|

시장보고서

상품코드

1907267

독일의 수의 의료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Veterinary Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

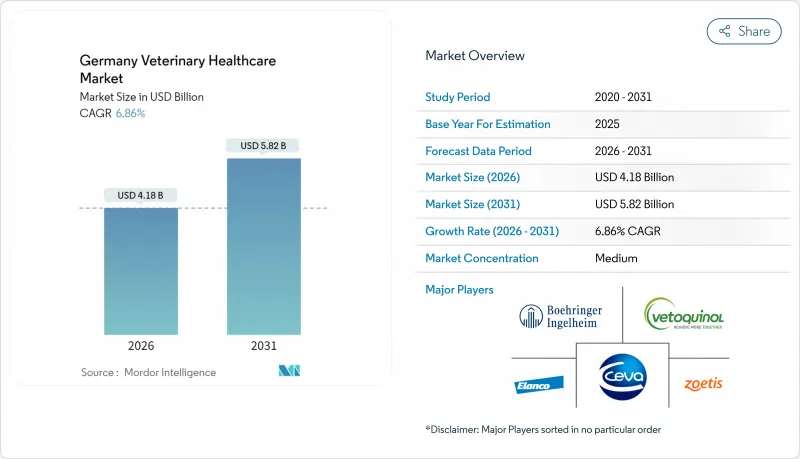

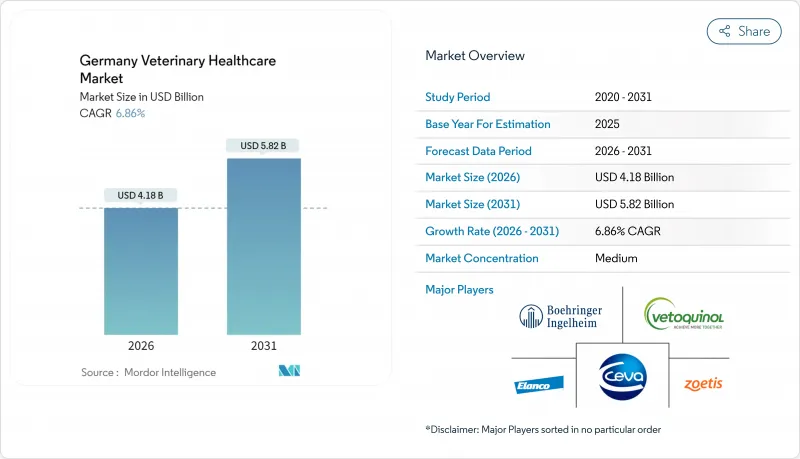

독일의 수의 의료 시장 규모는 2026년 41억 8,000만 달러로 평가되었고, 2025년 39억 1,000만 달러에서 성장할 것으로 예측됩니다.

2031년에는 58억 2,000만 달러에 이를 것으로 보이며, 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 6.86%로 성장할 전망입니다.

반려동물 소유의 안정적 증가, 가축 건강 관리 규제의 강화, 신속한 진단 기술 혁신이 이러한 성장을 뒷받침합니다. 3,390만 마리에 달하는 반려동물 인구는 지속적인 수요를 창출하며, 증가하는 인수공통전염병 위협과 1988년 이후 첫 국내 구제역 발생 사례는 강력한 예방 프로그램의 필요성을 강조합니다. 인공지능 기반 혈액 분석기 및 원격진료 플랫폼 같은 디지털 도구는 진료 효율성을 높이고 농촌 지역 서비스 공백을 메우는 데 기여합니다. 제조사 간 기업 통합은 제품 출시를 가속화하며, 반려동물 보험 가입률 증가는 고가 치료의 접근성을 확대합니다. 그러나 인력 부족과 의무적 요금 체계는 단기 성장 모멘텀을 제한합니다.

독일의 수의 의료 시장 동향과 전망

반려동물 인구 증가

반려동물 소유 증가가 지속적인 서비스 수요를 뒷받침하며, 2024년 독일 가구의 44%가 최소 한 마리의 동물을 기르고 있습니다. 세대 변화로 반려동물이 가족 구성원으로 자리매김하면서 고급 치료에 대한 지불 의사가 높아지고 있습니다. 도시 아파트에 거주하는 독신자 및 커플이 1인당 지출을 증가시키고 있으며, 자녀가 있는 가정의 팬데믹 이후 입양률이 장기적 성장을 견인하고 있습니다. 이러한 환경은 전문 클리닉, 종양학 서비스 및 영양 상담을 지속 가능하게 합니다.

인수공통전염병 발생률 증가

기후 변화와 국경 간 교역이 병원체 확산을 가속화합니다. 연간 최대 20만 명에게 영향을 미치는 라임병과 같은 매개체 전염 위협은 반려인들로 하여금 진드기 예방책으로 눈을 돌리게 합니다. 슈말렌베르크 바이러스 혈청 유병률은 2023년 40.15%로 급증하며 바이러스의 예측 불가능성을 부각시켰습니다. 2025년 1월 발굽구진병 발병은 신속한 차단 조치를 촉발했으며, 이는 단일 사건이 공급망 전반에 미치는 파급 효과를 보여줍니다. 따라서 강력한 감시 및 예방접종 프로그램이 우선순위로 부상합니다.

고급 수의학의 높은 비용

2022년 의무적 요금 조정으로 시술 비용이 약 50% 인상되어 품질 향상에도 불구하고 예산 부담이 가중되었습니다. 제한된 보험 적용 범위로 인해 소유주들은 수술 및 MRI 검사 비용을 자체 부담해야 하며, 때로는 치료를 연기하기도 합니다. 가축 생산자들은 프리미엄 백신과 낮은 마진을 저울질하며, 저소득 지역에서는 증가하는 학생 부채로 인해 동물병원 창업이 위축되어 접근성 격차가 지속되고 있습니다.

부문 분석

2025년 시점에서 치료제는 독일의 수의 의료 시장 규모에서 치료제 부문은 백신 및 구충제를 중심으로 61.78%를 차지했습니다. 마렉병 및 조류 인플루엔자 예방을 위한 가금류 백신 접종은 여전히 중요하며, 표적 구충제는 반려동물을 매개체 전염병으로부터 보호합니다. 항감염제는 판매량 감소에 직면했으나 최후의 수단으로 사용되는 고가 분자 약물의 프리미엄 가격 정책으로 혜택을 보고 있습니다. 의료용 사료 첨가제는 돼지와 육계에서 항생제 비의존적 성장 지원을 제공합니다.

진단 시장은 연평균 7.42% 성장률로 확장되며, 개 암종에서 BRAF 또는 KIT 돌연변이에 맞춘 치료법을 제시하는 분자 패널에서 가치를 창출합니다. 인공지능(AI) 지원 영상 기술은 방사선 촬영 처리량을 증가시키고, 현장 PCR 키트는 신속한 발병 억제 규정을 충족시킵니다. 규제 수요와 기술의 융합이 이 부문 성장을 가속화합니다.

개와 고양이는 2025년 독일 수의 의료 시장 점유율 46.02%를 유지하며, 높은 가구 보급률과 특수 종양학 또는 정형외과적 치료에 대한 지출 의지를 반영했습니다. 프레가발린 경구 용액과 같은 고양이 전용 불안 치료제는 연간 병원 방문률이 고양이의 40%에 불과한 치료 격차 해소를 목표로 합니다.

가금류 시장은 연평균 6.88% 성장률로 전망되며, 포괄적 백신 접종과 수질 관리가 필요한 고밀도 사육 환경에 대응합니다. H5N1 사태는 다가 백신 투자의 타당성을 입증했으며, 수출 기준 충족을 위한 PFAS 무첨가 사료 첨가제가 주목받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 동물 의료 분야의 혁신을 주도하는 첨단 기술

- 정부 차원의 인식 제고 및 정책 추진

- 인수공통전염병 유행 증가

- 시장 성장 억제요인

- 동물 실험 및 수의 서비스 비용 상승

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 제품별

- 치료제별

- 백신

- 구충제

- 항감염제

- 의료용 사료 첨가물

- 기타 치료제

- 진단 분야별

- 면역진단 검사

- 분자진단

- 진단 화상 검사

- 임상 화학

- 기타 진단

- 치료제별

- 동물 유형별

- 개와 고양이

- 말

- 반추동물

- 돼지

- 가금류

- 기타 동물

제6장 경쟁 구도

- 기업 프로파일

- Boehringer Ingelheim International GmbH

- Ceva Animal Health

- Elanco Animal Health

- Idexx Laboratories

- Merck & Co. Inc.

- Phibro Animal Health

- Vetoquinol

- Virbac SA

- Zoetis, Inc

제7장 시장 기회와 미래 동향

HBR 26.02.04Germany veterinary healthcare market size in 2026 is estimated at USD 4.18 billion, growing from 2025 value of USD 3.91 billion with 2031 projections showing USD 5.82 billion, growing at 6.86% CAGR over 2026-2031.

Steady companion-animal ownership, stricter livestock health mandates and rapid diagnostic innovation sustain this expansion. A pet population of 33.9 million animals underpins recurrent demand, while increasing zoonotic threats and the first domestic foot-and-mouth disease case since 1988 reinforce the need for robust preventive programs. Digital tools such as AI-powered hematology analyzers and teleconsultation platforms improve practice efficiency and support rural coverage gaps. Corporate consolidation among manufacturers accelerates product rollouts, and rising pet insurance uptake broadens affordability for higher-value care. However, workforce shortages and mandatory fee schedules temper near-term growth momentum.

Germany Veterinary Healthcare Market Trends and Insights

Growth in Companion Animal Population

Rising pet ownership supports continuous service demand as 44% of German households kept at least one animal in 2024. Generational shifts position pets as family members, prompting willingness to pay for advanced treatments. Singles and couples in urban apartments boost per-capita spending, and post-pandemic adoption rates among families with children anchor long-term growth. This environment sustains specialty clinics, oncology services and nutrition counseling.

Rise in Zoonotic Disease Incidence

Climate change and cross-border trade intensify pathogen spread. Vector-borne threats such as Lyme borreliosis, affecting up to 200,000 people yearly, push owners toward tick preventives. Schmallenberg seroprevalence jumped to 40.15% in 2023, underscoring viral unpredictability. The January 2025 foot-and-mouth outbreak triggered rapid containment, illustrating how one event reverberates across supply chains. Robust surveillance and vaccination programs therefore gain priority.

High Cost of Advanced Veterinary Care

Mandatory fee revisions raised procedure prices by roughly 50% in 2022, straining budgets despite quality benefits. Limited insurance penetration means owners self-finance surgeries and MRI scans, sometimes deferring care. Livestock producers weigh premium vaccines against thin margins, and escalating student debt discourages clinic startups in low-income districts, sustaining access disparities.

Other drivers and restraints analyzed in the detailed report include:

- Government Animal Health Initiatives

- Advancements in Veterinary Diagnostics and Telehealth

- Stringent Regulatory Approval Process

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutics contributed 61.78% of Germany veterinary healthcare market size in 2025, anchored by vaccines and parasiticides. Poultry immunizations against Marek's disease and avian influenza remain critical, and targeted antiparasitics protect companion animals from vector-borne diseases. Anti-infectives face volume curbs but benefit from premium pricing for last-resort molecules. Medical feed additives provide non-antibiotic growth support across swine and broilers.

Diagnostics, expanding at 7.42% CAGR, capture value from molecular panels that match therapies to BRAF or KIT mutations in canine cancers. AI-assisted imaging increases radiograph throughput, while on-farm PCR kits satisfy rapid outbreak containment rules. This convergence of regulatory demand and technology fuels segment acceleration.

Dogs and cats maintained 46.02% Germany veterinary healthcare market share in 2025, reflecting high household penetration and willingness to fund specialty oncology or orthopedic interventions. Feline-specific anxiety therapies such as pregabalin oral solutions intend to close the care gap where only 40% of cats visit clinics annually.

Poultry, forecast to grow at 6.88% CAGR, responds to dense production environments needing comprehensive vaccination and water-quality oversight. H5N1 events have validated investment in multivalent vaccines, and PFAS-free feed additives gain traction to meet export standards.

The Germany Veterinary Healthcare Market Report is Segmented by Product (Therapeutics, Diagnostics), Animal Type (Dogs & Cats, Horses, and More), Route of Administration (Oral, Parenteral, and More), End User (Veterinary Hospitals & Clinics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Boehringer Ingelheim

- Ceva

- Elanco

- IDEXX

- Merck

- Phibro Animal Health

- Vetoquinol

- Virbac

- Zoetis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advanced Technology Leading to Innovations in Animal Healthcare

- 4.2.2 Rising Awareness and Initiatives by the Government

- 4.2.3 Increasing Prevalence of Zoonotic Diseases

- 4.3 Market Restraints

- 4.3.1 Increasing Cost of Animal Testing and Veterinary Services

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value in USD million)

- 5.1 By Product

- 5.1.1 By Therapeutics

- 5.1.1.1 Vaccines

- 5.1.1.2 Parasiticides

- 5.1.1.3 Anti-infectives

- 5.1.1.4 Medical Feed Additives

- 5.1.1.5 Other Therapeutics

- 5.1.2 By Diagnostics

- 5.1.2.1 Immunodiagnostic Tests

- 5.1.2.2 Molecular Diagnostics

- 5.1.2.3 Diagnostic Imaging

- 5.1.2.4 Clinical Chemistry

- 5.1.2.5 Other Diagnostics

- 5.1.1 By Therapeutics

- 5.2 By Animal Type

- 5.2.1 Dogs and Cats

- 5.2.2 Horses

- 5.2.3 Ruminants

- 5.2.4 Swine

- 5.2.5 Poultry

- 5.2.6 Other Animals

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Boehringer Ingelheim International GmbH

- 6.1.2 Ceva Animal Health

- 6.1.3 Elanco Animal Health

- 6.1.4 Idexx Laboratories

- 6.1.5 Merck & Co. Inc.

- 6.1.6 Phibro Animal Health

- 6.1.7 Vetoquinol

- 6.1.8 Virbac SA

- 6.1.9 Zoetis, Inc