|

시장보고서

상품코드

1850179

유럽의 스마트 제조 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Smart Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

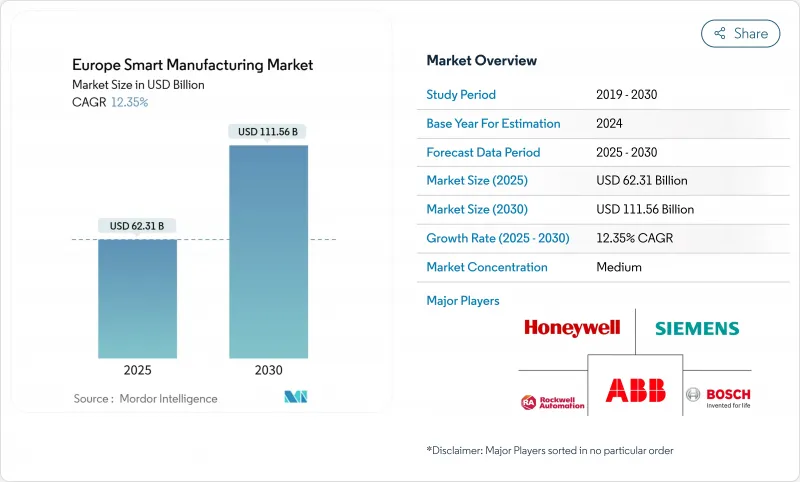

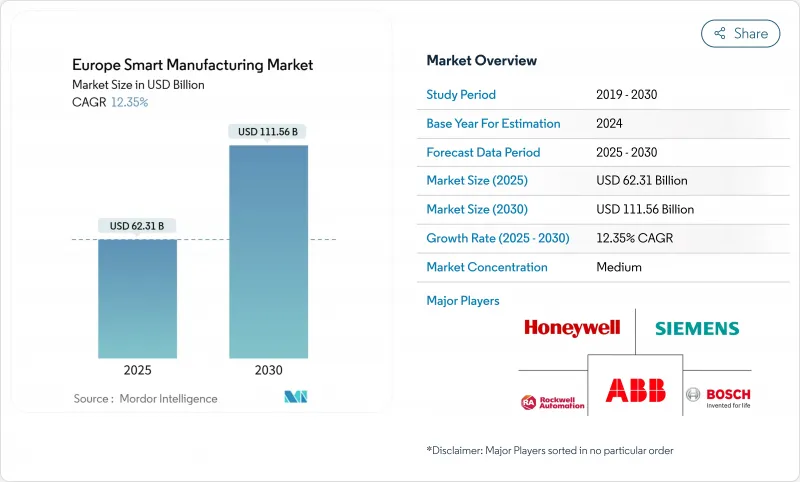

유럽의 스마트 제조 시장 규모는 2025년에 623억 1,000만 달러, 2030년에는 1,115억 6,000만 달러에 이르고, CAGR 12.35%로 확대될 것으로 예측됩니다.

인건비 인플레이션의 격화, 2,000억 유로(2,130억 달러)의 InvestAI 프로그램과 같은 주목도가 높은 공적 자금, 사이버 레지리언스법에 근거한 규제 압력의 증가로 커넥티드 생산 기술의 채택을 가속화하고 있습니다. 산업용 로보틱스가 계속 공장 현장의 자동화를 지원하는 한편, 엣지 AI와 디지털 트윈의 도입이 자산 활용을 확대하는 실시간 프로세스 인사이트를 풀어 놓습니다. 기업은 제어 하드웨어, IIoT 연결성, 분석 소프트웨어를 융합한 플랫폼 기반 생태계를 추구함으로써 에너지 소비를 억제하고 넷 제로 의무를 준수할 수 있습니다. 기존 기업이 AI 전문가를 흡수하고 정부가 재정적 인센티브를 지역 데이터 주권 보호에 연결함으로써 경쟁이 치열 해지고 유럽의 스마트 제조 시장은 경제 회복력의 전략적 지주가 됩니다.

유럽의 스마트 제조 시장 동향과 통찰

EU 인더스트리 4.0 자금 조달 계획

유럽의 강력한 자금 제공은 디지털 혁신을 위한 전례없는 자금을 인출합니다. 독일의 Manufacturing-X 프로그램은 상호 운용가능한 산업 데이터 공간 구축에 1억 5,000만 유로(1억 6,000만 달러)를 공급하고, 보다 광범위한 InvestAI 구조는 AI 인프라 전체에 2,000억 유로(2,130억 달러)를 동원하고 있습니다. 중소기업이 매칭 그랜트를 이용함으로써 진입 장벽을 낮췄습니다. 영국의 Made Smarter 파일럿에서는 이미 2,200만 파운드(2,800만 달러)를 350개의 기술 프로젝트에 투입하여 1,600명의 신규 고용을 창출했습니다. 벤처기업의 기세는 공적 자금을 추종하는 것으로, 독일에서는 AI를 활용한 제조업의 스타트업 기업이 67% 급증하고 AWS, 마이크로소프트, 애플이 하이퍼스케일러를 제공하는 것을 표명하고 있습니다. 이러한 자본의 흐름에 따라 유럽의 스마트 제조 시장은 지역의 기술 주권을 지키면서 아시아의 수탁 제조를 대신하는 신뢰할 수 있는 시장으로 자리매김하고 있습니다.

인건비 상승 압력이 공장 자동화를 촉진

EU의 시간당 평균 인건비는 2024년에는 전년 대비 5% 증가한 33.5유로(35.7달러)로 서유럽와 저임금 지역과의 델타가 확대됩니다. 룩셈부르크의 시급은 55.2유로(58.8달러)로 EU권의 최고이며, 프리미엄 생산자의 자동화에 대한 경쟁상의 긴급성이 높아지고 있습니다. 또한 고용주는 심각한 인재 격차에 직면하고 있습니다. 21개국의 조사 대상 기업의 75%가 숙련된 직무의 충족이 곤란하다고 보고하고 있습니다. 이러한 압력이 얽혀 자동화는 재량적인 효율화 수단에서 필수적인 요건으로 변화하고 스마트 제조 시장 전체에서 반복 작업을 로봇이나 컴퓨터 비전 시스템으로 대체하는 움직임이 가속화되고 있습니다.

사이버 보안 및 데이터 주권에 대한 우려

사이버 탄력성 법률은 위험 단계적 적합성 평가를 실시하고 최대 1,500만 유로(1,600만 달러) 또는 세계 매출의 2.5% 벌칙을 부과할 수 있습니다. GDPR(EU 개인정보보호규정)과 NIS 2의 규칙이 겹쳐지면서 특히 사이버 팀이 제한된 중소기업의 경우 문서화 작업이 확대됩니다. 지역 외부로의 데이터 전송을 두려워하기 때문에 EU 외부에서 호스팅되는 하이퍼스케일 플랫폼으로의 전환이 지연되어 공급업체는 소블린 클라우드 및 에지 애널리틱스 어플라이언스를 제공하지 않을 수 있습니다. 이러한 컴플라이언스 비용은 도입주기를 장기화하여 유럽 스마트 제조 시장의 단기 성장 속도를 억제합니다.

부문 분석

2024년 유럽 스마트 제조 시장 점유율은 산업용 로봇이 28%를 차지했고 자동차 최종 조립 자동화와 표준화된 용접 셀이 이를 지원합니다. 파낙의 스페인 진출은 남유럽의 미개척 클러스터의 개척을 시사하고 있으며, 방폭 사양의 협동 도장 로봇은 위험 환경 용도를 개척합니다. 디지털 트윈 & 시뮬레이션 플랫폼은 CAGR 16.8%로 확대되어 AI와 함께 물리 기반 모델을 통합하여 자산 거동을 예측하고 시운전 간격을 단축하고 있습니다. 시뮬레이션과 MES의 융합은 클로즈드 루프의 최적화를 가능하게 해, 디지털 트윈을 유럽의 스마트 제조 시장에서 가장 빠른 테코로서 위치시킵니다.

자동화 제어 시스템(PLC, SCADA, DCS)은 플랜트가 이더넷 기반 필드버스로 이동함에 따라 업데이트 수요가 발생합니다. 하니웰의 익스피리언 오퍼레이션 어시스턴트(Experion Operations Assistant)와 같은 AI로 확장된 HMI 레이어는 알람의 피로를 완화하는 컨텍스트에 따른 추천을 표시합니다. MES는 Valmet-FactoryPal과 같은 인수를 통해 빠르게 침투하고 OEE 대시보드를 처방 통찰력으로 충실하게 만듭니다. Additive Manufacturing은 형상의 복잡성이 정량적 경제성을 능가하는 예비 부품 완성에 틈새 비계를 유지합니다. 이러한 툴셋의 확대로 유럽의 스마트 제조 시장의 수익원은 다양해지고 있습니다.

유럽의 스마트 제조 시장은 기술별(자동 제어 시스템, 산업용 로봇 등), 구성요소별(하드웨어, 소프트웨어, 서비스), 최종 사용자 산업별(자동차, 항공우주 및 방위, 화학제품 및 석유화학제품 등), 국가별로 분류되어 있습니다. 시장 규모와 예측은 금액(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EU 인더스트리 4.0 자금 계획

- 공장 자동화를 추진하는 노동 비용의 압력 증가

- IIoT 연결의 급속한 도입

- 넷 제로 의무화에 의해 에너지 최적화 솔루션이 가속

- 유럽 중소기업에서 에지 AI 품질 검사 도입

- 산업 급의 5G 프라이빗 네트워크의 전개

- 시장 성장 억제요인

- 사이버 보안 및 데이터 주권에 대한 우려

- 브라운필드 통합 CAPEX의 고수준

- CEE 플랜트의 분산화된 레거시 머신 프로토콜

- 디지털 트윈 엔지니어링의 인력 부족

- 가치/공급망 분석

- 규제 상황(EU 디지털 10년, Gaia-X)

- 기술 전망(IIoT, 디지털 트윈, 5G, 엣지 AI)

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기술별

- 자동화 제어 시스템(PLC, SCADA, DCS)

- 산업용 로봇

- 산업용 IoT 플랫폼

- 휴먼 머신 인터페이스(HMI)

- 제조 실행 시스템(MES)

- 제품 수명주기 관리(PLM)

- 디지털 트윈과 시뮬레이션

- 적층 조형/3D 프린팅

- 구성요소별

- 하드웨어

- 센서

- 컨트롤러/IPC

- 엣지 컴퓨팅 기기

- 머신 비전 시스템

- 로보틱스

- 소프트웨어

- SCADA 및 HMI 소프트웨어

- 분석 및 AI 소프트웨어

- ERP 및 PLM 소프트웨어

- 서비스

- 통합 및 컨설팅

- 유지보수 및 지원

- 매니지드 서비스

- 하드웨어

- 최종 사용자 업계별

- 자동차

- 항공우주 및 방어

- 화학 및 석유화학제품

- 식음료

- 의약품과 생명공학

- 금속 및 광업

- 일렉트로닉스 및 반도체

- 석유 및 가스

- 유틸리티 및 에너지

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 네덜란드

- 스웨덴

- 폴란드

- 벨기에

- 오스트리아

- 스위스

- 노르웨이

- 핀란드

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- Market-share Analysis

- 기업 프로파일

- ABB Ltd

- Siemens AG

- Schneider Electric SE

- Rockwell Automation Inc.

- Honeywell International Inc.

- Emerson Electric Co.

- General Electric Co.

- Robert Bosch GmbH

- FANUC Corporation

- IBM Corporation

- Dassault Systems SE

- SAP SE

- Mitsubishi Electric Corp.

- KUKA AG

- Yokogawa Electric Corp.

- PTC Inc.

- Hexagon AB

- Omron Corp.

- Beckhoff Automation GmbH

- Endress Hauser AG

제7장 시장 기회와 장래의 전망

SHW 25.11.17Europe smart manufacturing market size is currently valued at USD 62.31 billion in 2025 and is forecast to reach USD 111.56 billion by 2030, expanding at a 12.35% CAGR.

Intensifying labor-cost inflation, high-profile public funding such as the EUR 200 billion (USD 213 billion) InvestAI program, and escalating regulatory pressure under the Cyber Resilience Act collectively accelerate adoption of connected production technologies. Industrial robotics continues to anchor plant-floor automation, while edge AI and digital-twin deployments unlock real-time process insights that magnify asset utilization. Enterprises pursue platform-based ecosystems that fuse control hardware, IIoT connectivity, and analytics software so they can curb energy consumption and comply with net-zero mandates. The competitive field tightens as incumbents absorb AI specialists, and governments link fiscal incentives to local data-sovereignty safeguards, turning the Europe smart manufacturing market into a strategic pillar of economic resilience.

Europe Smart Manufacturing Market Trends and Insights

EU Industry-4.0 Funding Schemes

Robust European funding unlocks unprecedented capital for digital transformation. Germany's Manufacturing-X program supplies EUR 150 million (USD 160 million) to create interoperable industrial data spaces, while the broader InvestAI architecture mobilizes EUR 200 billion (USD 213 billion) across AI infrastructure. SME access to matching grants lowers entry barriers; the UK's Made Smarter pilot has already funnelled GBP 22 million (USD 28 million) into 350 technical projects that generated 1,600 new jobs. Venture momentum follows public outlays, illustrated by Germany's 67% jump in AI-enabled manufacturing start-ups and hyperscaler commitments from AWS, Microsoft, and Apple. These capital flows position the Europe smart manufacturing market as a credible alternative to Asian contract manufacturing while defending regional technology sovereignty.

Rising Labor-Cost Pressure Driving Factory Automation

Average EU hourly labor costs climbed 5% year over year to EUR 33.5 (USD 35.7) in 2024, widening the delta between Western Europe and lower-wage regions. Luxembourg tops the bloc at EUR 55.2 (USD 58.8) per hour, sharpening competitive urgency for automation among premium producers. Employers also confront an acute talent gap: 75% of firms surveyed across 21 countries report difficulty filling skilled roles. These intertwined pressures convert automation from a discretionary efficiency lever into an existential requirement, accelerating replacement of repetitive tasks with robotics and computer-vision systems across the Europe smart manufacturing market.

Cyber-Security and Data-Sovereignty Concerns

The Cyber Resilience Act enforces risk-tiered conformity assessments and may levy penalties up to EUR 15 million (USD 16 million) or 2.5% of global turnover. Overlapping GDPR and NIS 2 rules escalate documentation workloads, especially for SMEs with limited cyber teams. Fear of extraterritorial data transfer slows migration to hyperscale platforms hosted outside the EU, compelling suppliers to offer sovereign clouds or edge-analytics appliances. These compliance costs elongate deployment cycles and temper the near-term growth pace of the Europe smart manufacturing market

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of IIoT Connectivity

- Net-Zero Mandates Accelerating Energy-Optimization Solutions

- High Brown-Field Integration CAPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial robotics held 28% of Europe smart manufacturing market share in 2024, supported by automotive final-assembly automation and standardized welding cells. FANUC's expansion in Spain signals pursuit of underserved Southern European clusters, while its explosion-proof collaborative paint robot opens hazardous-environment applications. Digital twin & simulation platforms are scaling at a 16.8% CAGR, embedding physics-based models alongside AI to forecast asset behaviour and shrink commissioning intervals. Simulation convergence with MES unlocks closed-loop optimisation, positioning digital twins as the fastest lever inside the Europe smart manufacturing market.

Automation control systems (PLC, SCADA, DCS) experience replacement demand as plants migrate to Ethernet-based fieldbuses. AI-augmented HMI layers such as Honeywell's Experion Operations Assistant surface contextual recommendations that cut alarm fatigue. MES penetration quickens through acquisitions like Valmet-FactoryPal, enriching OEE dashboards with prescriptive insights. Additive manufacturing maintains a niche foothold in spare-parts fulfillment, where geometry complexity outweighs volume economics. This broadening toolset cements diversified revenue streams across the Europe smart manufacturing market.

Europe Smart Manufacturing Market is Segmented by Technology (Automation Control Systems, Industrial Robotics, and More), Component (Hardware, Software, Services), End-User Industry (Automotive, Aerospace and Defense, Chemicals and Petrochemicals, and More), and Country. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABB Ltd

- Siemens AG

- Schneider Electric SE

- Rockwell Automation Inc.

- Honeywell International Inc.

- Emerson Electric Co.

- General Electric Co.

- Robert Bosch GmbH

- FANUC Corporation

- IBM Corporation

- Dassault Systems SE

- SAP SE

- Mitsubishi Electric Corp.

- KUKA AG

- Yokogawa Electric Corp.

- PTC Inc.

- Hexagon AB

- Omron Corp.

- Beckhoff Automation GmbH

- Endress+Hauser AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Industry-4.0 funding schemes

- 4.2.2 Rising labor-cost pressure driving factory automation

- 4.2.3 Rapid adoption of IIoT connectivity

- 4.2.4 Net-zero mandates accelerating energy-optimisation solutions

- 4.2.5 Edge-AI quality-inspection deployment in European SMEs

- 4.2.6 Industrial-grade 5G private-network roll-outs

- 4.3 Market Restraints

- 4.3.1 Cyber-security and data-sovereignty concerns

- 4.3.2 High brown-field integration CAPEX

- 4.3.3 Fragmented legacy machine protocols in CEE plants

- 4.3.4 Scarcity of digital-twin engineering talent

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (EU Digital Decade, Gaia-X)

- 4.6 Technological Outlook (IIoT, Digital Twin, 5G, Edge-AI)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Automation Control Systems (PLC, SCADA, DCS)

- 5.1.2 Industrial Robotics

- 5.1.3 Industrial IoT Platforms

- 5.1.4 Human-Machine Interface (HMI)

- 5.1.5 Manufacturing Execution System (MES)

- 5.1.6 Product Lifecycle Management (PLM)

- 5.1.7 Digital Twin and Simulation

- 5.1.8 Additive Manufacturing / 3-D Printing

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 Sensors

- 5.2.1.2 Controllers / IPC

- 5.2.1.3 Edge-Computing Devices

- 5.2.1.4 Machine-Vision Systems

- 5.2.1.5 Robotics

- 5.2.2 Software

- 5.2.2.1 SCADA and HMI Software

- 5.2.2.2 Analytics and AI Software

- 5.2.2.3 ERP and PLM Software

- 5.2.3 Services

- 5.2.3.1 Integration and Consulting

- 5.2.3.2 Maintenance and Support

- 5.2.3.3 Managed Services

- 5.2.1 Hardware

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace and Defense

- 5.3.3 Chemicals and Petrochemicals

- 5.3.4 Food and Beverage

- 5.3.5 Pharmaceuticals and Biotechnology

- 5.3.6 Metals and Mining

- 5.3.7 Electronics and Semiconductors

- 5.3.8 Oil and Gas

- 5.3.9 Utilities and Energy

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Russia

- 5.4.7 Netherlands

- 5.4.8 Sweden

- 5.4.9 Poland

- 5.4.10 Belgium

- 5.4.11 Austria

- 5.4.12 Switzerland

- 5.4.13 Norway

- 5.4.14 Finland

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market-share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Siemens AG

- 6.4.3 Schneider Electric SE

- 6.4.4 Rockwell Automation Inc.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Emerson Electric Co.

- 6.4.7 General Electric Co.

- 6.4.8 Robert Bosch GmbH

- 6.4.9 FANUC Corporation

- 6.4.10 IBM Corporation

- 6.4.11 Dassault Systems SE

- 6.4.12 SAP SE

- 6.4.13 Mitsubishi Electric Corp.

- 6.4.14 KUKA AG

- 6.4.15 Yokogawa Electric Corp.

- 6.4.16 PTC Inc.

- 6.4.17 Hexagon AB

- 6.4.18 Omron Corp.

- 6.4.19 Beckhoff Automation GmbH

- 6.4.20 Endress+Hauser AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment