|

시장보고서

상품코드

1850214

자동차 브레이크 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Brake System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

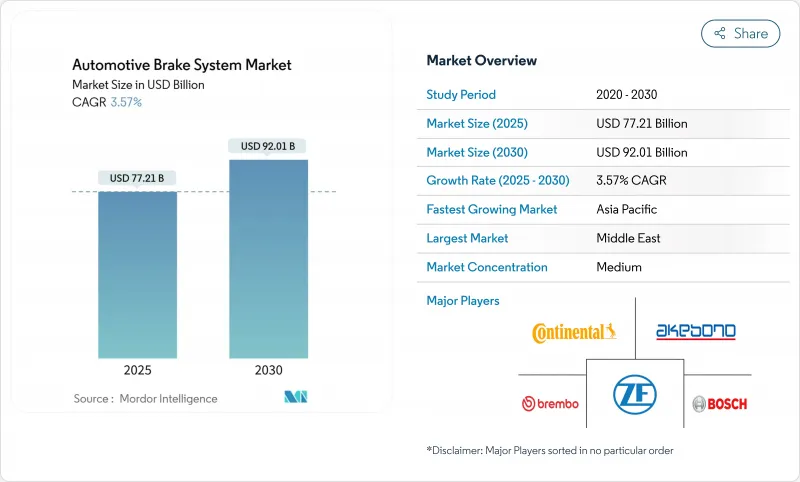

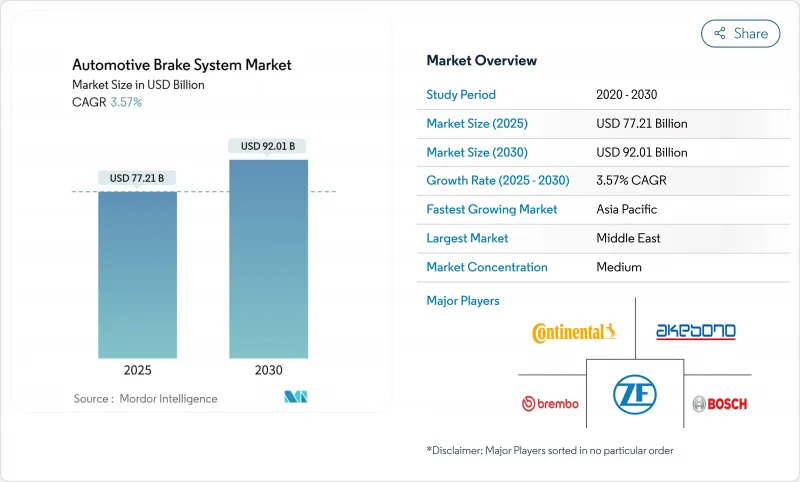

자동차 브레이크 시스템 시장은 2025년에 772억 1,000만 달러로 평가되었고, 2030년에는 920억 1,000만 달러에 이를 것으로 예측되며, CAGR은 3.57%를 나타낼 전망입니다.

시장 성장은 순수 유압식 시스템에서 소프트웨어 정의 차량의 전자식 제어 아키텍처로의 꾸준한 전환을 반영하며, 이는 소프트웨어로 정의된 차량에서 ABS(안티록 브레이크 시스템), 차량 안정성 제어, 회생 제동 기능을 통합 조정합니다. 아시아태평양 지역은 대규모 전기차(EV) 생산과 전자식 브레이크 어셈블리 아웃소싱을 통해 수요를 주도하는 반면, 중동 지역은 차량 현대화 정책과 인프라 투자 확대가 맞물리며 가장 빠른 성장세를 기록하고 있습니다. 기술 공급업체들은 UNECE R140 및 유로 7 미립자 배출 기준을 준수하기 위해 브레이크 바이 와이어(brake-by-wire) 및 저분진 마찰재에 집중하고 있으며, 경상용차(LCV) 운영사들은 계획되지 않은 가동 중단을 줄이는 예측 유지보수 프로그램을 통해 애프터마켓 물량을 증가시키고 있습니다.

세계의 자동차 브레이크 시스템 시장 동향 및 인사이트

급속한 전동화가 회생 대응 브레이크 하드웨어를 주도

전기차 구조는 트랙션 모터에 더 많은 제동 토크를 가하므로, 마찰 시스템은 소프트웨어 관리형 에너지 회수 장치와 완벽하게 연동되어야 합니다. Tevva와 ZF가 공동 개발한 회생 브레이크 키트는 표준 에어 브레이크 대비 최대 4배의 에너지를 회수하여 7.5톤 트럭의 주행 거리를 140마일(약 225km)까지 연장합니다. 메르세데스-벤츠 프로토타입은 브레이크 유닛을 e-드라이브 하우징 내부에 내장하여 녹 발생 가능성이 높은 하드웨어를 제거하고 미립자 배출을 줄였습니다. 아이신의 협동형 회생 시스템은 모든 부하 상태에서 차량 안정성을 유지하기 위해 유압 브레이크와 모터 브레이킹의 균형을 더욱 향상시킵니다.

ADAS 보급률 증가로 브레이크 바이 와이어 수요 상승

레벨 2+ 보조 기능과 계획된 레벨 4 자율주행은 유압 링크가 보장할 수 없는 밀리초 단위의 작동 속도를 요구합니다. 보쉬의 차세대 유압식 브레이크 바이 와이어 플랫폼은 기계식 페달 경로를 제거하면서도 이중 유체 회로를 유지해 이중화를 확보합니다. ZF는 통합 브레이크 제어와 소프트웨어 정의 섀시 모듈을 결합한 전기기계식 브레이크 기술로 이미 약 500만 대의 차량에 적용을 확정했습니다. 반도체 분야도 이에 발맞추고 있습니다. 르네사스의 R-Car X5H 시스템 온 칩은 하드웨어 격리 기술을 활용해 안전 핵심 브레이킹 영역을 보호합니다.

희토류 가격 변동성, 전자식 브레이크 액추에이터 비용 상승

미국 에너지부는 네오디뮴, 프라세오디뮴, 디스프로슘, 테르븀을 중국에 가공 공정이 집중된 핵심 소재로 지정하여 브레이크 바이 와이어 액추에이터를 가격 변동 위험에 노출시켰습니다. 공급업체들은 자석 화학 성분을 다각화하고 비자성 모터 대안을 모색 중이지만, 자동차 브레이크 시스템 시장 전반에 걸쳐 단기적 비용 압박은 지속되고 있습니다.

부문 분석

디스크 브레이크는 2024년 매출의 63.10%를 차지했으며, 열 안정성 덕분에 승용차 및 경트럭의 기본 선택으로 자리매김했습니다. 전기식 주차 브레이크 시장 규모는 공간 절약 및 ADAS와 시너지를 내는 전자적 통합으로 2030년까지 5.22% 성장할 전망입니다. 브레이크 인디아는 2024년 글로벌 OEM과 첫 전기식 주차 브레이크를 출시하며 신흥 시장의 비용 최적화 도입을 시사했습니다. 비용이 최우선인 후륜축에는 드럼 브레이크가 지속 사용되며, 배터리 전기차에서는 회생 모듈이 점유율을 확대 중입니다.

NASA 기술에서 파생된 경량 로터(현재 Orbis Brakes에 라이선스 제공)는 비탄성 질량을 42% 감소시키고 파형 통풍구를 통해 냉각 성능을 향상시킵니다. 이 혁신은 1kg의 무게도 중요한 고성능 전기차에 최초로 적용될 전망입니다. 이러한 혁신의 연속은 기존 물량을 희생하지 않으면서 자동차 브레이크 시스템 시장이 차세대 소재를 수용하는 데 기여합니다.

2024년 안티록 브레이크 시스템(ABS)은 45.10%의 시장 점유율로 안전 계층의 핵심을 이루었습니다. 그러나 전자식 차체 안정 제어(ESC)는 연평균 8.65% 성장률을 기록하며 이미 다수 지역에서 의무화되어 격차를 빠르게 좁힐 전망입니다. 콘티넨탈은 2024년 인도에서 100만 대 이상의 전자식 브레이크 시스템을 생산하며 확장 가능한 경제성을 입증했습니다. 트랙션 컨트롤 시스템(TCS)과 전자식 브레이크 분배(EBD)는 각각 트랙션과 하중 균형을 최적화하며 상호 보완적 역할을 지속합니다.

인공지능(AI) 기술이 기존 ABS를 강화하고 있습니다. 브렘보가 2024년 말 출시한 AI 기반 컨트롤러는 휠 잠김 전 그립 손실을 예측하여, 과거 하드웨어 경쟁이었던 분야를 이제 소프트웨어가 차별화할 것임을 입증했습니다. 이에 따라 자동차 브레이크 시스템 시장은 부품 공급에서 알고리즘 기반 성능 향상으로 계속 전환 중입니다.

유압식 작동 방식은 공급망과 서비스 기반이 확고히 자리잡아 2024년 매출의 66.25%를 차지했습니다. 그러나 연평균 9.50% 성장률이 예상되는 브레이크 바이 와이어 솔루션은 자율주행차의 지연 시간 기준을 충족합니다. 보쉬의 유압식 브레이크 바이 와이어 하이브리드는 기계식 페달을 제거하면서도 중복성을 위한 유체 경로를 유지해 신중한 OEM 업체들에게 진화적 단계를 제공합니다. 공압 시스템은 대형 트럭에서 유지되며, 기계식 케이블은 비용 제약이 있는 틈새 시장에서 생존합니다.

ZF의 경차 주문량은 순수 전기-기계식 브레이크의 상업적 타당성을 입증합니다. 자동차 브레이크 시스템 시장에 있어, 이 이중 트랙(진화적 하이브리드와 혁신적 바이-와이어)은 기존 제조 기반을 방해하지 않으면서 단계적 투자를 가능하게 합니다.

지역 분석

아시아태평양 지역은 2024년 매출의 58.55%를 차지했으며, 이는 중국의 전기차 보급 확대와 인도의 전자 부품 조립 규모에 힘입은 결과입니다. 콘티넨탈(Continental)만 해도 2024년 인도에서 100만 개 이상의 전자식 브레이크 시스템을 생산했습니다. 브레이크스 인디아-ADVICS(Brakes India-ADVICS)와 같은 현지 합작 기업들은 자국 기술 역량을 강화하고 있습니다.

유럽은 미세먼지 배출 규제로 인한 성숙하면서도 수익성 높은 수요를 창출합니다. 2025년 중반 시행 예정인 유로 7의 7mg/km 브레이크 먼지 기준은 무구리 소재 채택과 저항 감소형 캘리퍼 도입을 가속화합니다. 북유럽 국가들도 전기차 보급 확대로 재생 에너지 대응 시스템 수요가 증가하며 5%의 견고한 연평균 성장률(CAGR)을 기록합니다.

중동은 사우디아라비아의 ‘비전 2030’ 인프라 프로그램과 UAE의 운송 수단 다각화로 2030년까지 연평균 8.90% 성장률을 기록하며 지역 성장을 주도합니다. 남아프리카공화국과 이집트의 조립 허브 확대로 아프리카가 6.90%로 뒤를 잇습니다. 북미는 기존 유압식 설비를 대체하는 기술 갱신 주기로 4.5% 성장할 전망이며, 맥콤 카운티만으로도 2024년에는 브레이크 관련 제품의 매출이 1억 30만 달러에 달했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 급속한 전동화가 회생 대응 브레이크 하드웨어로 전환 촉진

- ADAS 보급률 증가로 브레이크 바이 와이어 아키텍처 수요 상승

- 강화된 미국 FMVSS 126 및 UNECE R140 규정으로 ABS/ESC 설치 확대

- 코로나19 이후 전자상거래 급증으로 경상용차(LCV) 브레이크 애프터마켓 확대

- 세계의 BEV 생산 가속화로 저분진 및 무구리 마찰재 필요성 증가

- OEM 보증 기간 연장으로 장수명 세라믹 패드 제형 채택 촉진

- 시장 성장 억제요인

- 희토류 가격 변동성으로 인한 전자식 브레이크 액추에이터 비용 상승

- EU 내 고급 강철 로터 공급망 병목 현상

- 회생 제동으로 인한 마모 감소로 애프터마켓 패드 매출 감소

- 디젤 상용차 생산 감소로 인한 공압식 브레이크 수요 위축

- 밸류체인 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 라이벌 관계의 격렬

제5장 시장 규모와 성장 예측

- 제품 유형별

- 디스크 브레이크

- 드럼 브레이크

- 전동 주차 브레이크

- 회생 브레이크 모듈

- 기술별

- 안티록 브레이크 시스템(ABS)

- 전자식 차체 안정 제어(ESC)

- 트랙션 컨트롤 시스템(TCS)

- 전자식 브레이크 분배(EBD)

- 작동 기구별

- 유압식

- 공압식

- 전자식/브레이크 바이 와이어

- 기계식(케이블)

- 컴포넌트별

- 브레이크 패드 및 슈

- 캘리퍼

- 로터 및 드럼

- 브레이크 부스터 및 마스터 실린더

- 전자 제어 장치 및 액추에이터

- 패드 재료별

- 유기(석면 미사용)

- 반금속

- 금속

- 세라믹

- 판매 채널별

- OEM

- 애프터마켓

- 차량 유형별

- 승용차

- 소형 상용차

- 대형 상용차 및 버스

- 추진별

- 내연기관(ICE) 차량

- 하이브리드 전기자동차(HEV/PHEV)

- 배터리 전기자동차(BEV)

- 연료전지 전기자동차(FCEV)

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 합작사업, 제품 출시)

- 시장 점유율 분석

- 기업 프로파일

- Continental AG

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Brembo SpA

- Akebono Brake Industry Co. Ltd

- Aisin Corporation

- ADVICS Co. Ltd

- Knorr-Bremse AG

- Hyundai Mobis Co. Ltd

- Mando Corporation

- Federal-Mogul Motorparts(Tenneco)

- Hitachi Astemo, Ltd.

- WABCO(ZF CVS)

- Meritor Inc.

- Nissin Kogyo Co. Ltd

- Bendix Commercial Vehicle Systems

- Aptiv PLC

- Haldex AB

- Hella Pagid GmbH

- Carlisle Brake & Friction

제7장 시장 기회와 장래의 전망

HBR 25.11.17The automotive brake system market stood at USD 77.21 billion in 2025 and is forecast to reach USD 92.01 billion by 2030, advancing at a 3.57% CAGR.

The market's growth reflects a steady migration from purely hydraulic setups toward electronically governed architectures that coordinate anti-lock, stability, and regenerative functions in software-defined vehicles. Asia Pacific anchors demand through large-scale electric-vehicle (EV) production and outsourcing of electronic brake assemblies, while the Middle East records the quickest expansion as fleet-modernization policies intersect with infrastructure spending. Technology vendors concentrate on brake-by-wire and low-dust friction materials to comply with UNECE R140 and Euro 7 particulate limits, and light commercial vehicle (LCV) operators lift aftermarket volumes via predictive maintenance programs that cut unplanned downtime.

Global Automotive Brake System Market Trends and Insights

Rapid Electrification Driving Regenerative-Compatible Brake Hardware

Electric-vehicle layouts place more braking torque on traction motors, so friction systems must synchronize seamlessly with software-managed energy recovery. A regenerative kit co-developed by Tevva and ZF captures up to four times more energy than standard air brakes, extending a 7.5-ton truck's range to 140 miles. Mercedes-Benz prototypes embed the brake unit inside the e-drive housing, eliminating rust-prone hardware and reducing particulate emissions. Aisin's cooperative regenerative system further balances hydraulic and motor braking to maintain vehicle stability under all load states.

Heightened ADAS Penetration Raising Demand for Brake-by-Wire

Level-2+ assistance and planned Level-4 autonomy require millisecond actuation that hydraulic linkages cannot guarantee. Bosch's upcoming hydraulic brake-by-wire platform removes mechanical pedal paths yet retains dual fluid circuits for redundancy. ZF has already booked almost 5 million vehicles for its electro-mechanical brake technology that combines integrated brake control and software-defined chassis modules. The semiconductor layer follows suit: Renesas' R-Car X5H system-on-chip uses hardware isolation to protect safety-critical braking domains.

Volatility in Rare-Earth Prices Inflating Electronic Brake Actuator Costs

The U.S. Department of Energy lists neodymium, praseodymium, dysprosium, and terbium as critical materials with concentrated processing in China, exposing brake-by-wire actuators to price swings. Suppliers are diversifying magnet chemistries and seeking non-magnetic motor alternatives, yet near-term cost pressures persist across the automotive brake system market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter FMVSS 126 & UNECE R140 Mandates Boosting ABS/ESC Installations

- Post-COVID E-commerce Surge Increasing LCV Brake Aftermarket

- Reduced Wear in Regenerative Braking Curtailing Aftermarket Pad Revenues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Disc brakes accounted for 63.10% of 2024 revenue, their thermal stability keeping them the default choice in passenger cars and light trucks. The automotive brake system market size for electric parking brakes is projected to expand 5.22% by 2030, driven by space savings and electronic integration that complements ADAS. Brakes India introduced its first electric park brake with a global OEM in 2024, signaling cost-optimized uptake in emerging markets. Drum brakes continue on rear axles where cost is king, while regenerative modules carve a share in battery electric vehicles.

NASA-derived lightweight rotors, now licensed to Orbis Brakes, lower unsprung mass by 42% and improve cooling via wave-shaped vents, an innovation likely to debut in high-performance EVs where every kilogram matters. This cascade of innovations helps the automotive brake system market embrace next-generation materials without sacrificing legacy volumes.

Anti-lock systems held 45.10% market share in 2024, anchoring the safety stack. Electronic stability control, however, is growing at 8.65% CAGR and is already mandated in many regions, positioning it to narrow the gap swiftly. Continental produced more than 1 million electronic brake systems in India during 2024, illustrating scalable economics. TCS and EBD remain complementary, optimizing traction and load balance respectively.

Artificial-intelligence layers are now enhancing classical ABS; Brembo's AI-enabled controller launched in late 2024 anticipates grip losses before wheel lock, confirming that software will differentiate what once was a hardware race. As a result, the automotive brake system market continues to pivot from component supply toward algorithm-driven performance gains.

Hydraulic actuation generated 66.25% of 2024 revenue as its supply chain and service base remain entrenched. Yet brake-by-wire solutions, forecast at a 9.50% CAGR, address autonomous-vehicle latency standards. Bosch's hydraulic brake-by-wire hybrid keeps fluid pathways for redundancy while removing mechanical pedals, offering an evolutionary step for cautious OEMs. Pneumatic systems hold in heavy trucks, and mechanical cables survive in cost-constrained niches.

ZF's bookings for light vehicles confirm the commercial viability of pure electro-mechanical brakes. For the automotive brake system market, this dual track, evolutionary hybrids and revolutionary by-wire, permits staged investment without disrupting existing manufacturing footprints.

The Automotive Brake System Market Report is Segmented by Vehicle Type (Passenger Cars and More), Product Type (Disc Brakes and More), Technology (Anti-Lock Braking System (ABS) and More), Actuation Mechanism (Hydraulic and More), Component (Brake Pads & Shoes and More), Pad Material (Organic and More), Sales Channel, Propulsion, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia Pacific held 58.55% of 2024 revenue, fueled by China's EV rollout and India's electronics assembly scale. Continental alone produced more than 1 million electronic brake systems in India during 2024. Local joint ventures, such as Brakes India-ADVICS, reinforce indigenous technology capability.

Europe contributes mature yet lucrative demand stemming from mandated particulate caps and rapid ESC retrofits. Euro 7's 7 mg/km brake-dust threshold, effective mid-2025, accelerates copper-free material adoption and low-drag calipers. Nordic nations also post a robust 5% CAGR as EV penetration fosters regenerative-ready systems.

The Middle East leads regional growth at an 8.90% CAGR through 2030, powered by Vision 2030 infrastructure programs in Saudi Arabia and transport diversification in the UAE. Africa follows at 6.90% due to growing assembly hubs in South Africa and Egypt. North America advances at 4.5% as technology refresh cycles replace legacy hydraulic setups; Macomb County alone tallied USD 100.3 million in brake-specific sales in 2024

- Continental AG

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Brembo S.p.A

- Akebono Brake Industry Co. Ltd

- Aisin Corporation

- ADVICS Co. Ltd

- Knorr-Bremse AG

- Hyundai Mobis Co. Ltd

- Mando Corporation

- Federal-Mogul Motorparts (Tenneco)

- Hitachi Astemo, Ltd.

- WABCO (ZF CVS)

- Meritor Inc.

- Nissin Kogyo Co. Ltd

- Bendix Commercial Vehicle Systems

- Aptiv PLC

- Haldex AB

- Hella Pagid GmbH

- Carlisle Brake & Friction

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Electrification Driving Shift to Regenerative-Compatible Brake Hardware

- 4.2.2 Heightened ADAS Penetration Raising Demand for Brake-by-Wire Architectures

- 4.2.3 Stricter U.S. FMVSS 126 & UNECE R140 Mandates Boosting ABS/ESC Installations

- 4.2.4 Post-COVID E-commerce Surge Increasing LCV Brake Aftermarket

- 4.2.5 Accelerating Global BEV Production Necessitating Low-Dust, Copper-Free Friction Materials

- 4.2.6 OEM Warranty Extensions Driving Adoption of Long-Life Ceramic Pad Formulations

- 4.3 Market Restraints

- 4.3.1 Volatility in Rare-earth Prices Inflating Electronic Brake Actuator Costs

- 4.3.2 Supply-chain Bottlenecks for High-grade Steel Rotors in EU

- 4.3.3 Reduced Wear in Regenerative Braking Curtailing Aftermarket Pad Revenues

- 4.3.4 Declining Diesel CV Production Dampening Pneumatic Brake Demand

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Product Type

- 5.1.1 Disc Brakes

- 5.1.2 Drum Brakes

- 5.1.3 Electric Parking Brakes

- 5.1.4 Regenerative Braking Modules

- 5.2 By Technology

- 5.2.1 Anti-lock Braking System (ABS)

- 5.2.2 Electronic Stability Control (ESC)

- 5.2.3 Traction Control System (TCS)

- 5.2.4 Electronic Brake-force Distribution (EBD)

- 5.3 By Actuation Mechanism

- 5.3.1 Hydraulic

- 5.3.2 Pneumatic

- 5.3.3 Electromagnetic / Brake-by-Wire

- 5.3.4 Mechanical (Cable)

- 5.4 By Component

- 5.4.1 Brake Pads & Shoes

- 5.4.2 Calipers

- 5.4.3 Rotors & Drums

- 5.4.4 Brake Boosters & Master Cylinders

- 5.4.5 Electronic Control Units & Actuators

- 5.5 By Pad Material

- 5.5.1 Organic (Non-Asbestos)

- 5.5.2 Semi-Metallic

- 5.5.3 Metallic

- 5.5.4 Ceramic

- 5.6 By Sales Channel

- 5.6.1 Original Equipment Manufacturers (OEM)

- 5.6.2 Aftermarket

- 5.7 By Vehicle Type

- 5.7.1 Passenger Cars

- 5.7.2 Light Commercial Vehicles

- 5.7.3 Heavy Commercial Vehicles & Buses

- 5.8 By Propulsion

- 5.8.1 Internal Combustion Engine (ICE) Vehicles

- 5.8.2 Hybrid Electric Vehicles (HEV/PHEV)

- 5.8.3 Battery Electric Vehicles (BEV)

- 5.8.4 Fuel-Cell Electric Vehicles (FCEV)

- 5.9 By Geography

- 5.9.1 North America

- 5.9.1.1 United States

- 5.9.1.2 Canada

- 5.9.1.3 Rest of North America

- 5.9.2 South America

- 5.9.2.1 Brazil

- 5.9.2.2 Argentina

- 5.9.2.3 Rest of South America

- 5.9.3 Europe

- 5.9.3.1 Germany

- 5.9.3.2 United Kingdom

- 5.9.3.3 France

- 5.9.3.4 Italy

- 5.9.3.5 Spain

- 5.9.3.6 Rest of Europe

- 5.9.4 Asia Pacific

- 5.9.4.1 China

- 5.9.4.2 India

- 5.9.4.3 Japan

- 5.9.4.4 South Korea

- 5.9.4.5 Rest of Asia Pacific

- 5.9.5 Middle East and Africa

- 5.9.5.1 Saudi Arabia

- 5.9.5.2 United Arab Emirates

- 5.9.5.3 Turkey

- 5.9.5.4 South Africa

- 5.9.5.5 Egypt

- 5.9.5.6 Rest of Middle East and Africa

- 5.9.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JV, Product Launches)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Robert Bosch GmbH

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Brembo S.p.A

- 6.4.5 Akebono Brake Industry Co. Ltd

- 6.4.6 Aisin Corporation

- 6.4.7 ADVICS Co. Ltd

- 6.4.8 Knorr-Bremse AG

- 6.4.9 Hyundai Mobis Co. Ltd

- 6.4.10 Mando Corporation

- 6.4.11 Federal-Mogul Motorparts (Tenneco)

- 6.4.12 Hitachi Astemo, Ltd.

- 6.4.13 WABCO (ZF CVS)

- 6.4.14 Meritor Inc.

- 6.4.15 Nissin Kogyo Co. Ltd

- 6.4.16 Bendix Commercial Vehicle Systems

- 6.4.17 Aptiv PLC

- 6.4.18 Haldex AB

- 6.4.19 Hella Pagid GmbH

- 6.4.20 Carlisle Brake & Friction

7 Market Opportunities & Future Outlook

- 7.1 Integration of IoT & Predictive Maintenance Platforms

- 7.2 Next-Gen Solid-state Brake-by-Wire for Level-4 Autonomy

- 7.3 Copper-free Pad Mandates Creating Material Innovation Space

- 7.4 Lightweight Carbon-Ceramic Discs for High-Performance EVs