|

시장보고서

상품코드

1846165

자동차용 스티어링 휠 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Steering Wheel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

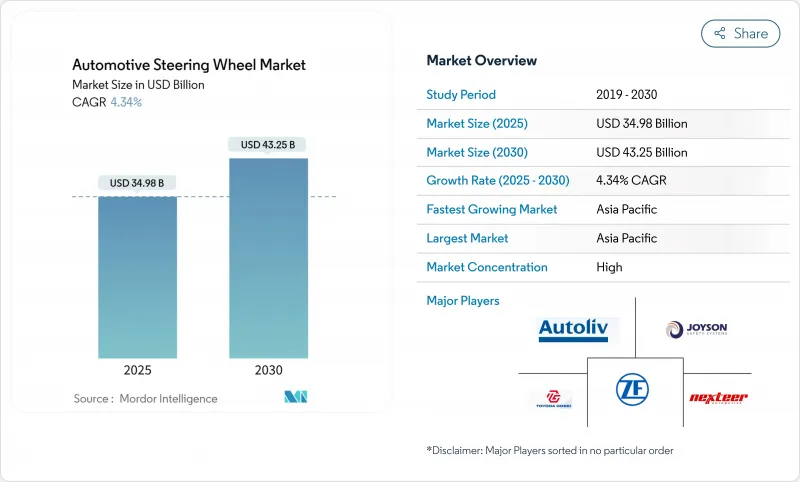

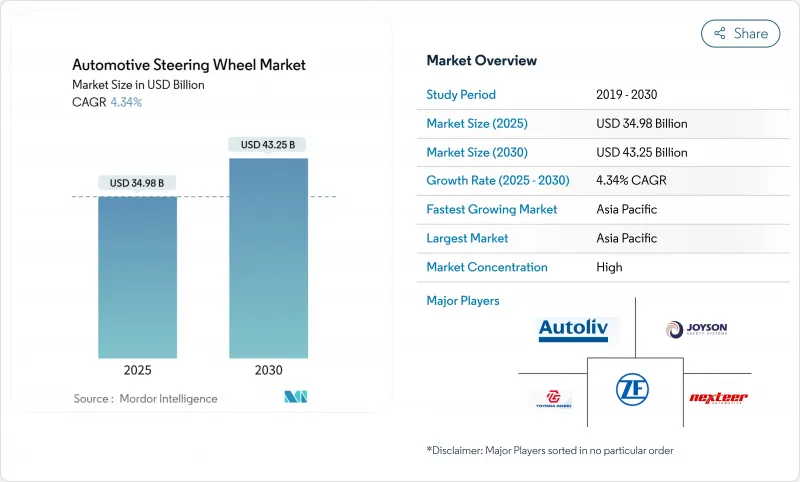

자동차용 스티어링 휠 시장은 2025년에 349억 8,000만 달러가 되고, 2030년에는 432억 5,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년)의 CAGR은 4.34%를 나타낼 전망입니다.

전동화, 레벨 3이상의 자율주행차의 개발, 에어백의 통합과 생체인증 드라이버·모니터링의 핸들에의 탑재를 추진하는 안전 지령의 확대가 개발을 뒷받침합니다. 전동 파워 스티어링(EPS)은 여전히 판매량의 핵심이지만 프리미엄 EV 프로그램이 칼럼리스 조종석을 검증함에 따라 스티어 바이 와이어(SbW) 플랫폼이 가장 빠르게 확대되고 있습니다. 경량 금속과 천연섬유 복합재료는 OEM의 지속가능성 목표를 지원하면서 질량을 제한합니다. 아시아태평양은 중국의 배터리 전기 붐과 반도체의 현지화에 의해 생산 점유율을 획득하고 있지만, 북미와 유럽은 촉각 컨트롤을 갖춘 프리미엄 인터페이스 수요를 견인하고 있습니다. 경쟁의 심각성은 적당하며 레거시 리더 오토 리브, 제트 에프 프리드리히스 하펜, 조이슨이 수직 통합을 진행하고 있습니다. 그러나 Software-Defined Vehicle의 전문가와 칩 제조업체는 스티어링 컨트롤과 사이버 보안 스택에서 백스페이스를 개척하고 있습니다.

세계의 자동차용 스티어링 휠 시장 동향 및 인사이트

스티어 바이 와이어(SBW) 플랫폼 채택 급증

메르세데스 벤츠는 NIO가 2025년에 ZF의 칼럼리스 아키텍처를 채용한 ET9를 발표한 데 이어 2026년 EQS에서 풀 SbW를 전개할 계획입니다. 이 기술은 기계적 링크를 제거하고 가변 비율과 소프트웨어로 튜닝된 피드백을 통해 도시 지역의 조종성과 고속 안정성을 제공합니다. Zet-Ef는 2030년까지 SbW 하드웨어의 CAGR 7.90%를 나타내는 여러 OEM 계약을 받았습니다. 이 변화는 소프트웨어에 의해 정의된 섀시 제어를 가능하게 하는 한편, 종래공급업체에게 전자 장치 및 사이버 보안의 능력 구축을 부과하고 있습니다. 중국의 초기 단계에서의 승리는 규제 당국이 이 아키텍처의 호모로게이션에 적극적임을 보여주며 세계적인 보급을 가속화하고 있습니다.

스티어링 휠에 전면 에어백 통합 의무화

2024년 7월에 발효된 EU 일반 안전 규칙 II는 긴급 브레이크와 졸음 경고 기능을 강화할 것을 의무화하여 스티어링 디자인을 재구성했습니다. 미국에서는 DADSS 프로그램 하에서 림에 내장된 촉각 센서를 이용한 운전장애 검지에 관한 NHTSA의 조사가 진행되고 있습니다. ZF LIFETEC은 미관과 충돌 성능을 융합시킨 탑 전개형 에어백을 설계하여 보다 엄격한 패키징 제한에 적합합니다. 규제 수렴은 시스템의 복잡성과 통합 비용을 증가시키지만 세계 요구 사항을 표준화하여 티어 온에서 볼륨 레버리지를 생성합니다.

불안정한 알루미늄과 마그네슘 가격

알루미늄과 마그네슘의 스팟 가격은 2024년부터 2025년에 걸쳐 20% 이상 변동해 경량 림과 스포크의 마진을 압박하고 있습니다. 공급업체는 장기 공급 계약과 합금 대체로 헤지하고 있지만, 비용 상승은 비용에 민감한 부문에서의 채용을 방해합니다. OEM은 변동을 상쇄하기 위해 재활용 원료를 찾고 있지만, Tier 2의 파운드리은 여전히 원료 위험에 노출되어 있습니다.

부문 분석

OEM이 효율성과 ADAS 대응성을 요구해 유압 시스템을 전동 어시스트로 업그레이드했기 때문에 2024년에는 EPS가 자동차용 스티어링 휠 시장의 38.23%를 차지했습니다. 저비용과 기계적 간편함을 선호하는 시장에서는 전통적인 칼럼 스티어가 뿌리 깊습니다. 스티어 바이 와이어는 여전히 틈새 시장이지만 프리미엄 EV 출시와 자율 주행 프로그램 덕분에 2030년까지 연평균 복합 성장률(CAGR)은 7.90%를 나타낼 것으로 예측됩니다.

스티어링 휠 시장 규모에서는 EPS의 비중이 높은 부분이 오늘날의 전동화를 지원하는 반면, SbW는 레벨 3의 핸즈프리 모드를 위한 지반을 정비하고 있습니다. Zet-Ef의 ET9 계약은 유압 작동유 없이 가변 비율과 소프트웨어 정의 느낌을 실현하여 상업적 실행 가능성을 보여줍니다. 상용 트럭은 EPS 유닛이 최대 8,000Nm의 토크를 발휘하면서도 유압 펌프에 비해 에너지 소비를 줄이고 효율성을 증명합니다.

2차 효과는 공급자의 포지셔닝을 형성합니다. EPS 유닛은 레인 유지 및 오토파크 기능을 제공하는 통합 토크 센서에 의존하며 저비용 기업의 진입 장벽을 높입니다. SbW 아키텍처는 수납식 칼럼을 위한 새로운 영역을 만들어 내고 거실의 캐빈 컨셉을 가능하게 합니다. 고대역폭 CAN-FD 또는 이더넷 기반 도메인 컨트롤러를 통합하면 섀시와 인포테인먼트 영역의 경계가 더욱 모호해지고 기존 칼럼 전문 제조업체가 아닌 소프트웨어 통합자에게 백스페이스를 제공하게 됩니다.

2024년 자동차용 스티어링 휠 시장 점유율은 알루미늄이 37.45%로 선두를 유지했습니다. 스틸은 무게보다 내구성이 중시되는 헤비 듀티 용으로 존속하고 있습니다. 마그네슘 림은 고성능 틈새를 지원하지만 가공 및 부식 비용의 장애물에 직면합니다. 대마와 아마를 중심으로 한 천연섬유 복합재료는 자동차 제조업체의 요람에서 게이트까지의 CO2 목표에 힘입어 2030년까지 연평균 복합 성장률(CAGR) 7.65%를 나타낼 것으로 전망되고 있습니다. 큐플러의 ampliTex 시트백은 탄소섬유에 비해 CO2를 49% 절감하여 내부 부품의 확장성을 보여줍니다.

스티어링 휠 시장에서는 알루미늄 골격 위에 바이오 복합재를 사용한 스킨이 구조적 무결성과 촉각적인 지속가능성 단서를 연결하는 이점이 있습니다. 흡습성에는 고급 수지 시스템이 필요하며 바이오 섬유 부품은 EV 페인트 라인에서 일반적인 200°C 베이크 사이클을 초과 할 수 없습니다. 하지만 2028년 이후 인테리어에 25%의 재활용 또는 바이오 소재를 사용하도록 요구하는 유럽의 지침은 천연섬유에 대한 지지를 강화하고 있습니다.

지역 분석

아시아태평양은 2024년 48.67%의 점유율로 자동차용 스티어링 휠 시장을 선도했고 중국의 EV 급증과 정책에 의한 칩 국산화의 뒷받침을 받아 CAGR 6.80%를 나타낼 전망입니다. 베이징은 2025년까지 반도체의 국산화율을 25%로 하는 것을 목표로 하고 있으며, 휠 일체형 센서와 ECU공급을 지원하고 있습니다. 대규모 생산과 비용 효율성은 햅틱 피드백과 같은 프리미엄 기능을 중간 부문 차량으로 빠르게 전환할 수 있게 합니다. 그러나 희토류 자석의 수출 규제는 스즈키와 포드 공장의 일시적인 운영 중단에서 볼 수 있듯이 OEM 생산 일정을 혼란스럽게 만듭니다.

북미는 여전히 비용 리더가 아닌 기술 어댑터입니다. 미국 인프라법에서는 운전자의 장애 감지가 요구되고 있으며 센서가 장착된 휠 수요에 박차를 가하고 있습니다. 한편 캐나다와 멕시코 공장에서는 디트로이트 쓰리의 EV 프로그램에 대응하기 위해 EPS 생산량을 확대하고 있습니다. Nexteer가 멕시코에 신설한 테크니컬 센터에서는 니어 쇼어링의 동향을 이용해, 칼럼 유형의 EPS와 SbW의 검증에 연마를 하기 위해, 2026년까지 350의 역할을 추가합니다. 멕시코 조립에 대한 미국의 잠재적 관세를 둘러싼 무역 정책의 불확실성은 운임 프리미엄이 있음에도 불구하고 조달을 아시아로 되돌릴 수 있습니다.

유럽은 프리미엄화와 엄격한 안전 의무화의 균형을 맞추고 있습니다. EU GSR II와 Euro NCAP 2026의 물리적 버튼 요구 사항은 통합 휠 컨트롤과 그립 센서에 대한 수요를 지원합니다. 보쉬의 헝가리 공장은 현재 지역 OEM을 위해 EPS 랙을 생산하고 있으며 프리미엄 고객 근처에서 생산 능력을 확대하고 있습니다. 공급면에서 독일 티어오너는 TUV와 KBA 당국을 통해 SbW 검증을 추진하고 세계 호모로게이션을 통해 파급하는 성능 벤치마크를 설정하고 있습니다.

남미, 중동, 아프리카 등 신흥 지역은 저수준에서 2자리수의 대수 성장을 보이고 있습니다. 인도의 부품 제조업체는 1,000억 달러의 수출을 목표로 하고 있으며, 스티어링 휠 어셈블리는 관세 친화적인 볼륨 카고로 보여지고 있습니다. ZF Rane이 TRW Sun Steering Wheels를 인수하면 글루그램 공장과 푸네 공장이 추가되어 에어백과 센서의 국산화가 강화됩니다. 걸프 국가, 차량의 탈탄소화를 위해 EV 도입을 가속, 인프라 격차가 SbW의 대규모 전개를 지연시킵니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 스티어 바이 와이어(SBW) 플랫폼 채용 급증

- 스티어링 휠에 전면 에어백 통합의 의무화

- EV OEM에 의한 경량화의 추진

- 프리미엄화와 차내 UX의 업그레이드

- 휠 센서에 의한 주행장애 모니터링의 법제화

- L3 차량에 있어서 수납 가능/칼럼리스 조종석 수요

- 시장 성장 억제요인

- 알루미늄과 마그네슘의 가격 변동

- 세계의 Sbw 호모로게이션과 사이버 보안 준수의 지연

- 햅틱/드라이버 센스 모듈의 칩 레벨 부족

- 로보 택시에서 조이스틱/음성 HMI의 점유율 위험

- 햅틱/드라이버 감지 모듈의 칩 레벨 부족

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 기술별

- 기존 컬럼 스티어링

- 전동식 파워 스티어링(EPS)

- 전동식 스티어 바이 와이어(SbW)

- 재료 유형별

- 알루미늄 림

- 마그네슘 림

- 강철 림

- 천연섬유 복합재 림

- 차종별

- 승용차

- 소형 상용차

- 대형 상용차

- 버스 및 코치

- 판매 채널별

- OEM

- 애프터마켓

- 추진 유형별

- 내연 엔진

- 배터리 전기자동차

- 하이브리드 전기자동차

- 플러그인 하이브리드 전기자동차

- 연료전지 전기자동차

- 대체연료

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 필리핀

- 인도네시아

- 베트남

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향과 파트너십

- 시장 점유율 분석

- 기업 프로파일

- Autoliv Inc.

- ZF Friedrichshafen AG

- Joyson Safety Systems

- Toyoda Gosei Co., Ltd.

- Valeo SA

- Nexteer Automotive Group

- Tokai Rika Co., Ltd.

- Hyundai Mobis Co., Ltd.

- JTEKT Corporation

- NSK Ltd.

- Mando Corporation

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- Thyssenkrupp AG

제7장 시장 기회와 전망

KTH 25.11.07The automotive steering wheel market stood at USD 34.98 billion in 2025 and is forecast to reach USD 43.25 billion by 2030, advancing at a 4.34% CAGR during the forecast period (2025-2030).

Growth is propelled by electrification, Level 3+ autonomous vehicle development, and expanding safety mandates pushing airbag integration and biometric driver-monitoring into the wheel. Electric Power Steering (EPS) remains the volume backbone, yet steer-by-wire (SbW) platforms are scaling fastest as premium EV programs validate column-less cockpits. Lightweight metals and natural-fiber composites limit mass while supporting OEM sustainability targets. Asia-Pacific commands production share thanks to China's battery-electric boom and semiconductor localisation, whereas North America and Europe pull demand for premium interfaces with haptic controls. Competitive intensity is moderate: legacy leaders Autoliv, ZF Friedrichshafen, and Joyson extend vertical integration. However, software-defined vehicle specialists and chipmakers are carving out white-space in steering control and cybersecurity stacks.

Global Automotive Steering Wheel Market Trends and Insights

Surging Adoption of Steer-By-Wire (SBW) Platforms

Mercedes-Benz will roll out full SbW on the 2026 EQS, following NIO's 2025 launch of the ET9 that features ZF's column-less architecture. The technology removes mechanical links, enabling variable ratios and software-tuned feedback for urban manoeuvrability and high-speed stability. ZF has secured multi-OEM contracts that underpin a 7.90% CAGR for SbW hardware through 2030. The shift allows software-defined chassis control while challenging traditional suppliers to build electronic and cybersecurity competencies. Early wins in China illustrate regulators' willingness to homologate the architecture, accelerating global uptake.

Mandatory Frontal-Airbag Integration in Steering Wheels

EU General Safety Regulation II, effective July 2024, compels enhanced emergency braking and drowsiness-warning functions that re-shape steering design. In the United States, NHTSA research into driver-impairment detection uses tactile sensors embedded in the rim under the DADSS program. ZF LIFETEC has engineered top-deployment airbags that blend aesthetics with crash performance, meeting stricter packaging limits. Convergence of mandates raises system complexity and integration cost but standardises global requirements, creating volume leverage for tier-ones.

Volatile Aluminum and Magnesium Prices

Spot prices for aluminium and magnesium have swung more than 20% in 2024-2025, squeezing margins on lightweight rims and spokes. Suppliers hedge through long-term supply contracts and alloy substitution, yet cost spikes deter adoption in cost-sensitive segments. OEMs explore recycled feedstock to offset volatility, but tier-two casting shops remain exposed to raw-material risk.

Other drivers and restraints analyzed in the detailed report include:

- Light-Weighting Push From EV OEMs

- Legislative Drive-Impairment Monitoring Via Wheel Sensors

- Global SbW Homologation and Cyber-Security Compliance Lag

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EPS controlled 38.23% of the automotive steering wheel market in 2024 as OEMs upgraded hydraulic systems to electric assist for efficiency and ADAS readiness. Conventional column-steer persists in markets prioritising low cost and mechanical simplicity. Steer-by-wire remains niche but is forecast at 7.90% CAGR to 2030 thanks to premium EV launches and autonomous drive programs.

The EPS-heavy portion of the steering wheel market size supports today's electrification, while SbW prepares the ground for Level 3+ hands-free modes. ZF's ET9 contract showcases commercial viability, delivering a variable ratio and software-defined feel without hydraulic fluid. In commercial trucks, EPS units provide up to 8,000 Nm torque yet trim energy draw compared with hydraulic pumps, underlining the efficiency case.

Second-order effects shape supplier positioning. EPS units rely on integrated torque sensors that feed lane-keep and auto-park functions, raising entry barriers for low-cost players. SbW architectures create fresh real estate for retractable columns, enabling living-room cabin concepts. Integration of high-bandwidth CAN-FD or Ethernet-based domain controllers further blurs lines between chassis and infotainment domains, offering white-space for software integrators rather than classic column specialists.

Aluminium remained the leader with 37.45% of the automotive steering wheel market share in 2024, credited to 40% mass savings and endless recyclability. Steel endures for heavy-duty fleets where durability trumps weight. Magnesium rims serve high-performance niches but face processing and corrosion cost hurdles. Natural-fibre composites, notably hemp and flax, are set to grow 7.65% CAGR through 2030, propelled by automakers' cradle-to-gate CO2 targets. Cupra's ampliTex seatbacks cut 49% CO2 versus carbon fibre, signalling scalability for interior parts.

The steering wheel market benefits from bio-composite skins over aluminium skeletons, marrying structural integrity with tactile sustainability cues. Challenges persist: moisture absorption demands advanced resin systems, and bio-fibre parts cannot exceed 200 °C bake cycles common in EV paint lines. Nevertheless, European directives urging 25% recycled or bio-based content in interiors post-2028 strengthen the pull for natural fibres.

The Automotive Steering Wheel Market is Segmented by Technology (Conventional Column-Steer, and More), Material Type (Aluminum Rim, Magnesium Rim, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (Original-Fitted and Aftermarket Replacement), Propulsion Type (Internal Combustion Engine, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the automotive steering wheel market with 48.67% share in 2024 and is growing at 6.80% CAGR on the strength of China's EV surge and policy-backed chip localisation. Beijing targets 25% local semiconductor content by 2025, anchoring supply for wheel-integrated sensors and ECUs. Large-scale production and cost efficiencies permit rapidly migrating premium features such as haptic feedback into mid-segment vehicles. However, export restrictions on rare-earth magnets have disrupted OEM production schedules, as seen in temporary shutdowns at Suzuki and Ford plants.

North America remains a technology adopter rather than a cost leader. US infrastructure legislation mandates driver-impairment detection, spurring demand for sensor-rich wheels, while Canadian and Mexican plants scale EPS output to serve Detroit Three EV programs. Nexteer's new technical centre in Mexico adds 350 roles by 2026 to hone column-type EPS and SbW validation, exploiting near-shoring trends. Trade-policy uncertainty around potential US tariffs on Mexican assemblies could shift sourcing back to Asia despite freight premiums.

Europe balances premiumisation with strict safety mandates. EU GSR II and Euro NCAP 2026 physical-button requirements anchor demand for integrated wheel controls and grip sensors. Bosch's Hungarian plant now produces EPS racks for regional OEMs, evidencing capacity expansion nearer to premium customers. On the supply side, German tier-ones push SbW validation through TUV and KBA authorities, setting performance benchmarks that ripple through global homologation.

Emerging regions - South America, the Middle East, and Africa - show double-digit unit growth off low bases. India's component makers pursue a USD 100 billion export ambition, with steering wheel assemblies viewed as tariff-friendly volume cargo. ZF Rane's acquisition of TRW Sun Steering Wheels adds Gurugram and Pune plants, enhancing domestic content for localised airbags and sensors. Gulf states accelerate EV adoption for fleet decarbonisation, yet infrastructure gaps delay large-scale SbW rollout.

- Autoliv Inc.

- ZF Friedrichshafen AG

- Joyson Safety Systems

- Toyoda Gosei Co., Ltd.

- Valeo SA

- Nexteer Automotive Group

- Tokai Rika Co., Ltd.

- Hyundai Mobis Co., Ltd.

- JTEKT Corporation

- NSK Ltd.

- Mando Corporation

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- Thyssenkrupp AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Steer-By-Wire (SBW) Platforms

- 4.2.2 Mandatory Frontal-Airbag Integration In Steering Wheels

- 4.2.3 Light-Weighting Push From EV OEMs

- 4.2.4 Premiumisation and In-Cabin UX Upgrades

- 4.2.5 Legislative Drive-Impairment Monitoring Via Wheel Sensors

- 4.2.6 Demand For Stowable/Column-Less Cockpits In L3+ Vehicles

- 4.3 Market Restraints

- 4.3.1 Volatile Aluminium and Magnesium Prices

- 4.3.2 Global Sbw Homologation and Cybersecurity Compliance Lag

- 4.3.3 Chip-Level Shortages For Haptic/Driver-Sense Modules

- 4.3.4 Share-Shift Risk From Joystick/Voice HMI In Robo-Taxis

- 4.3.5 Chip-Level Shortages For Haptic/Driver-Sense Modules

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Technology

- 5.1.1 Conventional Column-Steer

- 5.1.2 Electric Power-Assist (EPS)

- 5.1.3 Steer-by-Wire (SbW)

- 5.2 By Material Type

- 5.2.1 Aluminium Rim

- 5.2.2 Magnesium Rim

- 5.2.3 Steel Rim

- 5.2.4 Natural-fibre Composite Rim

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Bus and Coahes

- 5.4 By Sales Channel

- 5.4.1 OEM Fitted

- 5.4.2 Aftermarket Replacement

- 5.5 By Propulsion Type

- 5.5.1 Internal-Combustion Engine

- 5.5.2 Battery-Electric Vehicle

- 5.5.3 Hybrid Electric Vehicle

- 5.5.4 Plug-In Hybrid Electric Vehicles

- 5.5.5 Fuel Cell Electric Vehicles

- 5.5.6 Alternative Fuels

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Philippines

- 5.6.4.6 Indonesia

- 5.6.4.7 Vietnam

- 5.6.4.8 Australia

- 5.6.4.9 New Zealand

- 5.6.4.10 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves & Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Autoliv Inc.

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 Joyson Safety Systems

- 6.4.4 Toyoda Gosei Co., Ltd.

- 6.4.5 Valeo SA

- 6.4.6 Nexteer Automotive Group

- 6.4.7 Tokai Rika Co., Ltd.

- 6.4.8 Hyundai Mobis Co., Ltd.

- 6.4.9 JTEKT Corporation

- 6.4.10 NSK Ltd.

- 6.4.11 Mando Corporation

- 6.4.12 Robert Bosch GmbH

- 6.4.13 Denso Corporation

- 6.4.14 Continental AG

- 6.4.15 Thyssenkrupp AG