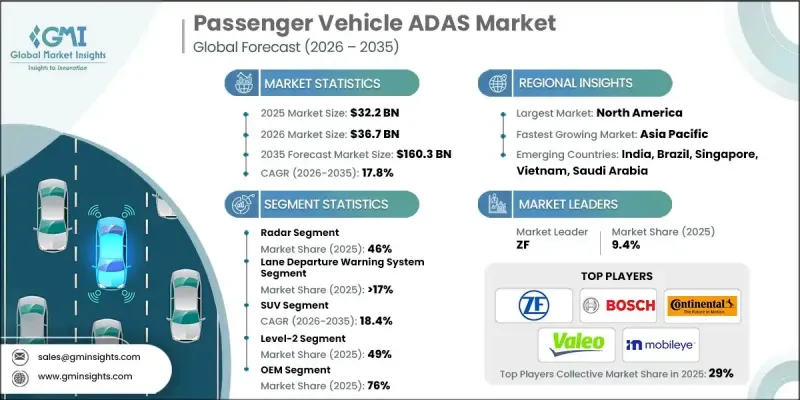

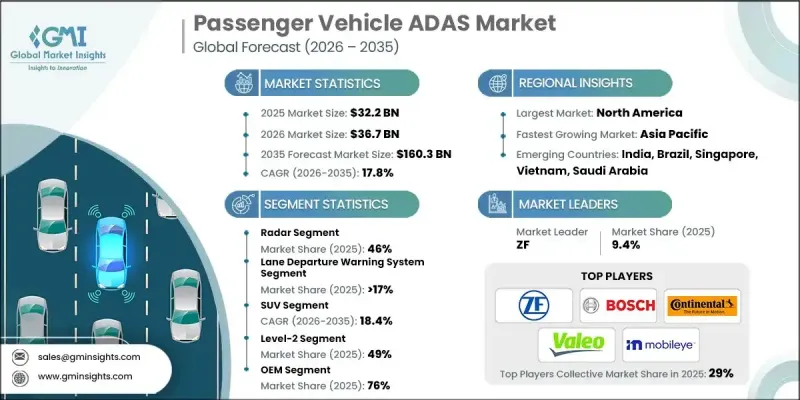

세계 승용차 ADAS 시장은 2025년에 322억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 17.8%로 성장하여 1,603억 달러에 이를 것으로 예측됩니다.

이 성장은 정부의 안전정책의 엄격화와 차량평가기준의 진화에 의한 것입니다. 이를 통해 자동차 제조업체는 컴플라이언스 목표 달성 및 경쟁력 강화를 위해 ADAS(첨단 운전 지원 시스템)를 통합하도록 촉구되었습니다. 구매자는 보호 성능, 운전 용이성, 피로 완화를 점점 더 중시하고 있으며, 이는 승용차 전체에서 지능형 지원 기술의 채택 확대를 지원합니다. 칩 제조 효율 향상, 대규모 생산, 공급업체 간의 경쟁 격화로 시스템 비용이 저하되고 차량 가격에 큰 영향을 주지 않고 ADAS의 보급이 프리미엄 모델을 넘어 확대되고 있습니다. 제조업체는 브랜드 이미지 강화, 가격 전략 지원, 장기 고객 충성도 구축을 위한 전략적 도구로 ADAS 기능 세트를 적극 활용하고 있습니다. 운전자 지원 기술에 대한 소비자의 이해가 깊어짐에 따라 수요가 더욱 강화되고 ADAS는 현대 승용차 설계의 핵심 요소로서의 지위를 확립하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 322억 달러 |

| 예측 금액 | 1,603억 달러 |

| CAGR | 17.8% |

레이더 부문은 2025년에 46%의 점유율을 차지했습니다. 레이더 시스템은 안정적인 성능과 신뢰성을 바탕으로 ADAS 아키텍처의 기반이 되는 감지 기술로 자리매김하고 있습니다. 한편, 이미지 센서는 정확한 시스템 해석을 지원하는 상세한 시각적 입력을 제공한다는 점에서 높은 평가를 받고 있습니다. 센서의 해상도와 처리 능력의 발전으로 전체 시스템의 정확성과 견고성이 향상되고 차세대 ADAS 배포에서 멀티센서 통합의 역할이 강화되었습니다.

차선 이탈 경보 시스템 부문은 2025년에 17%의 점유율을 차지했으며, 약 55억 달러 시장 규모가 되었습니다. 이 부문은 장시간 운전에 있어서 운전자 부담 경감과 쾌적성 향상을 지원하는 운전 지원 솔루션에 대한 수요 증가의 혜택을 받고 있습니다. 차량의 안정적인 위치 유지를 지원하는 본 시스템의 능력은 사용자의 신뢰성 향상과 지속적인 주의력 유지에 기여하고 있으며, 이러한 요인이 승용차 소유자의 본 시스템의 보급 확대를 촉진하고 있습니다.

미국 승용차 ADAS 시장은 2025년 107억 달러로 평가되었습니다. 고급 지원 기능에 대한 관심이 높아지고, 제조업체 주도의 기능 차별화, 인텔리전트 운전 기능의 보급 확대가 도입을 뒷받침하고 있습니다. 소프트웨어 중심 차량 플랫폼과 원격 업데이트 기능은 향상된 기능을 가속화하고 모든 차량 카테고리에서 새로운 수익 모델을 가능하게 합니다. 규제 측면에서도 구조화된 도입 프레임워크를 통해 관리되는 조건 하에서 보다 정교한 자동화 수준을 점진적으로 지원하는 움직임이 진행되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 수익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 규제상의 안전 요건

- 보다 안전한 차량에 대한 소비자의 기호

- 기술 비용 절감

- OEM의 차별화 전략

- 전기자동차의 성장

- 업계의 잠재적 위험 및 과제

- 첨단 시스템 통합의 복잡성

- 고도 자동화에 관한 규제의 불확실성

- 시장 기회

- 레벨 2 및 레벨 3 시스템 확대

- 센서 퓨전과 AI의 진보

- 애프터마켓 및 개조의 가능성

- 데이터 수익화 및 소프트웨어 서비스

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국- 연방자동차안전기준(FMVSS)

- 캐나다- 자동차 안전 규제

- 유럽

- 영국 - 도로 차량(구조 및 사용) 규제

- 독일 - 자율주행법

- 프랑스-모빌리티 지향법(LOM)

- 이탈리아- 도로 교통법(Codice della Strada)

- 스페인- 일반 교통 규제

- 아시아태평양

- 중국- 지능형 커넥티드카 규제

- 일본- 도로 운송 차량법

- 인도- 중앙 자동차 규칙

- 라틴아메리카

- 브라질- 국가 교통 법규

- 멕시코- 공식 멕시코 차량 안전 기준(NOM)

- 아르헨티나- 국가 교통법

- 중동 및 아프리카

- UAE-연방교통법

- 남아프리카- 국가 도로 교통법

- 사우디아라비아 - 교통 법규

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규기술

- 생산 통계

- 생산 허브

- 소비 허브

- 수출 및 수입

- 코스트 내역 분석

- 개발 비용 구조

- R&D 비용 분석

- 마케팅 및 판매 비용

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 배려형 이니셔티브

- ADAS 규격, 검증 및 안전 평가에 대한 영향

- Euro NCAP, Global NCAP, IIHS 평가가 ADAS 도입에 미치는 영향

- UNECE 규제(R79, R152, R157) 및 OEM의 적합 프로세스

- 자동화 레벨별 인증, 검증 및 시험 요건

- 안전평가가 OEM의 기능 패키징과 가격 설정에 미치는 영향

- ADAS 소프트웨어와 컴퓨팅 아키텍처의 개요

- 중앙 집중식 vs 도메인별 vs 영역별 ADAS 아키텍처

- SoC 및 ECU의 진화(ADAS ECU→중앙집중식 연산)

- 미들웨어, 운영 체제 및 실시간 제약

- OTA 갱신 대응 상황과 소프트웨어 수명 주기 영향

- ADAS 비용과 지불 의사액

- ADAS 데이터, 사이버 보안 및 기능 안전(ISO 26262/SOTIF)

- OEM의 ADAS 로드맵과 기능 전환 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 시스템별, 2022-2035

- 적응형 크루즈 컨트롤

- 사각지대감지 시스템

- 차선 이탈 경보 시스템

- 자동 긴급 브레이크(AEB)

- 전방 충돌 경보

- 나이트 비전 시스템

- 운전자 모니터링 시스템

- 타이어 공압 감시 시스템

- 헤드업 디스플레이

- 주차 지원 시스템

- 기타

제6장 시장 추정 및 예측 : 센서별, 2022-2035

- 레이더

- 라이더

- 초음파

- 카메라

- 기타

제7장 시장 추정 및 예측 : 차량별, 2022-2035

- 세단

- SUV

- 해치백

제8장 시장추정 및 예측 : 레벨별, 2022-2035

- 레벨 1

- 레벨 2

- 레벨 3

- 레벨 4

- 레벨 5

제9장 시장추정 및 예측 : 추진력별, 2022-2035

- 내연기관(ICE)

- 전기자동차(EV)

- 배터리 전기자동차(BEV)

- 하이브리드 전기자동차(HCEV)

- 수소연료전지 자동차(FCEV)

- 하이브리드

제10장 시장추정 및 예측 : 유통채널별, 2022-2035

- OEM

- 애프터마켓

제11장 시장추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 포르투갈

- 크로아티아

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

제12장 기업 프로파일

- 세계기업

- Aisin

- Aptiv

- Autoliv

- Bosch

- Continental

- Denso

- Harman

- Hella Forvia

- Magna International

- Mobileye

- Renesas Electronics

- Texas Instruments

- Valeo

- ZF Friedrichshafen

- 지역별 기업

- Ambarella

- Clarion

- Ficosa

- Gentex

- Siemens

- Emerging/Disruptor Players

- Black Sesame Technologies

- Horizon Robotics

- Innoviz Technologies

- Luminar Technologies

- Mobileye Vision Technologies(China)

- Spark Minda

- Uhnder

The Global Passenger Vehicle ADAS Market was valued at USD 32.2 billion in 2025 and is estimated to grow at a CAGR of 17.8% to reach USD 160.3 billion by 2035.

Growth is attributed to stricter government safety policies and evolving vehicle assessment standards that encourage automakers to integrate advanced driver assistance capabilities to meet compliance targets and enhance competitiveness. Buyers are increasingly prioritizing protection, driving ease, and reduced fatigue, which is supporting higher adoption of intelligent assistance technologies across passenger vehicles. Improvements in chip manufacturing efficiency, large-scale production, and intensified supplier competition have lowered system costs, allowing ADAS penetration to expand beyond premium models without significantly impacting vehicle pricing. Manufacturers are actively leveraging ADAS feature sets as a strategic tool to strengthen brand perception, support pricing strategies, and build long-term customer loyalty. Increased consumer familiarity with driver assistance technologies continues to reinforce demand, positioning ADAS as a core component of modern passenger vehicle design.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $32.2 Billion |

| Forecast Value | $160.3 Billion |

| CAGR | 17.8% |

The radar segment held 46% share in 2025. Radar systems are positioned as a foundational sensing technology within ADAS architectures due to their consistent performance and reliability. At the same time, image sensors are recognized for delivering detailed visual inputs that support accurate system interpretation. Advancements in sensor resolution and processing capability have improved overall system accuracy and robustness, reinforcing the role of multi-sensor integration in next-generation ADAS deployments.

The lane departure warning system segment held 17% share in 2025, with a valuation of approximately USD 5.5 billion. This segment benefits from the growing demand for driving assistance solutions that help reduce driver workload and improve comfort during extended vehicle operation. The system's ability to support stable vehicle positioning contributes to higher user confidence and sustained attention, factors that are driving its increasing acceptance among passenger vehicle owners.

U.S. Passenger Vehicle ADAS Market was valued at USD 10.7 billion in 2025. Adoption is supported by rising interest in advanced assistance capabilities, manufacturer-led feature differentiation, and broader availability of intelligent driving functions. Software-centric vehicle platforms and remote update capabilities are accelerating feature enhancements and enabling new revenue models across vehicle categories. Regulatory developments are also gradually supporting more advanced automation levels under controlled conditions through structured deployment frameworks.

Key companies active in the Global Passenger Vehicle ADAS Market include Bosch, Mobileye, Continental, Valeo, Aptiv, ZF, Magna International, Denso, Autoliv, Harman, Siemens, and Clarion. Companies operating in the Global Passenger Vehicle ADAS Market are reinforcing their market position through continuous innovation, strategic partnerships, and scalable product development. Leading players are investing heavily in sensor fusion, software intelligence, and system integration to deliver reliable and cost-effective solutions. Collaboration with automakers is helping suppliers align technologies with evolving vehicle platforms and regulatory expectations. Firms are also focusing on modular architectures that allow flexible deployment across different vehicle segments. Expansion of global production capacity and long-term supply agreements are being used to improve cost efficiency and market reach.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System

- 2.2.3 Sensor

- 2.2.4 Vehicle

- 2.2.5 Level

- 2.2.6 Propulsion

- 2.2.7 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook & strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Regulatory safety mandates

- 3.2.1.3 Consumer preference for safer vehicles

- 3.2.1.4 Technology cost reduction

- 3.2.1.5 OEM differentiation strategies

- 3.2.1.6 Growth of electric vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system integration complexity

- 3.2.2.2 Regulatory uncertainty for higher automation

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Level 2+ and Level 3 systems

- 3.2.3.2 Advancement in sensor fusion and AI

- 3.2.3.3 Aftermarket and retrofit potential

- 3.2.3.4 Data monetization and software services

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - Federal Motor Vehicle Safety Standards (FMVSS)

- 3.4.1.2 Canada - Motor Vehicle Safety Regulations

- 3.4.2 Europe

- 3.4.2.1 UK - Road Vehicles (Construction and Use) Regulations

- 3.4.2.2 Germany - Autonomous Driving Act

- 3.4.2.3 France - Mobility Orientation Law (LOM)

- 3.4.2.4 Italy - Highway Code (Codice della Strada)

- 3.4.2.5 Spain - General Traffic Regulation

- 3.4.3 Asia Pacific

- 3.4.3.1 China - Intelligent Connected Vehicle Regulations

- 3.4.3.2 Japan - Road Transport Vehicle Act

- 3.4.3.3 India - Central Motor Vehicle Rules

- 3.4.4 Latin America

- 3.4.4.1 Brazil - National Traffic Code

- 3.4.4.2 Mexico - Official Mexican Vehicle Safety Standards (NOM)

- 3.4.4.3 Argentina - National Traffic Law

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - Federal Traffic Law

- 3.4.5.2 South Africa - National Road Traffic Act

- 3.4.5.3 Saudi Arabia - Traffic Law

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Cost breakdown analysis

- 3.9.1 Development cost structure

- 3.9.2 R&D cost analysis

- 3.9.3 Marketing & sales costs

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 ADAS standards, validation & safety ratings impact

- 3.12.1 Euro NCAP, Global NCAP & IIHS rating impact on ADAS adoption

- 3.12.2 UNECE regulations (R79, R152, R157) and OEM compliance pathways

- 3.12.3 Homologation, validation & testing requirements by automation level

- 3.12.4 Impact of safety ratings on OEM feature packaging & pricing

- 3.13 ADAS software & compute architecture landscape

- 3.13.1 Centralized vs domain vs zonal ADAS architectures

- 3.13.2 SoC and ECU evolution (ADAS ECUs → centralized compute)

- 3.13.3 Middleware, operating systems & real-time constraints

- 3.13.4 OTA update readiness & software lifecycle implications

- 3.14 ADAS Cost vs Willingness-to-Pay

- 3.15 ADAS Data, Cybersecurity & Functional Safety (ISO 26262 / SOTIF)

- 3.16 OEM ADAS Roadmap & Feature Migration Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By System, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Adaptive cruise control

- 5.3 Blind spot detection

- 5.4 Lane departure warning system

- 5.5 Automatic emergency braking (AEB)

- 5.6 Forward collision warning

- 5.7 Night vision system

- 5.8 Driver monitoring

- 5.9 Tire pressure monitoring system

- 5.10 Head-up display

- 5.11 Park assist system

- 5.12 Others

Chapter 6 Market Estimates & Forecast, By Sensor, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Radar

- 6.3 Lidar

- 6.4 Ultrasonic

- 6.5 Camera

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Sedan

- 7.3 SUV

- 7.4 Hatchback

Chapter 8 Market Estimates & Forecast, By Level, 2022-2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Level-1

- 8.3 Level-2

- 8.4 Level-3

- 8.5 Level-4

- 8.6 Level-5

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 ICE

- 9.3 EV

- 9.3.1 BEV

- 9.3.2 HCEV

- 9.3.3 FCEV

- 9.4 Hybrid

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Portugal

- 11.3.9 Croatia

- 11.3.10 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Turkey

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Aisin

- 12.1.2 Aptiv

- 12.1.3 Autoliv

- 12.1.4 Bosch

- 12.1.5 Continental

- 12.1.6 Denso

- 12.1.7 Harman

- 12.1.8 Hella Forvia

- 12.1.9 Magna International

- 12.1.10 Mobileye

- 12.1.11 Renesas Electronics

- 12.1.12 Texas Instruments

- 12.1.13 Valeo

- 12.1.14 ZF Friedrichshafen

- 12.2 Regional Players

- 12.2.1 Ambarella

- 12.2.2 Clarion

- 12.2.3 Ficosa

- 12.2.4 Gentex

- 12.2.5 Siemens

- 12.3 Emerging / Disruptor Players

- 12.3.1 Black Sesame Technologies

- 12.3.2 Horizon Robotics

- 12.3.3 Innoviz Technologies

- 12.3.4 Luminar Technologies

- 12.3.5 Mobileye Vision Technologies (China)

- 12.3.6 Spark Minda

- 12.3.7 Uhnder