|

시장보고서

상품코드

1850984

운송 관리 시스템 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Transportation Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

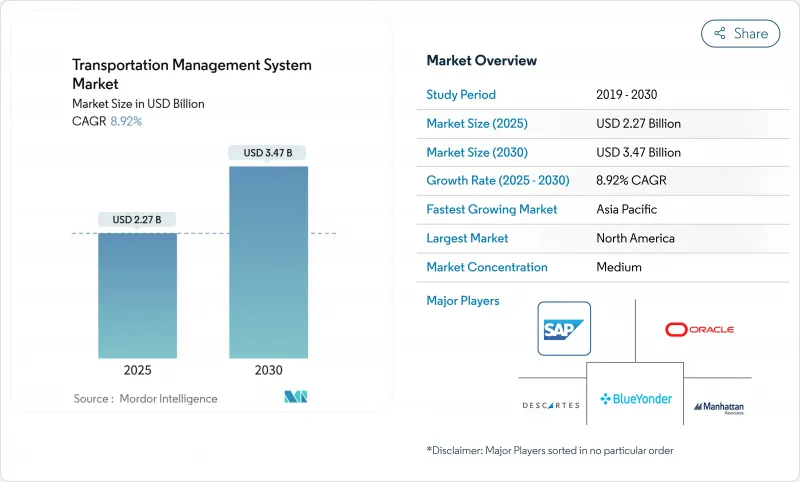

운송 관리 시스템 시장의 규모는 2025년에 22억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 8.92%로, 2030년에는 34억 7,000만 달러에 달할 것으로 예측됩니다.

이 가속은 기업이 자본 부담이 큰 On-Premise 도구를 도입이 빠르고, 총 소유 비용을 절감하며, 실시간 업무 시각화를 실현하는 확장성이 높은 클라우드 플랫폼으로 대체하면서 발생합니다. 전자 자동 기록장치(ELD)와 온실가스 보고에 관한 규제의 의무화에 의해 컴플라이언스 데이터가 전략적 인텔리전스로 바뀌고 있는 반면, E-Commerce의 성장에 의해 정교한 라스트 원마일과 복합 일관 운송 최적화에 대한 수요가 높아지고 있습니다. 화물 마켓플레이스의 통합으로 화주가 스팟 용량을 즉시 확보할 수 있게 되었고, AI를 활용한 ETA 엔진은 반환지연료를 줄이고 지속가능성 목표가 엄격해지는 가운데 공급망의 서비스 수준을 올리고 있습니다.

세계의 운송 관리 시스템 시장의 동향과 인사이트

클라우드 기반 TMS 배포로 비용 절감 가속화

클라우드 배포는 하드웨어 및 IT 오버헤드를 줄이고 레거시 시스템에 비해 총 소유 비용을 30% 절감합니다. 운송 데이터를 시설 간에 실시간으로 동기화하여 중앙 집중식 시각화 및 신속한 예외 관리를 제공합니다. 마이크로서비스 아키텍처를 사용하면 발송인이 모듈을 단계적으로 활성화할 수 있으므로 대규모 롤아웃 위험을 피할 수 있습니다. 공급업체는 기술 비용과 화물량을 일치시키는 구독 가격을 제공하며, 내장 AI는 지속가능성 목표를 따르는 저탄소 경로를 제안합니다. 이러한 요인들로부터 클라우드는 새로운 운송 관리 시스템 시장 도입의 기본 아키텍처로 자리매김하고 있습니다.

전자상거래와 옴니채널 소매업에서는 라스트 마일의 실시간 최적화가 요구됩니다.

당일 배송이나 익일 배송에 대한 기대에 의해 루트 계획은 정적에서 동적으로 변화하고 있습니다. 최신 TMS 엔진은 트래픽, 날씨 및 운송 회사의 용량 데이터를 수분마다 캡처하고, 드라이버를 다시 라우팅하고, 고객에 대한 경고를 자동화합니다. 라스트 원마일의 비용은 전체 배송비의 53%에 달할 수 있으며, AI를 활용한 최적화에 의해 통합 오더 오케스트레이션 플랫폼으로 전환하는 소매 기업은 그 부담을 경감하고 있습니다. 고급 지오펜싱은 커브사이드 픽업과 매장 간 배달을 지원하며, 예측 ETA는 실패 없는 배달 성공을 뒷받침하며 NPS 점수와 수익 유지율을 높입니다.

레거시 ERP/WMS 스택과의 높은 통합 비용

기업은 종종 최신 API가 없는 고도로 맞춤화된 ERP 및 WMS 플랫폼을 사용하므로 TMS 통합 프로젝트는 6-18개월, 예산은 50만-500만 달러로 예상됩니다. 데이터 마이그레이션은 일관성이 없는 형식과 오래된 비즈니스 로직의 발견과 대규모 클렌징을 필요로 합니다. 시스템의 병행 가동은 가동 사이클을 길게 하고 미들웨어의 레이어는 라이선스료를 증가시킵니다. 이러한 장애물은 ROI를 늦추고 특히 다운타임 위험이 높은 자본 집약형 제조업에서는 업그레이드를 지연시킵니다.

부문 분석

2024년 운송 관리 시스템 시장수익의 58%는 도로화물운송이 차지하였습니다. 만재 트럭 및 혼적 화물 적재를 위한 TMS 모듈은 차선 가격, 백홀 충전 및 잔여 회피를 최적화합니다. 인터모달 커넥터는 트럭 구간과 철도 램프를 동기화하여 네트워크 민첩성을 강화합니다. CAGR 12.8%를 기록한 항공 분야는 전자상거래의 크로스보더 택배와 고액 화물 증가를 반영하고 있습니다. AI를 활용한 적재 계획은 화물 공간 이용 부족을 줄이고 실시간 이정표 추적을 통해 주요 허브 공항에서의 체류 요금을 줄일 수 있습니다. 예측 분석이 화물 터미널에서 슬롯 예약을 개선함에 따라, 발송인은 재고 속도와 서비스 약속의 균형을 이루는 안정적인 옵션을 프리미엄 비용에 얻을 수 있습니다.

도로 기반 솔루션으로 인한 운송 관리 시스템 시장의 규모는 상세한 여행 가시성을 필요로 하는 저배출 구역으로의 규제 강화와 함께 확대될 것으로 예측됩니다. 반대로 항공화물 최적화 플랫폼은 날씨 분석과 슬롯 재스케줄링 기능을 통합하여 서비스 중단 위험을 억제합니다. 해운과 철도는 벌크 운송 전용 사용자 기반을 유지하지만, 벤더는 컨테이너 가시성 데이터와 기차 일정을 통합하고 단일 TMS 내에서 진정한 종단 간 오케스트레이션을 구축하고 있습니다. 이러한 변화는 운송 관리 시스템 시장이 기술적 범위를 확대함에 따라 모든 운송 형태가 차별화된 가치에 기여할 수 있도록 합니다.

클라우드는 2024년에 운송 관리 시스템 시장의 63% 점유율을 획득했으며, 8주 이내에 완료되는 경우가 많고 빠른 온보딩 사이클을 배경으로 CAGR 14.92%의 기세를 보이고 있습니다. 구독 모델을 통해 설비 투자를 운영 비용으로 전환하고 예측 ETA 및 자동화물 감사와 같은 고급 모듈에 예산을 부과할 수 있습니다. API 우선 설계는 운송 회사 포털, IoT 비콘, 분석 엔진과 쉽게 연결하고 사용자의 요구에 따라 진화하는 확장 가능한 생태계를 형성합니다. On-Premise는 데이터 저장이 엄격하게 의무화된 섹터에서 살아나고 있지만, 하이브리드 실적은 민감한 데이터를 방화벽으로 보호하면서 대량의 최적화 작업을 클라우드에 푸시함으로써 그 격차를 메우고 있습니다.

클라우드의 민주화 효과는 소규모 화주들 사이에서 가장 두드러집니다. 중소기업은 하드웨어 구매나 IT 전문 팀 없이 엔터프라이즈급 최적화를 조달할 수 있게 되어 이 부문의 CAGR을 15% 밀어 올렸습니다. 중소기업에 특화된 SaaS 운송 관리 시스템 시장의 규모는 2025년부터 2030년에 걸쳐 두배로 증가할 것으로 예상되며 클라우드가 각 지역에서 기본 도입 패러다임으로 강화됩니다.

운송 관리 시스템 시장은 운송 수단(도로, 철도 등), 도입 형태(On-Premise, 클라우드, 하이브리드), 기업 규모, 최종 사용자 산업(제조, 소매, 전자상거래 등), 구성 요소, 용도(수주 관리, 실시간 시각화 및 추적 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 2024년 운송 관리 시스템 시장 매출의 38%를 차지했으며, 클라우드 물류 제품군의 조기 도입과 ELD 의무화 등의 규제 강화에 지지를 받았습니다. 미국 운송업체는 성숙한 운송 회사 네트워크와 상세한 운임 기반 데이터를 활용하여 최적화 시나리오를 강화합니다. 캐나다는 미국과의 국경을 넘어서는 무역으로 커스텀 대응 워크플로에 대한 수요가 높아지는 한편, 멕시코는 니어 쇼어링의 동향으로부터 혜택을 받고, 제조업체 각사는 운송 경로의 신속한 디지털화를 추진하고 있습니다.

아시아태평양은 중국, 인도, 동남아시아에서 전자상거래량이 급증하면서 2030년까지 연평균 복합 성장률(CAGR) 13.9%로 성장할 전망입니다. 중국의 택배 네트워크는 도시 리드 타임을 2시간 미만으로 절감하는 AI 루트 시퀀서에 의존합니다. 인도의 제조업은 TMS를 채용하여 단편화한 인프라를 횡단하는 복합 운송을 오케스트레이션 하고 비용과 서비스의 밸런스를 유지합니다. 일본의 Society 5.0 청사진은 공장 센서와 운송 회사 네트워크를 통합하는 IoT 리치 로지스틱스 투자에 박차를 가해 운송 관리 시스템 시장을 더욱 확대시킵니다.

유럽은 엄격한 지속가능성 지침과 복잡한 국경을 넘어선 무역규칙에 따라 주목할만한 점유율을 차지하고 있습니다. 독일 수출업체는 입찰 엔진에 CO2 계산기를 통합하고, 프랑스 소매업체는 혼잡한 수수료를 줄이기 위해 멀티모달 TMS를 도입했으며 영국 운송인은 브렉시트 후 고급 세관 심사가 필요합니다. 중동 및 아프리카에서는 항만 확장과 자유 무역 지역이 확대됨에 따라 TMS 이용이 증가하고 있습니다. 한편 남미에서는 전자상거래 확대와 인프라 근대화로 운송관리시스템 시장 침투를 위한 새로운 길이 열리고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 클라우드 기반 TMS 도입으로 서비스 비용 절감 가속

- 전자상거래와 옴니채널 소매업에서 실시간 마일 최적화를 요구하고 있음

- ELD와 온실가스보고의 규제 강화에 의해 화물의 디지털화가 진행됨

- 화물 시장의 융합에 의해 동적인 용량 조달이 가능해짐

- AI 구동형 도착 예정 시각 예측 툴이 반환지연/SLA 페널티를 절감

- API 퍼스트의 마이크로 서비스가 중소기업용 모듈형 TMS를 실현

- 시장 성장 억제요인

- 기존 ERP/WMS 스택과의 통합 비용이 높음

- 클라우드 도입에 있어서의 데이터 보안과 프라이버시의 우려

- 분석 모듈을 활용하기 위한 사내 데이터 사이언스 인력 부족

- 단편화된 캐리어 텔레매틱스 규격이 멀티 모달인 가시성을 저해

- 가치/공급망 분석

- 규제 상황

- 기술 전망(AI, IoT, 5G, API 기반 생태계)

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 운송수단별

- 육로

- 철도

- 항공

- 선박

- 전개별

- On-Premise

- 클라우드

- 하이브리드

- 기업 규모별

- 대기업

- 중소기업

- 마이크로 기업

- 최종 사용자 업계별

- 제조업

- 소매업 및 전자상거래

- 식음료

- 헬스케어 및 의약품

- 자동차

- 3PL 및 물류 서비스 제공업체

- 컴포넌트별

- 소프트웨어

- 서비스

- 컨설팅

- 통합 및 구현

- 지원 및 유지 보수

- 용도별

- 주문 관리

- 루트 계획 및 최적화

- 화물 감사 및 지불

- 실시간 가시성 및 추적

- 재고와 창고의 통합

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 자금 조달, 파트너십)

- 시장 점유율 분석

- 기업 프로파일

- SAP SE

- Oracle Corp.

- Blue Yonder(JDA)

- Descartes Systems Group

- Manhattan Associates

- MercuryGate International

- Trimble Transportation

- E2open

- Project44

- Transplace(Uber Freight)

- Infor Nexus

- Kinaxis Inc.

- CH Robinson

- BluJay Solutions(E2open)

- CargoSmart Ltd.

- 3Gtms Inc.

- Alpega Group

- Cloud Logistics by E2open

- Kuebix(Trimble)

- WiseTech Global(CargoWise TMS)

제7장 시장 기회와 미래 전망

CSM 25.11.20The Transportation Management System Market size is estimated at USD 2.27 billion in 2025, and is expected to reach USD 3.47 billion by 2030, at a CAGR of 8.92% during the forecast period (2025-2030).

The acceleration stems from enterprises replacing capital-heavy on-premises tools with scalable cloud platforms that deliver rapid deployment, lower total cost of ownership, and real-time operational visibility. Regulatory mandates for electronic logging devices (ELDs) and greenhouse-gas reporting are turning compliance data into strategic intelligence, while e-commerce growth amplifies demand for sophisticated last-mile and multimodal optimisation. Freight-marketplace integrations now let shippers secure spot capacity on the fly, and AI-driven ETA engines reduce detention penalties, lifting supply-chain service levels even as sustainability targets tighten.

Global Transportation Management System Market Trends and Insights

Cloud-based TMS adoption accelerates cost-to-serve savings

Cloud deployments cut hardware and IT overhead, trimming total cost of ownership by 30% compared with legacy systems. They synchronise shipment data across facilities in real time, yielding centralised visibility and rapid exception management. Microservices architecture lets shippers activate modules incrementally, avoiding the risk of big-bang rollouts. Vendors offer subscription pricing that aligns technology costs with freight volumes, while embedded AI suggests lower-carbon routes that align with sustainability targets. These factors position cloud as the default architecture for new transportation management system market implementations.

E-commerce & omnichannel retail demand real-time last-mile optimization

Same-day and next-day delivery expectations have moved route planning from static to dynamic. Modern TMS engines ingest traffic, weather, and carrier capacity data every few minutes, rerouting drivers and automating customer alerts. Last-mile costs can reach 53% of total shipping spend, and AI-enabled optimisation is cutting that burden for retailers that pivot to unified order orchestration platforms. Advanced geofencing supports curb side pickup and store-to-door fulfilment, while predictive ETAs boost first-attempt delivery success, raising NPS scores and revenue retention.

High integration cost with legacy ERP/WMS stacks

Enterprises often run heavily customised ERP and WMS platforms that lack modern APIs, pushing TMS integration projects to 6-18 months and budgets from USD 500,000 to USD 5 million. Data migration uncovers inconsistent formats and outdated business logic, requiring extensive cleansing. Parallel system runs prolong go-live cycles, and middleware layers add licence fees. These hurdles delay ROI and deter some organisations from upgrading, especially in capital-intensive manufacturing where downtime risks are high.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory push for ELD & greenhouse-gas reporting digitalizes freight

- Freight-marketplace convergence enables dynamic capacity procurement

- Data-security & privacy concerns for cloud deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Road freight delivered 58% of transportation management system market revenue in 2024 thanks to its ubiquity in last-mile and regional haulage. TMS modules for truckload and less-than-truckload optimise lane pricing, back-haul filling, and detention avoidance. Intermodal connectors allow truck legs to synchronise with rail ramps, strengthening network agility. The airway segment, posting 12.8% CAGR, underscores the rise of e-commerce cross-border parcels and high-value cargo. AI-based load-planning cuts under-utilisation in belly space, and real-time milestone tracking mitigates dwell fees at major hubs. As predictive analytics refine slot booking at cargo terminals, shippers gain a premium-cost yet high-reliability option that balances inventory velocity with service promises.

The transportation management system market size attributed to road-based solutions is forecast to grow alongside regulatory pushes for lower emissions zones that require granular trip visibility. Conversely, air-cargo optimisation platforms integrate weather analytics and slot rescheduling features to contain service-disruption risk. While maritime and rail retain dedicated user bases for bulk moves, vendors are integrating container visibility data and train schedules to build true end-to-end orchestration inside a single TMS cockpit. These shifts ensure every mode contributes differentiated value as the transportation management system market widens its technological scope.

Cloud captured 63% transportation management system market share in 2024 and is on track for 14.92% CAGR on the back of rapid onboarding cycles that often conclude within eight weeks. Subscription pricing converts capex to opex, freeing budget for advanced modules such as predictive ETAs and automated freight audit. API-first design links easily with carrier portals, IoT beacons, and analytics engines, forming an extensible ecosystem that evolves with user needs. On-premise persists in sectors with strict data residency mandates, though hybrid footprints are bridging that gap by retaining sensitive data behind the firewall while pushing high-volume optimisation jobs to the cloud.

Cloud's democratisation effect is most visible among smaller shippers. SMEs can now procure enterprise-grade optimisation without hardware spend or specialist IT teams, driving 15% CAGR in the segment. The transportation management system market size for SME-focused SaaS is expected to double between 2025 and 2030, reinforcing cloud's status as the default deployment paradigm across regions.

Transportation Management System Market is Segmented by Mode of Transporation (Roadways, Railways and More), Deployment (On-Premise, Cloud and Hybrid), Enterprise Size, End-User Industry (Manufacturing, Retail and E-Commerce, and More), Component, Application (Order Management, Real-Time Visibility and Tracking and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38% of transportation management system market revenue in 2024, underpinned by early adoption of cloud logistics suites and regulatory catalysts like ELD mandates. United States shippers leverage mature carrier networks and detailed rate-base data to refine optimisation scenarios. Canada's cross-border trade with the US boosts demand for customs-ready workflows, while Mexico benefits from nearshoring trends that push manufacturers to digitise freight corridors quickly.

Asia-Pacific leads growth at 13.9% CAGR to 2030 as e-commerce volumes soar across China, India, and Southeast Asia. Chinese parcel networks rely on AI route sequencers that compress urban lead times to under two hours. Indian manufacturers adopt TMS to orchestrate multimodal moves across fragmented infrastructure, balancing cost and service. Japan's Society 5.0 blueprint spurs investments in IoT-rich logistics that integrate factory sensors with carrier networks, further enlarging the transportation management system market.

Europe commands a notable share owing to stringent sustainability directives and complex cross-border trade rules. German exporters integrate CO2 calculators into tendering engines, French retailers deploy multimodal TMS to cut congestion charges, and UK shippers post-Brexit need advanced customs screening. Middle East and Africa witness incremental uptake aligned with port expansions and free-trade zones, whereas South America's growing e-commerce and infrastructure modernisation open fresh lanes for transportation management system market penetration.

- SAP SE

- Oracle Corp.

- Blue Yonder (JDA)

- Descartes Systems Group

- Manhattan Associates

- MercuryGate International

- Trimble Transportation

- E2open

- Project44

- Transplace (Uber Freight)

- Infor Nexus

- Kinaxis Inc.

- C.H. Robinson

- BluJay Solutions (E2open)

- CargoSmart Ltd.

- 3Gtms Inc.

- Alpega Group

- Cloud Logistics by E2open

- Kuebix (Trimble)

- WiseTech Global (CargoWise TMS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-based TMS adoption accelerates cost-to-serve savings

- 4.2.2 E-commerce & omnichannel retail demand real-time, last-mile optimisation

- 4.2.3 Regulatory push for ELD & Green-house-gas reporting digitalises freight

- 4.2.4 Freight-marketplace convergence enables dynamic capacity procurement

- 4.2.5 AI-driven predictive ETA tools cut detention/SLA penalties

- 4.2.6 API-first micro-services unlock modular TMS for SMEs

- 4.3 Market Restraints

- 4.3.1 High integration cost with legacy ERP/WMS stacks

- 4.3.2 Data-security and privacy concerns for cloud deployments

- 4.3.3 Shortage of in-house data-science talent to exploit analytics modules

- 4.3.4 Fragmented carrier-telematics standards hinder multimodal visibility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (AI, IoT, 5G, API-based ecosystems)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Transportation

- 5.1.1 Roadways

- 5.1.2 Railways

- 5.1.3 Airways

- 5.1.4 Maritime

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small & Medium Enterprises

- 5.3.3 Micro Enterprises

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-commerce

- 5.4.3 Food and Beverage

- 5.4.4 Healthcare and Pharmaceuticals

- 5.4.5 Automotive

- 5.4.6 3PL and Logistics Service Providers

- 5.5 By Component

- 5.5.1 Software

- 5.5.2 Services

- 5.5.2.1 Consulting

- 5.5.2.2 Integration and Implementation

- 5.5.2.3 Support and Maintenance

- 5.6 By Application

- 5.6.1 Order Management

- 5.6.2 Route Planning and Optimization

- 5.6.3 Freight Audit and Payment

- 5.6.4 Real-time Visibility and Tracking

- 5.6.5 Inventory and Warehouse Integration

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 Middle East

- 5.7.4.1.1 Israel

- 5.7.4.1.2 Saudi Arabia

- 5.7.4.1.3 United Arab Emirates

- 5.7.4.1.4 Turkey

- 5.7.4.1.5 Rest of Middle East

- 5.7.4.2 Africa

- 5.7.4.2.1 South Africa

- 5.7.4.2.2 Egypt

- 5.7.4.2.3 Rest of Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, funding, partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 SAP SE

- 6.4.2 Oracle Corp.

- 6.4.3 Blue Yonder (JDA)

- 6.4.4 Descartes Systems Group

- 6.4.5 Manhattan Associates

- 6.4.6 MercuryGate International

- 6.4.7 Trimble Transportation

- 6.4.8 E2open

- 6.4.9 Project44

- 6.4.10 Transplace (Uber Freight)

- 6.4.11 Infor Nexus

- 6.4.12 Kinaxis Inc.

- 6.4.13 C.H. Robinson

- 6.4.14 BluJay Solutions (E2open)

- 6.4.15 CargoSmart Ltd.

- 6.4.16 3Gtms Inc.

- 6.4.17 Alpega Group

- 6.4.18 Cloud Logistics by E2open

- 6.4.19 Kuebix (Trimble)

- 6.4.20 WiseTech Global (CargoWise TMS)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment