|

시장보고서

상품코드

1850043

문서 관리 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Document Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

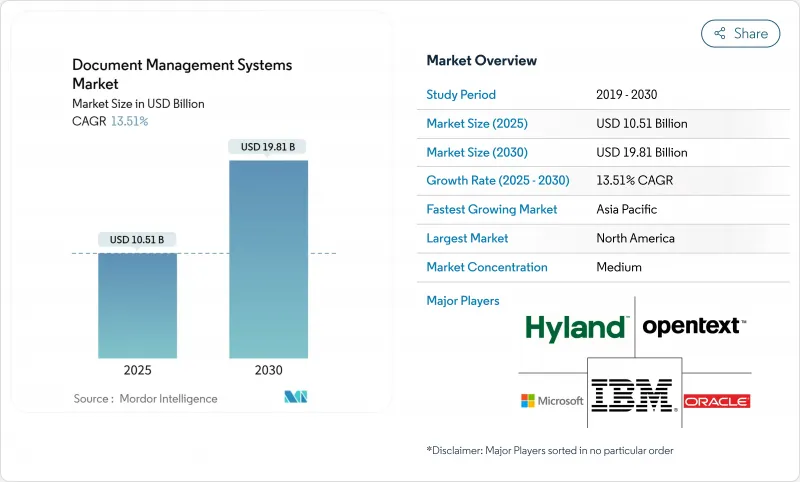

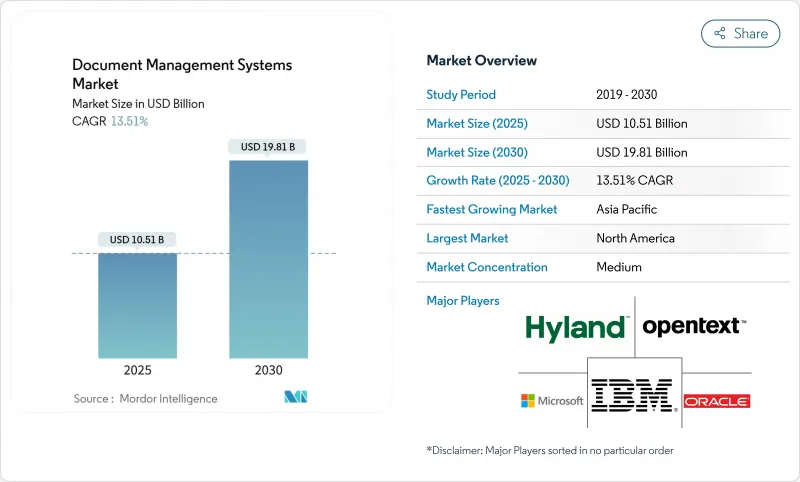

문서 관리 시스템 시장의 2025년 시장 규모는 105억 1,000만 달러로 평가되었고, 2030년에 198억 1,000만 달러에 이를 것으로 예측되며, 13.5%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

성장은 문서 중심 워크플로우를 디지털화하고, 확대되는 규정 준수 요구사항을 충족하는 검색 가능한 디지털 저장소로 종이 아카이브를 대체해야 하는 기업의 필요성에 기반합니다. 조직들은 정적 저장소를 비정형 파일에서 인사이트을 도출하는 지식 엔진으로 전환하기 위해 적극적으로 AI를 도입하며, 이는 측정 가능한 효율성 향상과 거버넌스 개선을 주도하고 있습니다. 문서 관리 시스템 시장은 클라우드 전환, 협업 도구와의 통합을 단순화하는 모듈형 플랫폼 설계, 신흥 데이터 주권 규정을 해결하는 지역별 맞춤형 솔루션의 등장으로 혜택을 보고 있습니다. 일상적인 비즈니스 애플리케이션 내에서 콘텐츠를 요약, 초안 작성, 전달할 수 있는 생성형 AI 코파일럿을 탑재하기 위한 벤더들의 경쟁이 치열해지면서 시장 경쟁 강도가 높아지고 있습니다.

세계의 문서 관리 시스템 시장 동향 및 인사이트

종이없는 프로세스로의 급속한 변화는 기업 채택 촉진

기업들은 운영 비용 절감과 ESG 목표 달성을 위해 종이 아카이브를 폐기하고 있으며, 다수는 디지털 우선 워크플로우를 중심으로 정책을 재조정하고 있습니다. 문서 관리 시스템 시장 솔루션 도입은 최대 30%의 운영 비용 절감과 50%에 가까운 처리 시간 개선을 실현하고 있습니다. 전자 문서 워크플로우를 도입한 병원들은 기록 처리 속도가 40-50% 빨라지고 HIPAA 규정 준수가 강화되었다고 보고합니다. 성공 사례는 도입의 선순환 구조를 강화하고 있습니다. 초기 투자 수익이 나타나면 경영진은 고객 서비스, 인사, 공급망 팀으로 신속하게 전개를 확대합니다. 이러한 확대된 적용 범위는 문서 관리 시스템 시장의 지속적인 성장 동력을 뒷받침합니다.

통합 역량을 재정의하는 클라우드 네이티브 DMS 플랫폼

클라우드 협업 제품군 내 문서 기능의 내재화는 구매자의 기대를 재편하고 있습니다. 마이크로소프트는 2025년 3분기 100조 개 이상의 AI 토큰을 처리했으며, 클라우드 서비스 매출은 22% 증가한 424억 달러를 기록하며 통합 플랫폼에 대한 수요를 입증했습니다. 기업들은 통합 인증 하에 콘텐츠 생성, 저장, 거버넌스를 결합한 친숙한 인터페이스를 선호하며, 기존 벤더들에게 상호운용성 심화를 요구하고 있습니다. 이 추세는 원활한 크로스 디바이스 접근이 필수인 원격 및 하이브리드 업무 환경에서 특히 강력합니다. 결과적으로 문서 관리 시스템 시장은 독립형 기능 체크리스트보다 즉시 통합이 가능한 벤더 쪽으로 기울고 있습니다.

지속적인 사용자 저항이 도입 성공을 방해

명확한 투자 수익률(ROI)에도 불구하고, 기존 백오피스 팀은 새로운 워크플로우를 방해 요소로 보는 경우가 많습니다. 조직의 70%가 사용자 저항을 전개 지연의 주요 요인으로 꼽습니다. 특히 감사 추적이 핵심인 의료 및 금융 분야에서 회의론이 두드러집니다. 교육 투자와 변화 관리 로드맵은 기술적 출시보다 자주 지연되어 투자 회수 기간을 늘리고 문서 관리 시스템 시장의 잠재력을 저해합니다. 그러나 전용 도입 프로그램을 운영하는 기업들은 사용자 만족도가 62% 높고 가치 실현 속도가 41% 빠른 것으로 나타나, 기능성만큼 문화적 정렬이 중요함을 보여줍니다.

부문 분석

구현 복잡성이 전문 서비스 및 관리형 서비스 지출을 증가시키고 있습니다. 2024년 문서 관리 시스템 시장에서 소프트웨어가 76%를 차지했지만, 기업들이 ERP, CRM 및 산업별 플랫폼과의 맞춤형 통합을 추구함에 따라 2025년부터 2030년까지 서비스 매출은 연평균 18.9% 성장할 전망입니다. 서비스 부문 문서 관리 시스템 시장 규모는 지속적인 최적화 계약 및 규정 준수 감사 수요 증가를 반영하여 다른 컴포넌트보다 빠르게 확장될 것으로 예상됩니다. 공급업체들은 AI 모델 튜닝 및 메타데이터 전략과 연계된 자문 계약이 현재 가장 수익성이 높은 서비스 라인이라고 보고합니다.

이러한 변화는 성공이 단순한 라이선싱이 아닌 프로세스 재설계에 달려 있음을 강조합니다. 컨설팅 팀은 사용자 수용성 파일럿을 기획하고, 템플릿을 구축하며, 규제 기관을 만족시키는 보존 정책을 수립합니다. 개인정보 보호법이 확산됨에 따라 거버넌스 중심 컨설팅 수요가 증가하고 있습니다. 결과적으로, 수직적 노하우를 보유한 시스템 통합업체들이 문서 관리 시스템 시장 내 전체 프로젝트 예산에서 더 큰 비중을 차지하고 있습니다.

문서 관리 시스템 시장은 컴포넌트별(소프트웨어 및 서비스), 전개별(클라우드 및), 최종 사용자 산업별(은행 및 금융 서비스, 제조업 및 건설업 등), 지역별로 세분화되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 2024년 글로벌 매출의 35%를 유지했으며, 이는 초기 클라우드 전환과 세분화된 감사 추적을 의무화하는 성숙한 규제 프레임워크에 기반합니다. 금융 서비스 및 의료 구매자가 지역 지출을 주도하며, 고급 AI 모듈을 통합해 비정형 데이터 인사이트를 확보하고 있습니다. 마이크로소프트, IBM, 어도비 등 주요 벤더들은 기존 기업 라이선스를 활용해 문서 관리 모듈을 확장함으로써 지역적 규모 이점을 강화하고 있습니다. 종이 없는 조달을 장려하는 정부 인센티브는 지출을 더욱 촉진하여, 문서 관리 시스템 시장이 미국과 캐나다 전역의 광범위한 디지털 전환 로드맵의 핵심 축으로 유지되도록 합니다.

아시아태평양 지역은 2025-2030년 동안 15.8%의 연평균 성장률(CAGR)이 예상되는 가장 빠르게 성장하는 지역입니다. 인도, 중국, 한국의 정책 주도 디지털화 프로그램은 공공 및 민간 부문 전반에 걸쳐 채택을 가속화하고 있습니다. 인도의 DPDP법은 은행과 보험사가 지오펜싱 저장 노드를 도입하도록 촉진하고 있으며, 중국 기업들은 사이버보안법 요건을 충족하기 위해 국내 공급업체를 선택하는 경우가 많다. 일본은 제조업체들이 DMS를 린 생산 시스템에 통합하는 등 강력한 도입세를 보이고 있습니다. 하이퍼스케일 클라우드 제공업체들은 지역 데이터 센터를 확장하며, 한때 국경 간 전개를 지연시켰던 데이터 거주지 문제를 해결하고 문서 관리 시스템 시장이 아시아태평양 전역의 현대화 기업들을 포착하도록 지원하고 있습니다.

유럽 시장은 GDPR과 국가별 개인정보 보호법이 주도하며, 규정 준수 기능이 핵심 구매 기준으로 작용합니다. 영국과 독일이 도입 규모에서 선두를 달리며 통제된 기록 관리와 보존 자동화를 중시합니다. 기업들은 콘텐츠가 지정된 EU 구역을 절대 벗어나지 않도록 보장하는 플랫폼을 선호하여, 주권적 자격을 갖춘 유럽 공급업체에 대한 수요를 촉진합니다. 지속가능성 이니셔티브는 종이 사용 감축 목표를 장려하여 프로젝트를 더욱 부추긴다. 남유럽의 도입은 증가하고 있지만, 다중 이해관계자 승인으로 인해 조달 주기는 더 길어지고 있습니다. 전반적으로, 데이터 거버넌스의 엄격함은 유럽을 글로벌 문서 관리 시스템 시장 내에서 프라이버시 우선 기능의 선두 주자로 자리매김하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 종이 없는 프로세스로의 급속한 전환(기업 비용 및 ESG 의무)

- 협업 제품군에 통합된 클라우드 네이티브 DMS 플랫폼

- AI 강화 검색과 자동 분류의 정밀도가 비약적으로 향상(>95%)

- 엄격한 데이터 주권 규정(EU GDPR, 인도 DPDP)으로 인한 규정 준수형 DMS 도입 촉진

- 산업별 맞춤형 템플릿(의료, 법률, AEC) 확산으로 인한 전개 주기 단축

- 생성형 AI 코파일럿을 통한 컨텍스트 기반 콘텐츠 워크플로 활성화

- 시장 성장 억제요인

- 규제 대상 백오피스 기능에서 지속적인 사용자 변화 저항

- 부실한 메타데이터 관리로 인한 높은 전자 증거개시 비용

- DMS 중심 랜섬웨어 사건 이후 상승하는 사이버 보험료

- 기존 ECM 시스템 이주를 지연시키는 벤더 종속성 우려(보고 부족)

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 가격 분석

- 업계 생태계 분석

- 거시 경제 영향 평가

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 소프트웨어

- 서비스

- 전개별

- 클라우드

- 온프레미스

- 최종 사용자 업계별

- 은행 및 금융 서비스

- 제조업과 건설업

- 교육

- 헬스케어

- 소매

- 법무

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Microsoft Corp.

- OpenText Corp.

- IBM Corp.

- Hyland Software Inc.

- Oracle Corp.

- Box Inc.

- Adobe Inc.

- Laserfiche

- M-Files Corp.

- Alfresco(-Hyland)

- Dropbox Business

- Zoho Corp.

- DocStar(Epicor)

- AODocs

- LogicalDOC Srl

- Agiloft Inc.

- Synergis Technologies

- Everteam

- FileHold Systems

- PaperSave

제7장 시장 기회와 장래의 전망

HBR 25.11.14The document management systems market is valued at USD 10.51 billion in 2025 and is forecast to reach USD 19.81 billion by 2030, advancing at a 13.5% CAGR throughout the period.

Growth rests on the enterprise need to digitize document-centric workflows and replace paper archives with searchable digital repositories that satisfy expanding compliance mandates. Organizations are aggressively embedding AI to turn static repositories into knowledge engines that surface insights from unstructured files, driving measurable efficiency gains and improved governance. The document management systems market is also benefitting from cloud migration, modular platform designs that simplify integration with collaboration tools, and region-specific offerings that address emerging data-sovereignty rules. Competitive intensity is rising as vendors race to embed generative AI copilots able to summarize, draft, and route content inside everyday business applications.

Global Document Management Systems Market Trends and Insights

Rapid Shift Toward Paper-Free Processes Driving Enterprise Adoption

Organizations are discarding paper archives to reduce operating costs and meet ESG targets, and many are realigning policies around digital-first workflows. Implementations of document management systems market solutions are delivering operating-cost reductions up to 30% and processing-time improvements near 50%. Hospitals that introduce electronic document workflows report 40-50% faster record handling and tighter HIPAA compliance. Success stories are reinforcing an adoption flywheel: once early ROI appears, executives rapidly extend deployments across customer-service, HR, and supply-chain teams. This widening footprint underpins the sustained momentum of the document management systems market.

Cloud-Native DMS Platforms Redefining Integration Capabilities

The embedding of document functionality inside cloud collaboration suites is reshaping buyer expectations. Microsoft processed more than 100 trillion AI tokens in Q3 2025, and revenue from cloud services jumped 22% to USD 42.4 billion, underscoring demand for integrated platforms. Enterprises prefer familiar interfaces that blend content creation, storage, and governance under unified authentication, pressuring legacy vendors to deepen interoperability. The trend is especially powerful within remote and hybrid workplaces, where seamless cross-device access is non-negotiable. Consequently, the document management systems market is tilting toward vendors capable of drop-in integrations rather than standalone feature checklists.

Persistent User Resistance Hampering Implementation Success

Despite clear ROI, entrenched back-office teams often view new workflows as disruptive. Seventy percent of organizations cite user resistance as the key factor behind delayed deployments. Skepticism is especially acute in healthcare and finance where audit trails are mission critical. Training investments and change-management roadmaps frequently lag technical rollout, stretching payback periods and muting the full potential of the document management systems market. Enterprises with dedicated adoption programs, however, record 62% higher user satisfaction and 41% faster value realization, illustrating that cultural alignment is as important as functionality.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enhanced Search Transforming Information Retrieval

- Data Sovereignty Regulations Reshaping Implementation Strategies

- Industry-Specific Templates Shorten Deployment Cycles

- Generative-AI Copilots Unlock "Content-in-Context" Workflows

- Vendor Lock-In Concerns Creating Implementation Hesitancy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Implementation complexity is tilting spending toward professional and managed services. Although software captured 76% of the document management systems market in 2024, services revenue is rising at an 18.9% CAGR from 2025-2030 as enterprises seek customized integrations with ERP, CRM, and industry-specific platforms. The document management systems market size for services is forecast to expand faster than any other component category, reflecting growing demand for continuous optimization contracts and compliance audits. Vendors report that advisory engagements tied to AI model tuning and metadata strategy are now the most profitable service lines.

The shift also underscores how success hinges on process re-engineering rather than licensing alone. Consulting teams orchestrate user-acceptance pilots, build templates, and craft retention policies that satisfy regulators. Demand for governance-centric consulting is climbing as privacy laws proliferate. Consequently, system integrators with vertical know-how are capturing a larger portion of overall project budgets within the document management systems market.

Document Management System Market Segmented by Component (Software and Services), Deployment (Cloud and ), End-User Industry (Banking and Financial Services, Manufacturing and Construction and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 35% of global revenue in 2024, anchored by early cloud migration and mature regulatory frameworks that mandate granular audit trails. Financial services and healthcare buyers dominate regional spending, integrating advanced AI modules to unlock unstructured insights. Leading vendors such as Microsoft, IBM, and Adobe leverage existing enterprise licenses to expand document management modules, reinforcing regional scale advantages. Government incentives that reward paper-free procurement further stimulate spending, ensuring the document management systems market remains a core pillar of broader digital-transformation roadmaps across the United States and Canada.

Asia-Pacific is the fastest growing geography with a 15.8% CAGR projected for 2025-2030. Policy-driven digitization programs in India, China, and South Korea are accelerating adoption across public and private sectors. India's DPDP Act is prompting banks and insurers to implement geo-fenced storage nodes, while Chinese firms often select domestic vendors to satisfy cybersecurity law requirements. Japan shows robust uptake among manufacturers embedding DMS in lean production systems. Hyperscale cloud providers are expanding regional data centers, addressing residency concerns that once slowed cross-border deployments and helping the document management systems market capture modernizing enterprises throughout APAC.

Europe's market is shaped by GDPR and country-specific privacy laws, making compliance functionality a critical purchase filter. The United Kingdom and Germany lead in volume, emphasizing controlled records-management and retention automation. Organizations favour platforms guaranteeing that content never leaves designated EU zones, boosting demand for European vendors with sovereignty credentials. Sustainability initiatives promote paper-reduction targets, further fuelling projects. Southern European adoption is rising, yet procurement cycles are lengthier due to multi-stakeholder approvals. Overall, data governance stringency positions Europe as a bellwether for privacy-first capabilities within the global document management systems market.

- Microsoft Corp.

- OpenText Corp.

- IBM Corp.

- Hyland Software Inc.

- Oracle Corp.

- Box Inc.

- Adobe Inc.

- Laserfiche

- M-Files Corp.

- Alfresco (-Hyland)

- Dropbox Business

- Zoho Corp.

- DocStar (Epicor)

- AODocs

- LogicalDOC Srl

- Agiloft Inc.

- Synergis Technologies

- Everteam

- FileHold Systems

- PaperSave

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift toward paper-free processes (enterprise cost and ESG mandates)

- 4.2.2 Cloud-native DMS platforms bundled inside collaboration suites

- 4.2.3 Surge in AI-enhanced search and auto-classification accuracy (>95 %)

- 4.2.4 Strict data-sovereignty rules (EU GDPR, India DPDP) triggering compliant DMS roll-outs

- 4.2.5 Rise of industry-specific templates (health, legal, AEC) shortening deployment cycles

- 4.2.6 Generative-AI copilots unlocking content-in-context workflows (under-reported)

- 4.3 Market Restraints

- 4.3.1 Persistent user-change resistance in regulated back-office functions

- 4.3.2 High e-discovery costs from poor metadata hygiene

- 4.3.3 Cyber-insurance premiums rising after DMS-centred ransomware events (under-reported)

- 4.3.4 Vendor lock-in concerns slowing migration from legacy ECMs (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Industry Ecosystem Analysis

- 4.10 Macroeconomic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By End-User Industry

- 5.3.1 Banking and Financial Services

- 5.3.2 Manufacturing and Construction

- 5.3.3 Education

- 5.3.4 Healthcare

- 5.3.5 Retail

- 5.3.6 Legal

- 5.3.7 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Israel

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 United Arab Emirates

- 5.4.5.1.4 Turkey

- 5.4.5.1.5 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corp.

- 6.4.2 OpenText Corp.

- 6.4.3 IBM Corp.

- 6.4.4 Hyland Software Inc.

- 6.4.5 Oracle Corp.

- 6.4.6 Box Inc.

- 6.4.7 Adobe Inc.

- 6.4.8 Laserfiche

- 6.4.9 M-Files Corp.

- 6.4.10 Alfresco (-Hyland)

- 6.4.11 Dropbox Business

- 6.4.12 Zoho Corp.

- 6.4.13 DocStar (Epicor)

- 6.4.14 AODocs

- 6.4.15 LogicalDOC Srl

- 6.4.16 Agiloft Inc.

- 6.4.17 Synergis Technologies

- 6.4.18 Everteam

- 6.4.19 FileHold Systems

- 6.4.20 PaperSave

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment