|

시장보고서

상품코드

1850211

합성생물학 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Synthetic Biology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

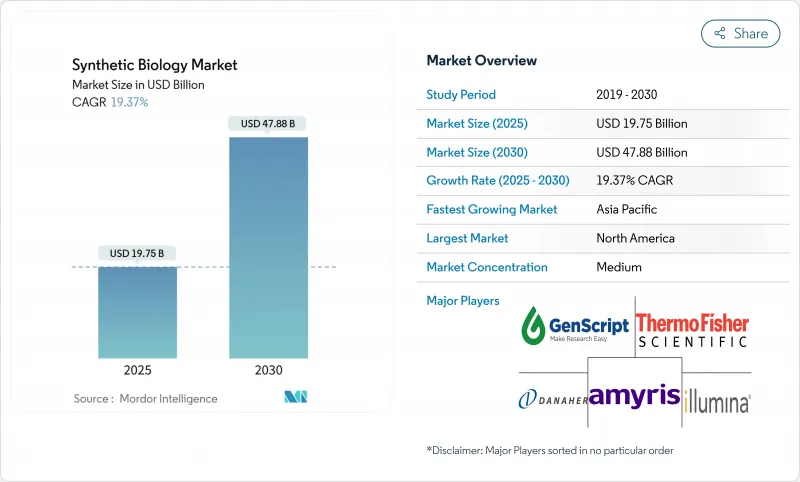

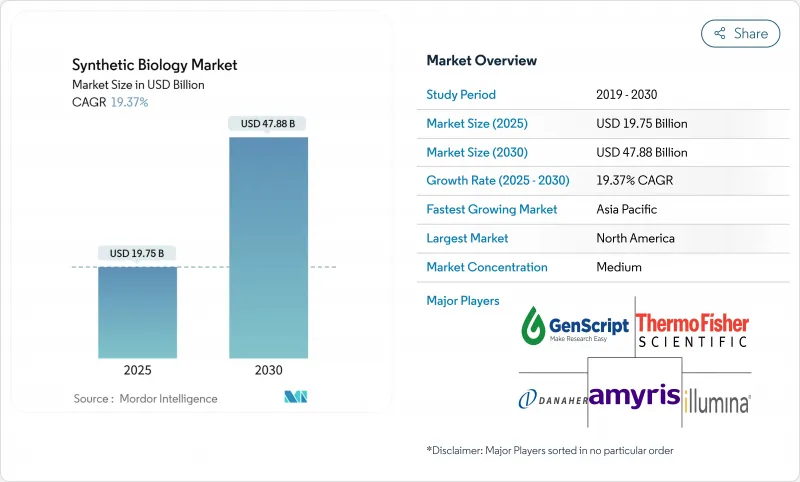

합성생물학 시장 규모는 2025년에 197억 5,000만 달러, 2030년에는 CAGR 19.37%로, 478억 8,000만 달러로 성장할 것으로 예상됩니다.

최근의 성장은 개념 증명의 생물 공학에서 대규모 생물 제조로의 전환을 반영합니다. 인공지능으로 유도된 단백질 설계의 진보, 유전자 합성 비용의 저하, 안정된 정부 자금이 기술 혁신 사이클을 단축하고 진입 장벽을 낮추고 있습니다. 기업의 넷 제로에 대한 헌신은 석유화학제품에 대한 바이오의 지속적인 수요를 창출하고, 유전자 편집과 자동 바이오 파운드리에서의 비약적인 진보는 헬스케어, 식품, 특수 소재에서의 대응 가능한 용도를 확대하고 있습니다. 동시에 듀얼 유스 규제와 인재 부족이 성장 궤도를 약화시키고 합성생물학 시장 전체에서 규제 대응과 인재 개척에 중점을 두고 있습니다.

세계 합성생물학 시장 동향과 통찰

정부와 VC에 의한 자금조달 급증

대규모 공공 프로그램은 바이오 제조업의 사업 확대를 지원하는 자본 풀을 확대하고 있습니다. 미국은 2040년까지 국내 화학 수요의 30%를 바이오 생산으로 충족하기 위해 150억 달러의 국가 생명공학 추진법을 제정했습니다. 중국은 2024년에 41억 7,000만 달러를 바이오제조 인프라 정비에 충당할 것을 약속하며, 기술주권 우선의 자세를 나타내고 있습니다. 호라이즌 유럽의 SYNBEE 프로젝트는 25개국에서 스타트업 기업을 육성하고 있으며, SynBioBeta에 따르면 벤처 자금은 유행 이전 수준을 능가하고 있습니다. 이와 같이 공적자본과 민간자본이 합류함으로써 연구실 벤치에서 파일럿 플랜트까지의 '죽음의 계곡'이 단축되고 합성생물학 시장 전체 시장 투입까지의 시간이 단축됩니다.

유전자 합성의 비용 곡선 감소

효소 DNA 합성은 이제 몇 주가 아닌 며칠 만에 몇 킬로 염기의 구조를 제공합니다. Ansa Biotechnologies 플랫폼은 현재 1,000 bp 이상의 서열을 합성하고 2025년까지 10,000 bp의 능력을 목표로 하고 있습니다. Evonetix의 반도체 기반 칩은 기존의 포스포로아미다이트 화학보다 10배 빠른 유전자 길이 단편을 생산합니다. Kilobaser와 Telesis Bio의 벤치탑 합성기는 소규모 실험실 접근을 더욱 민주화합니다. 이러한 기술 혁신은 대사 공학 및 단백질 최적화 프로젝트의 반복 비용을 줄이고 합성생물학 시장 전체 수요를 강화하고 있습니다.

이중 용도 바이오 위협 규제의 발판

정책 입안자가 유전자 물질 스크리닝을 강화함에 따라 컴플라이언스 부담이 증가합니다. SecureDNA는 30bp 이상의 주문마다 병원체 데이터베이스와 대조하여 고객의 기밀성을 유지하면서 스크리닝을 실시합니다. 중국의 바이오 세이프티 프레임 워크는 유전적으로 조작된 미생물에 엄격한 모니터링을 부과하면서도 혁신을 지원하는 것을 목표로합니다. 유럽은 바이오테크놀러지법을 2026년 3분기까지 연기하여 불확실성을 길게 하고 있습니다. 프론티어 조사는 AI에 의한 바이오 자동화가 입법 사이클을 초과할 수 있으며 새로운 거버넌스 모델이 필요하다고 경고합니다. 합성생물학 시장의 소규모 기업에는 이러한 규제를 극복하기 위한 규제 당국에 대한 대응력이 부족한 경우가 많아 제품 출시가 늦어지고 있습니다.

부문 분석

DNA/RNA 합성기와 유전자 편집 키트가 연구실 워크플로우에 필수적인 인프라를 형성하고 있기 때문에 핵심 제품이 2024년 매출의 48.34%를 차지했습니다. 에보네틱스의 칩 기반 합성기는 하드웨어의 혁신성을 보여주며, 합성 시간을 10분의 1로 단축하고 소모품 수요를 지원하고 있습니다. 핵심 제품의 합성생물학 시장 규모는 정확성과 처리량의 지속적인 업그레이드를 지원하며 안정적인 성장이 예상됩니다.

Enabling Products(올리고뉴클레오티드, 클로닝 벡터, 무세포 시스템 포함)는 2030년까지 연평균 복합 성장률(CAGR) 20.20%를 보일 것으로 예측되며 제품 등급 중 가장 빠릅니다. 트위스트 바이오사이언스의 AI 안전성 컨소시엄 참여는 안전한 DNA 조달의 전략적 중요성을 강조합니다. 최초의 합성 효모 유전체과 프로그램 가능한 무세포 단백질 공장은 복잡성에 대한 요구 증가를 반영하여 합성생물학 시장 전체의 소모품 볼륨을 확대하고 있습니다.

유전체 엔지니어링은 2024년에는 합성생물학 시장 점유율의 33.86%를 차지하며, CRISPR-Cas9의 보급과 TIGR과 같은 신흥의 대체 기술에 의해 지원되고 있습니다. CASGEVY와 같은 상용화 이정표는 치료 수익 풀을 확인합니다. 규제 전례는 산업용 및 농업용 유전자 편집 이니셔티브를 뒷받침하고 이 기술 부문의 리더십을 강화하고 있습니다.

바이오인포매틱스와 CAD 툴은 19.83%의 연평균 복합 성장률(CAGR)로 확대되어 경험적인 왕따를 알고리즘에 이끌린 엔지니어링으로 바꿉니다. 설문조사팀은 CodonTransformer의 여러 유형 최적화 프레임워크가 히트까지의 타임라인을 단축한다고 말합니다. AI 모델의 규모가 확대됨에 따라 구독 소프트웨어 매출은 시약 매출을 능가하는 속도로 증가하고 밸류체인 기업 간 합성생물학 시장 규모 분포가 재구성됩니다.

합성생물학 세계 시장 보고서는 제품별(코어 제품, 인에이블링 제품, 인에이블드 제품), 용도별(헬스케어, 화학(바이오연료 포함), 식품 및 농업, 기타 용도(바이오보안, 에너지, 환경)), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류하고 있습니다.

지역 분석

북미는 2024년에 43.57%의 매출 점유율을 차지했습니다. 150억 달러의 연방 정부에 의한 바이오 제조에 대한 헌신이 생산 능력 증진을 지원하는 반면, 벤처 캐피탈과 확립된 R&D 클러스터는 스타트업 형성을 지원합니다. 긴코 바이오웍스의 플랫폼 파트너십과 Thermo Fisher Scientific의 400억-500억 달러의 M&A는 통합과 규모의 이점을 보여줍니다. 그럼에도 불구하고 미국 기업은 바이오인포매틱스의 인재 병목 현상과 중복 연방 및 주 규칙의 컴플라이언스 부담에 직면하고 있으며,이 지역의 합성생물학 시장의 성장을 감속시키는 요인이 되고 있습니다.

아시아태평양은 CAGR 22.14%에서 가장 빠르게 성장하는 지역입니다. 중국은 2024년 41억 7,000만 달러의 투자와 2025년의 추가 투자에 힘입어 영향력이 큰 생명공학 논문과 특허로 유럽을 몰아냈습니다. 상하이의 생명공학 허브는 병설된 제조 인프라와 보조금 제도를 활용하여 상업화를 가속화하고 있습니다. 가격 경쟁력 있는 생산 능력으로 이 지역은 주요 수출 플랫폼으로 자리매김하여 세계 합성생물학 시장에 대한 영향력을 강화하고 있습니다.

유럽은 견고한 지속가능성 정책과 단편적인 규제의 이행을 겸비하고 있습니다. 순환 바이오 기반 유럽 이니셔티브는 16만 5,000명의 노동자를 고용하는 15개 바이오정유소에 22억 달러를 투입합니다. Horizon Europe의 SYNBEE는 기업 지원을 25개국으로 확대하고 있습니다. 그러나 EU 생명 공학법의 지연은 불확실성을 늘리고 프로젝트 자금 조달을 지연시킬 수 있습니다. Insempra와 같은 기업은 신중한 자본 시장에서도 화장품용 바이오 원료를 확대하기 위해 2,000만 달러를 조달하고 있습니다. 장애물이 있는 것, 유럽의 서큘러 이코노미의 이념은 합성생물학 시장에서 장기적인 관련성을 확보하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부와 벤처캐피탈로부터 자금 급증

- 유전자 합성의 비용 곡선 저하

- AI 구동형 단백질 설계의 채택

- 공급망의 회복력 강화를 위해, 인공 단백질과 차세대 작물을 확보하기 위한 농업·식품 대기업에 의한 전략적 움직임

- 유전자 편집 플랫폼의 브레이크 스루에 의해 적용 가능한 용도 확대

- 기업의 넷 제로 의무화에 의해 바이오의 화학물질, 연료, 재료 수요가 증가

- 시장 성장 억제요인

- 이중용도 생물위협 규제의 제약

- 바이오인포매틱스 엔지니어의 인력 부족

- 제한된 DNA 데이터 보존 규격

- GMO 도입에 대한 사회적, 윤리적인 우려

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 코어 제품

- DNA/RNA 합성 장치

- 유전자 편집 키트와 효소

- 유효화 제품

- 올리고뉴클레오티드

- 클로닝 벡터

- 대응 제품

- 무세포 시스템

- 유전자 변형 미생물

- 코어 제품

- 기술별

- 유전체 공학

- DNA/RNA 합성

- 바이오인포매틱스와 CAD 툴

- 바이오프로세스와 자동화

- 용도별

- 헬스케어

- 약물 발견

- 유전자 및 세포 치료

- 화학약품과 바이오연료

- 특수화학제품

- 첨단 바이오연료

- 식품과 농업

- 대체 단백질

- 작물 특성 엔지니어링

- 기타(바이오 보안, 환경, 데이터 스토리지)

- 헬스케어

- 최종 사용자별

- 산업 생명 공학 기업

- 제약 및 바이오의약품

- 학술연구기관

- 방위 및 정부 연구소

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동

- GCC

- 남아프리카

- 기타 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific

- Danaher(IDT & Cytiva)

- Illumina

- GenScript

- Twist Bioscience

- Amyris

- Gingko Bioworks

- Precigen

- Novozymes

- DSM-Firmenich

- Zymergen

- Synthetic Genomics(Viridos)

- New England Biolabs

- Inscripta

- Benchling

- Oxford Nanopore

- Evonetix

- Prokarium

- Arzeda

- Deep Genomics

제7장 시장 기회와 장래의 전망

SHW 25.11.17The synthetic biology market size reached USD 19.75 billion in 2025 and is projected to climb to USD 47.88 billion by 2030, advancing at a 19.37% CAGR.

Recent gains reflect the transition from proof-of-concept bioengineering to large-scale biomanufacturing. Converging advances in artificial-intelligence-guided protein design, decreasing gene-synthesis costs, and steady government funding have shortened innovation cycles and lowered entry barriers. Corporate net-zero commitments create durable demand for bio-based alternatives to petrochemicals, while breakthroughs in genome editing and automated biofoundries extend addressable applications in healthcare, food, and specialty materials. At the same time, dual-use regulations and talent shortages temper the growth trajectory, placing a premium on regulatory navigation and workforce development across the synthetic biology market.

Global Synthetic Biology Market Trends and Insights

Government & VC Funding Surge

Large-scale public programs are deepening the capital pool that supports biomanufacturing build-outs. The United States enacted a USD 15 billion National Biotechnology Initiative Act to meet 30% of domestic chemical demand through bio-based production by 2040 . China committed USD 4.17 billion in 2024 for biomanufacturing infrastructure, signaling technology sovereignty priorities. Horizon Europe's SYNBEE project nurtures start-ups across 25 nations, while venture funding has remained above pre-pandemic levels according to SynBioBeta. This confluence of public and private capital shortens the "valley of death" from lab bench to pilot plant, accelerating time-to-market across the synthetic biology market.

Falling Cost Curve for Gene Synthesis

Enzymatic DNA synthesis now delivers multi-kilobase constructs in days instead of weeks. Ansa Biotechnologies' platform synthesizes sequences exceeding 1,000 bp today and targets 10,000 bp capability by 2025 . Evonetix's semiconductor-based chips fabricate gene-length fragments 10 times faster than traditional phosphoramidite chemistry. Benchtop synthesizers from Kilobaser and Telesis Bio further democratize access for smaller labs. These innovations cut iteration costs for metabolic-engineering and protein-optimization projects, reinforcing demand across the synthetic biology market.

Dual-Use Bio-Threat Regulation Drag

Compliance burdens grow as policymakers tighten genetic-material screening. SecureDNA screens every order over 30 bp against pathogen databases while preserving customer confidentiality, adding cost and processing time. China's biosafety framework imposes strict oversight of engineered microbes yet aims to support innovation. Europe postponed its Biotech Act until Q3 2026, prolonging uncertainty. Frontiers research warns that AI-enabled bio-automation may outpace legislative cycles, requiring new governance models. Smaller firms in the synthetic biology market often lack the regulatory-affairs bandwidth to navigate these regimes, slowing product launches.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Protein Design Adoption

- Breakthroughs in Gene-Editing Platforms Expanding Addressable Applications

- Corporate Net-Zero Mandates Driving Demand for Bio-Based Chemicals, Fuels, and Materials

- Talent Bottleneck in Bio-Informatics Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Core Products accounted for 48.34% of 2024 revenue as DNA/RNA synthesizers and gene-editing kits formed the indispensable infrastructure of laboratory workflows. Evonetix's chip-based synthesizer exemplifies hardware innovation, cutting synthesis times by a factor of 10 and anchoring recurring consumables demand. The synthetic biology market size for Core Products is expected to grow steadily, supported by continuous upgrades to accuracy and throughput.

Enabling Products-encompassing oligonucleotides, cloning vectors, and cell-free systems-are forecast to grow at a 20.20% CAGR through 2030, the fastest among product classes. Twist Bioscience's participation in AI safety consortia underscores the strategic importance of secure DNA sourcing. The first synthetic yeast genome and programmable cell-free protein factories reflect rising complexity needs, which magnify consumables volume across the synthetic biology market.

Genome Engineering held 33.86% of synthetic biology market share in 2024, buoyed by widespread CRISPR-Cas9 adoption and emergent alternatives like TIGR. Commercialization milestones such as CASGEVY validate therapeutic revenue pools. Regulatory precedents are encouraging industrial and agricultural genome-editing initiatives, reinforcing leadership of this technology segment.

Bioinformatics & CAD Tools will expand at a 19.83% CAGR, transforming empirical tinkering into algorithmically guided engineering. Researchers describes CodonTransformer's multi-species optimization framework that shortens path-to-hit timelines . As AI models scale, subscription software revenues are set to rise faster than reagent sales, reshaping the synthetic biology market size distribution among value-chain players.

The Global Synthetic Biology Market Report is Segmented by Product (Core Products, Enabling Products, and Enabled Products), Application (Healthcare, Chemicals (Including Biofuels), Food and Agriculture, and Other Applications (Biosecurity, Energy, and Environment)), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America).

Geography Analysis

North America held 43.57% revenue share in 2024. The USD 15 billion federal biomanufacturing commitment anchors capacity build-outs, while venture capital and established R&D clusters sustain start-up formation. Ginkgo Bioworks' platform partnerships and Thermo Fisher Scientific's USD 40-50 billion M&A war chest illustrate consolidation and scale advantages. Nevertheless, U.S. firms face talent bottlenecks in bio-informatics and the compliance load of overlapping federal and state rules, factors that could modulate synthetic biology market growth in the region.

Asia-Pacific is the fastest-expanding region at 22.14% CAGR. China has overtaken Europe in high-impact biotech papers and patents, supported by USD 4.17 billion in 2024 investments and further allocations slated for 2025. Shanghai's biotech hub leverages co-located manufacturing infrastructure and subsidy programs to accelerate commercialization. Price-competitive production capabilities position the region as a leading export platform, reinforcing its influence on the global synthetic biology market.

Europe combines robust sustainability policy with fragmented regulatory execution. The Circular Bio-Based Europe initiative directs USD 2.2 billion toward 15 biorefineries employing 165,000 workers. Horizon Europe's SYNBEE extends entrepreneur support to 25 nations. Delays in the EU Biotech Act, however, prolong uncertainty and may slow project financing. Companies like Insempra have raised USD 20 million to scale bio-based ingredients for cosmetics even amid cautious capital markets. Despite hurdles, Europe's circular-economy ethos secures long-term relevance within the synthetic biology market.

- Thermo Fisher Scientific

- Danaher (IDT & Cytiva)

- Illumina

- Genscript

- Twist Bioscience

- Amyris

- Gingko Bioworks

- Precigen

- Novozymes

- DSM-Firmenich

- Zymergen

- Synthetic Genomics (Viridos)

- New England Biolabs

- Inscripta

- Benchling

- Oxford Nanopore

- Evonetix

- Prokarium

- Arzeda

- Deep Genomics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government & VC funding surge

- 4.2.2 Falling cost curve for gene synthesis

- 4.2.3 AI-driven protein design adoption

- 4.2.4 Strategic moves by agriculture and food majors to secure engineered proteins and next-gen crops for supply-chain resilience

- 4.2.5 Breakthroughs in gene-editing platforms expanding addressable applications

- 4.2.6 Corporate net-zero mandates driving demand for bio-based chemicals, fuels, and materials

- 4.3 Market Restraints

- 4.3.1 Dual-use bio-threat regulation drag

- 4.3.2 Talent bottleneck in bio-informatics engineers

- 4.3.3 Limited DNA data-storage standards

- 4.3.4 Societal and ethical concerns over GMO adoption,

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value / USD)

- 5.1 By Product

- 5.1.1 Core Products

- 5.1.1.1 DNA/RNA Synthesizers

- 5.1.1.2 Gene Editing Kits & Enzymes

- 5.1.2 Enabling Products

- 5.1.2.1 Oligonucleotides

- 5.1.2.2 Cloning Vectors

- 5.1.3 Enabled Products

- 5.1.3.1 Cell-Free Systems

- 5.1.3.2 Engineered Micro-organisms

- 5.1.1 Core Products

- 5.2 By Technology

- 5.2.1 Genome Engineering

- 5.2.2 DNA/RNA Synthesis

- 5.2.3 Bioinformatics & CAD Tools

- 5.2.4 Bioprocessing & Automation

- 5.3 By Application

- 5.3.1 Healthcare

- 5.3.1.1 Drug Discovery

- 5.3.1.2 Gene & Cell Therapy

- 5.3.2 Chemicals & Biofuels

- 5.3.2.1 Specialty Chemicals

- 5.3.2.2 Advanced Biofuels

- 5.3.3 Food & Agriculture

- 5.3.3.1 Alternative Proteins

- 5.3.3.2 Crop Trait Engineering

- 5.3.4 Other (Bio-security, Environment, Data Storage)

- 5.3.1 Healthcare

- 5.4 By End-User

- 5.4.1 Industrial Biotech Companies

- 5.4.2 Pharma & Biopharma

- 5.4.3 Academic & Research Institutes

- 5.4.4 Defense & Government Labs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Thermo Fisher Scientific

- 6.3.2 Danaher (IDT & Cytiva)

- 6.3.3 Illumina

- 6.3.4 GenScript

- 6.3.5 Twist Bioscience

- 6.3.6 Amyris

- 6.3.7 Gingko Bioworks

- 6.3.8 Precigen

- 6.3.9 Novozymes

- 6.3.10 DSM-Firmenich

- 6.3.11 Zymergen

- 6.3.12 Synthetic Genomics (Viridos)

- 6.3.13 New England Biolabs

- 6.3.14 Inscripta

- 6.3.15 Benchling

- 6.3.16 Oxford Nanopore

- 6.3.17 Evonetix

- 6.3.18 Prokarium

- 6.3.19 Arzeda

- 6.3.20 Deep Genomics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment