|

시장보고서

상품코드

1836580

이탈리아의 당뇨병 기기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Italy Diabetes Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

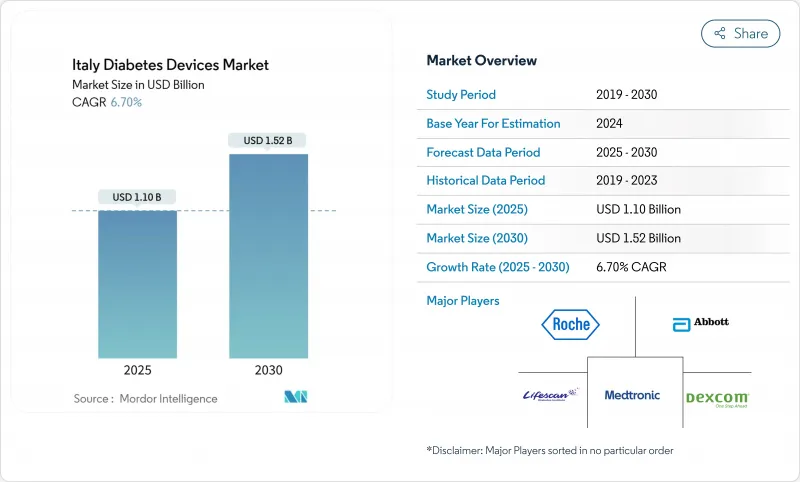

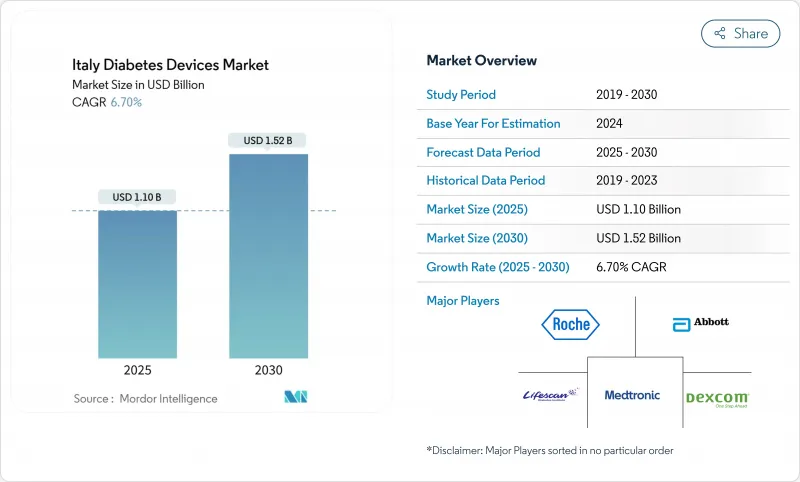

이탈리아 당뇨병 기기 시장은 2025년에 11억 달러로, 2030년에는 15억 2,000만 달러에 이르고, CAGR 6.7%를 나타낼 전망입니다.

이러한 꾸준한 증가는 고령화 인구, 전체의 92.14%를 차지하는 제2형 당뇨병 환자 비율, 그리고 국민건강보험제도(NHS) 하에서 우선순위 대상자에게 연속혈당측정기(CGM) 비용을 보상하는 정책 환경을 반영한 것입니다. 약국이 임상 기지가 되어 원격 의료 도구가 72%의 시설에 보급되고, 하이브리드형 폐쇄 루프 펌프가 보험 상환 포뮬러에 합류함에 따라 도입이 더욱 가속화되고 있습니다. 관리 제품은 주 1회 인슐린과 튜브리스 자동 전달의 전개에 의해 CAGR 7.14%를 누리고, 모니터링용 기기는 2024년에 58.12%의 점유율로 규모의 리더를 유지합니다. 남북 간의 자금 격차와 유럽의 엄격한 정밀도 규칙이 기세를 약화시키고 있지만, 16억 유로의 디지털 지출 목표로 이탈리아는 첨단 당뇨병 기술에 있어서 유럽에서 가장 매력적인 파일럿 시장의 지위를 유지하고 있습니다.

이탈리아 당뇨병 기기 시장 동향과 통찰

T1 및 소아 환자용 CGM 센서 보험 상환

의회법 130/2023은 1-17세의 국민을 대상으로 한 스크리닝을 의무화하고 있어, 새롭게 진단된 소아는 신속하게 CGM의 도입에 향합니다. 보건부는 이미 1형 및 인슐린 부하가 높은 2형 사용자를 위한 FreeStyle Libre에 자금을 제공하고 있어 중요한 비용면의 장애물을 제거하고 있습니다. 롬바르디아주, 에밀리아 로마냐주, 토스카나주에서 실시한 다시설 공동시험에서는 간헐적으로 스캔한 CGM을 사용한 경우 HbA1c는 3개월에 0.4%, 6개월에 0.6% 저하했다고 보고되었습니다. 어린 시절의 조기 CGM 습관화는 평생 순응도를 높이고 장기적인 센서 수익을 확대할 것으로 예상됩니다. 칼라브리아와 사르데냐에서는 도입 지연이 보이지만, 국가 상환 규칙은 공급자에게 명확한 수요 신호를 제공합니다.

PNRR 이후 확대되는 원격 의료 도입과 재택 케어 추진

재건 계획에 따른 16억 유로는 전자 의료 기록을 현대화하여 72% 병원이 포도당 데이터를 임상 포털에 직접 입력하는 원격 진료를 가능하게 했습니다. 600명의 임상의를 대상으로 한 연구는 82%가 일상적인 혈당 검토를 위한 원격 후속을 지지하고, 80%가 COVID 이후 시대에 감염 제어를 향상시켰습니다. 커넥티드 케어 플랫폼과 레질리아 앱은 센서 피드의 안전한 공유를 가능하게 하지만, 66%의 임상의는 디지털 케어가 중요한 대면 적정 방문을 대체할 수 없다고 경고합니다. 내륙부의 바질리카타 주에서는 광대역이 보급되지 않기 때문에 실시간 업로드가 느려지고 있지만, 약국의 Wi-Fi 스테이션이 그 갭을 메우게 되어 왔습니다. 전반적으로 원격 모니터링은 노인 환자의 이동 시간을 절약하고 폐쇄 루프 투여 알고리즘을 지원하는 지속적인 데이터 흐름을 촉진합니다.

남북 간 지역 자금 격차

칼라브리아와 사르데냐를 포함한 7개 지역은 2021년 최소 진료 기준에 실패하여, CGM 할당이 배급제가 되어 대기 시간이 길어졌습니다. 2024년 6월의 새로운 자치법을 통해 부유한 지역은 보다 충실한 혜택을 자금으로 충당할 수 있어 접근 격차가 확대될 수 있습니다. 약제비의 자기 부담은 국민의료비의 23%에 상당하지만, 남부에 많은 저소득 가구의 부담이 더 큽니다. 임상의의 북쪽 이주는 수용 능력 부족을 악화시킵니다. 따라서 의료기기 공급업체는 자금 부족 지역에서의 판매량 감소를 피하기 위해 가격 및 자기 부담 지원 프로그램을 조정해야 합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 약국 경영의 당뇨병 클리닉의 확대

- 2형 당뇨병의 유병률의 상승과 발병의 조기화

- 신규 진입을 지연시키는 eCGM의 엄격한 정밀 규제

부문 분석

모니터링 카테고리는 2024년 이탈리아 당뇨병 기기 시장 점유율의 58.12%를 차지했으며, 이 나라의 정착된 자기검사 문화와 집중 인슐린 유저에 대한 FreeStyle Libre의 완전 상환에 뒷받침되었습니다. 모니터링 솔루션의 이탈리아 당뇨병 기기 시장 규모는 2025년 6억 4,000만 달러로 센서 업그레이드와 소아과 영역 확대로 CAGR 5.9%로 상승할 전망입니다. 많은 노인들이 지문에 의한 확인을 신뢰하기 때문에 혈당 스트립은 계속 팔리고 있지만, 리브레 2 사용자는 롬바르디아 주 2,000명의 환자 코호트에서 6개월 후 HbA1c가 0.6% 감소한 것으로 나타났습니다. 병원에서는 입원 환자 적정에 업무용 CGM을 도입하는 경우가 늘어나고 일회용 센서의 대응 가능한 수량이 확대되고 있습니다.

2025년 4억 6,000만 달러로 평가되는 관리 기기는 자동화된 딜리버리 플랫폼이 보급됨에 따라 2030년까지 연평균 복합 성장률(CAGR)이 7.14%로 모니터링을 웃돌았습니다. 2025년 1월에 출시된 인슬릿사의 옴니포드 5는 듀얼 센서에 대응한 최초의 튜브리스 시스템을 도입해, 공적 상환의 대상이 되는 이탈리아의 1형 유저 30만명의 선택지를 넓혔습니다. 2025년 6월에 출시된 주당 1회 투여의 인슐린 제형 Icodec은 주사 사건을 86% 줄이고 주사 바늘과 주사기 교체 주기를 유발하며 복용량의 정확성을 확인하기 위한 펌프 시험을 권장합니다. 이탈리아의 비교 시험에서 미니메드 780G가 71%의 Time-in-Range를 달성하고, Tandem Control-IQ의 68%를 상회한 것이 밝혀져 내분비 전문의의 처방 행동에 영향을 줍니다. 펜니들 제조업체는 SIMDO 지침에 따라 지방 과다증의 위험을 최소화하기 위해 4mm 32G 형식을 권장합니다. 이러한 경영혁신은 이탈리아의 당뇨병 기기 시장에서 보다 높은 성장의 길을 굳히고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- T1 및 소아 환자용 CGM 센서의 보험 상환

- PNRR 후 원격 의료 도입과 재택 케어 확대

- 약국 경영의 당뇨병 클리닉(Farmacie dei Servizi)의 확대

- 청소년 비만 유병률 증가, 당뇨병 조기 발병 증가

- 하이브리드 폐쇄 루프 펌프에서 AI 기반 의사결정 지원

- 제2형 당뇨병의 유병률의 상승과 조기 발병

- 시장 성장 억제요인

- 남북 간 지역 자금 격차

- 신규 진입을 지연시키는 엄격한 eCGM 정도 규제

- 일회용 플라스틱 규제에 의한 공급 체인에 대한 영향

- 클라우드 포도당 플랫폼의 데이터 프라이버시 제약

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 기기 유형별

- 관리 기기

- 인슐린 펌프

- 인슐린 펌프 장치

- 인슐린 펌프 저장소

- 주입 세트

- 인슐린 주사기

- 재사용 가능한 펜 카트리지

- 인슐린 일회용 펜

- 제트 인젝터

- 모니터링 기기

- 혈당 자기 측정 기기

- 글루코미터 기기

- 혈당 측정용 스트립

- 란셋

- 연속 포도당 모니터링

- 센서

- 내구 소비재

- 관리 기기

- 최종 사용자별

- 병원 및 진료소

- 재택치료

- 당뇨병 전문센터·약국

- 환자 유형별

- 제1형 당뇨병

- 제2형 당뇨병

- 임신성 당뇨 및 기타 특정 유형

제6장 시장 지표

- 제1형 당뇨병 인구

- 제2형 당뇨병 인구

제7장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Diabetes Care

- Roche Diabetes Care

- LifeScan Inc.

- Dexcom

- Medtronic

- Arkray Inc.

- Ascensia Diabetes Care

- Novo Nordisk A/S

- Eli Lilly

- Sanofi

- Insulet Corporation

- A. Menarini Diagnostics

- Sinocare Inc.

- Terumo Corporation

- B. Braun Melsungen AG

- Ypsomed AG

- Tandem Diabetes Care

제8장 시장 기회와 전망

SHW 25.10.28Italy diabetes devices market stood at USD 1.1 billion in 2025 and is forecast to reach USD 1.52 billion by 2030, advancing at a 6.7% CAGR.

The steady rise reflects an aging population, a 92.14% dominance of Type 2 cases, and a policy environment that reimburses continuous glucose monitoring (CGM) for priority groups under the National Health Service. Adoption accelerates further as pharmacies become clinical hubs, telemedicine tools spread to 72% of facilities, and hybrid closed-loop pumps enter reimbursement formularies. Management products enjoy a 7.14% CAGR due to weekly insulin and tubeless automated delivery roll-outs, while monitoring devices retain scale leadership at 58.12% share in 2024. North-South funding gaps and stringent European accuracy rules temper momentum, yet targeted digital spending of EUR 1.6 billion keeps Italy among Europe's most attractive pilots for advanced diabetes technology.

Italy Diabetes Devices Market Trends and Insights

Reimbursement of CGM Sensors for T1 & Pediatric Patients

Parliamentary Law 130/2023 mandates national screening for citizens aged 1-17 years, routing newly diagnosed children swiftly toward CGM adoption . The Ministry of Health already funds FreeStyle Libre for both Type 1 and insulin-intensive Type 2 users, removing a key cost hurdle. Multi-center trials in Lombardy, Emilia Romagna, and Toscana report HbA1c falls of 0.4% at three months and 0.6% at six months with intermittently scanned CGM. Early CGM habituation in childhood is expected to lift lifetime adherence and enlarge long-term sensor revenue. Implementation lags occur in Calabria and Sardegna, yet national reimbursement rules give suppliers a clear demand signal.

Growing Telemedicine Adoption & Home-Care Push Post-PNRR

EUR 1.6 billion from the Recovery Plan modernizes electronic health records, enabling 72% of hospitals to activate tele-consults that directly feed glucose data into clinical portals. Surveys of 600 clinicians show 82% endorse tele-follow-up for routine glycemic reviews, while 80% cite infection-control gains in a post-COVID era. The Connected Care platform and Resilia app allow secure sharing of sensor feeds, though 66% of practitioners caution that digital care cannot replace critical in-person titration visits. Broadband blackspots in inland Basilicata slow real-time uploads, but pharmacy Wi-Fi stations increasingly bridge the gap. Overall, remote monitoring saves travel time for elderly patients and encourages continuous data flow that underpins closed-loop dosing algorithms.

Regional Funding Disparity Between North & South

Seven regions, including Calabria and Sardegna, failed minimum-care benchmarks in 2021, leading to rationed CGM allocations and longer waiting lists. New autonomy legislation of June 2024 allows wealthier regions to self-fund enhanced benefits, potentially widening access gaps. Out-of-pocket drug spending equals 23% of national healthcare costs but weighs heavier on lower-income households prevalent in the South. Clinician migration northward compounds capacity shortages. Device suppliers must therefore calibrate pricing tiers and co-pay support programs to avoid lost volumes in underfunded territories.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Pharmacy-Run Diabetes Clinics

- Rising Prevalence & Earlier Onset of Type 2 Diabetes

- Strict eCGM Accuracy Rules Delaying New Entrants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The monitoring category retained 58.12% of Italy diabetes devices market share in 2024, underpinned by the country's entrenched self-testing culture and full reimbursement of FreeStyle Libre for intensive insulin users. Italy diabetes devices market size for monitoring solutions was USD 0.64 billion in 2025 and is set to climb at a 5.9% CAGR on the strength of sensor upgrades and wider pediatric coverage. Blood-glucose strips continue to sell because many seniors trust finger-prick verification, yet Libre 2 users showed HbA1c drops of 0.6% after six months in a 2,000-patient Lombardy cohort . Hospitals increasingly deploy professional CGM for in-patient titration, expanding the addressable volume of disposable sensors.

Management devices, valued at USD 0.46 billion in 2025, outpace monitoring with a 7.14% CAGR to 2030 as automated delivery platforms proliferate. Insulet's Omnipod 5 launch in January 2025 introduced the first tubeless system with dual-sensor compatibility, extending choice for the 300,000 Italian Type 1 users eligible for public reimbursement. The weekly insulin Icodec debut in June 2025 slashes injection events by 86%, triggering needle-syringe replacement cycles and encouraging pump trials for dose accuracy. Italian comparative studies reveal MiniMed 780G achieves 71% Time-in-Range, exceeding Tandem Control-IQ's 68% result, influencing endocrinologist prescribing behaviour. Pen-needle makers follow SIMDO guidance favoring 4 mm 32G formats to minimize lipohypertrophy risk. Management innovations thereby cement a higher-growth runway within the Italy diabetes devices market.

The Italy Diabetes Devices Market Report Segments the Industry Into Device Type (Management Devices and Monitoring Devices), End User (Hospital & Clinics, Home-Care Settings, and More), Diabetes Type (Type 1 Diabetes, Type 2 Diabetes, and Gestational & Other Specific Types). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Abbott Laboratories

- Roche

- Lifescan

- Dexcom

- Medtronic

- Arkray

- Ascensia

- Novo Nordisk

- Eli Lilly and Company

- Sanofi

- Insulet

- A. Menarini Diagnostics

- Sinocare

- Terumo

- B. Braun

- Ypsomed

- Tandem Diabetes Care

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Reimbursement of CGM sensors for T1 & pediatric patients

- 4.2.2 Growing telemedicine adoption & home-care push post-PNRR

- 4.2.3 Expansion of pharmacy-run diabetes clinics (Farmacie dei Servizi)

- 4.2.4 Rising Prevalence of Obesity Among Youth Increasing Earlier Onset Diabetes

- 4.2.5 AI-powered decision-support in hybrid-closed-loop pumps

- 4.2.6 Rising prevalence & earlier onset of Type-2 diabetes

- 4.3 Market Restraints

- 4.3.1 Regional funding disparity between North & South

- 4.3.2 Strict eCGM accuracy rules delaying new entrants

- 4.3.3 Supply-chain exposure to single-use plastics legislation

- 4.3.4 Data-privacy constraints on cloud glucose platforms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Device Type

- 5.1.1 Management Devices

- 5.1.1.1 Insulin Pump

- 5.1.1.1.1 Insulin Pump Device

- 5.1.1.1.2 Insulin Pump Reservoir

- 5.1.1.1.3 Infusion Set

- 5.1.1.2 Insulin Syringes

- 5.1.1.3 Cartridges in Reusable Pens

- 5.1.1.4 Insulin Disposable Pens

- 5.1.1.5 Jet Injectors

- 5.1.2 Monitoring Devices

- 5.1.2.1 Self-Monitoring Blood Glucose

- 5.1.2.1.1 Glucometer Devices

- 5.1.2.1.2 Blood Glucose Test Strips

- 5.1.2.1.3 Lancets

- 5.1.2.2 Continuous Glucose Monitoring

- 5.1.2.2.1 Sensors

- 5.1.2.2.2 Durables

- 5.1.1 Management Devices

- 5.2 By End User

- 5.2.1 Hospitals & Clinics

- 5.2.2 Home-care Settings

- 5.2.3 Specialized Diabetes Centers & Pharmacies

- 5.3 By Patient Type

- 5.3.1 Type-1 Diabetes

- 5.3.2 Type-2 Diabetes

- 5.3.3 Gestational & Other Specific Types

6 Market Indicators

- 6.1 Type-1 Diabetes Population

- 6.2 Type-2 Diabetes Population

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Market Share Analysis

- 7.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 7.3.1 Abbott Diabetes Care

- 7.3.2 Roche Diabetes Care

- 7.3.3 LifeScan Inc.

- 7.3.4 Dexcom

- 7.3.5 Medtronic

- 7.3.6 Arkray Inc.

- 7.3.7 Ascensia Diabetes Care

- 7.3.8 Novo Nordisk A/S

- 7.3.9 Eli Lilly

- 7.3.10 Sanofi

- 7.3.11 Insulet Corporation

- 7.3.12 A. Menarini Diagnostics

- 7.3.13 Sinocare Inc.

- 7.3.14 Terumo Corporation

- 7.3.15 B. Braun Melsungen AG

- 7.3.16 Ypsomed AG

- 7.3.17 Tandem Diabetes Care

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment