|

시장보고서

상품코드

1844664

유럽의 당뇨병 관리 기기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Diabetes Care Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

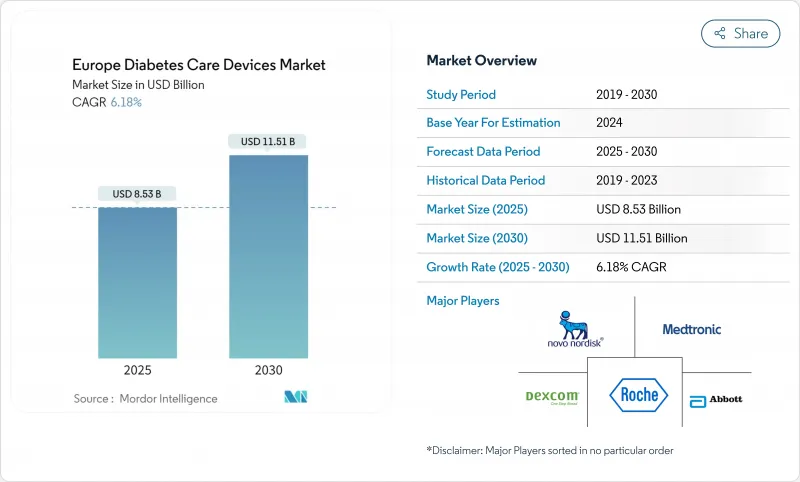

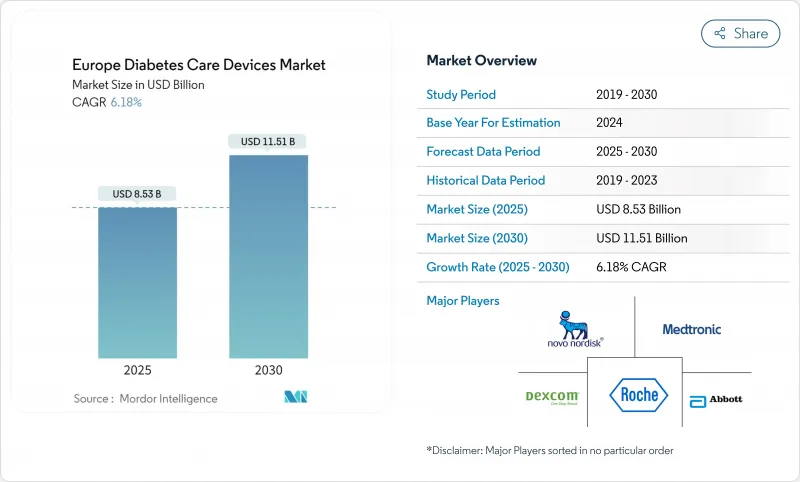

유럽의 당뇨병 관리 기기 시장 규모는 2025년 85억 3,000만 달러로 평가되었고, 2030년에 115억 1,000만 달러에 이를 것으로 예측되며 CAGR은 6.18%를 나타낼 전망입니다.

실시간 혈당 데이터에 대한 수요 증가, 연결형 인슐린 투여 시스템의 확산, 그리고 지원적 보험 적용 조치가 결합되어 성장 모멘텀을 유지하고 있습니다. 주요 유럽 의료 시스템 전반에 걸친 지속적 혈당 모니터링(CGM) 적용 범위 확대는 치료 대상 인구를 넓히고 있으며, 병원형 가정 치료 시범 사업은 입원 치료에서 원격 당뇨병 관리로의 전환을 가속화하고 있습니다. 제조사들은 교육 시간을 최소화하고 치료 순응도를 높이는 올인원 CGM 센서와 패치 펌프를 우선시하고 있으며, 인공지능 기반 용량 조정 소프트웨어는 시범 연구에서 일상적 진료로 전환되고 있습니다. 기존 선도 기업들이 규모 중심의 합병을 추진하고 민첩한 신규 진입자들이 비침습적 모니터링에 집중하면서 경쟁 강도가 높아지고 있어, 제조 역량과 혁신 속도 모두를 보상하는 균형 잡힌 시장 환경이 조성되고 있습니다.

유럽의 당뇨병 관리 기기 시장 동향 및 인사이트

국가적 보험급여 개혁으로 독일 및 북유럽 국가에서 CGM 보급 확대

독일 법정보험은 2024년 초부터 인슐린 의존형 환자 전체로 CGM 적용 범위를 확대하여 주요 비용 장벽을 즉시 해소했습니다. 덴마크, 스웨덴, 노르웨이도 동일한 조치를 취하며, 이제 테스트 스트립보다 센서 기반 모니터링을 우대하는 통일된 북부 클러스터를 형성했습니다. 이에 따른 처방 급증으로 공급업체들은 입찰 확보 및 리드 타임 단축을 위해 센서 조립을 현지화하고 있습니다. 의료 제공자들은 인슐린 치료 시작 후 4주 이내에 CGM을 시작하도록 임상 경로를 수정하며, 일차 진료와 당뇨병 클리닉 간의 연계성을 강화하고 있습니다. 제조사들은 향후 3년간 의료진의 친숙도 향상과 환자 자가관리 앱의 국가 전자건강기록 연동으로 기기 활용률이 꾸준히 상승할 것으로 전망합니다. 따라서 보험 적용 확정은 준수 공급업체에게 더 높은 판매량, 예측 가능한 수익, 강화된 협상력을 가져다주고 있습니다

EU 의료기기 규정(MDR) IIb등급 ‘스마트 펜’ 신속 심사 도입으로 제품 출시 가속화

EU 의료기기 규정(MDR) 하에서 2024년 도입된 연결형 인슐린 펜에 대한 12-15개월 신속 심사 제도는 평균 시장 출시 기간을 약 1/3 단축시켰다. 주요 개발사들은 투여량 데이터를 수집하고 투여 누락을 경고하며 정보를 의사 대시보드로 전송하는 블루투스 지원 펜을 신속히 제출했습니다. 초기 승인으로 후속 신청이 잇따르며 규제 병목 현상이 당분간 재발하지 않을 것임을 시사합니다. 마케팅 팀은 유럽 출시를 글로벌 브랜드 캠페인과 연계해 초기 시장 점유율을 극대화하며 단축된 일정을 활용하고 있습니다. 프리미엄 펜의 보험 적용을 주저하던 국가별 의약품 목록 관리 기관들은 실제 사용 환경에서의 복약 순응도 향상이 이제 정량화되기 쉬워짐에 따라 비용-편익 모델을 재검토 중입니다. 이러한 요소들이 종합적으로 작용하며 유럽은 차세대 인슐린 투여 하드웨어의 발판이 되고 있습니다.

기기 대비 소모품의 상이한 부가가치세율, 자가혈당관리 경제성 왜곡

여러 EU 국가에서 혈당 측정기는 부가가치세 감면 대상이지만 테스트 스트립은 전액 과세되어 자가혈당관리의 평생 비용이 부풀려지고 있습니다. 환자들은 검사를 미루거나 스트립 사용을 늘려 혈당 조절을 저해할 수 있습니다. 제조사들은 의료기기 부가가치세 제도의 조화를 위해 로비하고 있으나 입법 진전은 더딘 상태다. 그동안 저가 스트립 번들 및 구독 모델이 검사 빈도 유지를 목표로 하고 있습니다. 세금 균등화가 달성될 때까지 스트립 기반 모니터링의 경제성은 유럽 당뇨병 치료 기기 시장 내 해당 부문의 성장 잠재력을 제한할 것입니다.

부문 분석

모니터링 부문은 2024년 유럽 당뇨병 관리 기기 시장의 54.01%를 차지하며, 일상 치료에서 정확한 혈당 데이터의 중요성을 반영했습니다. CGM 시스템은 통증 없는 연속 측정값을 제공하고 스마트폰 및 병원 대시보드와 원활하게 연동되어 현재 모니터링 매출의 대부분을 차지합니다. CGM 보급률은 1형 당뇨병 환자를 넘어 모든 인슐린 치료 환자로 보험 적용이 확대되면서 가속화되었습니다. 공급업체들은 센서 착용 시간, 교정 불필요 작동, 시계 직접 연결 기능으로 차별화를 꾀하며, 정기적 측정을 위한 핑거스틱 측정기의 점진적 퇴출을 예고하고 있습니다.

관리 기기는 수익 규모는 작지만 2030년까지 연평균 7.07% 성장할 것으로 전망됩니다. CGM 입력값과 폐쇄 루프 알고리즘을 결합한 자동 인슐린 투여 시스템이 이러한 추세를 대표합니다. 그 결과 전통적으로 분리된 하드웨어 카테고리가 자율적 혈당 조절이 가능한 통합 생태계로 더욱 긴밀하게 융합되고 있습니다. 알고리즘 정확도가 향상됨에 따라 보험사들은 고급 펌프-센서 시스템을 향후 합병증 비용을 상쇄하는 투자로 인식하는 경향이 커지고 있습니다. 결과적으로 관리 기기는 모니터링 도구와의 격차를 좁히고, 10년 말에는 가치 측면에서 이를 추월할 수도 있어 유럽 당뇨병 관리 기기 시장 내 경쟁 중심축을 재편할 전망입니다.

2024년 유럽 당뇨병 관리 기기 시장 규모에서 제2형 당뇨병 환자가 81.35%를 차지하며, 제1형 중심 설계에서 광범위한 대사 건강 활용 사례로의 패러다임 전환을 부각시켰다. 이 집단을 겨냥한 제품 로드맵은 단순성, 눈에 띄지 않는 디자인, 낮은 교육 부담을 지향합니다. 식이 추적 앱과 연동되는 연결형 센서는 집중적인 인슐린 조절보다 생활습관 피드백에 관심이 많은 제2형 사용자에게 어필합니다. 국가 지침이 이제 기초 인슐린 요법에도 CGM(지속적 포도당 모니터링)을 권장함에 따라, 기기 제조사들은 핵심 정확도는 유지하면서 고급 부가 기능을 생략한 가성비 센서를 출시하고 있습니다.

1형 당뇨병은 획기적 혁신에 여전히 막대한 영향력을 행사합니다. 하이브리드 폐쇄 루프 시스템은 성인 사용자로 확대되기 전 소아 1형 당뇨병 환자군에서 완성되었으며, 최근에는 특정 2형 당뇨병 하위 그룹으로 확대되고 있습니다. 한편 임신성 당뇨병은 신속한 도입과 임신기별 구독 모델을 강조하는 맞춤형 솔루션의 관심을 받기 시작했습니다. 환자 유형의 다양화는 종합적으로 유럽 당뇨병 치료 기기 시장을 확대하고 특정 치료 경로에 대한 의존도를 완화합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 독일 및 북유럽 국가의 CGM 도입 촉진하는 국가적 보상 제도 개혁

- 제품 출시 가속화하는 EU MDR Class IIb “스마트 펜” 신속 승인 절차

- 남유럽 지역 테스트 스트립 가격의 입찰 주도적 통합

- 중부 및 동유럽(CEE) 지역 소아 1형 당뇨병(T1D) 유병률 급증으로 패치-펌프 수요 촉진

- 영국 및 프랑스의 ‘병원-앳-홈(Hospital-at-Home)’ 시범 사업으로 원격 모니터링 키트 수요 증가

- 스페인의 AI 기반 의사 결정 지원 의무화로 스마트 펜 판매 증가

- 시장 성장 억제요인

- 기기 대비 소모품에 대한 상이한 부가가치세(VAT)율로 인한 자가혈당측정(SMBG) 경제성 왜곡

- DACH 지역 클라우드 CGM 플랫폼 제한하는 데이터 거주 규정

- 이탈리아 및 스페인 인슐린 펌프 지원 지연시키는 분산된 HTA 절차

- 베네룩스 지역 소유 비용 증가시키는 센서 폐기물 처리 규정

- 공급망 분석

- 규제 전망

- 기술적 전망

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 기기유형별

- 모니터링 기기

- 자기 혈당 측정 장치

- 혈당 측정기

- 테스트 스트립

- 란셋

- 연속 혈당 모니터링

- 센서

- 내구 소비재

- 관리 기기

- 인슐린 펌프

- 인슐린 펌프 장치

- 인슐린 펌프 저장소

- 주입 세트

- 인슐린 주사기

- 인슐린 펜

- 제트 인젝터

- 모니터링 기기

- 환자 유형별

- 1형 당뇨병

- 2형 당뇨병

- 임신 및 기타

- 최종 사용자별

- 병원 및 클리닉

- 재택치료

- 외래수술센터(ASC)

- 약국, 소매 체인

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 전자상거래

- 국가별

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

제6장 경쟁 구도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Medtronic PLC

- F. Hoffmann-La Roche AG

- Dexcom Inc.

- Ascensia Diabetes Care Holdings AG

- Novo Nordisk A/S

- Sanofi SA

- Insulet Corporation

- Tandem Diabetes Care Inc.

- Ypsomed AG

- Senseonics Holdings Inc.

- Becton, Dickinson and Company(BD)

- Terumo Corporation

- Eli Lilly and Company

- B. Braun Melsungen AG

- Owen Mumford Ltd.

- Nipro Corporation

- Menarini Diagnostics Srl

- AgaMatrix Holdings LLC

- Sooil Development Co. Ltd.

제7장 시장 기회와 전망

HBR 25.11.03The Europe diabetes care devices market size is valued at USD 8.53 billion in 2025 and is forecast to reach USD 11.51 billion by 2030, advancing at a 6.18% CAGR.

Strong demand for real-time glucose data, wider adoption of connected insulin delivery systems, and supportive reimbursement measures combine to sustain growth momentum. Expanded coverage for continuous glucose monitoring (CGM) across major European health systems is broadening the treated population, while hospital-at-home pilots are accelerating the shift from inpatient to remote diabetes management. Manufacturers are prioritizing all-in-one CGM sensors and patch pumps that minimize training time and improve adherence, and artificial-intelligence-driven dose-adjustment software is moving from pilot studies to routine practice. Competitive intensity is rising as incumbent leaders pursue scale-driven mergers and nimble entrants focus on non-invasive monitoring, creating a balanced landscape that rewards both manufacturing depth and innovation speed.

Europe Diabetes Care Devices Market Trends and Insights

National Reimbursement Reforms Boosting CGM Uptake in Germany & Nordics

Statutory insurance in Germany broadened CGM coverage to all insulin-dependent patients at the start of 2024, instantly eliminating the primary cost barrier. Denmark, Sweden, and Norway mirrored the move, creating a unified northern cluster where reimbursement now favors sensor-based monitoring over test strips. The resulting surge in prescriptions is encouraging suppliers to localize sensor assembly to secure tender points and shorten lead times. Healthcare providers are revising clinical pathways so that CGM initiation happens within four weeks of insulin therapy commencement, tightening links between primary care and diabetology clinics. Manufacturers expect device utilization rates to climb steadily over the next three years as physician familiarity increases and patient self-management apps integrate national e-health records. Reimbursement certainty is therefore translating into higher volumes, more predictable revenue, and stronger negotiating power for compliant suppliers

EU MDR Fast-Track for Class IIb "Smart Pens" Accelerating Product Launches

The 2024 introduction of a twelve-to-fifteen-month fast-track review for connected insulin pens under the EU Medical Device Regulation slashed average time-to-market by roughly one-third. Leading developers rapidly submitted Bluetooth-enabled pens that capture dose data, flag omissions, and transmit information to physicians' dashboards. Early approvals have prompted a queue of follow-on filings, signaling that the regulatory bottleneck is unlikely to return soon. Marketing teams are capitalizing on the compressed timeline by aligning European launches with global brand campaigns, thereby maximizing initial uptake. National formularies that previously hesitated to reimburse premium pens are reassessing cost-benefit models because real-world adherence gains are now easier to quantify. Collectively, these factors make Europe the launchpad for next-generation insulin-delivery hardware. .

Divergent VAT Rates on Devices vs. Consumables Distorting SMBG Economics

Reduced VAT on glucose meters but full VAT on test strips in several EU states inflates lifetime costs for self-monitoring of blood glucose. Patients may defer testing or stretch strip use, undermining glycemic control. Manufacturers are lobbying for harmonized medical-device VAT schemes, yet legislative progress remains slow. In the interim, low-priced strip bundles and subscription models aim to preserve testing frequency. Until tax parity is achieved, the economics of strip-based monitoring will limit growth potential for the segment inside the Europe diabetes care devices market.

Other drivers and restraints analyzed in the detailed report include:

- Tender-Driven Consolidation of Test-Strip Pricing in Southern Europe

- Hospital-at-Home Pilots in the UK & France Driving Remote Monitoring Kits

- Data-Residency Rules Limiting Cloud CGM Platforms in the DACH Region

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The monitoring segment captured 54.01% of the Europe diabetes care devices market in 2024, reflecting the primacy of accurate glucose data in day-to-day therapy. CGM systems now account for a majority of monitoring revenue because they deliver painless, continuous readings and integrate seamlessly with smartphones and hospital dashboards. CGM penetration accelerated once reimbursement expanded beyond type-1 to all insulin-treated patients. Suppliers are differentiating through sensor wear time, calibration-free operation, and direct-to-watch connectivity, signalling a gradual fade-out of fingerstick meters for regular measurement.

Management devices represent a smaller revenue pool but are forecast to progress at a 7.07% CAGR to 2030. Automated insulin delivery systems that combine CGM input with closed-loop algorithms epitomize this momentum. The result is a tighter convergence of traditionally separate hardware categories into unified ecosystems capable of autonomous glucose control. As algorithm accuracy improves, payers increasingly view advanced pump-sensor systems as an investment that offsets future complication costs. Consequently, management devices will narrow the gap with monitoring tools and may even surpass them in value toward the end of the decade, reshaping the competitive centre of gravity within the Europe diabetes care devices market.

Type-2 diabetes patients accounted for 81.35% of the Europe diabetes care devices market size in 2024, underscoring a paradigm shift from type-1-centric engineering to broader metabolic-health use cases. Simplicity, discreet form factors, and low training overhead guide product roadmaps aimed at this cohort. Connected sensors that pair with diet-tracking apps appeal to type-2 users keen on lifestyle feedback rather than intensive insulin titration. As national guidelines now encourage CGM even for basal-insulin regimens, device makers are rolling out value-priced sensors that maintain core accuracy while omitting premium bells and whistles.

Type-1 diabetes retains outsized influence on breakthrough innovation. Hybrid closed-loop systems were perfected in the paediatric type-1 population before scaling to adult users and, more recently, to select type-2 subgroups. Meanwhile, gestational diabetes is beginning to attract tailored solutions that emphasise rapid onboarding and per-trimester subscription models. Collectively, patient-type diversification broadens the Europe diabetes care devices market and mitigates reliance on any single therapy pathway.

Europe Diabetes Care Devices Market Report is Segmented by Device Type (Monitoring Devices, Management Devices), Patient Type (Type-1 Diabetes, Type-2 Diabetes, Gestational & Others), End-User (Hospitals & Clinics, Home-Care Settings, and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Abbott Laboratories

- Medtronic

- Roche

- Dexcom

- Ascensia Diabetes Care Holdings AG

- Novo Nordisk

- Sanofi

- Insulet

- Tandem Diabetes Care

- Ypsomed

- Senseonics

- Beckton Dickinson

- Terumo

- Eli Lilly and Company

- B. Braun

- Owen Mumford

- Nipro

- Menarini Diagnostics Srl

- AgaMatrix Holdings LLC

- Sooil Development Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 National Reimbursement Reforms Boosting CGM Uptake in Germany & Nordics

- 4.2.2 EU MDR Fast-Track for Class IIb "Smart Pens" Accelerating Product Launches

- 4.2.3 Tender-Driven Consolidation of Test-Strip Pricing in Southern Europe

- 4.2.4 Pediatric T1D Prevalence Surge in CEE Fueling Patch-Pump Demand

- 4.2.5 Hospital-at-Home Pilots in UK & France Driving Remote Monitoring Kits

- 4.2.6 AI-based Decision Support Mandates in Spain Increasing Smart Pen Sales

- 4.3 Market Restraints

- 4.3.1 Divergent VAT Rates on Devices vs. Consumables Distorting SMBG Economics

- 4.3.2 Data-Residency Rules Limiting Cloud CGM Platforms in DACH Region

- 4.3.3 Fragmented HTA Processes Delaying Insulin Pump Funding in Italy & Spain

- 4.3.4 Sensor Waste-Disposal Regulations Raising Cost of Ownership in Benelux

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Device Type

- 5.1.1 Monitoring Devices

- 5.1.1.1 Self-Monitoring Blood Glucose

- 5.1.1.1.1 Glucometer Devices

- 5.1.1.1.2 Test Strips

- 5.1.1.1.3 Lancets

- 5.1.1.2 Continuous Glucose Monitoring

- 5.1.1.2.1 Sensors

- 5.1.1.2.2 Durables

- 5.1.2 Management Devices

- 5.1.2.1 Insulin Pumps

- 5.1.2.1.1 Insulin Pump Device

- 5.1.2.1.2 Insulin Pump Reservoir

- 5.1.2.1.3 Infusion Set

- 5.1.2.2 Insulin Syringes

- 5.1.2.3 Insulin Pens

- 5.1.2.4 Jet Injectors

- 5.1.1 Monitoring Devices

- 5.2 By Patient Type

- 5.2.1 Type-1 Diabetes

- 5.2.2 Type-2 Diabetes

- 5.2.3 Gestational & Others

- 5.3 By End-user

- 5.3.1 Hospitals & Clinics

- 5.3.2 Home-care Settings

- 5.3.3 Ambulatory Surgical Centres

- 5.3.4 Pharmacies & Retail Chains

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Direct-to-Consumer E-commerce

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Spain

- 5.5.5 Italy

- 5.5.6 Rest of Europe

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Medtronic PLC

- 6.3.3 F. Hoffmann-La Roche AG

- 6.3.4 Dexcom Inc.

- 6.3.5 Ascensia Diabetes Care Holdings AG

- 6.3.6 Novo Nordisk A/S

- 6.3.7 Sanofi S.A.

- 6.3.8 Insulet Corporation

- 6.3.9 Tandem Diabetes Care Inc.

- 6.3.10 Ypsomed AG

- 6.3.11 Senseonics Holdings Inc.

- 6.3.12 Becton, Dickinson and Company (BD)

- 6.3.13 Terumo Corporation

- 6.3.14 Eli Lilly and Company

- 6.3.15 B. Braun Melsungen AG

- 6.3.16 Owen Mumford Ltd.

- 6.3.17 Nipro Corporation

- 6.3.18 Menarini Diagnostics Srl

- 6.3.19 AgaMatrix Holdings LLC

- 6.3.20 Sooil Development Co. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment