|

시장보고서

상품코드

1848046

중국의 안과용 의료기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)China Ophthalmic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

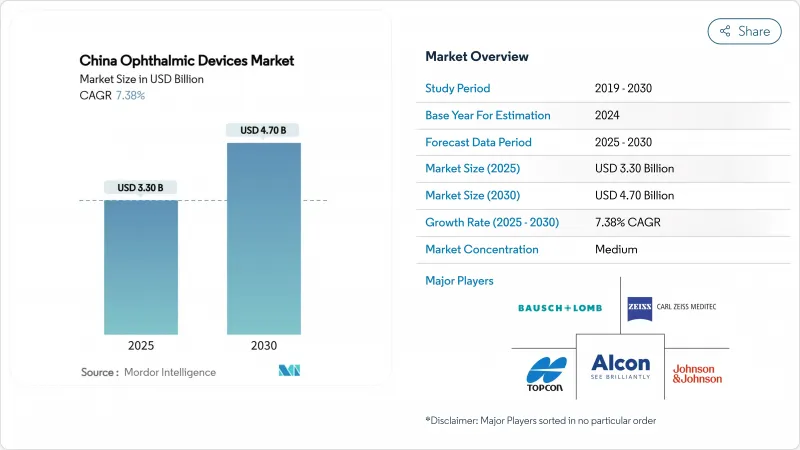

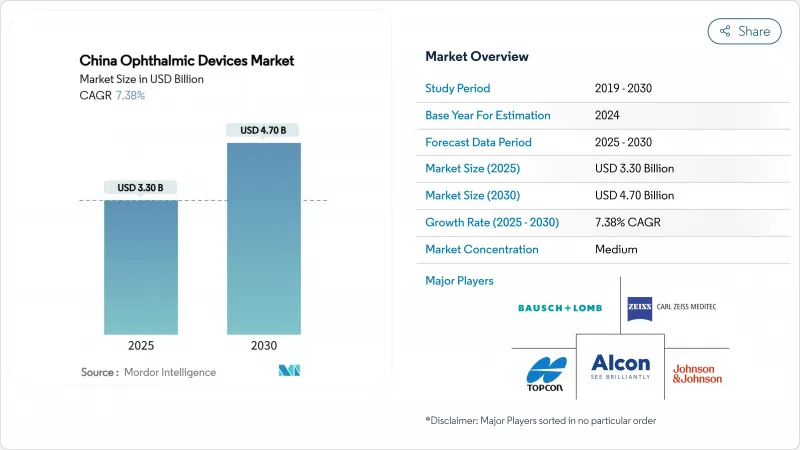

중국의 안과용 의료기기 시장 규모는 2025년에 33억 달러로 평가되었고, 2030년에 47억 달러에 이를 것으로 예측되며, 2025-2030년의 CAGR은 7.38%를 나타낼 전망입니다.

인구 고령화, 청소년 근시 급증, 국가 백내장 치료비 지원 프로그램으로 시술 건수가 증가하는 가운데, 정부 주도의 대량 구매 입찰을 통해 국내 개발 영상·수술·시력 관리 제품이 주류 조달 시장에 진입하고 있습니다. 관세 인상으로 수입 가격이 상승한 병원은 이제 글로벌 정확도 기준을 충족하는 중국산 프리미엄 레이저를 시험 도입하며 수입 대체를 가속화하고 공급원을 다각화하고 있습니다. 동시에 개인 안과 체인점들은 2선 및 3선 도시에 완비된 진단 기기 패키지를 공급하며 지리적 커버리지를 확대하고, 향후 10년간 중국의 안과용 의료기기 시장의 성장 모멘텀을 강화하고 있습니다.

중국의 안과용 의료기기 시장 동향 및 인사이트

급증하는 청소년 근시, 기기 수요 변화 주도

청소년 근시 증가로 가족 지출이 기본 안경에서 프리미엄 검진 및 치료로 전환되며 중국의 안과용 의료기기 시장 내 고마진 부문이 부상하고 있습니다. 국가의료제품감독관리국(NMPA) 승인 유수정체 안구내렌즈(IOL)로 이제 청소년 대상 수술적 교정이 가능해져 성인 전용 시술에서 도약한 증거다. 지역 클리닉들은 95% 이상의 진단 정확도를 가진 AI 안저 카메라를 도입하여 조기 발견을 가속화하고 수술 센터로의 환자 유입을 촉진하고 있습니다. 부모들은 축장 연장 억제를 약속하는 일회용 렌즈를 점점 더 선택하고 있어, 소매업체 수익을 증대시키고 치료 결과를 추적하는 축장 측정기의 수요를 지속시키고 있습니다. 진단 소프트웨어의 짧은 혁신 주기는 하드웨어 감가상각 전에 시스템 업그레이드를 촉진하여 반복 구매 행동을 강화하고 있습니다.

정부 주도로 백내장 수술 보험 적용 확대

국가 보험급여 확대로 5년간 백내장 수술 건수가 두 배 증가하며 점탄성제, 초음파 백내장 수술 핸드피스, 인공수정체 사용이 확대되었습니다. 예산 안정성으로 병원들은 노후 콘솔을 합병증 발생률을 낮추는 펨토초 플랫폼으로 교체하며, 보장된 수술 건수로 높은 자본 지출을 상쇄할 수 있다는 확신을 가지고 있습니다. 가격 상한선을 충족하는 국내 소모품을 선호하는 대량 구매 입찰은 중국의 안과용 의료기기 시장의 장기적 수익 동력을 공고히 합니다. 캡슐 절개술 부가 기기와 일회용 팩을 묶어 판매하는 공급업체들은 회전 시간 단축과 수술실 인력 효율화로 경쟁 우위를 확보합니다.

펠로우십 수료 안과 전문의 부족

내륙 현에서는 인구 대비 외과 의사 비율이 국가 목표에 미달하여 기기 가용성에도 불구하고 수술 처리량이 제한됩니다. 지방 보조금은 확인된 사례만 도시 병원으로 의뢰하는 AI 분류 키오스크를 지원하여 업무 부담을 완화하지만 복잡한 유리체망막 플랫폼 도입을 제약합니다. 교육 파트너십은 시뮬레이션 시스템 기증을 의무화하여 교육 센터의 자본 기기 판매를 촉진하지만, 중국의 안과용 의료기기 시장 성장을 저해하는 인력 병목 현상을 완전히 해소하지는 못합니다.

부문 분석

진단 및 모니터링 기기는 2024년 중국의 안과용 의료기기 시장 규모의 23.11%를 차지했으며, 2030년까지 연평균 복합 성장률(CAGR) 10.11%로 성장할 것으로 예상됩니다. 현지 공급업체들은 현재 군 병원에 설치된 OCT 워크스테이션의 절반 이상을 공급하고 있으며, 이는 기술자가 전문의 감독 없이도 즉시 의뢰 가능한 보고서를 제공할 수 있게 해주는 AI 모듈 덕분에 가능해졌습니다. 소프트웨어 출시 주기가 빨라지면서 시설들은 감가상각 일정보다 앞서 기기를 교체하게 되어 교체 수익이 증가하고 있습니다. 비전 케어는 전자상거래 보급의 혜택을 받는 일회용 실리콘 하이드로겔 렌즈에 힘입어 60.41%로 여전히 가장 큰 비중을 차지합니다. 수술용 기기는 16.6%를 차지하며, 백내장 렌즈 수요를 뒷받침하는 대량 입찰 보증의 혜택을 받고 있습니다. 한편 외래 진료 센터들은 수술실 시간을 최소화하기 위해 캡슐 절개술이 통합된 파코 콘솔을 구매하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중국 청소년층의 급속한 근시 증가

- 정부 주도에 의한 백내장 수술의 보험 적용 확대

- 2선 및 3선 도시에서의 개인 안과 체인점 투자 증가

- 연안 지방에서의 고령화에 수반하는 백내장 및 녹내장 발병률의 급증

- 지역 병원에서의 AI 대응 스크리닝 및 키오스크의 채택

- 혁신적 안과 임플란트에 대한 NMPA(국가약품감독관리국) 신속 승인

- 시장 성장 억제요인

- 중국 내륙 지역의 펠로우십 수료 안과 전문의 부족

- 고급 수술용 레이저에 대한 높은 수입 관세

- 가격에 민감한 공립 병원 조달 경매

- 비공식 유통 채널 내 위조 진단용 휴대기기

- 규제 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 기기 유형별

- 진단 및 모니터링 기기

- OCT 스캐너

- 안저 및 망막 카메라

- 오토레플렉터&케라토미터

- 각막 토포그래피 시스템

- 초음파 영상 시스템

- 페리미터 & 토노미터

- 기타 진단 및 모니터링 기기

- 수술용 기기

- 백내장 수술 기기

- 망막 유리체 수술 기기

- 망막 유리체 수술 기기

- 녹내장 수술용 기기

- 기타 수술기기

- 비전 케어 기기

- 안경 프레임 & 렌즈

- 콘택트렌즈

- 진단 및 모니터링 기기

- 질병별

- 백내장

- 녹내장

- 당뇨병 망막증

- 기타 질환

- 최종 사용자별

- 병원

- 안과 전문 클리닉

- 외래수술센터(ASC)

- 기타 최종 사용자

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Alcon Inc.

- Johnson & Johnson Vision Care Inc.

- Carl Zeiss Meditec AG

- Bausch Lomb Corp.

- HOYO Corporation

- Nidek Co., Ltd.

- Topcon Corp.

- Lumenis Be Ltd.

- Mindray Bio-Medical Electronics Co., Ltd.

- Shenzhen Certainn Technology Co., Ltd.

- Brighten Optix Corp.

- Shanghai Haohai Biological Technology Co., Ltd.

- Kanghua Ruiming Medical(VisionStar)

- OCULUS

제7장 시장 기회와 전망

HBR 25.11.10The China ophthalmic devices market size is USD 3.30 billion in 2025 and is on track to reach USD 4.70 billion by 2030, translating into a 7.38%CAGR over 2025-2030 for the China ophthalmic devices market.

Demographic ageing, a steep rise in juvenile myopia and a national cataract-reimbursement program are enlarging procedure volumes, while government-run bulk-buy auctions propel domestically engineered imaging, surgical and vision-care products into mainstream procurement. Hospitals facing tariff-inflated import prices now trial Chinese premium lasers that meet global accuracy thresholds, accelerating import substitution and diversifying supply. In parallel, private eye-care chains are equipping Tier-II and Tier-III cities with turnkey diagnostic suites, widening geographic coverage and reinforcing the China ophthalmic devices market's momentum through the decade.

China Ophthalmic Devices Market Trends and Insights

Rapid Urban Myopia Surge Transforms Device Demand

Escalating juvenile myopia has reoriented family spending from basic spectacles toward premium screening and treatment, lifting high-margin segments inside the China Ophthalmic Devices market. National-Medical-Products-Administration-cleared phakic intraocular lenses now extend surgical correction to teenagers, evidencing a leap from adult-only procedures. Community clinics deploy AI fundus cameras with >95% diagnostic accuracy, accelerating early detection and feeding referrals into surgical hubs. Parents increasingly choose daily disposable lenses promising axial-elongation control, boosting retailer revenue and sustaining demand for axial-length biometers that track therapy outcomes. Shorter innovation cycles in diagnostic software drive system upgrades ahead of hardware depreciation, reinforcing repeat-purchase behaviour.

Government-Led Cataract Surgery Reimbursement Expansion

National reimbursement doubled cataract surgeries in five years, elevating use of viscoelastics, phaco handpieces and intraocular lenses. Budget certainty prompts hospitals to replace aging consoles with femtosecond platforms that lower complication rates, confident that higher capital outlays are offset by guaranteed case volumes. Bulk-buy tenders favour domestic consumables meeting price ceilings, anchoring a long-run revenue engine for the China Ophthalmic Devices market. Suppliers bundling capsulotomy add-ons and single-use packs gain advantage by compressing turnover times and operating-room staffing.

Shortage of Fellowship-Trained Ophthalmic Surgeons

Surgeon-to-population ratios lag national targets in inland counties, capping surgical throughput despite equipment availability. Provincial grants subsidise AI-triage kiosks that refer only confirmed cases to city hospitals, easing workload but constraining adoption of complex vitreoretinal platforms. Training partnerships mandate donation of simulation systems, boosting capital equipment sales in teaching centres yet not fully eliminating the manpower bottleneck that tempers China Ophthalmic Devices market growth.

Other drivers and restraints analyzed in the detailed report include:

- Private Eye-Care Chain Investments in Tier-II & III Cities

- Ageing-Related Cataract & Glaucoma Incidence Spike

- High Import Tariffs on Premium Surgical Lasers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostic & Monitoring devices represented 23.11% of the 2024 China Ophthalmic Devices market size and are expected to compound at 10.11%CAGR to 2030. Local suppliers now install more than half of OCT workstations in county hospitals, buoyed by AI modules that allow technicians to deliver referral-ready reports without specialist oversight. Faster software release cycles persuade facilities to refresh equipment ahead of depreciation schedules, lifting replacement revenue. Vision Care remains the largest slice at 60.41%, driven by daily disposable silicone-hydrogel lenses that benefit from e-commerce penetration. Surgical devices contribute 16.6% and gain from bulk tender guarantees that underpin cataract lens offtake, while ambulatory centres purchase phaco consoles with integrated capsulotomy to minimize theatre time.

The China Ophthalmic Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices, Surgical Devices, and Vision Care Devices), Disease Indication (Cataract, Glaucoma, Diabetic Retinopathy, Other Disease Indications), End-User (Hospitals, Specialty Ophthalmic Clinics, and More. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alcon

- Johnson & Johnson

- Carl Zeiss

- Bausch + Lomb Corp.

- HOYO Corporation

- Nidek

- Topcon Corp.

- Lumenis

- Mindray Bio-Medical Electronics Co., Ltd.

- Shenzhen Certainn Technology Co., Ltd.

- Brighten Optix Corp.

- Shanghai Haohai Biological Technology Co., Ltd.

- Kanghua Ruiming Medical (VisionStar)

- Oculus

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Urban Myopia Surge among Chinese Youth

- 4.2.2 Government-led Cataract Surgery Reimbursement Expansion

- 4.2.3 Growing Private Eye-Care Chain Investments in Tier-II & III Cities

- 4.2.4 Aging-related Cataract & Glaucoma Incidence Spike in Coastal Provinces

- 4.2.5 AI-enabled Screening Kiosks Adoption by Community Hospitals

- 4.2.6 NMPA Fast-track Approvals for Innovative Ophthalmic Implants

- 4.3 Market Restraints

- 4.3.1 Shortage of Fellowship-trained Ophthalmic Surgeons in Inland China

- 4.3.2 High Import Tariffs on Premium Surgical Lasers

- 4.3.3 Price-sensitive Public Hospital Procurement Auctions

- 4.3.4 Counterfeit Diagnostic Hand-helds in Informal Distribution Channels

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 OCT Scanners

- 5.1.1.2 Fundus & Retinal Cameras

- 5.1.1.3 Autorefractors & Keratometers

- 5.1.1.4 Corneal Topography Systems

- 5.1.1.5 Ultrasound Imaging Systems

- 5.1.1.6 Perimeters & Tonometers

- 5.1.1.7 Other Diagnostic & Monitoring Devices

- 5.1.2 Surgical Devices

- 5.1.2.1 Cataract Surgical Devices

- 5.1.2.2 Vitreoretinal Surgical Devices

- 5.1.2.3 Refreactive Surgical Devices

- 5.1.2.4 Glaucoma Surgical Devices

- 5.1.2.5 Other Surgical Devices

- 5.1.3 Vision Care Devices

- 5.1.3.1 Spectacles Frames & Lenses

- 5.1.3.2 Contact Lenses

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Disease Indication

- 5.2.1 Cataract

- 5.2.2 Glaucoma

- 5.2.3 Diabetic Retinopathy

- 5.2.4 Other Disease Indications

- 5.3 By End-user

- 5.3.1 Hospitals

- 5.3.2 Specialty Ophthalmic Clinics

- 5.3.3 Ambulatory Surgery Centers (ASCs)

- 5.3.4 Other End-users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Alcon Inc.

- 6.3.2 Johnson & Johnson Vision Care Inc.

- 6.3.3 Carl Zeiss Meditec AG

- 6.3.4 Bausch + Lomb Corp.

- 6.3.5 HOYO Corporation

- 6.3.6 Nidek Co., Ltd.

- 6.3.7 Topcon Corp.

- 6.3.8 Lumenis Be Ltd.

- 6.3.9 Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.10 Shenzhen Certainn Technology Co., Ltd.

- 6.3.11 Brighten Optix Corp.

- 6.3.12 Shanghai Haohai Biological Technology Co., Ltd.

- 6.3.13 Kanghua Ruiming Medical (VisionStar)

- 6.3.14 OCULUS

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment