|

시장보고서

상품코드

1836472

영국의 일반 외과용 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)United Kingdom General Surgical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

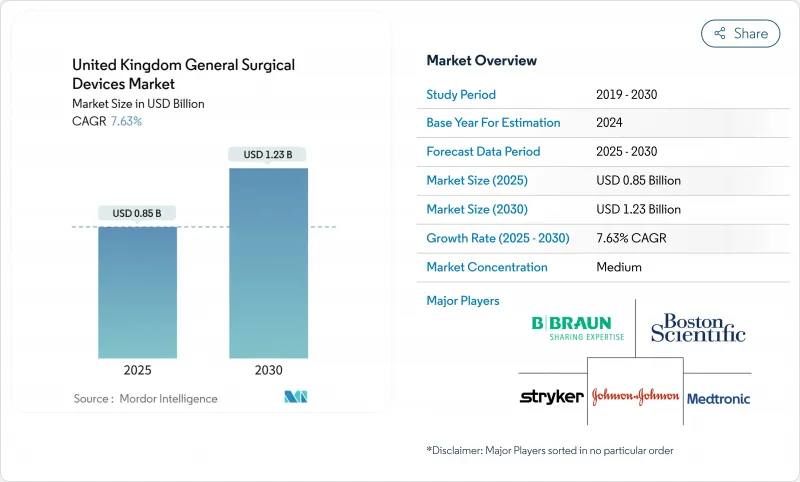

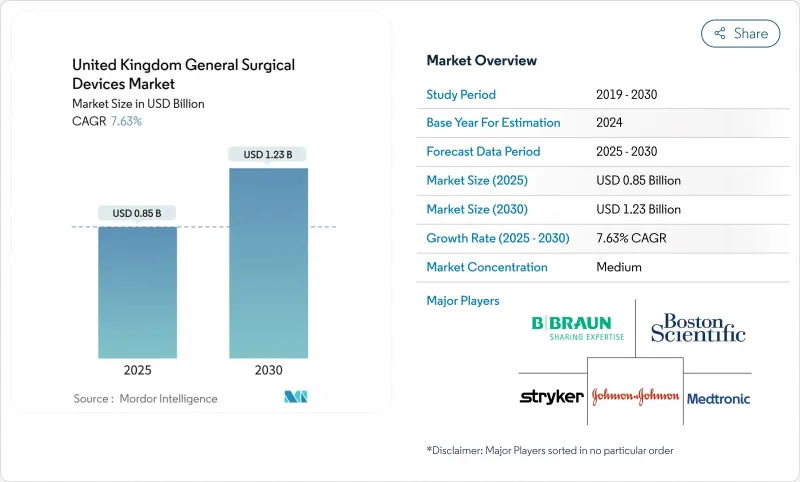

영국의 일반 외과용 기기 시장 규모는 2025년에 8억 5,000만 달러에 달하고, 예측 기간(2025-2030년)의 CAGR은 7.63%를 나타내, 2030년에는 12억 3,000만 달러에 달할 것으로 전망됩니다.

성장의 축이 되는 것은 저침습 수술과 당일치기 수술에 대한 국민보건서비스(NHS)의 축족, 국립의료기술평가기구(NICE)에 의한 11개의 로봇 시스템의 급속한 승인, 자본 예산의 역풍에도 불구하고 데이터 풍부한 수술 분석에 대한 지속적인 수요입니다. 특히 고령화 사회에서 외상 및 만성 질환 증가로 인해 정형외과 및 심혈관 수술이 가속화되는 반면, 탄소 발자국과 연동된 조달 기준은 재사용 가능한 기구 및 폐기물이 적은 기구공급업체를 유리하게 만듭니다. UKCA 마킹으로의 규제 이행은 단기적인 불확실성을 초래하지만, 단계적 구현은 당분간공급 충격을 완화시켜 강력한 컴플라이언스 기반을 가진 기존 기업이 유리하게 만듭니다.

영국의 일반 외과용 기기 시장 동향과 인사이트

낮은 침습 장비에 대한 수요 증가

로봇 및 복강경 플랫폼은 포츠머스의 퀸 알렉산드라 병원이 모든 키홀 당일치기 수술을 다빈치 시스템으로 변경하고 대상 환자의 입원 기간을 단축하는 등 계속 개복술을 대체하고 있습니다. Versius Surgical Registry는 2,083건의 수술로 불과 5.4%의 전환만을 기록했으며, 신뢰성과 외과 의사의 수용 태세를 뒷받침하고 있습니다. 사우샘프턴 소아 병원이 영국 최초의 소아 로봇 신장 수술을 실시한 후, 소아에의 도입이 확대되고 있습니다. Versius Clinical Insights 등의 분석 모듈을 통합하여 신규 사용자의 학습 곡선을 단축하는 실시간 벤치마크를 제공합니다.

외상과 만성 질환 증가

선택적 치료 회복 계획에서는 정형외과 로봇이 주목받고 있으며, Barking, Havering and Redbridge(BHR) 병원은 2024년 중반까지 Mako 로봇에 의한 100건의 로봇 관절 치환술을 기록해 정밀도 향상과 신속한 동원을 꼽았습니다. PICO 단일 청소년과 같은 음압상처치료 시스템은 복잡한 상처에 적용되어 감염의 발생률과 입원 기간을 감소시킵니다. 신경근 자극기 geko는 정맥성 허벅지 궤양의 치유 확률을 68% 개선하고 장기적인 상처 관리 비용을 15% 상쇄합니다. 이러한 움직임을 종합하면 수술 건수가 증가하고 병원 전체의 기기 수요가 다양화됩니다.

엄격한 MDR/UKCA 규제 일정

Brexit에 의한 괴리로 인해 2028년 이후 새로운 의료기기는 UKCA 마킹을 의무화합니다. 제조업체는 2025년 6월까지 새 스키마를 준수하는 인시던트 보고서 데이터 피드를 만들어 규정 준수 비용이 상승했습니다. 해외 기업은 영국의 책임자를 임명해야 하며 물류층이 두꺼워지고 출시 일정이 지연됩니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 당일치기 수술에 의한 입원 기간 단축을 위한 NHS 장기 계획

- 원내 감염 리스크 경감을 위한 일회용 기구로의 변화

- NHS 트러스트에서 자본 예산의 역풍

부문 분석

핸드헬드 디바이스는 영국의 일반 외과용 기기 시장에서 2024년 매출의 33.16%를 창출했습니다. 이 부문의 영국의 일반 외과용 기기 시장 규모는 2024년에 2억 8,000만 달러에 달했고 2030년까지 연평균 복합 성장률(CAGR) 6.3%를 나타낼 것으로 예측됩니다. 병원에서는 자본 집약적인 로봇에 비해 휴대성과 진료과 횡단적인 유용성이 지지되어 사용률이 극대화되고 있습니다. 상처 폐쇄 기구는 생체 흡수성 전기 자극 봉합사에 견인되어 CAGR 8.81%를 나타내 가장 빠르게 성장할 전망입니다.

지속적인 혁신으로 전기 수술용 연필, 복강경용 파지기 및 접근용 트래커 수요가 유지됩니다. NHS Supply Chain이 추진하는 표준화된 기술 팩은 설치 시간과 물류 복잡성을 줄이는 번들 장비 키트의 조달을 강화합니다. 국내 제조업체는 품질이 보장된 유럽제 강재와 부가가치가 높은 서비스로 수입 경쟁에 대응하고 있습니다.

낮은 침습 수술은 2024년 영국 일반 외과용 기기 시장 점유율의 73.43%를 차지했습니다. 환자의 외상을 줄이고, 회복을 가속화하고, 자원 이용을 최적화하는 수술에 대한 NHS의 전략적 헌신을 반영하여 CAGR 8.52%를 나타낼 것으로 예측됩니다. 저침습 승모판 수술은 초보자 센터에서 실시되어 재원 일수를 7일에서 5일로 크게 단축하는 한편, 종래의 접근과 동등한 치료 성적을 나타냈습니다.

개복 수술은 직접적인 시각화와 촉각 피드백이 필요한 복잡한 사례에 대한 관련성을 유지하며 외상, 긴급 수술 및 특수 수술에서 안정적인 수요로 나머지 시장 점유율을 차지합니다. 낮은 침습 접근법으로의 수술 변화는 수술 팀에 대한 훈련 요건을 창출하고 있으며, AI 주도 교육 시스템은 복강경 수술의 기술 습득과 유지 향상을 보여줍니다.

영국의 일반 외과용 기기 시장 보고서는 제품별(핸드헬드 디바이스, 복강경 디바이스, 전기 수술용 디바이스, 상처 봉합 기기, 기타), 수술 어프로치별(개복 수술, 저침습 수술), 용도별(부인과·비뇨기과, 순환기과, 기타), 최종 사용자별(병원, 외래수술센터(ASC), 기타)로 분류하고 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 낮은 침습 장치에 대한 수요 증가

- 외상과 만성 질환 증가

- 당일치기 수술에 의한 입원 기간 단축을 목표로 하는 NHS의 장기 계획

- 원내 감염 리스크를 경감하기 위한 일회용 기구로의 이행

- 기기 레벨의 데이터 분석을 가능하게 하는 수술실의 디지털화

- NHS공급 체인에 있어서의 탄소발자국와 연동한 조달 스코어링

- 시장 성장 억제요인

- 엄격한 MDR/UKCA 규제 스케줄

- NHS 트러스트에 있어서의 자본 예산의 역풍

- 공급망의 취약성

- 고도의 로봇 공학에 대한 외과의의 스킬 갭

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측(금액)

- 제품별

- 휴대용 기기

- 복강경 기기

- 전기 수술 장비

- 상처 봉합 기기

- 트로카 및 접근 기기

- 기타 제품

- 수술 접근법별

- 개복 수술

- 저침습 수술

- 용도별

- 부인과 및 비뇨기과

- 심장학

- 정형외과

- 신경학

- 기타 용도

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 기타 최종 사용자

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- B. Braun SE

- Medtronic plc

- Olympus Corporation

- Integra LifeSciences

- Stryker Corporation

- Johnson & Johnson(Ethicon)

- Erbe Elektromedizin GmbH

- Boston Scientific Corporation

- Smith & Nephew plc

- Getinge AB

- ConvaTec Group plc

- Zimmer Biomet Holdings Inc.

- Becton Dickinson & Co.

- Cook Medical

- CMR Surgical Ltd.

- Purple Surgical

- Teleflex Incorporated

- Surgical Holdings Ltd.

- Swann-Morton Ltd.

제7장 시장 기회와 전망

KTH 25.10.27The United Kingdom General Surgical Devices Market size is estimated at USD 0.85 billion in 2025, and is expected to reach USD 1.23 billion by 2030, at a CAGR of 7.63% during the forecast period (2025-2030).

Growth is anchored in the National Health Service (NHS) pivot toward minimally invasive and day-case surgery, the rapid approval of 11 robotic systems by the National Institute for Health and Care Excellence (NICE), and sustained demand for data-rich surgical analytics despite capital budget headwinds. A rising trauma and chronic-disease burden, especially among an aging population, accelerates orthopedic and cardiovascular procedures, while carbon-footprint-linked procurement criteria advantage suppliers of reusable or low-waste instruments. Regulatory transitions to UKCA marking create short-term uncertainty, but phased implementation mitigates immediate supply shocks and favors incumbents with strong compliance infrastructure.

United Kingdom General Surgical Devices Market Trends and Insights

Rising demand for minimally invasive devices

Robotic and laparoscopic platforms continue to displace open techniques, with Portsmouth's Queen Alexandra Hospital converting all keyhole day-case procedures to Da Vinci systems and cutting length of stay for eligible patients. The Versius Surgical Registry recorded only 5.4% conversions in 2,083 procedures, underscoring reliability and surgeon acceptance. Paediatric adoption is growing after Southampton Children's Hospital performed the UK's first robotic kidney surgery in children. Integration of analytics modules, such as Versius Clinical Insights, supplies real-time benchmarks that shorten learning curves for new users.

Increasing prevalence of trauma & chronic diseases

Elective-care recovery plans highlight orthopedic robotics: Barking, Havering and Redbridge (BHR) Hospitals logged 100 robotic joint replacements by mid-2024 with the Mako robot, citing accuracy gains and faster mobilisation. Negative-pressure wound therapy systems like PICO Single Use are scaling for complex wounds, lowering infection incidence and length of stay. The geko neuromuscular stimulator improved venous-leg-ulcer healing probability by 68%, offering 15% cost offsets on long-term wound care. Collectively, these dynamics lift procedure volumes and diversify device demand across hospitals.

Stringent MDR/UKCA regulatory timelines

Brexit-driven divergence requires UKCA marking for new devices from 2028, while transitional relief permits CE-marked products until then. Manufacturers must create incident-report data feeds conforming to new schemas by June 2025, elevating compliance costs. Overseas firms must appoint UK Responsible Persons, adding logistical layers and delaying launch timelines.

Other drivers and restraints analyzed in the detailed report include:

- NHS long-term plan to cut inpatient stay via day-case surgery

- Shift to single-use instruments to mitigate hospital-acquired-infection risk

- Capital-budget headwinds in NHS trusts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Handheld Devices generated 33.16% of 2024 revenue within the UK general surgical devices market. The UK general surgical devices market size for this segment equated to USD 0.28 billion in 2024 and is projected to advance at 6.3% CAGR through 2030. Hospitals favour their portability and cross-specialty utility, which maximises usage rates versus capital-intensive robots. Wound Closure Devices, led by bioabsorbable electro-stimulation sutures, will climb fastest at 8.81% CAGR, backed by evidence of accelerated healing and lower infection risk.

Continuous innovation sustains demand for electrosurgical pencils, laparoscopic graspers and access trocars. Standardised procedure packs promoted by NHS Supply Chain strengthen procurement of bundled device kits that reduce set-up time and logistics complexity. Domestic producers are responding to import competition with quality-assured European steel and value-added servicing.

Minimally Invasive Surgery accounted for 73.43% of the UK general surgical devices market share in 2024; it is forecast to rise at an 8.52% CAGR, reflecting the NHS's strategic commitment to procedures that reduce patient trauma, accelerate recovery, and optimize resource utilization. Implementation of minimally invasive mitral valve surgery in novice centers demonstrated comparable outcomes to conventional approaches while achieving significant reductions in hospital stays from 7 to 5 days.

Open Surgery maintains relevance for complex cases requiring direct visualization and tactile feedback, representing the remaining market share with steady demand in trauma, emergency, and specialized procedures. The procedural shift toward minimally invasive approaches is creating training requirements for surgical teams, with AI-driven education systems demonstrating improved skill acquisition and retention in laparoscopic techniques.

The United Kingdom General Surgical Devices Market Report is Segmented by Product (Handheld Devices, Laparoscopic Devices, Electrosurgical Devices, Wound Closure Devices, and More), Procedure Approach (Open Surgery, and Minimally Invasive Surgery), Application (Gynecology and Urology, Cardiology, and More) and End User (Hospitals, Ambulatory Surgical Centres and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- B. Braun

- Medtronic

- Olympus

- Integra LifeSciences

- Stryker

- Johnson & Johnson

- Erbe Elektromedizin

- Boston Scientific

- Smiths Group

- Getinge

- ConvaTec Group plc

- Zimmer Biomet

- Becton Dickinson & Co.

- Cook Group

- CMR Surgical Ltd.

- Purple Surgical

- Teleflex

- Surgical Holdings Ltd.

- Swann-Morton Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for minimally-invasive devices

- 4.2.2 Increasing prevalence of trauma & chronic diseases

- 4.2.3 NHS long-term plan to cut inpatient stay via day-case surgery

- 4.2.4 Shift to single-use instruments to mitigate hospital-acquired-infection risk

- 4.2.5 OR digitalisation enabling device-level data analytics

- 4.2.6 Carbon-footprint-linked procurement scoring in NHS supply chain

- 4.3 Market Restraints

- 4.3.1 Stringent MDR/UKCA regulatory timelines

- 4.3.2 Capital-budget headwinds in NHS trusts

- 4.3.3 Supply chain vulnerabilities

- 4.3.4 Surgeons' skills gap for advanced robotics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Handheld Devices

- 5.1.2 Laparoscopic Devices

- 5.1.3 Electrosurgical Devices

- 5.1.4 Wound Closure Devices

- 5.1.5 Trocars and Access Devices

- 5.1.6 Other Products

- 5.2 By Procedure Approach

- 5.2.1 Open Surgery

- 5.2.2 Minimally Invasive Surgery

- 5.3 By Application

- 5.3.1 Gynecology and Urology

- 5.3.2 Cardiology

- 5.3.3 Orthopedic

- 5.3.4 Neurology

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centres

- 5.4.3 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 B. Braun SE

- 6.3.2 Medtronic plc

- 6.3.3 Olympus Corporation

- 6.3.4 Integra LifeSciences

- 6.3.5 Stryker Corporation

- 6.3.6 Johnson & Johnson (Ethicon)

- 6.3.7 Erbe Elektromedizin GmbH

- 6.3.8 Boston Scientific Corporation

- 6.3.9 Smith & Nephew plc

- 6.3.10 Getinge AB

- 6.3.11 ConvaTec Group plc

- 6.3.12 Zimmer Biomet Holdings Inc.

- 6.3.13 Becton Dickinson & Co.

- 6.3.14 Cook Medical

- 6.3.15 CMR Surgical Ltd.

- 6.3.16 Purple Surgical

- 6.3.17 Teleflex Incorporated

- 6.3.18 Surgical Holdings Ltd.

- 6.3.19 Swann-Morton Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment