|

시장보고서

상품코드

1850124

미국의 플라스틱 포장 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)US Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

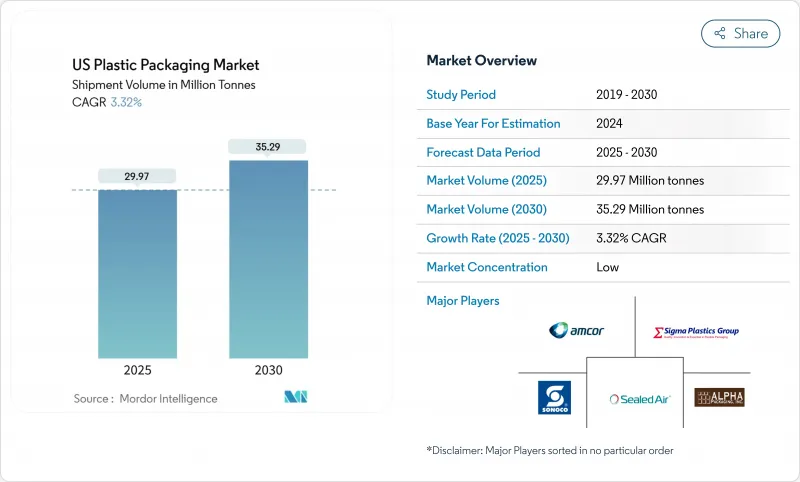

미국의 플라스틱 포장 시장 규모는 2025년에는 2,997만 톤, 2030년에는 3,529만 톤에 달하고, CAGR은 3.32%를 나타낼 전망입니다.

수요의 회복력은 E-Commerce 소포의 확대, 식음료의 편의 형식, 소비자 재생(PCR) 수지를 25% 핵심 재고 유닛에 통합한다는 브랜드 오너의 헌신에 의합니다. 캘리포니아 주 SB 54 및 워싱턴 주 재생 자원 이용법과 같은 규제 프레임 워크는 가벼운 게이지, 단일 소재 라미네이트 및 테더 클로저로의 설계 이동을 가속화하고 있습니다. FDA 인가의 rPET, rHDPE, rLLDPE를 채택함으로써 공급 스톡의 격차가 줄어들기 시작하고 있습니다. 또한 2023년에 플라스틱 성형업체가 새롭게 도입하는 1,646대의 로봇 도입으로 미국의 플라스틱 포장 시장에서는 처리량이 합리화되어 품질 수율이 향상되고 있습니다.

미국의 플라스틱 포장 시장 동향과 통찰

미국 CPG 브랜드에 의한 재활용 가능한 단일 소재 파우치의 신속한 채택

폴리에틸렌과 폴리프로필렌의 단일 소재 라미네이트는 한때 재활용을 방해했던 혼합 기재 필름을 대체합니다. 컨버터는 현재 미국 플라스틱 협정 2025의 설계 목표에 준거한 내열성 하이베리어 파우치를 제공해, 브랜드 오너에게 「리사이클 대응」의 캐치 불평을 스트레이트에 전하고 있습니다. DNP 인도네시아가 스낵과 반려동물 먹이의 단소재 팩을 상업 전개하는 것으로, 배리어 성능을 유지하면서 사용후 처리를 간소화할 수 있음을 실증하고 있습니다. 소매업체는 종래의 호일 구조와의 사양의 동등성을 요구하고 있어, 시험 데이터에서는 동등한 산소 투과율이 확인되고 있어 폭넓은 SKU 전환이 가능합니다. 미국 플라스틱 포장 시장의 패키징 팀은 단위당 필름 소비를 줄이기 위해 롤 스톡 폭 최적화와 재료 다운 가우징을 동기화합니다.

미국 소포 네트워크에서 경량 보호 메일러에 대한 전자상거래 수요 급증

소포 운송인은 불필요한 공동 충전을 계속 제거하고 제품 무결성을 유지하면서 치수 중량 요금을 줄이는 얇은 게이지의 커브 사이드 재활용 가능한 메일러에 대한 관심을 높입니다. 아마존은 미국용 소포의 3분의 1을 종이 기반 대체품으로 옮기고, 프로그램 시작 이후 150억개의 플라스틱 에어 베개를 줄였습니다. 이 회사의 파일럿 공장은 분당 250개가 넘는 라인 속도를 검증하고 자동화의 새로운 벤치마크를 설정합니다. 경쟁업체는 워싱턴주에서의 재생 이용법에서 의무화된 PCR을 30% 포함하는 단일 소재의 LDPE 버블 메일러의 성능에 필적합니다. 미국의 플라스틱 포장 시장에 진입한 컨버터는 매일 소포량의 급증에 대응하기 위해 고출력의 블로우 필름 타워와 자동 위케팅에 투자하고 있습니다.

특정 포장 형태를 줄이는 주 수준의 단일 사용 플라스틱 금지 조치 확대

캘리포니아의 SB54는 2032년까지 주 내에서 판매되는 버진 플라스틱 포장의 25% 절감을 의무화하고, 생산자는 2025년까지 생산자 책임 단체에 가입해야 한다고 합니다. 뉴저지, 콜로라도, 메인 주에서도 유사한 지침이 내려져 전국 브랜드에 대한 복잡한 컴플라이언스 맵이 단편화되었습니다. 컨버터 각 회사는 카탈로그에서 PS 크럼 쉘과 PVC 블리스터를 선점하여 폐지하고 원가가 오더라도 PET G와 코트 마분지의 대체품으로 전환하고 있습니다. 규제 불확실성은 장기 공급 계약에 리스크 프리미엄을 통합하고 기업이 연방 정부 지침의 조화를 기다리는 동안 미국의 플라스틱 포장 시장에서 재량적 자본 지출을 억제합니다.

부문 분석

유연한 형식은 2024년 미국 플라스틱 포장 시장 점유율의 54.14%를 차지했으며 CAGR 4.98%로 성장하고 있습니다. 각 신규 파우치는 60-70% 적은 폴리머로 경질 파우치를 대체하여 화물 배출량과 창고 실적을 줄입니다. 전자상거래는 골판지 상자의 1/10 입방체로 접히는 플랫 메일러를 선호하고 사용하여 보관 오버헤드를 줄입니다. 브랜드는 현재 근적외선(NIR) 판독 가능 잉크를 채택하고 있으며, 유연성은 재료 회수 시설에서 효율적으로 분리되어 실질적인 재활용률이 향상되었습니다. 한편, "스마트"파우치에는 RFID나 NFC 태그가 내장되어 충전으로부터 소비자의 스캔 이벤트까지, 엔드 투 엔드로 가시화할 수 있게 되어 있습니다.

경질 플라스틱은 음료, 의약품, 가정용 화학제품에서 여전히 중요한 역할을 하고 있지만, CAGR 2.1%로 성장은 늦어지고 있습니다. 경량 HDPE 병은 2023년의 설계보다 수지 사용량이 최대 12% 삭감되지만, 낙하 강도와 미각 중립에 관한 성능의 임계치에 의해 추가적인 다운가우징은 제한됩니다. 워싱턴주의 재활용 함량에 관한 법률은 병 제조업체에게 안정적인 rHDPE 스트림을 확보하도록 의무화하고 있으며, 내부 세척 라인에 공동 투자를 촉구하고 있습니다. 미국의 플라스틱 포장 시장의 경쟁은 편의성과 쓰레기 감소를 융합시키고, 가까이 의무화되는 폐쇄 유지 의무를 준수하는 끈이 달린 캡을 중심으로 전개되고 있습니다.

폴리에틸렌은 2024년 플렉서블 용기의 수량 점유율로 45.54%를 유지하며, 광범위한 가공창과 강력한 커브사이드 회수 인프라에 지원되고 있습니다. FDA가 스낵 과자 포장재에 rLLDPE를 100% 사용하는 것을 승인함으로써 식품안전 준수의 길을 확인하여 전국 규모의 소매업체가 '순환형' 프라이빗 라벨을 출시할 수 있게 되었습니다. 개발팀이 메탈로센 촉매를 채택하는 것으로, 보다 작은 게이지로 보다 높은 다트 임팩트를 실현해, 8-10%의 수지 절약에 기여합니다. 공압출 기술이 필름의 투명성을 손상시키지 않고 재활용 펠릿의 변동에 대응할 수 있게 되어, 미국의 PE 기반의 플렉서블 플라스틱 포장 시장 규모는 계속 확대되고 있습니다.

기타 소재' 카테고리는 퇴비화 가능한 PLA 블렌드, 셀룰로오스 기반 필름, 산화규소 코팅지가 뒷받침하여 CAGR 6.34%의 성장을 이룹니다. 소비자 브랜드는 사탕수수 유래의 바이오 PE를 시용하고 있어, 동등한 기계적 특성과 저탄소 실적를 실현하고 있습니다. BOPP는 광택 있는 간식과 과자의 겹침에 여전히 필수적이지만, 새로운 바니시 시스템은 모노 머티리얼 재활용 지침을 따라 금속화되지 않은 장벽 성능을 제공합니다. 수지 공급업체와 필름 컨버터 간의 파트너십은 적격성 확인 사이클을 가속화하고 새로운 블렌드 시장 출시 시간을 단축합니다.

미국의 플라스틱 포장 시장은 재료 유형별로 구분된다(경질 플라스틱(폴리에틸렌(PE), 폴리프로필렌(PP), 기타). 연질 플라스틱(폴리에틸렌(PE), 2축 연신 폴리프로필렌(BOPP), 기타)), 포장 유형(경질 플라스틱 포장, 연질 플라스틱 포장), 최종 이용 산업(식품, 음료, 의약품, 기타), 그리고 포장 기술(압출, 진공성형 등)별로 세분화됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 미국 소포 네트워크에 있어서의 경량 보호 메일러에 대한 전자상거래 수요 급증

- 미국 CPG 브랜드가 2025년 이후 플라스틱 협정 대상으로 재활용 가능한 단일 소재 파우치의 신속한 채택

- 높은 배리어성 플렉서블 필름을 필요로 하는 조리된 식품 및 운반용 식품의 성장

- 의약품 콜드체인의 확대가 특수 경질 용기와 물집 필름의 보급을 촉진

- PCR 함유량 25%에 대한 기업 헌신에 의해 rPET 및 rHDPE 병 수요가 증가

- 중소기업 브랜드의 단납기 커스터마이즈를 가능하게 하는 고도의 디지털 인쇄에 대한 투자

- 시장 성장 억제요인

- 주 수준에서 일회용 플라스틱 금지 강화 및 특정 포장 형태 감소

- 셰일 가스 원료의 변동에 따른 폴리올레핀 수지 가격의 변동

- 지속가능성의 관점에서 종이나 알루미늄의 대체품으로의 소비자의 이행

- 화학 재활용 인프라의 자본 집약성이 플라스틱 공급을 제한한다

- 공급망 분석

- 무역 시나리오 분석(관련 HS 코드에 기초)

- 미국의 현재 재활용 동향

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 재료 유형별

- 경질 플라스틱

- 폴리에틸렌(PE)

- 폴리프로필렌(PP)

- 폴리에틸렌테레프탈레이트(PET)

- 폴리염화비닐(PVC)

- 폴리스티렌(PS)과 발포 폴리스티렌(EPS)

- 기타 재료 유형

- 연질 플라스틱

- 폴리에틸렌(PE)

- 2축 연신 폴리프로필렌(BOPP)

- 캐스트 폴리프로필렌(CPP)

- 기타 재료 유형

- 경질 플라스틱

- 패키징 유형별

- 경질 플라스틱 포장

- 병 및 항아리

- 캡과 클로저

- 트레이와 클램쉘

- 기타 제품 유형

- 연질 플라스틱 포장

- 파우치

- 가방

- 필름과 랩

- 기타 제품 유형

- 경질 플라스틱 포장

- 최종 이용 산업별

- 식품

- 음료

- 의약품

- 화장품 및 퍼스널케어

- 가정용 및 공업용 화학약품

- 반려동물 식품과 동물 관리

- 기타 최종 이용 산업

- 포장 기술별

- 사출 성형

- 블로우 성형

- 압출

- 열성형

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Sealed Air Corp.

- Sonoco Products Co.

- Sigma Plastics Group Inc.

- ProAmpac LLC

- Constantia Flexibles

- Alpha Packaging Inc.

- Centor Inc.(Gerresheimer)

- Silgan Holdings Inc.

- Bericap Holdings

- Plastipak Holdings Inc.

- Coveris Holdings SA

- Printpack Inc.

- AptarGroup Inc.

- Pactiv Evergreen Inc.

- Novolex Holdings LLC

- Sabert Corp.

- Genpak LLC

- Mondi plc

제7장 시장 기회와 장래의 전망

SHW 25.11.17The United States plastic packaging market size is 29.97 million tonnes in 2025 and is projected to reach 35.29 million tonnes by 2030, exhibiting a 3.32% CAGR.

Demand resilience comes from e-commerce parcel expansion, food and beverage convenience formats, and brand owner commitments to integrate 25% post-consumer recycled (PCR) resin into core stock-keeping units. Regulatory frameworks such as California SB 54 and Washington State's recycled-content law are accelerating design shifts toward lighter gauges, mono-material laminates, and tethered closures. Adoption of FDA-cleared rPET, rHDPE, and rLLDPE has begun closing the feed-stock gap, while robotics installations-1,646 new units added by plastics molders in 2023-are streamlining throughput and raising quality yields within the United States plastic packaging market.

US Plastic Packaging Market Trends and Insights

Rapid Adoption of Recyclable Mono-Material Pouches by US CPG Brands

Mono-material polyethylene and polypropylene laminates are replacing mixed-substrate films that once obstructed recycling streams. Converters now deliver heat-resistant, high-barrier pouches that comply with the U.S. Plastics Pact 2025 design targets, giving brand owners a straightforward route to "recycle-ready" claims. DNP Indonesia's commercial roll-out of mono-material snack and pet-food packs demonstrates how barrier performance can be maintained while simplifying end-of-life processing. Retailers request specification parity with legacy foil structures, and test data confirm comparable oxygen-transmission rates, enabling broad SKU conversion. Packaging teams within the United States plastic packaging market are synchronizing material down-gauging with roll-stock width optimization to shrink film consumption per unit.

Surging E-Commerce Demand for Lightweight Protective Mailers in the US Parcel Network

Parcel shippers continue to eliminate unnecessary void fill, driving interest in thin-gauge, curbside-recyclable mailers that cut dimensional-weight fees while preserving product integrity. Amazon has shifted one-third of its U.S. outbound parcels to paper-based alternatives, eliminating 15 billion plastic air pillows since program inception. The company's pilot plants validate line speeds exceeding 250 parcels per minute, setting new benchmarks for automation. Competitors are matching performance with mono-material LDPE bubble mailers containing 30% PCR, as mandated by Washington's recycled-content law. Converters positioned within the United States plastic packaging market are investing in high-output blown-film towers and automated wicketing to address the spike in daily parcel volumes.

Escalating State-Level Single-Use Plastics Bans Reducing Certain Packaging Formats

California SB 54 mandates a 25% reduction in virgin plastic packaging sold within state borders by 2032, and producers must join a Producer Responsibility Organization by 2025. Similar mandates in New Jersey, Colorado, and Maine create a fragmented compliance map that raises complexity for nationwide brands. Converters are pre-emptively retiring PS clamshells and PVC blisters from their catalogs, turning to PET G and coated paperboard alternatives even when cost of goods rises. The regulatory uncertainty embeds risk premiums into long-term supply contracts, curbing discretionary capital spend within the United States plastic packaging market as firms await harmonized federal guidelines.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Ready-to-Eat and On-the-Go Foods Requiring High-Barrier Flexible Films

- Corporate Commitments to 25% PCR Content Boosting Demand for rPET and rHDPE Bottles

- Consumer Shift Toward Paper and Aluminum Alternatives for Sustainability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexible formats delivered 54.14% of United States plastic packaging market share in 2024 and are marching ahead at a 4.98% CAGR. Each new pouch replaces rigid counterparts with 60-70% less polymer, reducing freight emissions and warehouse footprints. E-commerce giants favor flat mailers because they collapse to one-tenth the inbound cube of corrugated boxes, slashing storage overhead. Brands now employ near-infrared (NIR) readable inks so flexibles sort efficiently at material-recovery facilities, improving real recycling rates. Meanwhile, "smart" pouches embed RFID or NFC tags, providing end-to-end visibility from filler to consumer scanning events.

Rigid plastics still account for essential roles in beverages, pharmaceuticals, and household chemicals, yet growth lags at 2.1% CAGR. Lightweight HDPE bottles use up to 12% less resin than 2023 designs, but performance thresholds on drop strength and taste neutrality limit further down-gauging. Washington State's recycled-content law compels bottle makers to secure stable rHDPE streams, prompting co-investment in in-house wash lines. Competition within the United States plastic packaging market now revolves around tethered caps that comply with forthcoming closure-retention mandates, merging convenience and litter reduction.

Polyethylene retained a 45.54% share of flexible volumes in 2024, supported by its broad processing window and robust curbside collection infrastructure. FDA approval for 100% rLLDPE content in snack wrappers confirms food-safety compliance pathways, allowing national retailers to launch "circular" private labels. Development teams adopt metallocene catalysts that provide higher dart impact at reduced gauge, contributing to resin savings of 8-10%. The United States plastic packaging market size for PE-based flexibles will continue scaling as co-extrusion technology accommodates recycled pellet variability without compromising film clarity.

The "other materials" category advances 6.34% CAGR, propelled by compostable PLA blends, cellulose-based films, and silicium-oxide coated papers. Consumer brands experiment with bio-PE derived from sugarcane that offers equivalent mechanical properties and a lower carbon footprint. BOPP remains indispensable for glossy snack and confectionery overwraps, yet new varnish systems deliver metallization-free barrier performance aligned with mono-material recycling guidelines. Partnerships between resin suppliers and film converters accelerate qualification cycles, shortening time-to-market for emerging formulations.

The United States Plastic Packaging Market is Segmented by Material Type ((Rigid Plastic(Polyethylene (PE), Polypropylene (PP) and More) Flexible Plastic (Polyethylene (PE), Biaxially Oriented Polypropylene (BOPP) and More)), Packaging Type (Rigid Plastic Packaging, Flexible Plastic Packaging), End-Use Industry (Food, Beverage, Pharmaceutical, and More) and Packaging Technology (Extrusion, Thermoforming, and More)

List of Companies Covered in this Report:

- Amcor plc

- Sealed Air Corp.

- Sonoco Products Co.

- Sigma Plastics Group Inc.

- ProAmpac LLC

- Constantia Flexibles

- Alpha Packaging Inc.

- Centor Inc. (Gerresheimer)

- Silgan Holdings Inc.

- Bericap Holdings

- Plastipak Holdings Inc.

- Coveris Holdings SA

- Printpack Inc.

- AptarGroup Inc.

- Pactiv Evergreen Inc.

- Novolex Holdings LLC

- Sabert Corp.

- Genpak LLC

- Mondi plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging E-commerce Demand for Lightweight Protective Mailers in US Parcel Network

- 4.2.2 Rapid Adoption of Recyclable Mono-Material Pouches by US CPG Brands Post-2025 Plastics Pact Targets

- 4.2.3 Growth of Ready-to-Eat and On-the-Go Foods Requiring High-Barrier Flexible Films

- 4.2.4 Pharmaceutical Cold-Chain Expansion Driving Specialty Rigid Containers and Blister Films

- 4.2.5 Corporate Commitments to 25 % PCR Content Boosting Demand for rPET and rHDPE Bottles

- 4.2.6 Investments in Advanced Digital Printing Enabling Short-Run Customization for SME Brands

- 4.3 Market Restraints

- 4.3.1 Escalating State-Level Single-Use Plastics Bans Reducing Certain Packaging Formats

- 4.3.2 Volatility in Polyolefin Resin Prices Linked to Shale Gas Feedstock Swings

- 4.3.3 Consumer Shift Toward Paper and Aluminum Alternatives for Sustainability

- 4.3.4 Capital Intensity of Chemical Recycling Infrastructure Limiting rPlastics Supply

- 4.4 Supply-Chain Analysis

- 4.5 Trade Scenario Analysis (under relevant HS codes)

- 4.6 Current Recycling Trends in United States

- 4.7 Regulatory Outlook

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitute Products

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Material Type

- 5.1.1 Rigid Plastic

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polyethylene Terephthalate (PET)

- 5.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.1.5 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.1.1.6 Other Material Types

- 5.1.2 Flexible Plastic

- 5.1.2.1 Polyethylene (PE)

- 5.1.2.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.2.3 Cast Polypropylene (CPP)

- 5.1.2.4 Other Material Types

- 5.1.1 Rigid Plastic

- 5.2 By Packaging Type

- 5.2.1 Rigid Plastic Packaging

- 5.2.1.1 Bottles and Jars

- 5.2.1.2 Caps and Closures

- 5.2.1.3 Trays and Clamshells

- 5.2.1.4 Other Product Types

- 5.2.2 Flexible Plastic Packaging

- 5.2.2.1 Pouches

- 5.2.2.2 Bags

- 5.2.2.3 Films and Wraps

- 5.2.2.4 Other Product Types

- 5.2.1 Rigid Plastic Packaging

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Home and Industrial Chemicals

- 5.3.6 Pet Food and Animal Care

- 5.3.7 Other End-use Industry

- 5.4 By Packaging Technology

- 5.4.1 Injection Molding

- 5.4.2 Blow Molding

- 5.4.3 Extrusion

- 5.4.4 Thermoforming

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Amcor plc

- 6.4.2 Sealed Air Corp.

- 6.4.3 Sonoco Products Co.

- 6.4.4 Sigma Plastics Group Inc.

- 6.4.5 ProAmpac LLC

- 6.4.6 Constantia Flexibles

- 6.4.7 Alpha Packaging Inc.

- 6.4.8 Centor Inc. (Gerresheimer)

- 6.4.9 Silgan Holdings Inc.

- 6.4.10 Bericap Holdings

- 6.4.11 Plastipak Holdings Inc.

- 6.4.12 Coveris Holdings SA

- 6.4.13 Printpack Inc.

- 6.4.14 AptarGroup Inc.

- 6.4.15 Pactiv Evergreen Inc.

- 6.4.16 Novolex Holdings LLC

- 6.4.17 Sabert Corp.

- 6.4.18 Genpak LLC

- 6.4.19 Mondi plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment