|

시장보고서

상품코드

1848051

수성 알키드 코팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Water-based Alkyd Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

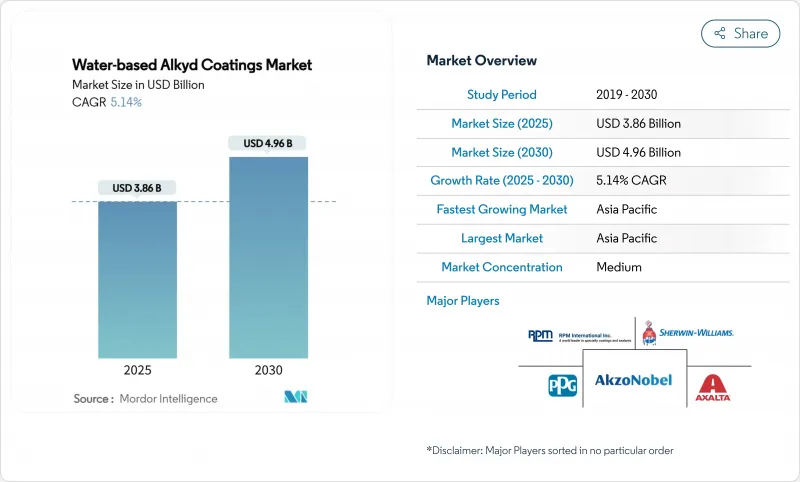

수성 알키드 코팅 시장 규모는 2025년에 38억 6,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 5.14%를 나타낼 것으로 예측되며, 2030년에 49억 6,000만 달러로 성장할 전망입니다.

강화된 환경 규정 준수, 회복세에 접어든 건설 부문, 꾸준한 제품 혁신이 이러한 성장을 뒷받침하고 있습니다. 제조업체들은 강화되는 글로벌 규제를 충족시키기 위해 저휘발성 유기화합물(VOC) 제형과 코발트 프리 건조 시스템에 주력하고 있습니다. 아시아태평양 지역은 가속화된 산업화와 용매 배출에 대한 정부의 단속으로 소비를 주도하고 있습니다. 북미와 유럽의 건축물 재도장 주기는 기본 수요를 유지하는 반면, 자동차 재도장 같은 고속 성장 틈새 시장은 공정 시간 단축과 에너지 비용 절감의 혜택을 누리고 있습니다. 전략적 통합과 수직적 통합으로 선도 브랜드들은 가격 결정력을 확보했으나, 바이오 기반 에멀젼은 차별화된 도전자들에게 기회를 열어주고 있습니다.

세계의 수성 알키드 코팅 시장 동향 및 인사이트

용매 기반 기술에서 수성 기술로의 전환

글로벌 규제 강화로 용매 시스템에서 수성 알키드로의 전환이 촉진되고 있습니다. 2018년 상하이의 용매 건축용 도료 사용 금지는 중국 건설업계 전반에 걸쳐 전국적 채택으로 이어져 원자재 흐름을 변화시키고 지역 공급망에 영향을 미쳤습니다. 미국 환경보호청(EPA)의 2025년 에어로졸 코팅 VOC 규정 개정안은 반응성이 낮은 원료 수요를 더욱 부추기고 있습니다. 퍼스토르프(Perstorp)와 같은 공급업체들은 경도나 광택을 희생하지 않으면서도 VOC 배출량을 거의 제로 수준으로 낮출 수 있는 차세대 유화제를 선보이고 있습니다. 기존 성능을 유지하면서 규제 준수를 동시에 달성하는 기업들은 선점자 프리미엄을 확보하고 고객 충성도를 강화할 수 있습니다.

건설 부문 회복 및 재도장 주기

노후 주택 재고와 DIY(직접 시공)의 경제성이 신규 건설 감소세를 상쇄하면서 주거용 재도장 시장은 여전히 탄탄한 모습을 보이고 있습니다. 셔윈-윌리엄스는 전문 계약업체 채널이 이미 미국 도료 판매량의 63%를 차지한다고 보고하며 전문 네트워크의 가치를 재확인했습니다. 아시아 페인트는 인도의 ‘모두를 위한 주택’ 정책 지원을 위해 48억 달러 규모의 프로그램으로 장식용 도료 생산 능력을 두 배 이상 확대했습니다. 이러한 패턴은 소폭의 GDP 성장만으로도 재도장 수요를 통해 꾸준한 판매량을 확보할 수 있어 경기 변동성을 완화할 수 있음을 보여줍니다.

용매 시스템 대비 긴 건조/경화 시간

습도가 높을수록 물의 증발이 느려져 공사 일정이 길어지고 인건비가 상승합니다. 폴린트의 속건성 DTM 알키드 에멀젼은 공정 주기를 단축하지만 여전히 최적화된 건조제 배합에 의존합니다. 제형 개발자들은 건조제 작용을 유지하면서 독성을 완화하기 위해 코발트 대체재 개발에 고심하고 있습니다. 성능 격차는 매년 좁혀지고 있으나, 적도 기후 지역의 계약자들은 외부 작업 시 여전히 용매 제형을 선호하는 경향이 있습니다.

부문 분석

건축용 도료는 2024년 수성 알키드 코팅 시장 규모의 46.51%를 차지했으며, 이는 주거용 실내 공간에서 지속되는 재도장 주기와 규제에 따른 수요를 반영합니다. 제형 개발자들은 거주 공간에 적합한 저취성 페인트와 50g/L까지 낮춘 VOC 제한을 제공합니다. Asian Paints 및 지역 경쟁사들이 주도하는 아시아 지역의 생산 능력 확장은 도시 주택 프로그램과 보조를 맞추고 있습니다. 비황변 마감재와 같은 내구성 개선은 비닐 아크릴 대비 가치 제안을 강화합니다.

자동차 재도장 부문은 2030년까지 6.56%의 가장 빠른 연평균 성장률(CAGR)을 기록할 전망입니다. AkzoNobel의 Sikkens Autowave Optima는 부스 에너지 소비를 60% 절감하고 도막 층수를 1.5회로 줄여 작업장 처리량을 향상시키고 탄소 집약도를 낮춥니다. 산업용 금속, 목재, 해양 틈새 시장은 유화 기술이 ISO 12944 부식 기준을 충족함에 따라 수성 알키드 코팅을 채택하고 있습니다. 가구 제조업체는 기업의 지속가능성 목표에 부합하는 바이오 기반 변형을 환영하는 반면, 기계 및 해양 코팅은 고급 차단 첨가제가 필요한 특수한 기회를 나타냅니다.

수성 알키드 코팅 보고서는 적용 분야(건축용, 보호/산업용 금속, 목재 마감 등), 최종 사용자 산업(건설 및 인프라, 산업용 OEM, 자동차 및 운송, 해양 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 세분화됩니다. 시장 전망은 가치(USD) 기준으로 제공됩니다.

지역별 분석

아시아태평양 지역은 2024년 글로벌 매출의 41.32%를 차지했으며, 2030년까지 연평균 5.68% 성장률을 기록할 전망입니다. 상하이 등 중국 도시의 용매 사용 금지 조치는 규정을 준수하는 수성 알키드 코팅으로의 전면적 전환을 촉진하고 있습니다. 납 함량을 90mg/kg으로 제한하는 국가 표준은 이러한 전환을 더욱 강화하여 국내 생산자에게 기술적 의무와 수출 경쟁력을 부여합니다. 견고한 건설 시장, 확대되는 자동차 보유량, 높아지는 소비자 인식이 다중 부문 수요를 견인하고 있습니다.

북미는 확립된 유통망과 엄격한 환경 규제로 강력한 입지를 유지하고 있습니다. 캘리포니아주의 50g/L 제한은 연구 개발을 촉진하는 한편, 전문 재도장 서비스가 판매량을 견인합니다. 미국 생산자들은 통제된 유통 채널과 사설 브랜드 계약을 활용해 마진을 최적화합니다. 자동차 재도장 분야의 신속한 채택은 차체 수리업체들이 공정 시간 단축 효과를 인식함에 따라 가속화되고 있습니다.

유럽은 바이오 기반 에멀젼과 코발트 프리 건조제의 조기 상용화를 통해 혁신 중심의 위치를 유지하고 있습니다. 성숙한 소비는 물량 성장을 완화하지만, 기존 건물 개조 및 에너지 효율 개선 공사가 꾸준한 수요를 유지합니다. EU 그린딜 인센티브는 공공 부문의 저휘발성 유기화합물(VOC) 도료 조달을 장려하여 규정을 준수하는 공급업체에게 우선 입찰 자격을 부여합니다.

남미는 도시 인프라 확장에 따라 점진적인 채택이 이루어지고 있으며, 특히 브라질의 월드컵 전 시설 리뉴얼이 두드러집니다. 규제 시행은 국가별로 차이가 있지만, 높아지는 건강 의식이 구매자들을 수성 시스템으로 유도하고 있습니다. 중동 및 아프리카는 부식 방지 기능과 규정 준수를 동시에 충족해야 하는 고급 상업용 및 석유·가스 인프라를 중심으로 초기 단계의 기회를 제공합니다. 가격 민감도와 극단적인 기후 조건이 전환 속도를 늦추고 있어, 습도에 최적화된 제형과 현지 혼합의 필요성이 부각되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 용매형에서 수성 기술로의 전환

- 건설 부문 회복 및 재도장 주기

- 세계 VOC 및 HAP 규제 강화

- 저취성 실내 페인트 선호도 증가

- 바이오 기반 알키드 에멀젼의 상업적 규모 달성

- 시장 성장 억제요인

- 용매 시스템 대비 긴 건조/경화 시간

- 신흥 경제국에서의 가격 민감성

- 습도 유발 내후성 한계

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 정도

제5장 시장 규모와 성장 예측

- 용도별

- 건축

- 보호 및 산업용 금속

- 목재 마감

- 자동차 보수

- 기타(선박, 기계)

- 최종 사용자 산업별

- 건설 및 인프라

- 산업용 OEM

- 자동차 및 운수

- 해양

- 가구 및 건구

- 기타

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)**/랭킹 분석

- 기업 프로파일

- Akzo Nobel NV

- Axalta Coating Systems, LLC

- Benjamin Moore & Co.

- Brillux GmbH & Co. KG

- Caparol Paints

- Cloverdale Paint Inc.

- Hempel A/S

- Jotun

- Kansai Paint Co.,Ltd.

- NATIONAL PAINTS FACTORIES CO. LTD.

- NIPSEA Group

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

- Tikkurila

제7장 시장 기회와 전망

HBR 25.11.10The Water-based Alkyd Coatings Market size is estimated at USD 3.86 billion in 2025, and is expected to reach USD 4.96 billion by 2030, at a CAGR of 5.14% during the forecast period (2025-2030).

Stronger environmental compliance rules, a recovering construction sector, and steady product innovation underpin this growth. Manufacturers focus on low-VOC formulations and cobalt-free drying systems to satisfy tightening global regulations. Asia-Pacific dominates consumption, helped by accelerated industrialization and government crackdowns on solvent emissions. Architectural repaint cycles in North America and Europe sustain baseline demand, while fast-growth niches such as automotive refinish benefit from shorter process times and lower energy costs. Strategic consolidation and vertical integration give leading brands pricing power, yet bio-based emulsions open doors for differentiated challengers.

Global Water-based Alkyd Coatings Market Trends and Insights

Shift from Solvent- to Water-based Technology

Global mandates catalyze the conversion from solvent systems to water-based alkyds. Shanghai's 2018 ban on solvent architectural paints triggered nationwide adoption across Chinese construction, altering raw-material flows and influencing regional supply chains. The U.S. EPA's 2025 update of aerosol-coating VOC rules further boosts demand for less reactive ingredients. Suppliers such as Perstorp showcase next-generation emulsifiers that allow near-zero VOC performance without sacrificing hardness or gloss. Firms able to balance compliance with legacy performance secure early mover premiums and strengthen customer loyalty.

Construction Sector Recovery and Repaint Cycles

Residential repainting remains resilient as aging housing stock and DIY affordability offset slower new builds. Sherwin-Williams reports that its pro-contractor channel already captures 63% of U.S. paint volumes, reinforcing the value of professional networks. Asian Paints more than doubled decorative capacity with a USD 4.8 billion program to serve India's Housing for All initiative. These patterns illustrate that even modest GDP growth can unlock steady volume through repaint demand, cushioning cyclicality.

Longer Drying/Curing Time vs. Solvent Systems

Water slows evaporation under high humidity, lengthening project schedules and raising labor costs. Fast-dry DTM alkyd emulsions from Polynt shorten cycles yet still depend on optimized drier blends. Formulators wrestle with cobalt-replacement to mitigate toxicity while preserving siccative action. Performance gaps narrow each year, but contractors in equatorial climates often default to solvent formulations for exterior work.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Global VOC and HAP Regulations

- Preference for Low-odor Indoor Paints

- Humidity-Driven Weatherability Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Architectural coatings generated 46.51% of the water-based alkyd coatings market size in 2024, reflecting sustained repaint cycles and regulation-driven demand in residential interiors. Formulators deliver low-odor paints suited to occupied spaces and VOC limits as low as 50 g/L. Asian capacity expansion, led by Asian Paints and regional peers, keeps pace with urban housing programs. Longevity improvements such as non-yellowing finishes strengthen value propositions versus vinyl acrylics.

The automotive refinish segment will post the fastest 6.56% CAGR through 2030. AkzoNobel's Sikkens Autowave Optima cuts booth energy 60% and reduces layers to 1.5, enhancing shop throughput and lowering carbon intensity. Industrial metal, wood, and marine niches adopt water-borne alkyds as emulsification technologies hit ISO 12944 corrosion benchmarks. Furniture makers welcome bio-based variants that align with corporate sustainability goals, while machinery and offshore coatings represent specialized opportunities requiring advanced barrier additives.

The Water-Based Alkyd Coatings Report is Segmented by Application (Architectural, Protective/Industrial Metal, Wood Finishes, and More), End-User Industry (Construction and Infrastructure, Industrial OEM, Automotive and Transportation, Marine and Offshore, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 41.32% of global revenue in 2024 and is set to advance at a 5.68% CAGR through 2030. China's solvent bans in cities such as Shanghai prompt wholesale migration to compliant water-based alkyds. National standards capping lead at 90 mg/kg further reinforce the shift, giving domestic producers technical mandates and export leverage. Robust construction, expanding automotive fleets, and rising consumer awareness anchor multi-segment demand.

North America maintains a strong position built on established distribution and stringent environmental codes. California's 50 g/L limit catalyzes research and development, while professional repaint services drive volume. U.S. producers leverage controlled channels and private-label contracts to optimize margins. Rapid adoption in automotive refinish accelerates as bodyshops realize cycle-time reduction.

Europe remains innovation-centric with early commercialization of bio-based emulsions and cobalt-free dryers. Mature consumption moderates volume growth, yet retrofitting of historical buildings and energy-efficient refurbishments sustain steady demand. EU Green Deal incentives encourage public-sector procurement of low-VOC coatings, giving compliant suppliers favored-bidder status.

South America witnesses incremental uptake as urban infrastructure expands, especially in Brazil's pre-World Cup facility renewals. Regulatory enforcement varies by country, but rising health awareness nudges buyers toward water-borne systems. Middle-East and Africa present early-stage opportunities centered on high-end commercial and oil-gas infrastructure needing corrosion-resistant yet compliant solutions. Price sensitivity and climate extremes temper speed of conversion, underlining the need for humidity-optimized formulations and local blending.

- Akzo Nobel N.V.

- Axalta Coating Systems, LLC

- Benjamin Moore & Co.

- Brillux GmbH & Co. KG

- Caparol Paints

- Cloverdale Paint Inc.

- Hempel A/S

- Jotun

- Kansai Paint Co.,Ltd.

- NATIONAL PAINTS FACTORIES CO. LTD.

- NIPSEA Group

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift from Solvent to Water-Based Technology

- 4.2.2 Construction Sector Recovery and Repaint Cycles

- 4.2.3 Tightening Global VOC and HAP Regulations

- 4.2.4 Preference for Low-Odor Indoor Paints

- 4.2.5 Bio-Based Alkyd Emulsions Reach Commercial Scale

- 4.3 Market Restraints

- 4.3.1 Longer Drying/Curing Time Vs. Solvent Systems

- 4.3.2 Price Sensitivity in Emerging Economies

- 4.3.3 Humidity-Driven Weatherability Limitations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Architectural

- 5.1.2 Protective/Industrial Metal

- 5.1.3 Wood Finishes

- 5.1.4 Automotive Refinish

- 5.1.5 Others (Marine, Machinery)

- 5.2 By End-User Industry

- 5.2.1 Construction and Infrastructure

- 5.2.2 Industrial OEM

- 5.2.3 Automotive and Transportation

- 5.2.4 Marine and Offshore

- 5.2.5 Furniture and Joinery

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Axalta Coating Systems, LLC

- 6.4.3 Benjamin Moore & Co.

- 6.4.4 Brillux GmbH & Co. KG

- 6.4.5 Caparol Paints

- 6.4.6 Cloverdale Paint Inc.

- 6.4.7 Hempel A/S

- 6.4.8 Jotun

- 6.4.9 Kansai Paint Co.,Ltd.

- 6.4.10 NATIONAL PAINTS FACTORIES CO. LTD.

- 6.4.11 NIPSEA Group

- 6.4.12 PPG Industries Inc.

- 6.4.13 RPM International Inc.

- 6.4.14 The Sherwin-Williams Company

- 6.4.15 Tikkurila