|

시장보고서

상품코드

1693685

반도체 본딩 장치 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Semiconductor Bonding Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

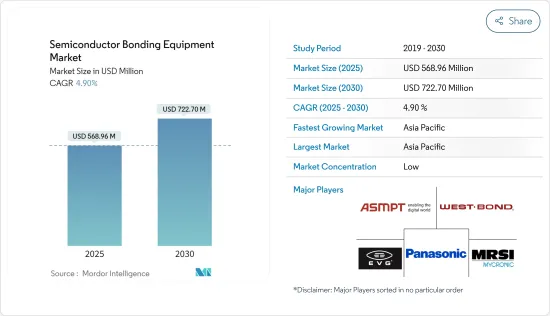

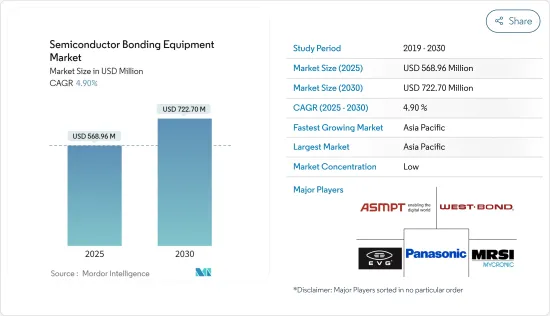

세계의 반도체 본딩 장치 시장 규모는 2025년 5억 6,896만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR 4.9%로 확대되어, 2030년에는 7억 2,270만 달러에 달할 것으로 예측되고 있습니다.

반도체 본딩 장치는 높은 효율, 처리 능력 및 더 작은 실적를 가진 반도체 칩에 대한 수요가 증가함에 따라 용도가 발견되어 예측 기간 동안 시장 수요를 견인하고 있습니다.

주요 하이라이트

- 디지털화의 영향이 확대됨에 따라 반도체 시장은 활황을 보이고 있습니다.

- 향후 10년간 칩 수요가 급증함에 따라 세계 반도체 산업은 2030년까지 1조 달러 산업이 될 것으로 예상되고 있습니다.

- 중요한 기술 부품을 제조하고 있는 반도체 산업은 수요의 급증으로 표제를 활기차고 있습니다. 이것은 반도체가 일렉트로닉스나 제조업, 농업, 의료, 인프라, 엔터테인먼트, 수송, 통신, 군사 시스템, 에너지 관리, 우주 등 다양한 산업에 있어서의 하이컴퓨팅·용도에 빠뜨릴 수 없기 때문입니다.

- 제품이 2개의 다이나 웨이퍼의 접합을 필요로 하는 경우, 몇개의 방법이 이용됩니다. 한 프로세스에 있어서 가장 중요한 3개의 요인은 본딩에 필요한 업스트림 프로세스의 비용, 본딩 프로세스의 사이클 타임, 본딩 프로세스의 수율입니다.

- 세계의 유행성 발생과 COVID-19의 확산을 억제하기 위한 제한 조치로 반도체 본딩장치 산업의 세계 공급망은 크게 혼란스러워 각 회사의 생산 능력에 영향을 주었습니다.

반도체 본딩 장치 시장 동향

파워 IC와 파워 이산 용도 부문이 큰 시장 점유율을 차지

- 파워 반도체 디바이스는 다양한 용도에서 효율적인 전력 관리, 변환 및 제어를 촉진합니다. 에너지 절약과 전력 소비에 대한 관심 증가는 파워 반도체 디바이스의 중요성을 증가시키고 있습니다. 이 시장을 지원하는 것은 손실의 감소, 제어성의 향상, 내구성의 향상, 표준 상태나 고장 상태에 있어서의 신뢰성이 높은 성능입니다. 파워 반도체 수요가 증가의 일도를 따르는 가운데, 파워 IC와 본딩 기술 시장 확대도 기대되고 있습니다.

- 이 부문의 성장을 견인하는 것은 산업의 급속한 디지털화와 연결 장치 증가입니다. 이 소자들은 효율적인 전력 관리와 고성능 파워 반도체 소자를 필요로 합니다. 이들 디바이스를 이용함으로써 최적의 전력 변환이 달성되고, 에너지 손실이 삭감되어, 전자 시스템의 전체적인 에너지 효율이 향상됩니다.

- 이 부문은 고에너지 및 전력 효율이 높은 장치에 대한 수요가 증가함에 따라 성장하고 있습니다. 이러한 수요는 무선 및 휴대용 전자 제품의 보급, 자동차 산업의 전기화로의 전환, 이러한 장치의 사용 증가에 의해 더욱 촉진되고 있습니다.

- 산업에서는 전력 모듈과 통합 솔루션에 대한 경사가 증가하고 있습니다. 파워 반도체 제조업체는 시스템 설계의 간소화, 부품 수 감소, 전체 시스템 효율 향상을 위해 스위치, 다이오드, 드라이버 등 다양한 파워 컴포넌트를 통합한 컴팩트하고 고도로 통합된 모듈을 개발하고 있습니다. 파워 반도체 회사는 경쟁을 유지하기 위해 제품 설계 프로세스의 초기 단계에서 장애 및 시장 동향을 이해함으로써 이익을 얻을 수 있습니다. 공급업체의 파워 반도체 생산 증가 투자 증가는 시장 확대에 영향을 미칠 것으로 예측됩니다.

- 파워 IC와 이산 부품의 대폭적인 개발로 전력 관리 효율성이 향상되고 있습니다. 높은 전력 전송 능력을 가능하게 하고 커넥티드 조명과 같은 혁신적인 디바이스 카테고리의 창출을 촉진했습니다.

- 스마트폰의 트랜스미션 속도가 대폭 상승하고 있어 처리 요건에 대응하기 위해 배터리 모듈이 필요하게 되고 있습니다.

- 예를 들어, Ericsson에 따르면 세계의 셀룰러 IoT 연결은 2022년에 19억에 달했으며 2027년에는 55억에 이를 것으로 추정되고 있습니다.

- 마찬가지로 기술적으로 강화된 연계 디바이스를 세계 소비자에게 제공하는 것을 목적으로 한 IoT 용도의 대폭적인 기술 진보도 시장 성장에 긍정적인 영향을 미칠 것으로 예측됩니다.

- Ericsson은 주로 단거리 IoT 디바이스 증가에 따라 2022-2028년까지 세계의 접속 디바이스 수가 약 2배 증가한다고 말하고 있습니다.

아시아태평양이 가장 급성장하는 시장이 될 전망

- 반도체 산업은 아시아의 경제 성장의 중요한 원동력으로서 대두해 왔습니다.

- 아시아태평양은 세계적으로 반도체 주조의 주요 점유율을 차지하며 Samsung Electronics, TSMC 등의 유명 기업이 진출하고 있습니다. 이 지역에서는 한국, 대만, 중국이 큰 점유율을 차지하고 있습니다.

- 2023년 9월, 중국은 반도체 산업을 뒷받침하기 위해 400억 달러의 기금을 출시했습니다. 3개의 펀드 중에서 가장 중요한 것으로 발전할 자세입니다.

- 확대하는 국내 칩 수요에 근거해 중국은 미국을 제치고 반도체 산업에 있어서 세계 제일의 대국이 될 것으로 추정되고 있습니다.

- 이 새로운 반도체 공장은 디스플레이 드라이버, 파워 매니지먼트 IC, 마이크로컨트롤러, 고성능 컴퓨팅 로직 등의 용도용 칩을 제조하고, 컴퓨팅과 데이터 스토리지, 자동차, 무선 통신, 인공지능 등 시장에서 높아지는 수요에 대응합니다.

반도체 본딩 장치 시장 개요

반도체 본딩장치 시장은 매우 세분화되어 EV Group, ASMPT Semiconductor Solutions, MRSI Systems(Myronic AB), WestBond Inc., Panasonic Holding Corporation 등의 대기업이 참가하고 있습니다.

- 2023년 11월 - EV Group(EVG)은 EVG 본사 확대의 다음 단계 건설공사 완료를 발표. 투자를 보여주는 것입니다. EVG는 급성장하는 첨단 포장 시장과 3D/이기종 인테그레이션 시장을 지원하기 위해 EVG의 하이브리드 본딩 솔루션 및 기타 프로세스 솔루션, 프로세스 개발 서비스에 대한 지속적인 높은 수요의 혜택을 받고 있습니다.

- 2023년 9월 - MRSI Systems(Mycronic AB)는 정평 MRSI-7001 플랫폼의 새로운 변형, MRSI 7001HF의 발매를 발표했습니다. 7001HF는 접합시 최대 500N의 힘을 가할 수 있는 가열식 본드 헤드를 특징으로 합니다. 이것에 의해 7001HF는 IC 포장용 파워 반도체 소결이나 IC 포장용 열압착 본더 등의 용도용의 고하중 다이 본더에 최적인 툴이 됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 시장의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 산업 밸류체인/공급 체인 분석

- 시장에 대한 COVID-19의 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 반도체 제조업체에 의한 제조 능력 확대를 위한 투자 증가

- 다양한 용도에서 반도체 칩 수요 증가

- 시장 성장 억제요인

- 높은 소유 비용

- 회로의 소형화에 의한 복잡화

제6장 시장 세분화

- 유형별

- 영구 본딩 장치

- 임시 본딩 장치

- 하이브리드 본딩 장치

- 용도별

- 첨단 포장

- 파워 IC 및 파워 이산

- 포토닉 디바이스

- MEMS 센서와 액추에이터

- 엔지니어 기판

- RF 디바이스

- CMOS 이미지 센서(CIS)

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- EV Group

- ASMPT Semiconductor Solutions

- MRSI Systems.(Myronic AB)

- WestBond Inc.

- Panasonic Holding Corporation

- Palomar Technologies

- Dr. Tresky AG

- BE Semiconductor Industries NV

- Fasford Technology Co.Ltd(Fuji Group)

- Kulicke and Soffa Industries Inc.

- DIAS Automation(HK) Ltd

- Shibaura Mechatronics Corporation

- SUSS MicroTec SE

- Tokyo Electron Limited

제8장 투자 분석

제9장 시장의 미래

JHS 25.05.13The Semiconductor Bonding Equipment Market size is estimated at USD 568.96 million in 2025, and is expected to reach USD 722.70 million by 2030, at a CAGR of 4.9% during the forecast period (2025-2030).

Semiconductor bonding equipment finds application owing to the rising demand for semiconductor chips with higher efficiency, processing power, and smaller footprint, thereby driving the demand for the market during the forecast period.

Key Highlights

- As the impact of digitalization has increased, semiconductor markets have boomed. Notably, this has further resulted in government programs to support the 5G deployment. For instance, the European Commission recognized the importance of the 5G network early and established a public-private partnership to develop and research 5G technology.

- With chip demand set to surge over the coming decade, the global semiconductor industry is expected to become a trillion-dollar industry by 2030. This growth is favored by companies and countries funneling vast sums of money into semiconductor manufacturing, materials, and research to guarantee a constant supply of chips and know-how to support growth across a broad swath of increasingly data-centric industries.

- The semiconductor industry, which makes crucial technological components, has been hitting the headlines due to a rampant demand increase. A recent Wall Street Journal report shows that semiconductors rank as the world's fourth-largest traded product (imports and exports, counted), after crude oil, refined oil, and cars. This is because semiconductors are critical for high-computing applications in various industries, including electronics and manufacturing industries, agriculture, healthcare, infrastructure, entertainment, transportation, telecommunications, military systems, energy management, and space, to name just a few.

- Several methods might be used when a product needs the bonding of two dies or wafers. Not only does the type of bonding method itself have to be selected, but it must also be decided whether the items being bonded will be in wafer or die form. The selected bonding process is the primary driver for the cost of ownership of bonding. For a given process, the three most important factors are the cost of the upstream process needed for bonding, the cycle time of the bonding process, and the yield of the bonding process.

- With the global outbreak of the pandemic and restrictive measures taken to control the spread of COVID-19, the global supply chain of the semiconductor bonding equipment industry was significantly disrupted, impacting the production capabilities of various companies. Although the number of COVID-19-infected patients decreased considerably, salient issues with materials supply and demand for these components still need to be addressed, challenging the market's growth.

Semiconductor Bonding Equipment Market Trends

Power IC and Power Discrete Application Segment Holds Significant Market Share

- Power semiconductor devices facilitate efficient power management, conversion, and control across various applications. The increasing focus on energy conservation and power consumption is increasing the significance of power semiconductor devices. The market is supported by reduced losses, enhanced controllability, greater durability, and reliable performance in standard and fault conditions. As the demand for power semiconductors continues to rise, there is also an expected increase in the market for power ICs and bonding technology.

- The segment's growth is driven by the rapid digitization of industries and the increasing number of connected devices. These devices necessitate efficient power management and high-performance power semiconductor devices. By utilizing these devices, optimal power conversion is achieved, energy losses are reduced, and the overall energy efficiency of electronic systems is enhanced.

- The segment is experiencing growth due to the rising demand for high-energy and power-efficient devices. This demand is further fueled by the prevalence of wireless and portable electronic products, the automotive industry's shift toward electrification, and the increased use of these devices.

- The industry has a rising inclination toward power modules and integrated solutions. Manufacturers of power semiconductors are creating compact, highly integrated modules that merge various power components like switches, diodes, and drivers to streamline system design, lower component quantity, and improve overall system efficiency. Power semiconductor firms stand to gain by understanding the obstacles and market trends early in the product design process to remain competitive. The increasing investments by vendors to boost power semiconductor production are anticipated to affect the market's expansion.

- A significant development in power IC and discrete components enhances power management efficiency. Recent advancements in system architectures have led to more efficient AC-DC power adapters with reduced size and component numbers. Introducing new Power-over-Ethernet (PoE) standards has enabled higher power transfer capabilities, facilitating the creation of innovative device categories like connected lighting. The growing emphasis on minimizing electricity consumption by electronics manufacturers and the increasing demand from consumer electronics are the primary drivers behind the necessity for Power ICs. These factors could potentially boost the demand for bonding equipment.

- There is a significant rise in smartphone transmission speeds, necessitating battery modules to accommodate the processing requirements. Power adapters are now incorporating discrete semiconductors, leading to an anticipated surge in demand driven by the increasing sales of battery-powered devices. The growth of IoT applications is projected to propel the demand for discrete semiconductors further.

- For example, according to Ericsson, global cellular IoT connections reached 1.9 billion in 2022 and are estimated to reach 5.5 billion by 2027. The increasing penetration of smartphones with the evolution of 5G is expected to drive the market's growth.

- Similarly, the market's growth is expected to be positively influenced by the significant technological advancements in IoT applications, which aim to provide technologically enhanced linked devices to consumers worldwide. The expansion of IoT applications has increased the prevalence of smart devices and small semiconductors, consequently driving the demand for advanced semiconductor bonding equipment.

- Ericsson stated that the number of connected devices globally will nearly double from 2022 to 2028, primarily due to the rise in short-range IoT devices. It is expected that there will be approximately 28.72 billion such devices by 2028. With the growing demand for these IoT-connected devices, the demand for power ICs is expected to rise, thereby enhancing the growth of the bonding equipment market.

Asia-Pacific is Expected to be the Fastest Growing Market

- The semiconductor industry has emerged as a critical driver of economic growth in Asia. Its rapid expansion and technological advancements have become an important component of the global supply chain.

- Asia-Pacific holds a major share of semiconductor foundries globally, with the region having the presence of prominent companies like Samsung Electronics, TSMC, etc. South Korea, Taiwan, Japan, and China have significant market shares in the region. Taiwan holds a prominent share of the foundries in the world and is a vital region in the semiconductor value chain. The increasing investments in the expansion of semiconductor manufacturing capacities in the region are expected to aid the market's growth significantly.

- In September 2023, China launched a USD 40 billion fund to boost the semiconductor industry. China plans to establish a state-backed investment fund to narrow the gap with global rivals, especially the United States. This initiative is poised to evolve as the most significant of the trio of funds managed by the China Integrated Circuit Industry Investment Fund, generally known as the Big Fund. President Xi Jinping of China stressed the critical importance of achieving semiconductor self-sufficiency, primarily in response to export control measures imposed by the United States. The latest fund obtained approval from Chinese authorities, with the finance ministry committing CNY 60 billion (USD 8.30 billion).

- Based on its expanding domestic chip demand, China is estimated to overtake the United States as the world's top powerhouse in the semiconductor industry. By 2030, the semiconductor market is expected to double in size to reach more than USD 1 trillion, with China contributing over 60% of that increase, according to the Semiconductor Industry Association. Such exponential growth is anticipated to increase demand for semiconductor bonding equipment.

- The new semiconductor fab would fabricate chips for applications like display drivers, power management IC, microcontrollers, and high-performance computing logic, addressing the growing demand in markets like computing and data storage, automotive, wireless communication, and artificial intelligence. This fab claims to have a manufacturing capacity of up to 50,000 wafers per month, and the first chip will come out of the facility before the end of 2026.

Semiconductor Bonding Equipment Market Overview

The semiconductor bonding equipment market is highly fragmented, with major players like EV Group, ASMPT Semiconductor Solutions, MRSI Systems (Myronic AB), WestBond Inc., and Panasonic Holding Corporation. Market players participate in partnerships and acquisitions to gain sustainable competitive advantage and enhance their product offerings.

- November 2023 - The EV Group (EVG) announced the completion of construction works for the next phase of the expansion of EVG corporate headquarters. The "Manufacturing V" facility serves as EVG's manufacturing department for equipment components and offers a significant expansion of production floor and warehouse space. The opening of the Manufacturing V facility marks the latest expansion phase and investment of EVG, which continues to benefit from the continuing high demand for EVG's hybrid bonding solutions and other process solutions, as well as process development services, to support the fast-growing advanced packaging market and 3D / heterogeneous integration market.

- September 2023 - MRSI Systems (Mycronic AB) announced the launch of the new variant of the well-established MRSI-7001 platform, the MRSI 7001HF. The 7001HF features a heated bond head capable of applying up to 500N forces during bonding. The heated bond head also provides heating from the top at a temperature of 400°C. This makes the 7001HF the perfect tool for high-force die bonders for applications such as power semiconductor sintering for IC packaging or thermocompression bonders for IC packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5 Market Dynamics

- 5.1 Market Driver

- 5.1.1 Increasing Investment by Semiconductor Manufacturers to Expand their Manufacturing Capacity

- 5.1.2 Rising Demand for Semiconductor Chips across Various Application

- 5.2 Market Restraints

- 5.2.1 High Cost of Ownership

- 5.2.2 Increased Complexity Owing to Miniaturization of Circuits

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Permanent Bonding Equipment

- 6.1.2 Temporary Bonding Equipment

- 6.1.3 Hybrid Bonding Equipment

- 6.2 By Application

- 6.2.1 Advanced Packaging

- 6.2.2 Power IC and Power Discrete

- 6.2.3 Photonic Devices

- 6.2.4 MEMS Sensors and Actuators

- 6.2.5 Engineered Substrates

- 6.2.6 RF Devices

- 6.2.7 CMOS Image Sensors (CIS)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 EV Group

- 7.1.2 ASMPT Semiconductor Solutions

- 7.1.3 MRSI Systems. (Myronic AB)

- 7.1.4 WestBond Inc.

- 7.1.5 Panasonic Holding Corporation

- 7.1.6 Palomar Technologies

- 7.1.7 Dr. Tresky AG

- 7.1.8 BE Semiconductor Industries NV

- 7.1.9 Fasford Technology Co.Ltd (Fuji Group)

- 7.1.10 Kulicke and Soffa Industries Inc.

- 7.1.11 DIAS Automation (HK) Ltd

- 7.1.12 Shibaura Mechatronics Corporation

- 7.1.13 SUSS MicroTec SE

- 7.1.14 Tokyo Electron Limited